Managing risk in decentralized finance requires a fundamental shift in mindset from traditional investing. In the centralized financial world, banks and brokerages often absorb operational risks or provide insurance guarantees like FDIC protection. In the DeFi ecosystem, these safety nets do not exist by default. The responsibility for asset protection falls entirely on the individual user.

This autonomy offers immense power and efficiency, but it demands a robust framework for identifying and neutralizing threats. A comprehensive strategy relies on three primary tools: hedging against market volatility, insuring against technical failures, and managing decentralized credit or leverage responsibly. Understanding when and how to deploy these tools distinguishes a sophisticated DeFi participant from a gambler.

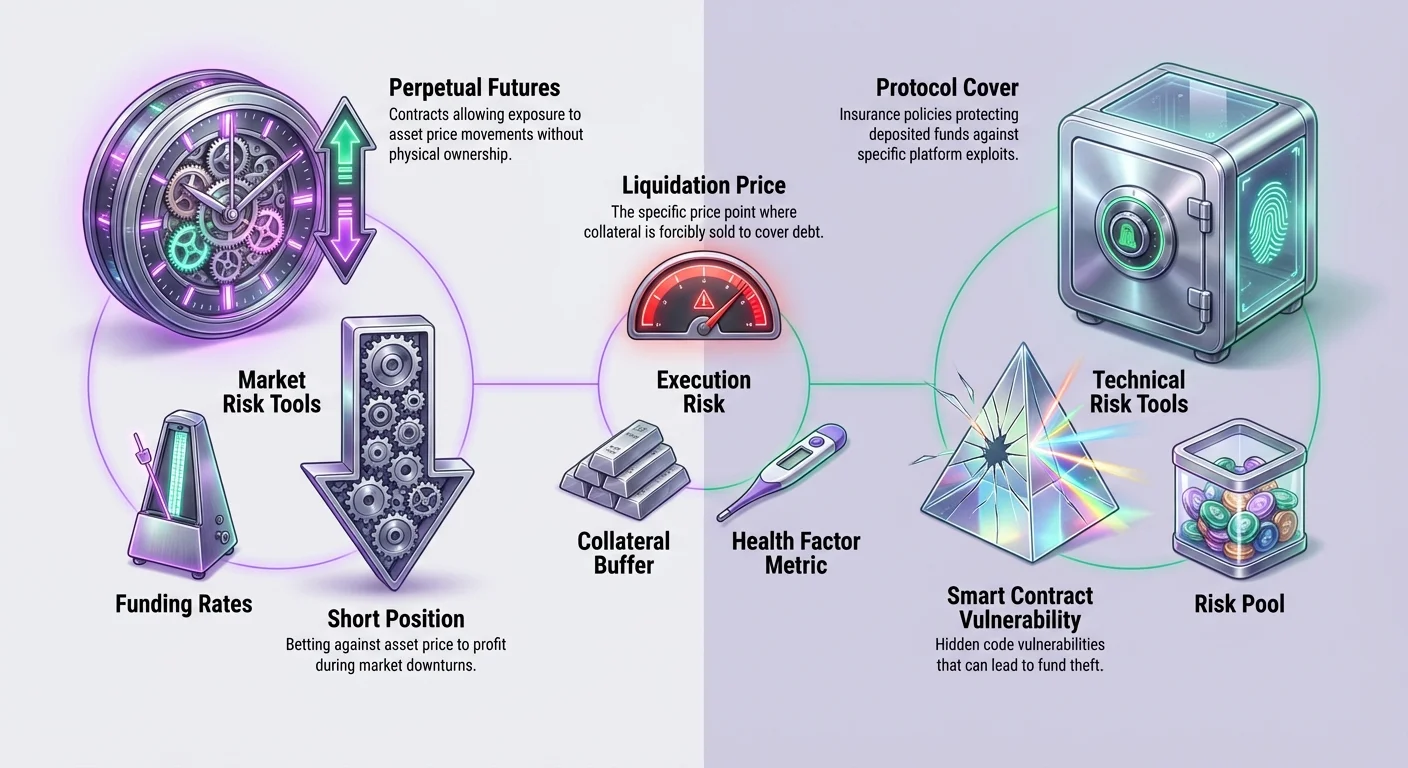

The landscape of digital assets exposes users to unique vectors of loss. Market prices can swing violently based on sentiment, wiping out portfolio value in hours. Simultaneously, the underlying smart contracts that power decentralized applications may contain hidden bugs or vulnerabilities. Even the solvency of the platforms themselves can be a concern if they are not fully decentralized.

To navigate this, users must construct a personalized risk management stack. This involves utilizing derivatives to lock in value without selling, purchasing protocol cover to protect against hacks, and understanding the mechanics of leverage to prevent liquidation. By mastering these components, you can interact with decentralized markets with a level of security comparable to, or even exceeding, traditional finance.

Decentralizētās hedžēšanas mehānikas

Hedžēšana ir aizsardzības stratēģija, ko izmanto, lai kompensētu potenciālos zaudējumus jūsu turējumos. DeFi tā galvenokārt tiek sasniegta, izmantojot derivātus. Derivāti ir finanšu līgumi, kas izrieto savu vērtību no pamata aktīva, piemēram, Bitcoin vai Ethereum. Atšķirībā no spot tirdzniecības, kur jūs vienkārši pērkat un turat aktīvu, cerot uz tā vērtības pieaugumu, derivāti ļauj gūt peļņu gan no cenu kāpuma, gan krituma.

Biežākais instruments šim nolūkam kripto telpā ir pastāvīgais nākotnes līgums. Šie līgumi ļauj tirgotājiem iegūt ekspozīciju pret aktīva cenu bez fiziskas īpašuma. Šī elastība ir būtiska riska pārvaldībai. Ja jūs turat nozīmīgu kripto aktīva daudzumu un baidāties no īstermiņa cenas krituma, jums nav jāpārdod savs turējums un jāizraisa nodokļa pienākums.

Īsās hedžēšanas izveidošana

Lai aizsargātu portfeļa vērtību tirgus krituma laikā, tirgotājs var atvērt "īsu" pozīciju. Īsa pozīcija nozīmē derību, ka aktīva cena kritīsies. Ja tirgus krīt, peļņa no jūsu īsās pozīcijas var kompensēt zaudējumus jūsu spot turējumu vērtībā. Tas efektīvi fiksē jūsu portfeļa dolāra vērtību neatkarīgi no tirgus kustības.

Piemēram, ja jūs turat Ethereum un uzskatāt, ka cena kritīsies, jūs varat pārdot ETH pastāvīgo līgumu. Ja Ethereum cena krīt par 10%, jūsu fiziskie turējumi zaudē vērtību, bet jūsu īsais līgums iegūst vērtību. Neto rezultāts ir tas, ka jūsu kopējā portfeļa vērtība paliek stabila. Šī tehnika ļauj ilgtermiņa turētājiem izturēt svārstības, neizkāpjot no pozīcijām.

Sviras izpratne hedžēšanā

Viens no izteiktākajām DeFi derivātu iezīmēm ir sviras izmantošanas iespēja. Svira palielina jūsu pirkšanas spēju, ļaujot kontrolēt lielu pozīciju ar mazāku nodrošinājuma summu. Lai gan bieži izmantota spekulācijām, svira ir spēcīgs instruments kapitāleficientai hedžēšanai.

Piemēram, ja vēlaties hedžēt 10 000 USD vērtu Bitcoin, jums nav jāiegulda 10 000 USD derivātu protokolā. Ar 2x sviru jums jāiegulda tikai 5000 USD, lai atvērtu ekvivalentas lieluma īso pozīciju. Tas atbrīvo atlikušo kapitālu citām ienākumu ģenerējošām aktivitātēm vai papildu drošības buferiem.

Tomēr svira ievieš likvidācijas risku. Ja tirgus kustas pret jūsu pozīciju — šajā gadījumā, ja cena ievērojami pieaug —, jūsu nodrošinājums var būt nepietiekams zaudējumu segšanai. Protokols tad automātiski aizvērs jūsu pozīciju, lai novērstu slikto parādu. Tāpēc riska neitrālām hedžēšanas stratēģijām ieteicams izmantot zemu sviru, piemēram, 1x vai mazāk.

Finansēšanas likmju loma

Turot pastāvīgo līgumu, jāņem vērā finansēšanas likmes. Finansēšana ir mehānisms, kas uztur derivātu līguma cenu tuvu pamata aktīva spot cenai. Tas darbojas kā periodiska maksājuma starp garajām un īsajām pozīcijām.

Kad tirgus noskaņojums ir optimistisks un pastāvīgās cenas ir augstākas par spot cenu, tirgotāji ar garajām pozīcijām maksā tiem ar īsajām. Pretēji, kad tirgus ir pesimistisks, īsās maksā garajām. Šīs izmaksas var uzskatīt par maksu par pozīcijas uzturēšanu vai kompensāciju par tirgus līdzsvarošanu.

Ja uzturat ilgtermiņa hedžēšanu, finansēšanas likmes var ietekmēt jūsu rentabilitāti. Spēcīgi optimistiskā tirgū īsās hedžēšanas uzturēšana var ģenerēt ienākumus, ja garās maksā īsajām. Pesimistiskā tirgū jums var nākties maksāt par aizsardzības uzturēšanu. Šo likmju uzraudzība ir kritiska izmaksu efektīvas hedžēšanas uzturēšanai laika gaitā.

Operational Risks and Smart Contract Safety

While hedging protects against market price volatility, it does not protect against the failure of the technology itself. DeFi relies on smart contracts—code that executes automatically on the blockchain. If this code contains a bug, it can be exploited by hackers, leading to the loss of deposited funds. This is where decentralized insurance becomes vital.

Traditional insurance is often slow, opaque, and burdened by high overhead costs for real estate and workforce. Decentralized insurance platforms operate on the blockchain, increasing transparency and efficiency. They use smart contracts to pool risk and automate potential payouts, allowing users to buy protection directly against specific technical failures.

Decentralized Insurance Models

Platforms like Nexus Mutual operate as decentralized autonomous organizations (DAOs) owned by their members. Instead of a corporate board deciding on claims, the community participates in assessing risk and voting on payouts. Funds are held in a shared risk pool, and membership rights are often represented by a token.

These platforms offer "protocol cover" or "smart contract cover." This specific type of policy protects assets deposited into other DeFi protocols. For example, if you lend funds on a decentralized lending platform or deposit liquidity into a decentralized exchange, you are exposed to the risk that the platform's code might fail.

By purchasing cover, you transfer this risk to the insurance pool. If the protocol you are using suffers a hack or a smart contract failure that results in a loss of funds, you can file a claim. If the claim is approved by the community assessors, the pool pays out the covered amount, making you whole.

The Efficiency of On-Chain Coverage

Decentralized insurance brings significant efficiency gains over traditional models. Because they run on public blockchains like Ethereum, these platforms operate 24/7 without holidays or business hours. Automation via smart contracts reduces the administrative burden, allowing for potentially lower premiums and faster processing times.

The assessment process is also more transparent. In traditional insurance, the decision-making process for claims is internal and often hidden from the policyholder. In a decentralized model, the assessment is done by members of the protocol. The voting and decision data are recorded on-chain, providing a clear audit trail of how the conclusion was reached.

This transparency aligns the incentives of the platform with its users. Members are incentivized to assess claims accurately to maintain the integrity and reputation of the mutual. It represents a shift from an adversarial relationship between insurer and insured to a cooperative risk-sharing agreement.

Utilizing Decentralized Credit and Lending

Credit markets in DeFi serve a dual purpose in a risk management framework. They allow users to earn yield on idle assets, but they also enable borrowing against assets to access liquidity without selling. This can be a form of risk management for tax purposes or to maintain upside exposure while covering real-world expenses.

However, interacting with lending protocols introduces its own set of risks. When you deposit funds to lend, you face the smart contract risk of that platform. When you borrow, you face liquidation risk if the value of your collateral falls below a certain threshold relative to your loan.

Borrowing Mechanics and Risks

To borrow in DeFi, you typically must over-collateralize your loan. This means depositing more value in crypto than you take out in debt. For example, you might deposit $1,000 worth of ETH to borrow $500 in stablecoins. This creates a safety buffer for the protocol.

The risk here is volatile collateral value. If the price of ETH drops significantly, the value of your collateral may no longer be sufficient to secure the $500 loan. The protocol will liquidate a portion of your collateral to repay the debt. This is a forced sale, often at an unfavorable price, plus a liquidation penalty fee.

Managing this risk requires constant monitoring of your "health factor" or collateralization ratio. Prudent borrowers maintain a wide buffer, ensuring that even a substantial market drop will not trigger liquidation. This parallels the leverage risk in derivatives trading, where maintaining adequate margin is crucial for survival.

Integrating Insurance with Lending

Because lending protocols are frequent targets for exploits due to the large value locked in their smart contracts, they are prime candidates for insurance coverage. A robust risk framework might involve depositing assets into a lending protocol to earn interest, while simultaneously purchasing smart contract cover for that specific protocol.

This strategy layers protection. The user gains the utility of the lending market—yield or credit lines—while mitigating the catastrophic risk of a platform hack. The cost of the insurance premium acts as an expense that reduces the net yield but secures the principal capital.

For users who are yield farming or providing liquidity on decentralized exchanges (DEXs), the same logic applies. These activities involve depositing assets into smart contracts. While they generate returns, they carry inherent code risk. Insuring these deposits ensures that the pursuit of yield does not result in total loss due to a technical bug.

Practical Execution of Derivatives Trading

To execute a hedging strategy, users need a reliable platform and the right tools. Decentralized exchanges (DEXs) like dYdX allow for perpetual futures trading directly from a self-custodial wallet. This setup protects users from the opaque behaviors of centralized exchanges, which may misuse funds or face insolvency.

Getting started requires a Web3 wallet, such as the Bitcoin.com Wallet, and some cryptocurrency for collateral and transaction fees. Since derivatives trading often occurs on Layer 2 solutions to save on gas costs, users may need to deposit assets into the specific Layer 2 protocol used by the exchange.

Opening and Managing Positions

Once your wallet is connected and funded, you can choose between going long or short. If you believe the market will rise, you buy a contract (long). If you believe it will fall, or if you are hedging existing holdings, you sell a contract (short).

There are two primary order types to understand: market orders and limit orders. A market order executes immediately at the current available price. This is useful when speed is the priority. A limit order executes only at a specific price you set, or better. This allows for more precise entry points but carries the risk that the order may never be filled if the price does not reach your target.

When opening a position, you must also select your leverage. As noted earlier, leverage amplifies both gains and losses. New users are strongly advised to stick to 1x leverage or lower to avoid rapid liquidation. High leverage ratios, such as 10x or 20x, significantly tighten the liquidation price, leaving very little room for market volatility.

Calculating Liquidation Prices

Understanding where your position will be liquidated is the most critical mathematical component of trading derivatives. The liquidation price is the point at which your collateral can no longer support the position.

For a long position, the liquidation price is below your entry price. If you buy Bitcoin at $20,000 with 1x leverage using $100 of collateral, your liquidation price might be around $600. This is extremely safe. However, at 10x leverage, the liquidation price moves up to $18,600. A mere 7% drop in price would wipe out your position.

For a short position, the liquidation price is above your entry. If you short Bitcoin at $20,000 with 1x leverage, your liquidation price is nearly double the entry, offering a massive safety buffer. At 10x leverage, the liquidation price drops to $21,400. A small upward pump would result in a total loss of collateral.

| Leverage | Collateral (USD) | Position Size | Liquidation Risk |

|---|---|---|---|

| 1x | 100 | 100 | Low |

| 5x | 100 | 500 | Moderate |

| 10x | 100 | 1000 | High |

The Insurance Procurement Process

Securing insurance in DeFi is a straightforward process that begins with identifying the need. Coverage is essentially useless if it does not match your specific exposure. You must identify which protocols hold your funds—whether it is a DEX, a lending platform, or a yield aggregator—and seek policies that cover those specific entities.

You will need a digital wallet and cryptocurrency to pay for the premium. The premium is the cost of the cover, usually determined by the amount of protection desired and the duration of the policy. On Ethereum-based platforms, ETH is typically required for transaction fees, while the premium itself might be paid in ETH, a stablecoin, or the platform's native token.

Buying Cover Step-by-Step

After connecting your self-custodial wallet to a platform like Nexus Mutual, you navigate to the "cover" section. Here you can browse available products. Once you find the protocol you wish to insure, you enter the cover amount. This should match the value of the assets you have deposited in that protocol.

Next, you select the cover period. This could range from a few weeks to several months. The platform will generate a quote based on these inputs. If the price is acceptable, you approve the transaction in your wallet. Once confirmed on the blockchain, your cover is active immediately.

This process empowers users to tailor their security. You are not forced into a blanket policy; you can surgically apply insurance to the highest-risk portions of your portfolio. This flexibility is a hallmark of decentralized risk management.

Filing a Claim

If an incident occurs, such as a hack of the covered protocol, the claims process is initiated through the same interface. It is vital to check the wording of your cover policy first to ensure the specific event is included in the terms.

To make a claim, you submit a request along with details of the incident and proof of loss. The requirements for proof can vary by product but generally involve demonstrating that you held funds in the affected protocol at the time of the hack.

Once submitted, the claim goes to the community assessors. They review the evidence and vote on the validity of the claim. If approved, the payout is processed directly to your wallet. This community-driven approach ensures that decisions are made by stakeholders who understand the technical nuances of the ecosystem.

Comparing Risk Management Tools

Choosing between hedging, insurance, and credit depends on the specific risk you are trying to mitigate. These tools are not mutually exclusive; they are complementary parts of a total framework.

Hedging via derivatives is the correct tool for managing market risk. If you are worried about the price of your assets going down, insurance will not help you. Insurance generally does not cover market devaluation. Only a short hedge or selling the asset can protect against price drops.

Insurance is the correct tool for protocol risk. If you are worried that a smart contract will be hacked, hedging will not help you. A short hedge protects against price, but if the tokens themselves are stolen from a smart contract, the hedge does nothing to replace them. Insurance provides a replacement of the lost value.

Cost Analysis

Each tool carries a cost. Hedging involves trading fees and potentially funding payments. If the market moves in your favor (against your hedge), you also face the opportunity cost of capped gains. Insurance involves an upfront premium, which is a direct expense that lowers your overall return on investment.

Credit involves interest rates. Borrowing assets to avoid selling requires paying interest to lenders. The user must weigh these costs against the potential benefits. For example, is the cost of the insurance premium lower than the risk-adjusted yield you are earning? Is the cost of funding a short hedge lower than the potential tax bill from selling your assets?

Decentralized vs. Centralized Execution

A key component of this framework is the venue of execution. Trading derivatives on decentralized protocols like dYdX offers protection from counterparty risk that exists on centralized exchanges. On a centralized exchange, you do not technically own your funds; the exchange does. If they mismanage deposits, you lose everything.

In DeFi, you retain custody of your assets in your own wallet until the moment of trade execution or smart contract deposit. While this introduces smart contract risk (which can be insured), it eliminates the "black box" risk of centralized entities. Using self-custodial wallets is the foundational layer of all DeFi risk management.

Uzlabota sviras pārvaldība

Tiem, kas izmanto derivātus ne tikai hedžēšanai, bet aktīvai tirdzniecībai, sviras pārvaldība kļūst par galveno riska faktoru. Svira ir divgriezīgs zobens, kas var pastiprināt atdevi, bet arī paātrināt zaudējumus.

Katram tirgum ir maksimālais sviras limits, bieži no 10x līdz 20x galvenajiem aktīviem kā Bitcoin. Tomēr tas, ka augsta svira ir pieejama, nenozīmē, ka to vajag izmantot. Galvenais jēdziens, ko apgūt, ir "marža".

Sākotnējā vs. uzturēšanas marža

Sākotnējā marža ir nodrošinājums, kas nepieciešams pozīcijas atvēršanai. Uzturēšanas marža ir minimālais nodrošinājuma daudzums, kas nepieciešams pozīcijas uzturēšanai. Ja jūsu maržas bilance krīt zem uzturēšanas līmeņa nelabvēlīgu cenu kustību dēļ, jūs tiksiet likvidēts.

Viedra riska pārvaldība ietver maržas bilances uzturēšanu ievērojami virs uzturēšanas līmeņa. Tas izveido buferi, kas ļauj jūsu pozīcijai izdzīvot normālas tirgus svārstības bez aizvēršanas. Tirgotājiem jāizvairās no "maksimālas" sviras izmantošanas, jo tas neatstāj vietu kļūdām.

Finansēšanas likmju arbitrāža

Uzlaboti lietotāji var arī pārvērst finansēšanas likmes par ienākumu plūsmu. Ja finansēšanas likmes ir pozitīvas (garās maksā īsajām), īsās pozīcijas atvēršana ļauj savākt šos maksājumus. Ja vienlaikus turat spot aktīvu, jūs esat "delta neitrāls" — imūns pret cenu kustībām —, vienlaikus gūstot finansēšanas likmes ienesumu.

Šī stratēģija efektīvi izmanto derivātu tirgu ienesuma ģenerēšanai ar zemu cenas risku. Tomēr tā prasa modīgu uzraudzību. Finansēšanas likmes mainās nepārtraukti, un rentabla tirdzniecība var pārvērsties izmaksās, ja tirgus noskaņojums apgriežas.

Secinājums

Pilns DeFi riska pārvaldības ietvars nav par riska pilnīgu izvairīšanos, bet par tā izpratni un kontroli. Atšķirot tirgus risku, tehnisko risku un likviditātes risku, lietotāji var izmantot atbilstošos rīkus sava kapitāla aizsardzībai.

Derivāti un pastāvīgie nākotnes līgumi nodrošina mehānismu hedžēšanai pret cenas svārstībām, fiksējot vērtību bez aktīvu likvidācijas. Decentralizētā apdrošināšana nodrošina drošības tīklu pret unikālajām tehniskajām briesmām no viedu līgumu kļūdām un hakiem. Decentralizētais kredīts un atbildīga sviras pārvaldība ļauj efektīvi izmantot kapitālu bez liekas likvidācijas briesmām.

Šo elementu integrēšana prasa praksi un disciplīnu. Tas sākas ar pašaprūpi, turpinās ar rūpīgu protokolu izvēli un nostiprinās ar stratēģisku finanšu instrumentu izmantošanu. Augot DeFi ekosistēmai, šie rīki kļūs vēl izsmalcinātāki, bet aizsardzības pamatprincipi paliks tie paši.

Patiesa riska pārvaldība ir apzināta izvēle apmainīt potenciālo augšupeiti pret garantētu izdzīvošanu.