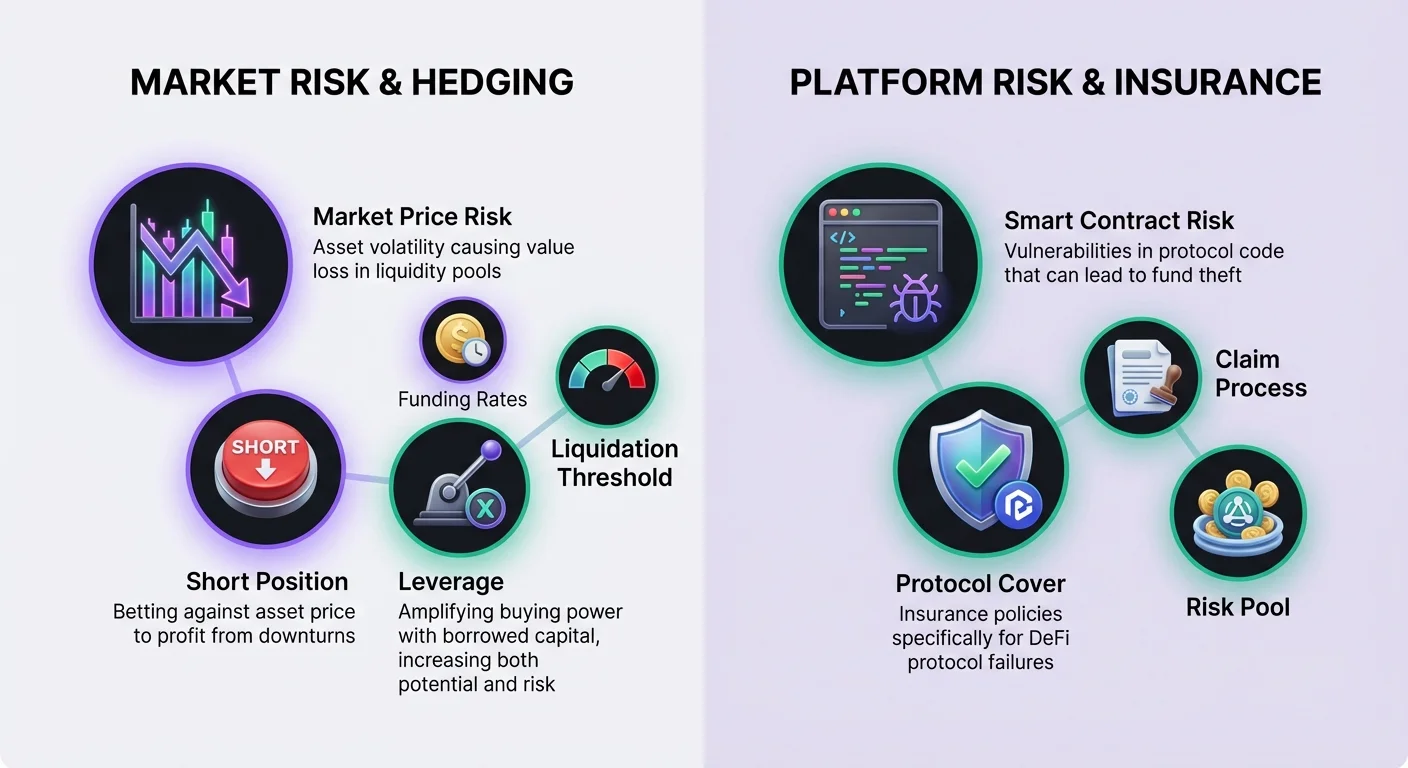

Decentralized finance offers opportunities to earn yield through liquidity provision, but this activity comes with inherent market risks. When asset prices change significantly, liquidity providers often face a reduction in value compared to simply holding the tokens, a phenomenon known as impermanent loss. To combat this, sophisticated participants turn to financial derivatives. These instruments allow users to neutralize their market exposure. By combining these trading tools with decentralized insurance, investors can create a more robust strategy that addresses both market volatility and smart contract risks.

Derivatives markets in DeFi have evolved to offer perpetual futures and other contract types that settle on-chain or via layer-2 solutions. These protocols enable users to express granular views on price direction without needing to own the underlying asset physically. This capability is essential for hedging. When a user holds a spot position in a liquidity pool, they are implicitly long the asset. Using derivatives to take an opposing short position can flatten this exposure, protecting the principal value in dollar terms regardless of market movement.

The Fundamentals of DeFi Derivatives

DeFi allows users to deposit collateral and trade financial contracts that derive their value from underlying cryptocurrencies. Unlike buying a cryptoasset on a spot exchange, which represents immediate ownership, a derivative contract is an agreement based on the future price of that asset. This distinction is critical for hedging strategies. Spot ownership only allows for profit when prices rise. Derivatives enable traders to profit when prices fall, which is the mechanism used to offset losses in a liquidity pool during a downturn.

Leading decentralized applications (DApps) for derivatives often operate on layer-2 networks. For example, platforms like dYdX function as a layer-2 Ethereum decentralized exchange specializing in perpetual futures. This architecture offers significant improvements in transaction speed and reduces costs compared to layer-1 execution. Importantly, trades are still settled on the base layer, providing security guarantees. These platforms utilize smart contracts to manage positions, removing the need for central intermediaries or opaque order books found on traditional exchanges.

Mechanics of Long and Short Positions

Understanding the specific directional views available through derivatives is necessary for constructing a hedge. Perpetual trading consists of either going long or going short on an underlying asset. Going long signifies a belief that the asset's value will increase. This is achieved by buying a perpetual contract. For a liquidity provider who already owns the tokens in a pool, they are already effectively long. Adding a long derivative position would only increase their risk exposure.

To neutralize exposure, a liquidity provider would focus on the short side. Going short means betting that the underlying asset will fall in value. This is executed by selling a perpetual contract. If the market price of the asset drops, the value of the tokens in the liquidity pool decreases. However, the short position in the derivatives market gains value. Ideally, the profit from the short hedge offsets the decline in the portfolio's spot value. This balance preserves the total dollar value of the capital deployed.

Leverage and Capital Efficiency

One of the primary advantages of using derivatives over spot selling is the access to leverage. Leverage allows a trader to purchase or sell more contracts than their deposited collateral would normally permit. This acts as a multiplier for purchasing ability. In the context of hedging, leverage allows a user to protect a large liquidity position with a relatively small amount of capital set aside for the hedge. This capital efficiency is vital for maintaining a high yield on the main portfolio.

However, leverage introduces significant risks that must be managed carefully. It exposes the trader to liquidation if the market moves against the position. Platforms define a maximum leverage for different markets. For instance, a BTC-USD market might offer up to 20x leverage, while an AVAX-USD market might be capped at 10x. The risk increases as the position size grows relative to the collateral. A highly leveraged hedge requires less upfront capital but demands strict monitoring to prevent the position from being wiped out during volatility.

Calculating Leverage Ratios

It is helpful to visualize how leverage impacts purchasing power. If a trader deposits 100 USDC as collateral, different leverage settings drastically change the theoretical maximum position size. At 1x leverage, the user can buy or sell 100 USDC worth of contracts. This is effectively a fully collateralized position with no added leverage risk. At 10x leverage, that same 100 USDC controls 1,000 USDC worth of contracts.

Pushing the limits further dramatically increases exposure. At 20x leverage, the 100 USDC deposit controls 2,000 USDC worth of contracts. While this allows for aggressive hedging with minimal capital, it leaves very little room for price fluctuations. New users or those using derivatives strictly for insurance-like hedging are often encouraged to use 1x leverage or less to minimize liquidation risks.

Understanding Liquidation Thresholds

Liquidation occurs when the trader runs out of margin to support their position. When this happens, the protocol automatically closes the position, and the trader pays a liquidation fee. The liquidation price depends heavily on the leverage used. Consider a scenario where a trader wants to long Bitcoin at 20,000 USD with 100 USD of collateral. Using 1x leverage, the liquidation price might be as low as 600 USD, providing immense safety.

As leverage increases, the liquidation price moves much closer to the entry price. With 2x leverage on the same trade, the liquidation price might jump to roughly 10,600 USD. At 10x leverage, the liquidation price could be around 18,600 USD. In this high-leverage scenario, a mere 7% drop in the asset price would wipe out the collateral. For short positions used to hedge, the risk is inverted; a sharp rise in price can trigger liquidation.

Fininšu likmes un uzturēšanas marža

Derivātu pozīcijas uzturēšana ietver divu galveno finanšu konceptu izpratni: maržu un finansējumu. Marža ir nodrošinājums, kas nepieciešams, lai uzturētu darījumu atvērtu. Tā tiek kategorizēta sākotnējā maržā un uzturēšanas maržā. Sākotnējā marža ir summa, kas nepieciešama pozīcijas atvēršanai. Uzturēšanas marža ir minimālā summa, kas nepieciešama, lai pozīcija paliktu atvērta un novērstu likvidāciju. Ja konta vērtība krīt zem uzturēšanas maržas, protokols likvidē pozīciju, lai nodrošinātu maksātspēju.

Finansējums ir mehānisms, kas unikāls pastāvīgajiem futūriem un piestiprina līguma cenu pie spot cenas. Tas darbojas kā periodiska maksājuma starp tirgotājiem. Kad pastāvīgā līguma cena ir zem pamata spot cenas, short maksā long. Tas parasti notiek, kad valda bearish noskaņojums un vairāk tirgotāju shorto. Pretēji, kad pastāvīgā cena ir virs pamata aktīva, long maksā short. Tas norāda bullish noskaņojumu.

Hedžerim, kurš tur short pozīciju, fininšu likmes ir mainīga izmaksu vai atlaides. Buļļu tirgū, kur long maksā short, hedžeris efektīvi saņem maksājumu par aizsardzības uzturēšanu. Tomēr lāču tirgū, kur pūlis shorto, hedžeris var būt spiests maksāt fininšu nodevas. To var uzskatīt par nodokli uz vairākuma noskaņojumu, ko maksā mazākumam. Hedžeriem jāņem vērā šī potenciālā izmaksu, aprēķinot likviditātes nodrošināšanas stratēģijas neto ienesumu.

Hedža izpilde

Lai īstenotu hedžu, lietotājiem jāinteragē ar derivātu DApp interfeisu. Ir divi galvenie veidi pozīcijas atvēršanai: tirgus ordeņi un limit ordeņi. Tirgus ordeņi izpildās tūlītējā pašreizējās ordeņu grāmatas cenās. Tas nodrošina, ka hedžs tiek ievietots uzreiz, bet piedāvā mazāku kontroli pār specifisko ievades cenu. Limit ordeņi izpildās tikai norādītajā cenā vai labāk. Tas piedāvā cenas noteiktību, bet rada risku, ka orderis netiks izpildīts, ja tirgus attālināsies no mērķa.

Pirms tirdzniecības aktīvi jāiemaksā protokolā. Platformas kā dYdX prasa lietotājiem pārvietot kriptoaktīvus no pašpārvaldības maciņa uz DApp, lai samazinātu darījumu izmaksas un uzlabotu ātrumu. Citas platformas var atļaut tirdzniecību tieši no maciņa bez atsevišķa iemaksas soļa. Lietotāji pieslēdz savu web3 maciņu, izvēlas aktīvu iemaksai un gaida darījuma apstiprināšanos blokķēdē. Kad finansēts, viņi var izvēlēties tirgu, kas atbilst viņu LP pozīcijai, un pārdot līgumus, lai sāktu hedžu.

Pozīcijas aizvēršana ir pēdējais solis ciklā. Šī darbība pārvērš nereālizētos ieguvumus vai zaudējumus realizētos rezultātos. Ja hedžs bija veiksmīgs tirgus krituma laikā, short pozīcija būs uzkrājusi nereālizētus ieguvumus. Pozīcijas aizvēršana pievieno šos ieguvumus konta atlikumam, kompensējot zaudējumus likviditātes baseinā. Lietotāji parasti pāriet uz atvērto pozīciju cilni un izvēlas aizvērt, pilnībā izkāpjot no darījuma.

Managing Smart Contract and Platform Risk

While derivatives manage market price risk, using them introduces a new layer of risk: platform failure. Decentralized finance relies on smart contracts, which are code-based agreements on the blockchain. These contracts can contain bugs or vulnerabilities that hackers might exploit. Additionally, the DApps used for hedging are distinct entities from the liquidity pools. This means a user is exposing capital to two different protocols simultaneously.

To mitigate this operational danger, users can purchase decentralized insurance. Blockchain technology allows for insurance efficiency by reducing overhead and increasing transparency. Decentralized insurance platforms replace traditional corporate structures with code and community governance. Assessments are performed by on-chain members, and claims are often voted on by the community. This creates a transparent process compared to the opaque decision-making of centralized insurers.

The Role of Protocol Cover

In the context of DeFi, insurance is often referred to as "cover." A specific type of policy relevant to hedgers is "protocol cover." This protects against financial losses resulting from failures within specific DApps. For a user hedging on a derivatives platform, buying protocol cover for that specific exchange protects their margin collateral. If the derivatives platform suffers a hack or a smart contract failure, the insurance policy is designed to reimburse the lost funds.

This type of protection is essential for a complete risk management strategy. Without it, a user might successfully neutralize their impermanent loss only to lose their hedging capital in a protocol exploit. Major decentralized insurance platforms, such as Nexus Mutual, offer coverage for a wide variety of leading DeFi protocols. They operate as a discretionary mutual where members hold a token, such as NXM, which is used to purchase cover and participate in risk assessment.

Purchasing and Claiming Insurance

To buy protection, a user needs a digital wallet and cryptocurrency to pay for the premium. The process involves connecting a self-custodial wallet to the insurance application. The user selects the specific protocol they wish to insure—in this case, the derivatives exchange hosting their short position. They then specify the amount of cover, typically denominated in ETH or stablecoins, and the duration of the policy. A premium is calculated based on these inputs.

If an incident occurs, the user must file a claim. A claim is a formal request for payment based on the terms of the cover. Unlike traditional insurance which may require lengthy investigations, DeFi claims are often streamlined because the loss event is verifiable on-chain. The user submits proof of loss, and the claim is reviewed by the community or claims assessors. If approved, the payout covers the losses up to the policy limit.

Where Insurance Applies in DeFi

Insurance is not limited to just the hedging venue. A comprehensive strategy might involve buying cover for multiple points of failure in the DeFi ecosystem. Since the user is engaging in several activities to construct this hedge, each step carries its own profile of risk that can be insured.

Key areas where cover is applicable include:

- Trading derivatives: Protecting the collateral deposited on platforms like dYdX.

- Lending or borrowing: Protecting assets supplied to money markets like Aave.

- Yield farming: Protecting the principal tokens deposited in the DEX liquidity pool itself.

- Custody: Protecting assets if they must be held on centralized services, though self-custody is preferred.

Prerequisites for DeFi Hedging

Executing a strategy that combines liquidity provision, derivatives hedging, and insurance requires specific tools and assets. The foundation of all these interactions is the digital wallet. These are often called web3 wallets. The most secure option is a self-custodial wallet. Self-custody means the user retains full control over the private keys and the contents of the wallet. This contrasts with custodial wallets where a third party controls the funds.

The wallet serves as the passport to connect to various decentralized applications via protocols like WalletConnect. Whether accessing a derivatives exchange or an insurance provider, the connection process is similar. The user approves the DApp to interact with their wallet, allowing them to sign transactions and move funds. This interoperability is what makes composable DeFi strategies possible.

Gas and Transaction Fees

Every action taken to set up a hedge requires cryptocurrency to pay for transaction fees. These fees pay for the changes made to the blockchain ledger. They are always paid in the native currency of the blockchain being used. For example, interacting with Ethereum-based protocols like Nexus Mutual or layer-2 settlements for dYdX requires ETH.

Users must ensure their wallet contains sufficient native currency to cover these costs in addition to the capital used for the hedge itself. Running out of gas prevents the user from adjusting a hedge or buying cover, potentially leaving them exposed at critical moments. Transaction costs should be factored into the overall profitability calculation of the strategy.

Selecting the Right Platforms

Success depends on choosing reputable platforms. For derivatives, liquidity is a primary concern. A platform must have a sufficient number of liquid markets to ensure the user can enter and exit hedges without significant price slippage. dYdX is noted for being a leading DApp in this sector, offering deep liquidity on perpetual futures. This depth ensures that the short hedge tracks the spot price accurately.

For insurance, the size of the risk pool is critical. The platform must have enough capital backing the pool to pay out claims if a major event occurs. Nexus Mutual is structured as a DAO owned by its members, with funds held in a risk-sharing pool. This structure aligns incentives, as the community is involved in assessing risks and accepting coverage proposals. Using established platforms mitigates the risk that the counterparty (the protocol) fails to perform its function.

Secinājums

Ekspozīcijas neitralizēšana likviditātes nodrošināšanā prasa finanšu instrumentu un aizsardzības pasākumu kombināciju. Izmantojot pastāvīgos futūrus, investori var ieņemt short pozīcijas, kas gūst peļņu, kad aktīvu cenas krīt, efektīvi līdzsvarojot zaudējumus viņu spot turējumos. Tas rada delta-neitrālu stāvokli, kur dolāra vērtība tiek saglabāta, neskatoties uz tirgus svārstībām. Svira ļauj to darīt efektīvi, lai gan prasa rūpīgu maržas un fininšu likmju pārvaldību.

Tomēr finanšu hedžēšana risina tikai tirgus risku. Lai izveidotu patiesi izturīgu stratēģiju, lietotājiem jārisina arī viedā līguma risks. Decentralizētie apdrošināšanas protokoli nodrošina nepieciešamo drošības slāni, ļaujot lietotājiem iegādāties pārklājumu platformām, kuras viņi izmanto. Apvienojot short hedžus ar protokola pārklājumu, investori var piedalīties DeFi ienesuma iespējās, minimizējot divus lielākos draudus viņu kapitālam: cenu sabrukumus un koda ekspluatācijas.

Derivāti kompensē tirgus kritumus, kamēr apdrošināšana aizsargā pret platformas hakiem, radot pilnīgu drošības tīklu kripto kapitālam.