Welcome to the new era of digital assets. For years, the cryptocurrency world operated largely outside the traditional financial system, earning a reputation as the “Wild West.” That era is concluding. As crypto matures from niche technology to a trillion-dollar asset class, global governments and regulatory bodies are stepping in to define the rules of engagement.

For the sophisticated investor, finance professional, or serious adopter of self-custody, understanding this evolving regulatory landscape is no longer optional—it is a critical necessity for strategic efficiency, risk management, and long-term participation. These regulations dictate where you can trade, how you transact, and what obligations you bear as an asset holder.

This comprehensive guide moves beyond simple transactional compliance to provide a forward-looking analysis of the key regulatory frameworks defining crypto’s future, specifically focusing on the Financial Action Task Force (FATF) guidelines, the landmark Markets in Crypto-Assets (MiCA) regulation in Europe, and the impending friction points concerning self-custody and decentralized finance (DeFi). Mastering this regulatory environment is the key to building self-sovereignty in the digital economy.

The Global Guardians: Understanding FATF and Its Mandate

At the foundation of nearly all global crypto regulation lies the need to prevent illicit financial activities, primarily money laundering and the financing of terrorism. The organizations responsible for setting these international standards act as the architects of compliance worldwide.

What is the Financial Action Task Force (FATF)?

The Financial Action Task Force (FATF) is an independent inter-governmental body that develops and promotes policies to combat money laundering (AML) and terrorist financing (CFT). It is not a law-making body itself; rather, it sets global standards that its member countries (which include most major world economies) are expected to implement through their own national laws.

When the FATF issues guidance, it effectively creates a global template for regulatory action. For the crypto industry, the FATF’s guidance has been transformative, requiring countries to treat digital assets and the services built around them with the same stringent compliance measures applied to traditional banks and financial institutions.

Defining Virtual Asset Service Providers (VASPs)

FATF’s most impactful step was defining the category of businesses subject to its rules: Virtual Asset Service Providers (VASPs).

A VASP is any person or entity that conducts one or more of the following activities or operations for or on behalf of another natural or legal person:

- Exchanging between virtual assets and fiat currencies.

- Exchanging between one or more forms of virtual assets.

- Transferring virtual assets.

- Safekeeping and/or administration of virtual assets or instruments enabling control over virtual assets.

- Participation in and provision of financial services related to an issuer’s offer and/or sale of a virtual asset.

In practical terms, this classification includes centralized cryptocurrency exchanges (CEXs) like Coinbase or Kraken, crypto custodians, brokers, and potentially even certain hosted wallet providers. Crucially, by categorizing them as VASPs, the FATF subjects these entities to mandatory KYC (Know Your Customer) and AML requirements.

The Critical Role of IOSCO

While the FATF focuses strictly on AML/CFT, another key player is the International Organization of Securities Commissions (IOSCO). IOSCO plays a role similar to that of a global standard-setter for securities markets.

If a cryptocurrency is deemed a "security" (a determination that varies by country), the regulatory frameworks set by IOSCO are crucial. IOSCO focuses on investor protection, ensuring market integrity, and reducing systemic risk. Their guidelines influence how stablecoins, DeFi lending protocols, and tokenized traditional assets are treated—often requiring prospectus disclosures, proper governance, and rules against market manipulation.

Implementing Global Anti-Money Laundering: The FATF Travel Rule

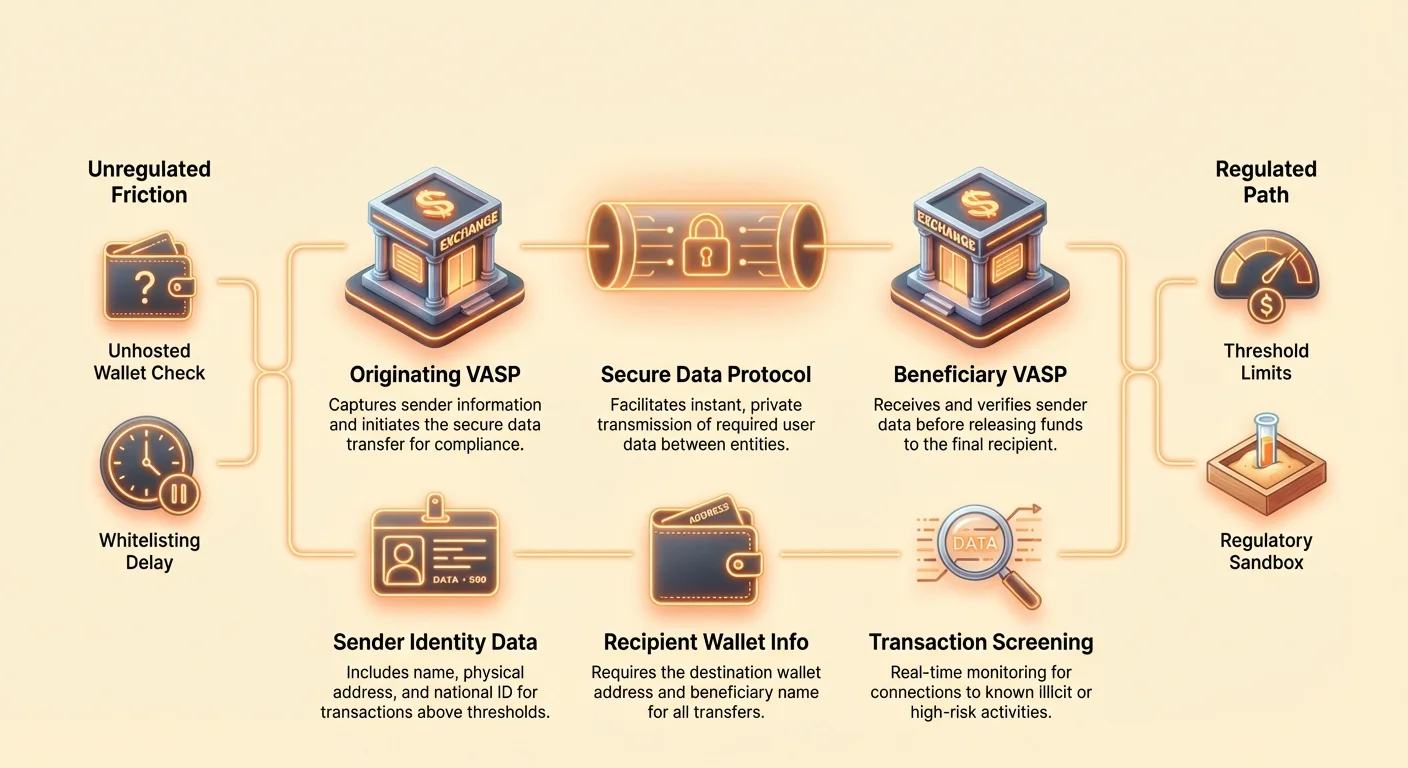

The single most disruptive regulatory implementation derived from FATF guidance is Recommendation 16, often called the "Travel Rule." This rule is designed to prevent bad actors from sending anonymous transfers across VASP platforms.

Deconstructing Recommendation 16

The Travel Rule requires VASPs to obtain, hold, and transmit certain required originator and beneficiary information to the counterparty VASP when transferring digital assets above a specified threshold (typically $1,000 or $3,000, depending on the jurisdiction).

Required Information for the Originator (Sender):

- Name

- Wallet address

- Physical address (or unique national identification number/date and place of birth, depending on jurisdiction)

Required Information for the Beneficiary (Recipient):

- Name

- Wallet address

This regulation mandates that crypto transactions, when moving between regulated entities, must carry identifying data, just like traditional wire transfers. The intent is clear: to ensure traceability of funds across the global ecosystem.

Technology Challenges for Compliance

The Travel Rule poses immense technological hurdles unique to crypto. Traditional banking transfers move slowly (hours or days) and use established, secure message channels (like SWIFT). Crypto transfers are instantaneous, permissionless, and cross-border by default.

To comply, VASPs must implement complex new protocols capable of:

- Counterparty VASP Identification: Determining if the receiving wallet belongs to another regulated VASP, and if so, which one.

- Secure Data Transfer: Sharing sensitive, personally identifiable information (PII) instantaneously and securely outside of the public blockchain network.

- Jurisdictional Segmentation: Handling varying thresholds and data requirements based on the VASP’s location.

Solutions like TRISA (Travel Rule Information Sharing Architecture) and Shyft Network are emerging to facilitate secure, off-chain, peer-to-peer data transmission between VASPs, but achieving global interoperability remains a massive challenge.

Impact on Centralized Exchanges (CEXs)

For users of CEXs, the Travel Rule significantly alters the withdrawal experience. CEXs are required to perform due diligence on destination addresses, leading to practical compliance changes:

- Whitelisting: Many exchanges now require users to "whitelist" or register external wallet addresses (even self-custody wallets) before withdrawing large amounts. This often involves manually verifying ownership or explaining the nature of the transaction.

- VASP-to-VASP Verification: If you send funds from Exchange A to Exchange B, both exchanges must exchange PII about you and the recipient (often yourself, if you own both accounts) before releasing the funds. If the receiving VASP fails to provide the required data, the sending VASP may halt or reject the transaction.

- Withdrawals to Unhosted Wallets: While the Travel Rule doesn't strictly prevent withdrawals to unhosted wallets, it requires the originating VASP to gather detailed information about the user sending the funds and often requires enhanced due diligence for transactions above the threshold.

Practical Guide to Travel Rule Compliance for Users

For the strategic crypto holder, navigating the Travel Rule requires preparation:

- Expect Delays: High-value transfers between CEXs, especially international ones, may no longer be instant. Budget time for the required VASP verification handshake.

- Verify Destination: If sending funds to another VASP account you own, ensure the receiving exchange supports the Travel Rule compliance protocol used by the sender.

- Maintain Documentation: Keep clear records of large transfers, especially when moving assets from a CEX to your self-custody wallet, as the CEX may request proof that you are the beneficial owner of the destination address.

- Threshold Awareness: Be mindful of local Travel Rule thresholds. Breaking a large transaction into smaller, separate transfers to avoid the threshold is often considered "structuring" and can flag regulatory scrutiny.

Europe’s Landmark Legislation: The Markets in Crypto Assets Regulation (MiCA)

While FATF provides the framework for global anti-money laundering, the Markets in Crypto Assets Regulation (MiCA) proposed by the European Union is the most comprehensive, jurisdiction-specific legal framework for digital assets yet devised. MiCA is set to fully apply across the EU by late 2024/early 2025 and is acting as a global template for holistic crypto regulation.

MiCA’s Scope and Purpose

MiCA’s primary goal is not just to prevent money laundering, but to establish legal certainty, support innovation, and protect consumers across the entire EU single market. Before MiCA, crypto firms had to adhere to 27 different sets of national laws. MiCA harmonizes these rules, creating a "passporting" system similar to traditional finance, allowing licensed crypto firms to operate across all EU member states with a single authorization.

The regulation covers three major categories of digital assets:

- Asset-Referenced Tokens (ARTs): Tokens backed by several fiat currencies or assets (like a basket of currencies).

- E-Money Tokens (EMTs): Tokens primarily backed by a single fiat currency (like EUR or USD stablecoins).

- Utility Tokens: Tokens intended to provide access to a good or service.

Significantly, Bitcoin and Ethereum (when used as pure decentralized assets without an identifiable issuer) are generally exempted from MiCA’s issuance rules, but the service providers handling them must still comply.

Key Requirements for Issuers and Service Providers

MiCA imposes rigorous requirements on any entity seeking to issue tokens or provide crypto services within the EU:

1. Authorization and Governance

Crypto Asset Service Providers (CASPs—MiCA’s version of VASPs) must obtain authorization from a national regulatory authority. This requires robust governance rules, clear organizational structures, and minimum capital requirements designed to ensure the CASP can withstand operational and market risks.

2. Investor Protection and Disclosure

For token issuers, MiCA introduces requirements for publishing a detailed "crypto-asset white paper." This paper must be filed with regulators, outline the risks, features, and technology, and be presented fairly and accurately. Misleading information could lead to civil liability. This mimics traditional prospectus requirements for securities.

3. Stablecoin Regulation

MiCA imposes stringent rules on stablecoins (ARTs and EMTs), requiring issuers to maintain a legal entity in the EU, hold adequate and liquid reserves (1:1 backing), and undergo regular audits. This regulation is crucial for managing the systemic risks associated with large, widely used stablecoins.

MiCA and Unhosted Wallet Transactions

One of MiCA’s most controversial extensions deals with transfers involving unhosted wallets (sometimes called self-custody or non-custodial wallets). While FATF guidelines recommend VASP reporting, MiCA—along with new, stringent updates to the EU’s Anti-Money Laundering Regulation (AMLR)—has adopted rules that dramatically increase scrutiny:

- Mandatory Identity Verification: Transfers of any amount (zero threshold) between a CASP (e.g., a CEX) and an unhosted wallet must be verified. If a user tries to withdraw funds from a CEX to an unhosted wallet, the CEX must now verify that the user controls that self-custody wallet.

- Enhanced Monitoring: For transfers exceeding €1,000 to an unhosted wallet, CASPs must implement enhanced due diligence and monitoring, including checking the source of funds and the destination address for ties to known illicit activities.

- The "Sunrise Issue": These comprehensive requirements pose significant integration problems, especially concerning the automatic collection of PII, solidifying the regulatory wall between the centralized ecosystem and self-custody.

MiCA and Global Precedent

MiCA is often cited by regulators in the US, UK, Singapore, and other major financial hubs. Its comprehensiveness and pan-national scope make it the de facto global gold standard for balancing innovation with regulation. Countries drafting their own legislation often use MiCA as a starting point, meaning its structure is likely to influence policy worldwide for the next decade.

The Frontier of Friction: Decentralization Meets Compliance

The core tension in crypto regulation exists at the interface between centralized, identifiable institutions (VASPs/CASPs) and decentralized, pseudonymized systems (DeFi, P2P networks, and self-custody wallets). Regulators are adapting their rules to reach into these previously unregulated spaces.

The Regulatory Treatment of Unhosted (Self-Custody) Wallets

An unhosted wallet (like MetaMask, Ledger, or Trezor) is a wallet where the user, and only the user, holds the cryptographic private keys. Regulators view transactions involving these wallets as high risk because they are inherently outside the purview of the regulated VASP ecosystem.

The goal of regulators is generally not to outlaw self-custody, but to prevent it from becoming a funnel for anonymous criminal finance. The key regulatory push, highlighted by MiCA and the enforcement of the Travel Rule, is to make the transfer out of the regulated space subject to severe scrutiny.

Implications for the User: If you routinely transfer large sums from a CEX to your self-custody wallet, expect more intrusive questions about the source of the funds and mandatory, verifiable proof that you own and control the receiving wallet. This creates a compliance burden aimed at deterring actors who wish to "off-ramp" or "on-ramp" anonymously through the decentralized ecosystem.

Challenges for P2P and DEX Activity

Peer-to-Peer (P2P) exchanges and Decentralized Exchanges (DEXs) are the most difficult entities for regulators to capture under the VASP model because there is often no central intermediary.

P2P Exchanges

In pure P2P trading, two individuals transact directly. Since there is no VASP facilitating the exchange, there is no regulated entity to enforce KYC/AML. Regulatory efforts often target the software providers or the interface developers who build the P2P marketplace, attempting to classify them as service providers, even if they never hold custody of the funds.

Decentralized Exchanges (DEXs)

DEXs operate via automated smart contracts. Who exactly is the VASP? The liquidity providers? The protocol founders? The front-end interface operators?

Regulatory focus has shifted to the accessible, centralized elements surrounding the protocol:

- Front-End Regulation: Regulators increasingly target the centralized web interface (the URL) that makes interacting with the DEX easy. If an interface operator restricts access based on geographical location or imposes KYC barriers to use their front-end, they might be classified as a regulated service.

- Gateway Providers: Services that bridge DeFi with traditional finance (e.g., tokenizing real-world assets or providing fiat on-ramps) are clearly VASPs and subject to full compliance.

- Protocol Founders/Developers: If developers maintain significant control over the protocol (e.g., multisig control over treasury funds or upgrade keys), they risk being treated as the regulated entity, forcing them to implement KYC at the protocol level—a concept often antithetical to DeFi principles.

The Impact of U.S. Legislation and Infrastructure

While MiCA sets the framework for Europe, the U.S. approach—often delivered through interpretations by agencies like the SEC and FinCEN—focuses on classifying assets and activities.

The implications stemming from the U.S. Infrastructure Bill, which initially sought to broadly define "broker" to include miners, developers, and protocol operators, illustrate the regulatory intent to cast a wide net. Although the final wording was softened, it signaled a clear future where any party profiting from facilitating crypto transactions will be pressured toward compliance. This ambiguity means that highly sophisticated users must constantly monitor court rulings and agency guidance to avoid legal risk.

Strategic Implications for the Self-Sovereign User

As regulatory scrutiny intensifies, self-sovereignty requires responsible action:

- Audit Your Assets: Understand which of your assets (e.g., stablecoins, utility tokens, governance tokens) might fall under securities laws or MiCA requirements in different jurisdictions.

- Isolate Transactions: Avoid "commingling" funds between wallets used for high-risk DeFi activity (which might later be scrutinized) and wallets used for transparent, compliant interactions with CEXs.

- Compliance Bridge: When moving funds from a regulated CEX to an unhosted wallet, treat the CEX interaction as the required compliance check-point. Ensure the CEX has all necessary KYC/AML data before the withdrawal.

- Understand Jurisdiction: Recognize that using a DEX front-end hosted in a different country does not necessarily shield you from the laws of your own jurisdiction.

Navigating the Future: Regulatory Innovation and Strategic Compliance

The relationship between regulators and the crypto industry is not purely adversarial. Many jurisdictions are actively seeking ways to incorporate blockchain technology while mitigating risks. This approach fosters innovation, legitimacy, and, ultimately, institutional trust.

Regulatory Sandboxes and Innovation Hubs

A "regulatory sandbox" is a defined space where businesses can test innovative products, services, and business models under relaxed regulatory requirements. Regulators oversee these tests, allowing firms to experiment with new technologies (like implementing the Travel Rule on a complex P2P structure) without immediately incurring the full weight of compliance costs.

Value for the Industry:

- De-Risking Innovation: Allows startups to ensure their technology is compliant before a full market launch.

- Regulatory Education: Helps regulators learn how new DeFi protocols function in real-world scenarios.

- Attracting Talent: Jurisdictions with active sandboxes (like the UK, Singapore, or parts of Switzerland) attract innovative firms seeking clear regulatory guidance.

The creation of these sandboxes demonstrates a global recognition that applying century-old banking laws directly to programmable money is impractical, necessitating tailored, innovative compliance solutions.

Compliance as a Competitive Advantage

For sophisticated users and institutional investors, regulation is not merely a hurdle—it is a filtering mechanism that brings credibility. Institutional capital, pension funds, and major corporate treasuries require regulatory clarity and compliance guarantees before entering an asset class.

The implementation of frameworks like MiCA signals market maturity, lowers counterparty risk, and facilitates the creation of audited, regulated financial products (like crypto ETFs or structured derivatives).

Strategic Takeaway: Firms and individuals who embrace and master complex compliance—such as integrating advanced Travel Rule solutions or maintaining meticulous audit trails—will be the first to attract regulated institutional partnerships and capital flow. Compliance shifts from a cost center to a key competitive advantage.

Future Compliance Trends to Monitor

Keeping ahead of the regulatory curve requires tracking specific areas that are likely to evolve rapidly:

- DeFi and AI-Driven Surveillance: Regulators will increasingly rely on sophisticated blockchain analytics and AI tools to monitor DeFi protocols for suspicious activity, focusing less on individual identity and more on the flow of illicit funds. This means protocol interactions linked to high-risk addresses will be flagged, regardless of the user's KYC status.

- Global Harmonization: Expect greater cooperation between FATF member states to standardize the Travel Rule implementation, making seamless VASP-to-VASP communication mandatory worldwide.

- Green Compliance: Following MiCA’s lead, we anticipate greater pressure on crypto service providers (especially mining and staking pools) to disclose and mitigate environmental impact, turning sustainability into a compliance requirement.

- Taxation Integration: Regulatory bodies (like the OECD) are pushing for automated information sharing regarding crypto holdings and transactions. This links the regulatory sphere (KYC/AML) directly to the tax compliance sphere, making comprehensive global tax reporting mandatory.

Zaključek

Prehod iz neregulirane panoge v opredeljeno finančno industrijo je ključen za dolgoročno vzdržnost digitalnih sredstev. Okviri, kot sta Pravilo potovanja FATF in MiCA EU, predstavljajo temeljne premike, ki kripto premikajo stran od nišne anonimnosti proti globalni, regulirani odgovornosti.

Za resnega udeleženca kripta ta regulativni poglobljeni vpogled poudarja eno samo resnico: samo-suverenost v digitalni ekonomiji se doseže ne z izogibanjem regulaciji, temveč z njenim obvladovanjem. Z razumevanjem osnovnih mandatov globalnih standardizatorjev, strateško navigacijo trenj med centralizacijo in decentralizacijo ter sprejemanjem napovednih najboljših praks lahko uporabniki zagotovijo svoje trajno, varno in skladno sodelovanje v prihodnosti financ.