Laipni lūdzam digitālo aktīvu jaunajā ērā. Gadiem ilgi kriptovalūtu pasaule darbojās lielākoties ārpus tradicionālās finanšu sistēmas, iegūstot slavu kā “Savage West”. Šī ēra beidzas. Kad kripto nobriest no nišas tehnoloģijas līdz triljona dolāru aktīvu klasei, globālās valdības un regulatīvie orgāni iesaistās, lai definētu iesaistes noteikumus.

Izsmalcinātajam investoram, finanšu profesionālim vai nopietnam pašsaimniecības piekritējam šīs evolucionējošās regulatīvās ainas izpratne vairs nav izvēles jautājums — tā ir kritiska nepieciešamība stratēģiskai efektivitātei, risku pārvaldībai un ilgtermiņa līdzdalībai. Šie noteikumi nosaka, kur jūs varat tirgoties, kā veicat darījumus un kādas saistības jūs uzņematies kā aktīvu turētājs.

Šis visaptverošais ceļvedis pārsniedz vienkāršu darījumu atbilstību, lai sniegtu vooruitredzīgu analīzi par galvenajiem regulatīvajiem ietvariem, kas definē kripto nākotni, īpaši koncentrējoties uz Financial Action Task Force (FATF) vadlīnijām, nozīmīgo Markets in Crypto-Assets (MiCA) regulu Eiropā un gaidāmajām berzes punktiem saistībā ar pašsaimniecību un decentralizēto finansi (DeFi). Šīs regulatīvās vides apgūšana ir atslēga pašsuverenitātes veidošanai digitālajā ekonomikā.

Globālie sargi: FATF izpratne un tās mandāts

Gandrīz visu globālo kripto regulu pamatā ir vajadzība novērst nelikumīgas finanšu darbības, galvenokārt naudas atmazgāšanu un terorisma finansēšanu. Organizācijas, kas nosaka šos starptautiskos standartus, darbojas kā atbilstības arhitekti visā pasaulē.

Kas ir Financial Action Task Force (FATF)?

Financial Action Task Force (FATF) ir neatkarīga starpvaldību organizācija, kas izstrādā un popularizē politiku naudas atmazgāšanas (AML) un teroristu finansēšanas (CFT) apkarošanai. Tā pati nav likumdošanas iestāde; tā nosaka globālos standartus, ko tās dalībvalstis (kurās ietilpst lielākā daļa galveno pasaules ekonomiku) sagaida īstenot caur savām nacionālajām likumdošanas aktiem.

Kad FATF izdod vadlīnijas, tā efektīvi izveido globālu regulatīvo darbību šablonu. Kripto nozarei FATF vadlīnijas ir bijušas transformējošas, prasot valstīm izturēties pret digitālajiem aktīviem un ap viņiem izveidotajām pakalpojumiem ar tiem pašiem stingrajiem atbilstības pasākumiem, kas piemēroti tradicionālajām bankām un finanšu iestādēm.

Virtuālo aktīvu servisa sniedzēju (VASPs) definēšana

FATF nozīmīgākais solis bija noteikt uzņēmumu kategoriju, kas pakļauta tās noteikumiem: Virtual Asset Service Providers (VASPs).

VASP ir jebkura persona vai uzņēmums, kas veic vienu vai vairākas no šādām darbībām vai operācijām cita fiziska vai juridiska persona vārdā:

- Apmaiņa starp virtuālajiem aktīviem un fiat valūtām.

- Apmaiņa starp vienu vai vairākām virtuālo aktīvu formām.

- Virtuālo aktīvu pārskaitīšana.

- Virtuālo aktīvu vai instrumentu uzglabāšana un/vai administrēšana, kas ļauj kontrolēt virtuālos aktīvus.

- Dalība un finanšu pakalpojumu sniegšana, kas saistīti ar emitenta virtuālā aktīva piedāvājumu un/vai pārdošanu.

Praktiski termini ietver centralizētas kriptovalūtu biržas (CEX), piemēram, Coinbase vai Kraken, kripto glabātājus, brokerus un potenciāli pat dažus viesotu maku sniedzējus. Izšķiroši ir tas, ka, tos klasificējot kā VASPs, FATF pakļauj šīs struktūras obligātajam KYC (Know Your Customer) un AML prasībām.

IOSCO kritiskā loma

Kamēr FATF koncentrējas stingri uz AML/CFT, cita galvenā spēlētāja ir International Organization of Securities Commissions (IOSCO). IOSCO spēlē lomu, kas līdzīga globālajam standartu noteicējam vērtspapīru tirgiem.

Ja kriptovalūta tiek uzskatīta par "security" (noteikums, kas atšķiras pa valstīm), IOSCO noteiktie regulatīvie ietvari ir izšķiroši. IOSCO koncentrējas uz investora aizsardzību, nodrošinot tirgus integritāti un samazinot sistēmisko risku. Tās vadlīnijas ietekmē, kā tiek izturēti stablecoins, DeFi aizdevuma protokoli un tokenizēti tradicionālie aktīvi — bieži prasa prospekta atklājumus, pareizu pārvaldību un noteikumus pret tirgus manipulāciju.

Implementing Global Anti-Money Laundering: The FATF Travel Rule

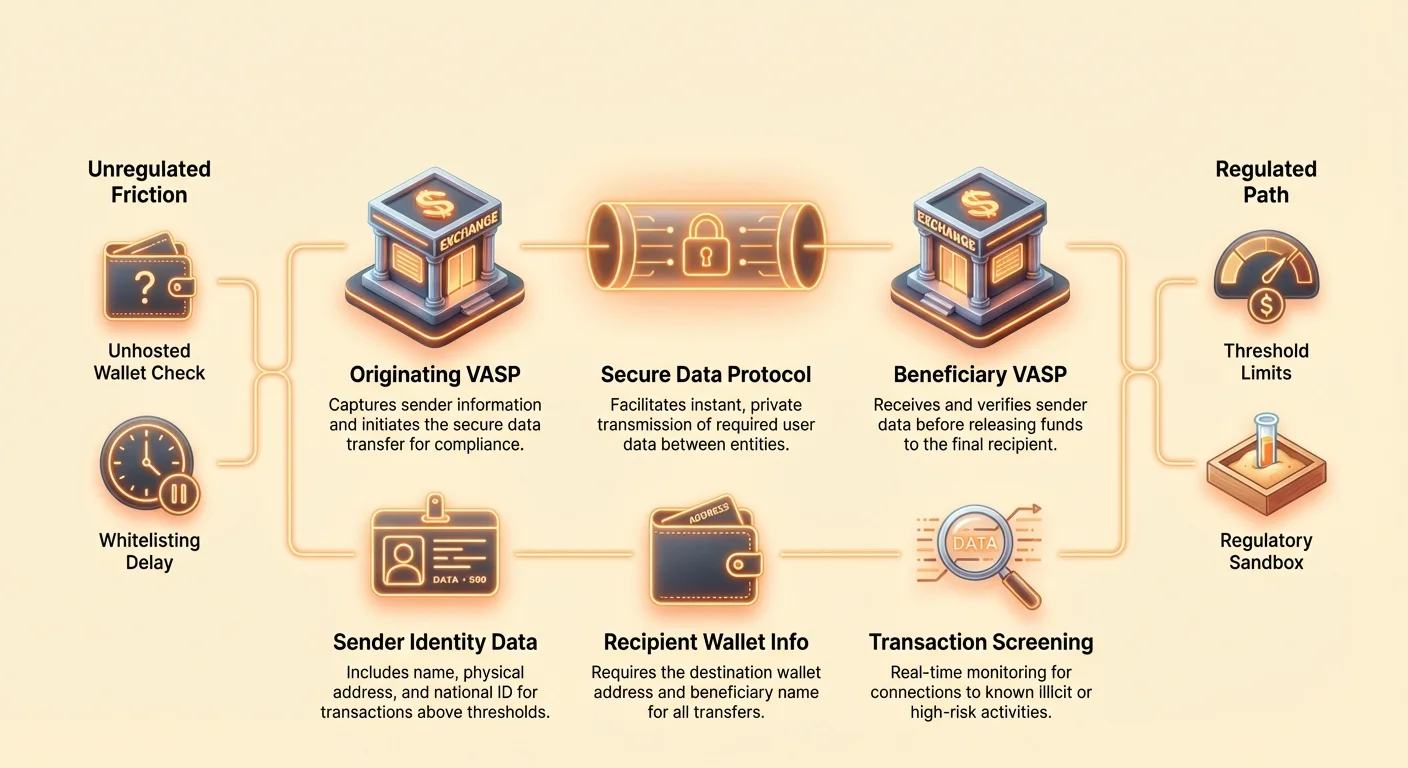

The single most disruptive regulatory implementation derived from FATF guidance is Recommendation 16, often called the "Travel Rule." This rule is designed to prevent bad actors from sending anonymous transfers across VASP platforms.

Deconstructing Recommendation 16

The Travel Rule requires VASPs to obtain, hold, and transmit certain required originator and beneficiary information to the counterparty VASP when transferring digital assets above a specified threshold (typically $1,000 or $3,000, depending on the jurisdiction).

Required Information for the Originator (Sender):

- Name

- Wallet address

- Physical address (or unique national identification number/date and place of birth, depending on jurisdiction)

Required Information for the Beneficiary (Recipient):

- Name

- Wallet address

This regulation mandates that crypto transactions, when moving between regulated entities, must carry identifying data, just like traditional wire transfers. The intent is clear: to ensure traceability of funds across the global ecosystem.

Technology Challenges for Compliance

The Travel Rule poses immense technological hurdles unique to crypto. Traditional banking transfers move slowly (hours or days) and use established, secure message channels (like SWIFT). Crypto transfers are instantaneous, permissionless, and cross-border by default.

To comply, VASPs must implement complex new protocols capable of:

- Counterparty VASP Identification: Determining if the receiving wallet belongs to another regulated VASP, and if so, which one.

- Secure Data Transfer: Sharing sensitive, personally identifiable information (PII) instantaneously and securely outside of the public blockchain network.

- Jurisdictional Segmentation: Handling varying thresholds and data requirements based on the VASP’s location.

Solutions like TRISA (Travel Rule Information Sharing Architecture) and Shyft Network are emerging to facilitate secure, off-chain, peer-to-peer data transmission between VASPs, but achieving global interoperability remains a massive challenge.

Impact on Centralized Exchanges (CEXs)

For users of CEXs, the Travel Rule significantly alters the withdrawal experience. CEXs are required to perform due diligence on destination addresses, leading to practical compliance changes:

- Whitelisting: Many exchanges now require users to "whitelist" or register external wallet addresses (even self-custody wallets) before withdrawing large amounts. This often involves manually verifying ownership or explaining the nature of the transaction.

- VASP-to-VASP Verification: If you send funds from Exchange A to Exchange B, both exchanges must exchange PII about you and the recipient (often yourself, if you own both accounts) before releasing the funds. If the receiving VASP fails to provide the required data, the sending VASP may halt or reject the transaction.

- Withdrawals to Unhosted Wallets: While the Travel Rule doesn't strictly prevent withdrawals to unhosted wallets, it requires the originating VASP to gather detailed information about the user sending the funds and often requires enhanced due diligence for transactions above the threshold.

Practical Guide to Travel Rule Compliance for Users

For the strategic crypto holder, navigating the Travel Rule requires preparation:

- Expect Delays: High-value transfers between CEXs, especially international ones, may no longer be instant. Budget time for the required VASP verification handshake.

- Verify Destination: If sending funds to another VASP account you own, ensure the receiving exchange supports the Travel Rule compliance protocol used by the sender.

- Maintain Documentation: Keep clear records of large transfers, especially when moving assets from a CEX to your self-custody wallet, as the CEX may request proof that you are the beneficial owner of the destination address.

- Threshold Awareness: Be mindful of local Travel Rule thresholds. Breaking a large transaction into smaller, separate transfers to avoid the threshold is often considered "structuring" and can flag regulatory scrutiny.

Europe’s Landmark Legislation: The Markets in Crypto Assets Regulation (MiCA)

While FATF provides the framework for global anti-money laundering, the Markets in Crypto Assets Regulation (MiCA) proposed by the European Union is the most comprehensive, jurisdiction-specific legal framework for digital assets yet devised. MiCA is set to fully apply across the EU by late 2024/early 2025 and is acting as a global template for holistic crypto regulation.

MiCA’s Scope and Purpose

MiCA’s primary goal is not just to prevent money laundering, but to establish legal certainty, support innovation, and protect consumers across the entire EU single market. Before MiCA, crypto firms had to adhere to 27 different sets of national laws. MiCA harmonizes these rules, creating a "passporting" system similar to traditional finance, allowing licensed crypto firms to operate across all EU member states with a single authorization.

The regulation covers three major categories of digital assets:

- Asset-Referenced Tokens (ARTs): Tokens backed by several fiat currencies or assets (like a basket of currencies).

- E-Money Tokens (EMTs): Tokens primarily backed by a single fiat currency (like EUR or USD stablecoins).

- Utility Tokens: Tokens intended to provide access to a good or service.

Significantly, Bitcoin and Ethereum (when used as pure decentralized assets without an identifiable issuer) are generally exempted from MiCA’s issuance rules, but the service providers handling them must still comply.

Key Requirements for Issuers and Service Providers

MiCA imposes rigorous requirements on any entity seeking to issue tokens or provide crypto services within the EU:

1. Authorization and Governance

Crypto Asset Service Providers (CASPs—MiCA’s version of VASPs) must obtain authorization from a national regulatory authority. This requires robust governance rules, clear organizational structures, and minimum capital requirements designed to ensure the CASP can withstand operational and market risks.

2. Investor Protection and Disclosure

For token issuers, MiCA introduces requirements for publishing a detailed "crypto-asset white paper." This paper must be filed with regulators, outline the risks, features, and technology, and be presented fairly and accurately. Misleading information could lead to civil liability. This mimics traditional prospectus requirements for securities.

3. Stablecoin Regulation

MiCA imposes stringent rules on stablecoins (ARTs and EMTs), requiring issuers to maintain a legal entity in the EU, hold adequate and liquid reserves (1:1 backing), and undergo regular audits. This regulation is crucial for managing the systemic risks associated with large, widely used stablecoins.

MiCA and Unhosted Wallet Transactions

One of MiCA’s most controversial extensions deals with transfers involving unhosted wallets (sometimes called self-custody or non-custodial wallets). While FATF guidelines recommend VASP reporting, MiCA—along with new, stringent updates to the EU’s Anti-Money Laundering Regulation (AMLR)—has adopted rules that dramatically increase scrutiny:

- Mandatory Identity Verification: Transfers of any amount (zero threshold) between a CASP (e.g., a CEX) and an unhosted wallet must be verified. If a user tries to withdraw funds from a CEX to an unhosted wallet, the CEX must now verify that the user controls that self-custody wallet.

- Enhanced Monitoring: For transfers exceeding €1,000 to an unhosted wallet, CASPs must implement enhanced due diligence and monitoring, including checking the source of funds and the destination address for ties to known illicit activities.

- The "Sunrise Issue": These comprehensive requirements pose significant integration problems, especially concerning the automatic collection of PII, solidifying the regulatory wall between the centralized ecosystem and self-custody.

MiCA and Global Precedent

MiCA is often cited by regulators in the US, UK, Singapore, and other major financial hubs. Its comprehensiveness and pan-national scope make it the de facto global gold standard for balancing innovation with regulation. Countries drafting their own legislation often use MiCA as a starting point, meaning its structure is likely to influence policy worldwide for the next decade.

The Frontier of Friction: Decentralization Meets Compliance

The core tension in crypto regulation exists at the interface between centralized, identifiable institutions (VASPs/CASPs) and decentralized, pseudonymized systems (DeFi, P2P networks, and self-custody wallets). Regulators are adapting their rules to reach into these previously unregulated spaces.

The Regulatory Treatment of Unhosted (Self-Custody) Wallets

An unhosted wallet (like MetaMask, Ledger, or Trezor) is a wallet where the user, and only the user, holds the cryptographic private keys. Regulators view transactions involving these wallets as high risk because they are inherently outside the purview of the regulated VASP ecosystem.

The goal of regulators is generally not to outlaw self-custody, but to prevent it from becoming a funnel for anonymous criminal finance. The key regulatory push, highlighted by MiCA and the enforcement of the Travel Rule, is to make the transfer out of the regulated space subject to severe scrutiny.

Implications for the User: If you routinely transfer large sums from a CEX to your self-custody wallet, expect more intrusive questions about the source of the funds and mandatory, verifiable proof that you own and control the receiving wallet. This creates a compliance burden aimed at deterring actors who wish to "off-ramp" or "on-ramp" anonymously through the decentralized ecosystem.

Challenges for P2P and DEX Activity

Peer-to-Peer (P2P) exchanges and Decentralized Exchanges (DEXs) are the most difficult entities for regulators to capture under the VASP model because there is often no central intermediary.

P2P Exchanges

In pure P2P trading, two individuals transact directly. Since there is no VASP facilitating the exchange, there is no regulated entity to enforce KYC/AML. Regulatory efforts often target the software providers or the interface developers who build the P2P marketplace, attempting to classify them as service providers, even if they never hold custody of the funds.

Decentralized Exchanges (DEXs)

DEXs operate via automated smart contracts. Who exactly is the VASP? The liquidity providers? The protocol founders? The front-end interface operators?

Regulatory focus has shifted to the accessible, centralized elements surrounding the protocol:

- Front-End Regulation: Regulators increasingly target the centralized web interface (the URL) that makes interacting with the DEX easy. If an interface operator restricts access based on geographical location or imposes KYC barriers to use their front-end, they might be classified as a regulated service.

- Gateway Providers: Services that bridge DeFi with traditional finance (e.g., tokenizing real-world assets or providing fiat on-ramps) are clearly VASPs and subject to full compliance.

- Protocol Founders/Developers: If developers maintain significant control over the protocol (e.g., multisig control over treasury funds or upgrade keys), they risk being treated as the regulated entity, forcing them to implement KYC at the protocol level—a concept often antithetical to DeFi principles.

The Impact of U.S. Legislation and Infrastructure

While MiCA sets the framework for Europe, the U.S. approach—often delivered through interpretations by agencies like the SEC and FinCEN—focuses on classifying assets and activities.

The implications stemming from the U.S. Infrastructure Bill, which initially sought to broadly define "broker" to include miners, developers, and protocol operators, illustrate the regulatory intent to cast a wide net. Although the final wording was softened, it signaled a clear future where any party profiting from facilitating crypto transactions will be pressured toward compliance. This ambiguity means that highly sophisticated users must constantly monitor court rulings and agency guidance to avoid legal risk.

Strategic Implications for the Self-Sovereign User

As regulatory scrutiny intensifies, self-sovereignty requires responsible action:

- Audit Your Assets: Understand which of your assets (e.g., stablecoins, utility tokens, governance tokens) might fall under securities laws or MiCA requirements in different jurisdictions.

- Isolate Transactions: Avoid "commingling" funds between wallets used for high-risk DeFi activity (which might later be scrutinized) and wallets used for transparent, compliant interactions with CEXs.

- Compliance Bridge: When moving funds from a regulated CEX to an unhosted wallet, treat the CEX interaction as the required compliance check-point. Ensure the CEX has all necessary KYC/AML data before the withdrawal.

- Understand Jurisdiction: Recognize that using a DEX front-end hosted in a different country does not necessarily shield you from the laws of your own jurisdiction.

Nākotnes navigēšana: Regulatīvā inovācija un stratēģiskā atbilstība

Attiecības starp regulatoriem un kripto nozari nav tīri antagonistiskas. Daudzas jurisdikcijas aktīvi meklē veidus, kā iekļaut blokķēdes tehnoloģiju, vienlaikus mazinot riskus. Šī pieeja veicina inovāciju, leģitimitāti un galu galā institucionālu uzticību.

Regulatīvie smilškastes un inovāciju centri

"Regulatīvais smilškaste" ir definēta telpa, kur uzņēmumi var testēt inovatīvus produktus, pakalpojumus un biznesa modeļus zem atvieglotām regulatīvām prasībām. Regulators uzrauga šos testus, ļaujot uzņēmumiem eksperimentēt ar jaunām tehnoloģijām (piemēram, Travel Rule īstenošanu sarežģītā P2P struktūrā), ne uzreiz gūstot pilnu atbilstības izmaksu slogu.

Vērtība nozarei:

- De-riskošana inovācijai: Ļauj startup uzņēmumiem nodrošināt, ka viņu tehnoloģija ir atbilstoša pirms pilnas tirgus palaišanas.

- Regulatīvā izglītība: Palīdz regulatoriem mācīties, kā jauni DeFi protokoli darbojas reālos scenārijos.

- Talantu piesaiste: Jurisdikcijas ar aktīvām smilškastēm (piemēram, Lielbritānija, Singapūra vai Šveices daļas) piesaista inovatīvus uzņēmumus, kas meklē skaidras regulatīvās vadlīnijas.

Šo smilškastu izveide demonstrē globālu atzīšanu, ka simtgadīgus banku likumus tieši piemērot programmējamai naudai ir nepraktiski, nepieciešot pielāgotus, inovatīvus atbilstības risinājumus.

Atbilstība kā konkurences priekšrocība

Izsmalcinātiem lietotājiem un institucionāliem investoriem regula nav tikai šķērslis — tā ir filtrēšanas mehānisms, kas nes ticamību. Institucionālais kapitāls, pensiju fondi un lielu korporāciju kases prasa regulatīvu skaidrību un atbilstības garantijas pirms ienākšanas aktīvu klasē.

Ietvaru kā MiCA īstenošana signalizē tirgus briedumu, samazina pretējas puses risku un atvieglo auditētu, regulētu finanšu produktu izveidi (piemēram, crypto ETF vai strukturētos derivātus).

Stratēģiskais secinājums: Uzņēmumi un indivīdi, kas pieņem un apgūst sarežģītu atbilstību — piemēram, integrējot progresīvus Travel Rule risinājumus vai uzturot metikulozus auditus — būs pirmie, kas piesaistīs regulētus institucionālos partnerus un kapitāla plūsmu. Atbilstība pārvēršas no izmaksu centra uz galveno konkurences priekšrocību.

Nākotnes atbilstības tendences, ko uzraudzīt

Lai būtu priekšā regulatīvajai līknei, jāseko līdzi specifiskām jomām, kas, visticamāk, attīstīsies ātri:

- DeFi un AI vadīta uzraudzība: Regulators arvien vairāk paļausies uz sarežģītām blokķēdes analītikām un AI rīkiem, lai uzraudzītu DeFi protokolus aizdomīgai aktivitātei, koncentrējoties mazāk uz individuālo identitāti un vairāk uz plūsmu nelikumīgiem līdzekļiem. Tas nozīmē, ka protokola mijiedarbības, kas saistītas ar augsta riska adresēm, tiks atzīmētas neatkarīgi no lietotāja KYC statusa.

- Globālā harmonizācija: Gaidiet lielāku sadarbību starp FATF dalībvalstīm, lai standartizētu Travel Rule īstenošanu, padarot bezšuvju VASP-uz-VASP komunikāciju obligātu visā pasaulē.

- Zaļā atbilstība: Sekojot MiCA vadībai, mēs sagaidām lielāku spiedienu uz kripto pakalpojumu sniedzējiem (īpaši mining un staking kopām), lai atklātu un mazinātu vides ietekmi, pārvēršot ilgtspējību atbilstības prasībā.

- Nodokļu integrācija: Regulatīvās iestādes (piemēram, OECD) spiedz uz automatizētu informācijas dalīšanos par kripto turējumiem un darījumiem. Tas savieno regulatīvo sfēru (KYC/AML) tieši ar nodokļu atbilstības sfēru, padarot visaptverošu globālu nodokļu ziņošanu obligātu.

Secinājums

Pāreja no neregulētas sektora uz definētu finanšu nozari ir izšķiroša digitālo aktīvu ilgtermiņa dzīvotspējai. Ietvari kā FATF Travel Rule un ES MiCA pārstāv fundamentālas pārmaiņas, pārvietojot kripto prom no nišas anonimitātes uz globālu, regulētu atbildību.

Nopietnam kripto dalībniekam šis regulatīvais padziļināts pārskats uzsver vienu patiesību: pašsuverenitāte digitālajā ekonomikā tiek sasniegta nevis izvairoties no regulas, bet apgūstot atbilstību. Izprotiet galvenos globālo standartu noteicēju mandātus, stratēģiski navigējiet berzes punktos starp centralizāciju un decentralizāciju, un pieņemiet vooruitredzīgas labākās prakses, lietotāji var nodrošināt savu ilgtspējīgu, drošu un atbilstošu līdzdalību finanšu nākotnē.