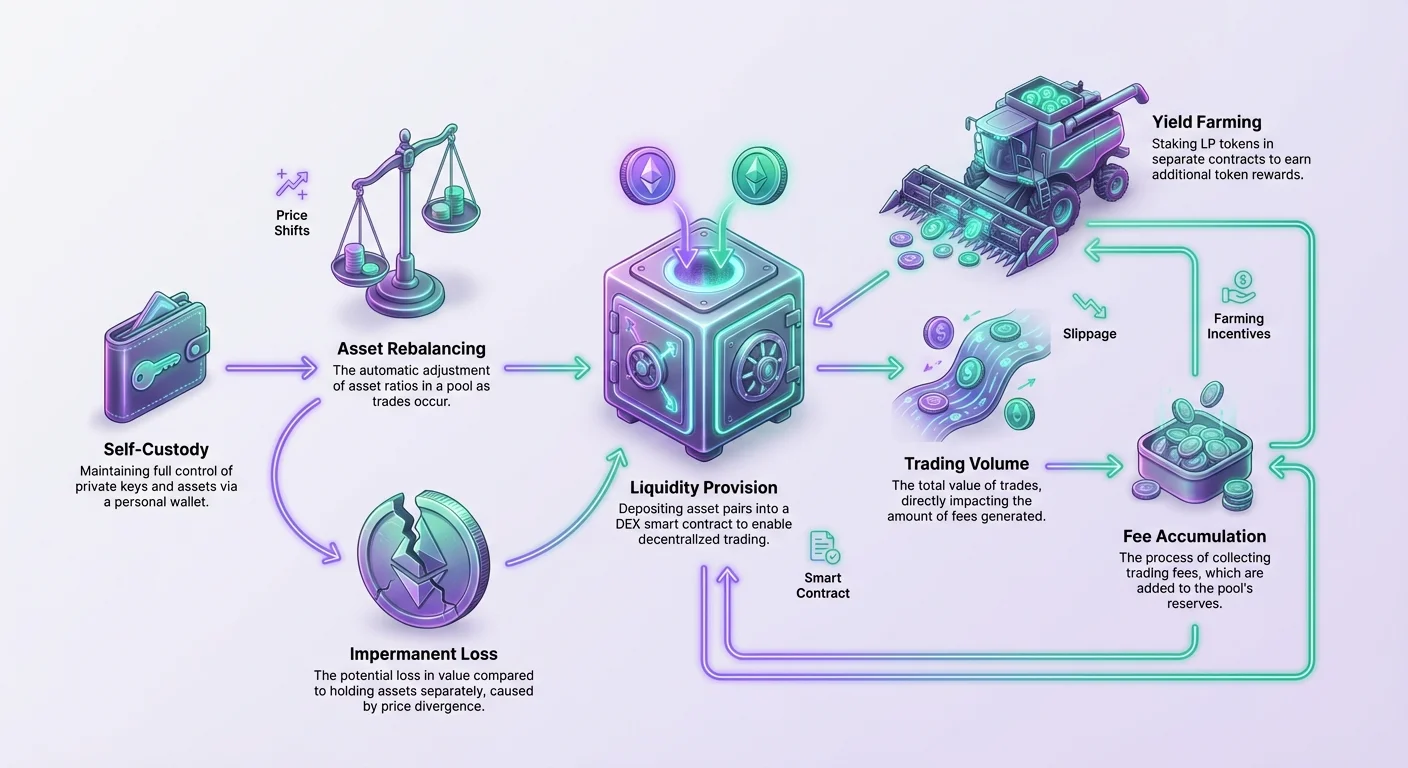

Decentralized finance offers mechanisms for asset owners to put their holdings to work. Rather than letting digital assets sit idle in a wallet, users can provide liquidity to decentralized exchanges. This process facilitates permissionless trading while offering the provider a share of the fees generated by the platform. However, this activity comes with inherent risks associated with market volatility and asset rebalancing.

To navigate these risks effectively, participants must employ specific strategies that go beyond simple depositing. The goal is to ensure that the rewards earned through fees and additional incentives outweigh any potential value changes that occur due to the mechanics of the liquidity pool. Understanding the interplay between trading volume, fee accumulation, and yield farming incentives is essential for anyone looking to maintain a profitable position in these markets.

The core of this activity revolves around the concept of liquidity. In the context of a decentralized exchange, or DEX, liquidity refers to the pool of assets available for traders to swap against. Without a deep reservoir of assets, trading becomes inefficient. Prices slip, and executing large orders becomes difficult without negatively impacting the market rate. DEXs solve this by crowdsourcing liquidity from users, turning them into market makers who earn a return for their service.

The Mechanics of Liquidity Provision

Providing liquidity is the act of depositing assets into a smart contract to facilitate trading for others. This creates a market where users can swap between tokens without needing a centralized intermediary. The protocol governs the pricing and the ratio of assets, ensuring that trades can always be executed as long as there are funds in the pool.

The Automated Market Maker Model

Most decentralized exchanges operate using an Automated Market Maker model. In this system, trading pairs do not rely on an order book of buyers and sellers. Instead, they rely on liquidity pools. A pool is a collection of funds locked in a smart contract. For a standard trading pair, such as VERSE-WETH, the pool holds both assets.

When a user wishes to provide liquidity, they generally must deposit an equal value of both assets. For example, if a user wants to contribute to the VERSE-WETH pool, they cannot simply deposit VERSE. They must calculate the current market value and deposit the equivalent amount of WETH alongside it. This 50/50 value ratio is critical for the mathematical formula that the DEX uses to determine the price of assets during a swap.

Once the assets are deposited, the smart contract takes custody of them. In exchange, the protocol mints a new asset known as a Liquidity Pool token, or LP token. This token acts as a receipt. It represents the user's specific share of the total pool. It is a claim on the underlying assets and any fees that accrue over time.

Asset Rebalancing and Price Shifts

The fundamental risk in this process arises from how the pool handles trades. When a trader swaps one asset for another, they add one type of token to the pool and remove the other. This changes the ratio of assets held in the smart contract. As the ratio changes, the price adjusts automatically to reflect the new scarcity of the removed asset and the abundance of the added asset.

For the liquidity provider, this means the composition of their position changes in real-time. If the price of one asset rises significantly compared to the other, the pool will naturally sell the appreciating asset and buy the depreciating one to maintain the balance. When the provider eventually withdraws their liquidity using their LP token, they will receive a different amount of each asset than they originally deposited.

This shift in asset ratios is the mechanical cause of what is often termed impermanent loss. The value of the withdrawn assets may be lower than if the user had simply held the two assets separately in a wallet. Mitigation strategies focus on ensuring that the income generated from the position is sufficient to cover this potential difference.

The Importance of Fee Revenue

The primary compensation for taking on the risk of asset rebalancing is the exchange fee. On platforms like the Verse DEX, a small percentage of every trade is collected as a fee. Specifically, 0.25% of the trading volume is paid out to liquidity providers. This fee is added directly to the pool, growing the total value of the reserves.

This revenue stream is proportional to the provider's share of the pool. If a user provides 1% of the liquidity, they are entitled to 1% of the fees collected. In a high-volume environment, these fees can accumulate rapidly. The strategy here is to identify pools with sufficient trading volume relative to their size.

If the accumulated fees over the duration of the deposit exceed the loss in value caused by price divergence, the position remains profitable. Therefore, seeking out active trading pairs is a defensive strategy. A stagnant pool with no volume generates no fees, leaving the provider exposed to price volatility with no offsetting income.

Yield Farming as a Strategic Hedge

While trading fees provide a baseline income, they are often insufficient to fully mitigate the risks of high volatility pairs. Advanced mitigation involves layering additional revenue streams on top of standard fee collection. This is where yield farming becomes a critical component of the liquidity provider's toolkit.

Leveraging Farming Incentives

Yield farming allows liquidity providers to put their LP tokens to work. After depositing assets into a pool and receiving the receipt tokens, users can take an additional step. They can deposit these LP tokens into a "farm." A farm is a separate smart contract designed to reward users for keeping their liquidity in the DEX.

The rewards for farming are typically paid in the protocol's native token. For instance, the Verse DEX runs a Verse Ecosystem Incentives program. This program allocates a significant portion of the total token supply to reward community growth. By depositing LP tokens into Verse Farms, providers earn a yield that is separate from and additional to the trading fees.

This secondary yield acts as a powerful hedge. Even if the underlying assets diverge in price, causing a theoretical loss in the principal value, the farming rewards can offset this outcome. In many cases, the Annual Percentage Yield (APY) from farming can be substantial, turning a potentially flat or negative position into a net positive one.

Sustainable Reward Structures

Not all farming opportunities offer the same level of security. Some platforms offer astronomical APYs to attract capital quickly. However, these high rates are often unsustainable. If the rewards are paid in a token that rapidly loses value due to inflation or selling pressure, the mitigation strategy fails.

A robust strategy involves analyzing the source of the rewards. The Verse DEX, for example, allocates rewards linearly on a block-by-block basis. The goal is to incentivize long-term liquidity rather than short-term speculation. The rewards are designed to distribute the token widely while bootstrapping the exchange's functionality.

Investors should look for programs where the APY is attractive but grounded in a long-term distribution model. "Mercenary liquidity" providers often chase the highest possible APY, dump the reward tokens immediately, and then withdraw their liquidity. This hurts the ecosystem. Sustainable farms aim to align the interests of the provider with the health of the DEX.

Calculating Net Position

To effectively mitigate risk, one must look at the total return. The total return is the sum of the trading fees earned plus the value of the farming rewards harvested. This combined total must be compared against the value of the assets if they had been held simply in a wallet.

Farming rewards are dynamic. The APY changes based on how many other people are in the farm. If more people deposit into the farm, the rewards are split among more participants, lowering the individual yield. Conversely, if liquidity leaves, the remaining participants earn a higher share. Monitoring these fluctuations is key to maintaining an efficient hedge.

Selecting the Right Liquidity Pools

The choice of which pair to fund is perhaps the most significant decision a provider makes. Not all pools behave the same way, and the risk profile varies dramatically depending on the assets involved. Strategies for mitigation begin with careful asset selection.

Analyzing Volatility and Correlation

The ideal scenario for a liquidity provider is a pair of assets that move in tandem. If both assets increase or decrease in price at the same time, the ratio between them remains relatively stable. This minimizes the rebalancing that occurs within the smart contract. Stablecoin pairs are the extreme example of this, but they offer lower yields.

When moving beyond stablecoins, users must assess the correlation between the assets. A pair like VERSE-WETH implies that the user is exposed to the price movements of both tokens. If the tokens are uncorrelated—meaning one creates massive gains while the other crashes—the pool will sell the winner to buy the loser. This maximizes the divergence.

Mitigation involves selecting pairs where the user is bullish on both assets long-term. If the user is comfortable holding both VERSE and WETH, the fluctuations in the ratio are less concerning. The provider views the pool as a way to accumulate more of the underperforming asset while earning fees and rewards on the total value.

The Impact of Liquidity Depth

The size of the pool itself, known as its depth, plays a role in risk management. A shallow pool with low liquidity is susceptible to drastic price swings from relatively small trades. This creates a volatile environment where the internal price of the pool can disconnect from the broader market price.

Low liquidity causes slippage. Slippage is the difference between the expected price of a trade and the executed price. In a thin pool, a single large swap can shift the price significantly. For the liquidity provider, this volatility can be dangerous. It creates arbitrage opportunities for traders to extract value from the pool at the expense of the liquidity providers.

Contributing to deeper, more established pools acts as a defensive measure. Deep pools can absorb larger trades with less price impact. This stability protects the provider's principal from wild oscillations that generate losses without generating sufficient fee volume to compensate.

Operational Management of Positions

Successful mitigation is not a "set it and forget it" activity. It requires active management and the use of proper tools to track performance. Users must interact with smart contracts securely and monitor their accruals.

Tracking Rewards and Fees

Modern decentralized exchanges provide analytics pages to help users track their performance. On the Verse DEX, users can view the APY of various pools and track their LP position in the "Pools" tab. Third-party DeFi tools can also be connected to a public address to visualize LP positions across different protocols.

Fees are typically auto-compounded into the pool position. This means the number of LP tokens the user holds remains the same, but the value of underlying assets that those tokens can claim increases. Farming rewards, however, often accumulate in a separate contract and must be claimed.

The timing of claiming rewards can impact the overall return. Since every interaction with a blockchain requires a network transaction fee (paid in the native currency like ETH), claiming rewards too frequently can eat into profits. A strategic approach involves balancing the desire to compound returns with the cost of gas fees.

Understanding Lockup Periods

Flexibility is a crucial component of risk mitigation. If market conditions change rapidly, a provider may need to exit their position to stop losses. Some yield farming protocols impose lockup periods, forcing users to keep their funds deposited for a set time. This prevents the user from reacting to volatility.

The Verse DEX allows for the withdrawal of funds at any time. There is no lockup period for the standard farms. This liquidity is vital. It empowers the provider to un-stake their LP tokens and remove their liquidity from the pool instantly if the market dynamics shift unfavorably. Being able to exit a position on demand is the ultimate stop-loss mechanism.

Self-Custodial Security

All of these strategies rely on the foundation of self-custody. Participating in DeFi requires a digital wallet, also known as a web3 wallet. The best practice is to use a self-custodial wallet, such as the Bitcoin.com Wallet app.

Self-custody means the user retains full control over their private keys and, by extension, their assets. There is no third party to freeze funds or deny withdrawals. However, this also places the responsibility of security on the user. Managing access to the wallet and ensuring sufficient native currency (like ETH) is available for transaction fees is a prerequisite for any advanced strategy.

Apjoma loma maksu ģenerēšanā

Apjoms ir dzinējs, kas nodrošina peļņu likviditātes nodrošinātājiem. Bez tirdzniecības aktivitātes nav maksu. Bez maksām nodrošinātājs tikai pakļauj sevi tirgus riskam bez kompensācijas. Tāpēc apjoma modeļu analīze ir galvenais stratēģiskais elements.

Augstas aktivitātes pāru identificēšana

Augsts APR (Gada Procentuālā Likme) uz panelī var būt maldinošs, ja tas balstās uz ļoti mazu baseinu ar sporādisku tirdzniecību. Visnoturīgākā mazināšanas stratēģija koncentrējas uz pāriem, kas ģenerē konsekventu apjomu. Tas ir tāpēc, ka 0,25% maksa tiek iekasēta no apgrozījuma.

Ja baseins ir ar 100 000 USD likviditāti un veic 10 000 USD ikdienas apjomu, ģenerētās maksas ir pieticīgas. Ja tas pats baseins veic 500 000 USD apjomu, ienākumi ir ievērojami. Nodrošinātājiem jāmeklē baseini, kur apjoma un likviditātes attiecība ir veselīga. Tas norāda, ka kapitāls tiek izmantots efektīvi.

Swingamība kā apjoma dzinējs

Paradoksāli, bet svārstīgums var būt izdevīgs maksu ģenerēšanai. Kad cenas kustas, arbitrāžas boți un tirgotāji kļūst aktīvi, apmainot aktīvus, lai izmantotu cenu starpības. Šī aktivitāte ģenerē apjomu. Ja no šī svārstīguma gūtais maksu ienākums pārsniedz nepastāvīgo zaudējumu, ko izraisa cenas maiņa, nodrošinātājs uzvar.

Briesmas slēpjas „toksiskā plūsmā”, kad cena pastāvīgi pārvietojas vienā virzienā bez atgriešanās. Šajā scenārijā baseins tiek iztukšots no vērtīgā aktīva, un gūtās maksas nav pietiekamas, lai segtu zaudējumus. Ideālā vide ir augsts apjoms ar vidēji atgriezenisku cenu kustību — cenas, kas svārstās strauji, bet atgriežas pie relatīvās bāzes līnijas.

Padziļinātas lauksaimniecības taktikas

Lauksaimniecība ir vairāk nekā tikai žetonu iemaksa. Tā ietver emisijas grafika izpratni un citu dalībnieku uzvedību.

Izplatīšanas periodi un APY

Lauksaimniecības atlīdzības bieži tiek izplatītas pēc noteikta grafika. Verse DEX laukos izplatīšanas periods parasti ir iestatīts uz vienas nedēļas intervāliem. Parādītais APY ir prognoze. Tā pieņem, ka pašreizējie apstākļi saglabāsies perioda garumā.

Tomēr faktiskā atdeve atkarīga no baseina procenta, kas likts laukā. Ja ne visi likviditātes nodrošinātāji cenšas likt savu LP žetonu, atlīdzības tiek sadalītas starp mazāk cilvēkiem. Tas palielina ienesumu tiem, kas piedalās. Viltīgie nodrošinātāji uzrauga dalības līmeni. Ja liels valis ienāk laukā, APY atšķaidās. Ja valsis aiziet, APY pieaug.

Atlīdzību reinvestēšana

Kombinēšanas stratēģija var tālāk mazināt zaudējumus. Tā vietā, lai pārdotu lauksaimniecības atlīdzības (VERSE) par stablecoin, nodrošinātājs var izvēlēties sapārot šīs atlīdzības ar citu aktīvu un atkārtoti ienākt likviditātes baseinā. Tas izveido atgriezenisko saiti, kur pirmās pozīcijas atlīdzības finansē otro pozīciju.

Tas palielina lietotāja kopējo daļu ekosistēmā un diversificē viņa ekspozīciju. Tomēr tas arī palielina ekspozīciju atlīdzību žetonam. Šī pieeja ir agresīva un balstās uz ticību ekosistēmas izaugsmei un žetona vērtības ilgtspējībai ilgtermiņā.

Izpildes tehniskās prasības

Šo stratēģiju īstenošanai nepieciešami specifiski rīki un aktīvi. Pirms risku mazināšanas mēģinājuma jābūt operatīvai kapacitātei, lai efektīvi izpildītu darījumus un iemaksas.

Nepieciešamās sastāvdaļas

| Komponente | Prasība | Funkcija |

|---|---|---|

| Digitālais maciņš | Pašpārvaldnieka | Tur aktīvus un paraksta darījumus |

| Dzimtā valūta | ETH, BCH utt. | Maksā par blokķēdes tīkla komisijām |

| LP žetoni | Pāra specifiski | Iemaksas pierādījums, kas nepieciešams lauksaimniecībai |

Maciņš darbojas kā saskarne. Tam jāspēj droši savienoties ar DEX vietni. Lietotājam jābūt pietiekami kriptovalūtas, lai segtu ne tikai apmaiņas komisijas, bet arī apstiprinājuma darījumus viedajiem līgumiem. Katru reizi, kad lietotājs mijiedarbojas ar jaunu līgumu (kā lauks), jāapmaksā komisija, lai autorizētu šo līgumu tērēt viņa žetonus.

Likviditātes žetona kvīts

LP žetona izpratne ir izsekošanai būtiska. Tas ir standarta žetons, kas atrodas lietotāja maciņā (vai lauka līgumā). Tas nav paši aktīvi, bet kvīts. Ja lietotājs zaudē piekļuvi maciņam, viņš zaudē kvīti un nevar prasīt pamata līdzekļus.

Aktīvu proporcija, kas atgriežas izpirkšanas brīdī, tiek noteikta izņemšanas brīdī. Viedais līgums sadedzina LP žetonu un atbrīvo proporcionālo daļu no baseina pašreizējām rezervēm uz lietotāja maciņu. Šī galīgā samierināšana ir vieta, kur realizētais ieguvums vai zaudējums kristalizējas.

Secinājumi

Likviditātes nodrošināšanas risku mazināšana prasa daudzpusēju pieeju, kas pārsniedz vienkāršu aktīvu alokāciju. Aktīvi piedaloties komisiju ģenerēšanā un ienesīguma lauksaimniecībā, investori var izveidot buferi pret tirgus svārstībām. Tirdzniecības apjoma 0.25% pelnīšanas un papildu ekosistēmas stimulu novākšanas kombinācija kalpo, lai kompensētu neizbēgamās aktīvu proporciju izmaiņas, kas raksturīgas decentralizētajiem tirgiem.

Veiksme balstās uz rūpīgu likviditātes baseinu izvēli, dodot priekšroku tiem ar ilgtspējīgu apjomu un korelētiem aktijiem. Turklāt fermu stratēģiska izmantošana ļauj nodrošinātājiem maksimizēt sava kapitāla lietderību. Operatīvā veiklība — iespēja ieņemt un pamest pozīcijas bez bloķēšanas — nodrošina, ka nodrošinātāji var reaģēt uz mainīgiem tirgus apstākļiem. Galu galā mērķis ir panākt, lai kumulatīvie atlīdzinājumi no komisijām un fermām pārsniegtu jebkuru aktīvu vērtības novirzi.

Aktīva fermu atlīdzību un tirdzniecības komisiju pārvaldība ir primārā aizsardzība pret svārstībām likviditātes baseinos.