Kriptovalutni trg deluje na bifurcirani strukturi, ki loči maloprodajne udeležence od kapitalskih sredstev v velikem obsegu institucionalnih vlagateljev. Medtem ko posamezni trgovci običajno komunicirajo z uporabniku prijaznimi vmesniki borz, institucionalni vlagatelji krmarijo po popolnoma drugačnem ekosistemu, zasnovanem za visok volumen in zasebnost. Razumevanje razlike med tema dvema okoljema je bistveno za razumevanje tega, kako likvidnost digitalnih sredstev deluje globalno. Infrastruktura, ki podpira trgovanje za sto dolarjev, se fundamentalno razlikuje od sistemov, potrebnih za premik sto milijonov dolarjev brez zrušitve trga.

Maloprodajne borze služijo kot vidno obličje kripto industrije. Zagotavljajo javne knjige naročil, kjer se naročila za nakup in prodajo ujemajo v realnem času. Te platforme dajejo prednost dostopnosti in enostavni uporabi. Nasprotno pa institucionalne trgovalne mize, pogosto imenovane OTC (Over-the-Counter) mize, delujejo v senci javnega trga. Omogočajo neposredne transakcije med dvema strankama, pogosto popolnoma obidejo javne knjige naročil. Ta segregacija zagotavlja, da masovni pretoki kapitala ne motijo cenovne stabilnosti širšega trga.

The Mechanics of Retail Exchanges

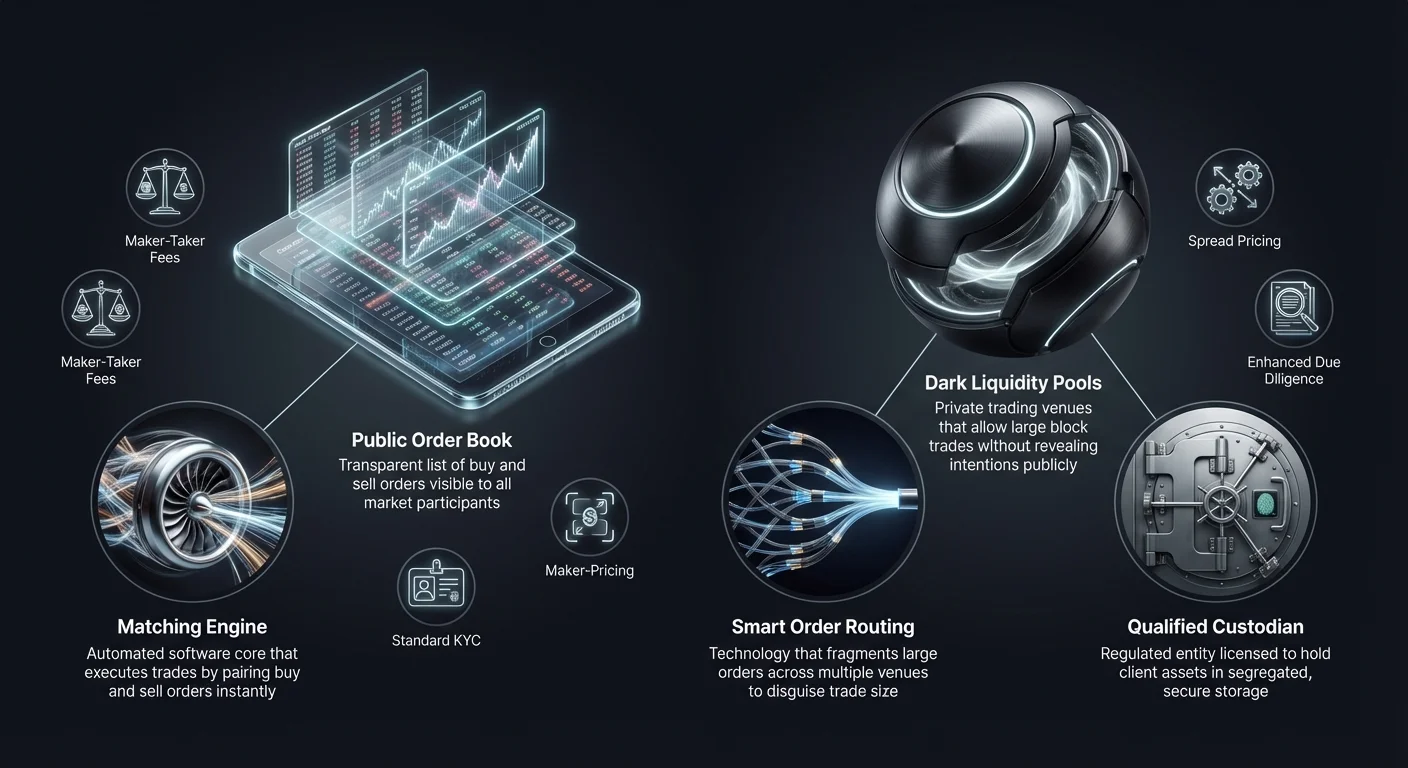

Retail cryptocurrency exchanges function similarly to traditional stock brokerages but with distinct operational nuances. They act as intermediaries that hold customer funds and facilitate trading through a central limit order book. When a user places a market order, the exchange's matching engine pairs it with the best available limit order from other users. This process creates immediate liquidity for small to medium-sized trades. The visibility of the order book allows traders to see market depth, which represents the volume of buy and sell orders at various price levels.

Order Book Dynamics

The central component of a retail exchange is the public order book. It displays a transparent list of diverse market participants willing to buy or sell assets at specific prices. This transparency is beneficial for price discovery, as it allows all participants to view the current market sentiment and supply-demand balance. However, this visibility becomes a liability for large trades. If a trader attempts to sell a massive amount of Bitcoin on a public order book, other market participants may react instantly, driving the price down before the trade completes.

Matching Engines and Latency

Retail platforms compete heavily on the speed and efficiency of their matching engines. A matching engine is the software core that maintains the order book and executes trades. For retail traders, speed is often a matter of convenience or basic strategy execution. High-performance engines ensure that users experience minimal delay between clicking "buy" and receiving their assets. This infrastructure is designed to handle thousands of small transactions per second rather than a single, massive, complex block trade.

Accessibility and User Interface

The primary goal of retail exchange infrastructure is lowering the barrier to entry. Platforms integrate fiat payment gateways, allowing users to deposit government currency via bank transfers or credit cards. The user interface is designed to be intuitive, often shielding the user from the complexities of blockchain settlements. While this simplifies the experience, it often means the user does not have direct control over the private keys during the trading process. The infrastructure prioritizes connectivity and user experience over the bespoke privacy needs of larger entities.

Institutional OTC Trading Architecture

Institutional trading desks operate on a premise of discretion and liquidity aggregation. OTC trading involves the direct exchange of assets between two counterparties, often facilitated by a specialized desk or broker. This method is the standard for high-net-worth individuals, hedge funds, and corporate treasuries looking to enter or exit large positions. The infrastructure here does not rely on a single public order book but rather on a network of liquidity providers and private communication channels.

Minimizing Market Impact

The primary objective of an institutional OTC desk is to minimize market impact. When a large buy order hits a public exchange, it can cause "slippage," where the price increases as the buyer consumes all available sell orders at lower prices. OTC desks mitigate this by locking in a price for the entire block. The desk takes on the risk of acquiring the assets and delivers them to the client at the agreed-upon rate. This ensures the institutional buyer does not accidentally drive the price up against themselves while trying to fill a position.

Smart Order Routing (SOR)

Sophisticated institutional platforms utilize Smart Order Routing technology to source liquidity. Instead of relying on a single exchange, an SOR connects to multiple liquidity pools, other OTC desks, and various exchanges simultaneously. It breaks a large order into smaller fragments and executes them across different venues intelligently. This fragmentation disguises the true size of the trade and prevents high-frequency traders on public exchanges from front-running the institutional order.

Principal vs. Agency Trading

Institutional desks typically operate under either a principal or agency model. In a principal model, the desk uses its own capital to buy the asset from the client or sell it to them. They act as the direct counterparty and take on market risk. In an agency model, the desk acts strictly as an intermediary, finding a counterparty on behalf of the client without using their own balance sheet. The choice of model affects the pricing structure and the speed of settlement, as principal trading often offers faster execution at a slightly higher cost.

Comparative Fee Models

The revenue models for retail exchanges and institutional desks differ significantly. Retail platforms typically rely on a transparent fee schedule based on trading volume. This often involves a "maker-taker" model. A "maker" who provides liquidity to the order book by placing a limit order pays a lower fee. A "taker" who removes liquidity by executing a market order pays a higher fee. These fees are usually a percentage of the total transaction value and are explicitly charged on top of the trade price.

Spread-Based Pricing in OTC

Institutional OTC desks rarely charge a separate commission fee. Instead, they utilize a "spread" or "all-in" pricing model. When a client asks for a quote to buy Bitcoin, the desk provides a price that is slightly higher than the current market rate. The difference between the market rate and the quoted price is the spread, which represents the desk's profit margin. This allows institutions to execute large trades with a single, predictable cost known upfront, simplifying accounting and cost analysis for the firm.

Zero-Fee Marketing vs. Reality

Some retail platforms and swap services market themselves as "zero-fee" exchanges. In reality, these platforms often adopt the institutional spread model for retail users. While no commission line item appears on the trade receipt, the price the user pays for the asset is slightly inflated compared to the raw market spot price. This approach simplifies the user experience by removing complex fee calculations, but it requires traders to be vigilant about the exchange rate they are accepting to ensure it remains competitive.

Volume Tiering Economics

Both retail and institutional environments offer incentives for high volume, but the mechanics differ. Retail exchanges use tiered systems where fees drop as 30-day trading volume increases. This encourages frequent trading and loyalty to a single platform. Institutional pricing is more dynamic and negotiable. A desk may offer a tighter spread for a specific trade if the market conditions are favorable or if the desk needs to offload inventory. The pricing relationship in the OTC world is often relational rather than algorithmic.

Liquidity and Slippage Analysis

Liquidity refers to the ease with which an asset can be converted into cash or another asset without affecting its price. In the context of crypto infrastructure, liquidity is the defining factor that separates retail and institutional venues. Retail exchanges rely on the "depth" of their order book. If the order book is thin, even a moderate trade can cause significant price movement. Institutional desks access "deep" liquidity, often sourced from miners, early adopters, or other institutions, allowing them to absorb selling pressure that would capsize a retail order book.

| Feature | Retail Exchange | Institutional OTC Desk |

|---|---|---|

| Primary Liquidity | Public Order Book | Private Networks/Pools |

| Price Discovery | Transparent/Real-time | Opaque/Negotiated |

| Slippage Risk | High for large volume | Minimal (Fixed Price) |

Understanding Slippage

Slippage is the difference between the expected price of a trade and the price at which the trade is executed. On a retail exchange, slippage occurs during times of high volatility or low liquidity. If a trader initiates a market buy order for 10 BTC, but the lowest sell orders only total 5 BTC, the matching engine will continue buying at higher and higher prices until the order is filled. This results in an average entry price significantly higher than the initial market display.

OTC Liquidity Pools

OTC desks create a buffer against slippage by utilizing liquidity pools that are not visible to the public. These dark pools allow institutions to trade large blocks without signaling their intentions to the broader market. By keeping these transactions private until they are settled, the desk prevents panic selling or FOMO (Fear Of Missing Out) buying that typically follows the revelation of a "whale" movement on a public blockchain explorer or exchange feed.

Settlement Impact

The speed of settlement also impacts liquidity. In retail trading, settlement is usually instant within the exchange's internal ledger. The user sees the balance update immediately. In institutional OTC, settlement may be delayed (T+1 or same-day wire deadlines). However, the price is locked at the moment of the trade agreement. This separation of trade execution and final settlement allows institutions to manage cash flow and liquidity without the immediate pressure of pre-funding every single transaction on a public venue.

Custody and Security Infrastructure

Security infrastructures for retail and institutional platforms are vastly different due to the scale of assets involved. Retail exchanges typically use a mix of hot (online) and cold (offline) wallets to manage user funds. The hot wallet handles immediate withdrawals and trading liquidity, while the majority of assets are kept in cold storage. However, retail users generally rely on the exchange's internal security protocols and do not have segregated on-chain accounts.

Qualified Custodians

Institutional clients often require the use of a "Qualified Custodian." This is a regulatory designation for entities licensed to hold client assets. Institutional infrastructure separates the trading venue from the custody provider. This segregation of duties ensures that even if the trading desk faces insolvency, the client's assets remain safe in a segregated vault. Coinbase Institutional, for example, safeguards billions in assets using this segregated model, providing a layer of trust essential for corporate governance.

Cold Storage Protocols

For high-volume OTC desks and institutional custodians, cold storage involves complex physical and digital security measures. This often includes multi-signature wallets where private keys are divided and stored in geographically dispersed, secure locations. Executing a transaction from these vaults requires multiple authorized personnel to sign off, often with time delays. This contrasts sharply with retail security, which usually relies on 2FA (Two-Factor Authentication) and email confirmations for withdrawals.

Audit and Insurance

Institutional infrastructure typically comes with higher standards of audit and insurance. Custodians serving hedge funds and corporations undergo regular SOC 1 and SOC 2 audits to verify their security controls and financial health. Furthermore, they often carry commercial crime insurance policies to cover potential theft or loss of assets. While some top-tier retail exchanges have adopted these standards, they are a mandatory baseline requirement for any platform serving institutional capital.

Regulatory and Compliance Frameworks

The regulatory landscape dictates much of the infrastructure difference between retail and institutional trading. Retail exchanges must comply with Know Your Customer (KYC) and Anti-Money Laundering (AML) laws, requiring users to upload ID documents. However, the screening process is often automated and designed for speed to onboard thousands of users quickly.

Enhanced Due Diligence

Institutional desks perform Enhanced Due Diligence (EDD). This goes far beyond simple ID verification. Desks must verify the source of funds, the corporate structure of the counterparty, and the ultimate beneficial owners of the entity. This process is manual, rigorous, and time-consuming. It ensures that large blocks of capital entering the crypto space are legitimate and compliant with global banking regulations. This level of scrutiny is necessary because institutional trades are often large enough to trigger banking alerts and regulatory audits.

Geographic Restrictions

Regulatory compliance also dictates where these services can operate. Some OTC desks are licensed only in specific jurisdictions, such as New York (under the BitLicense) or specific European nations. Retail exchanges often cast a wider net but may restrict specific features, like futures or margin trading, based on the user's location. Institutional desks must navigate a complex web of cross-border financial regulations to legally settle trades between international entities.

Tax Reporting Infrastructure

For retail traders, tax reporting is often a matter of downloading a transaction history CSV file and importing it into tax software. Institutional platforms provide bespoke tax reporting tools that integrate directly with corporate accounting software. Because swaps and trades are taxable events, the precision of cost-basis tracking for millions of dollars in assets is critical. Institutional infrastructure supports specific accounting methods like FIFO (First-In, First-Out) or specific lot identification to optimize tax liabilities.

The Role of Swap Platforms

Sitting somewhere between traditional retail exchanges and institutional desks are swap platforms. These services offer a simplified mechanism for converting one asset to another. Unlike a trading exchange where users speculate on price direction, swap platforms are primarily utility-focused. They are designed for users who need to exchange specific tokens for portfolio diversification or utility purposes rather than active profit generation.

Non-Custodial Nature

Many swap platforms operate on a non-custodial basis. This infrastructure allows users to trade directly from their private wallets without depositing funds onto a centralized exchange. This aligns with the ethos of decentralization and reduces counterparty risk, as the platform never holds the user's funds. For retail users, this offers a level of security similar to institutional segregation but without the complex legal frameworks.

Cross-Chain Capabilities

Swap infrastructure often specializes in cross-chain interoperability. While traditional exchanges are siloed ecosystems, modern swap platforms bridge different blockchains (e.g., swapping Bitcoin for an Ethereum-based token). This requires complex backend technology that interacts with multiple blockchain networks simultaneously. For institutions, this capability is vital for moving capital between different decentralized finance (DeFi) protocols without navigating multiple centralized exchange logins.

Automation and Speed

Swap platforms leverage automation to provide instant quotes and execution. They often aggregate rates from various other exchanges to offer a competitive price. This technology mirrors the Smart Order Routing used by institutional desks but is packaged for the retail consumer. It democratizes access to efficient pricing, although users must still be wary of spread-based fees that are typical in these convenient, "no-account-needed" environments.

Operational Risks and Considerations

Every trading venue carries specific risks. Retail exchanges are centralized targets for hackers. If a retail exchange's hot wallet is compromised, user funds can be stolen. Retail users also face the risk of platform insolvency, where the exchange may not hold 1:1 reserves for customer deposits. This risk is mitigated by using platforms that provide Proof of Reserves, but it remains a central concern for the retail sector.

Counterparty Risk in OTC

Institutional OTC trading minimizes hacking risk through cold storage but introduces counterparty risk. In a trade, there is a brief window where one party has sent funds, and the other has not yet reciprocated. While escrow services and established settlement layers mitigate this, the reputation of the OTC desk is paramount. Institutions rely heavily on the legal enforceability of their trade agreements and the financial solvency of the trading desk to ensure settlement occurs as promised.

Market Volatility Exposure

Both sectors face volatility risk, but the infrastructure handles it differently. Retail platforms may experience downtime or "system overloads" during periods of extreme market movement, locking users out of their accounts. Institutional desks, operating via private lines and voice trading, can typically continue to function during high volatility, providing a crucial lifeline for large investors to exit or enter positions when public infrastructure fails.

Conclusion

The divide between institutional crypto trading desks and retail exchanges is not merely a matter of account size; it is a fundamental difference in infrastructure, fee models, and risk management. Retail exchanges excel at providing access, transparency, and user-friendly interfaces for the general public. They democratize finance by allowing anyone with an internet connection to participate in the digital asset economy. However, their public nature and order book mechanics make them unsuitable for moving massive amounts of capital without incurring significant costs.

Institutional desks provide the necessary counterweight, offering privacy, deep liquidity, and personalized execution that protects large investors from market slippage. Their fee models, built on spreads rather than commissions, align with the needs of corporate treasuries and hedge funds. As the crypto market matures, the technology powering both sectors continues to converge, with retail platforms adopting institutional-grade security and institutional desks integrating the speed and automation of retail apps.

The choice between a retail exchange and an institutional desk ultimately depends on whether a trader prioritizes immediate accessibility and transparency or execution quality and trade confidentiality.