Ceļš kriptovalūtās bieži sākas ar aizraušanos par decentralizēto tehnoloģiju un eksplozīvo izaugsmes potenciālu. Tomēr, kad portfeļi nobriest un tirdzniecības apjoms pieaug, iestājas izšķiroša realitāte: nodokļu sekas. Daudziem nodokļu ziņošana tiek uzskatīta tikai par atbilstības pienākumu — nepieciešamu ļaunumu, lai izsekotu ieguvumiem un ziņotu par tiem precīzi.

Tomēr pārejot no pamata atbilstības uz stratēģisku nodokļu plānošanu, fundamentāli mainās jūsu peļņa. Tas nav par nodokļu izvairīšanos; tas ir par legālu un efektīvu jūsu aktīvu pārvaldības un darījumu plūsmas strukturēšanu, lai minimizētu saistības. Stratēģiski izmantojot sarežģītas grāmatvedības metodes, piemēram, Specific Identification, un aktīvi veicot nodokļu zaudējumu novākšanu, jūs varat ievērojami samazināt summu, kas jānomaksā nodokļu iestādēm, saglabājot kapitālu nākamām investīcijām.

Šis ceļvedis pārsniedz vienkāršu jūsu kopējā nodokļu rēķina aprēķināšanu. Mēs izpētīsim uzlabotas metodes un stratēģijas, ko izmanto gudri kripto investori, lai optimizētu savus finanšu rezultātus visa gada garumā, nodrošinot, ka katrs darījums tiek skatīts caur dubultu prizmu — tirgus iespējas un nodokļu efektivitāti. Šo konceptu apgūšana ir izšķirošs solis ceļā uz pašsuverenitāti digitālajā ekonomikā, pārvēršot nodokļu sezonu no stresa pilnas steigas stratēģiskā priekšrocībā.

Pamats: Kapitāla pieaugums un optimizācijas domāšana

Lielākajā daļā galveno jurisdikciju kriptovalūtas tiek uzskatītas par īpašumu, nevis valūtu. Šī pamatklasifikācija nozīmē, ka katru reizi, kad jūs apmaināt vienu kriptovalūtu pret otru, apmaināt kriptovalūtu pret fiat valūtu vai izmantojat kriptovalūtu preču vai pakalpojumu iegādei, jūs parasti realizējat kapitāla pieaugumu vai zaudējumu. Kapitāla pieauguma mehānikas izpratne ir jebkuras optimizācijas stratēģijas priekšnoteikums.

Iegādes vērtības imperatīvs

Jūsu iegādes vērtība ir kopējā cena, ko maksājāt par aktīvu, ieskaitot visas nodevas vai komisijas maksas, kas nepieciešamas tā iegūšanai. Kad jūs pārdodat aktīvu, apliekamais gadījums ir starpība starp pārdošanas cenu (iegūtajiem līdzekļiem) un jūsu iegādes vērtību.

- Peļņa: Iegūtie līdzekļi > Iegādes vērtība

- Zaudējums: Iegūtie līdzekļi < Iegādes vērtība

Ja jūs nopērkat 1 ETH par $2,000 un vēlāk pārdodat par $3,500, jūsu realizētā peļņa ir $1,500. Šī $1,500 ir tas, ko apliklē nodokļu iestādes. Nodokļu optimizācijas stratēģiju galvenais mērķis nav samazināt pārdošanas cenu, bet stratēģiski pārvaldīt, kura specifiskā iegādes vērtība tiek salīdzināta ar šo pārdošanas cenu.

Īstermiņa pret ilgtermiņa priekšrocība

Nodokļu minimizēšana tiek būtiski ietekmēta no jūsu aktīvu turēšanas perioda. Parasti nodokļu iestādes atšķir aktīvus, kas turēti mazāk nekā gadu (īstermiņa), un tos, kas turēti gadu vai vairāk (ilgtermiņa).

- Īstermiņa peļņa: Bieži apliekama ar jūsu parasto ienākuma nodokļa likmi, kas var būt augsta (potenciāli 30% vai vairāk, atkarībā no jūsu ienākumu grupas).

- Ilgtermiņa peļņa: Parasti apliekama ar labvēlīgākām, zemākām likmēm (dažās valstīs šīs likmes ir ievērojami samazinātas vai pat nulle noteiktiem ienākumu līmeņiem).

Stratēģisks padoms: Visnozīmīgākā optimizācijas stratēģija ir pacietība. Aktīvu turēšana ilgāk par gada atzīmi pārvērš augsti apliekamos parastos ienākumus zemāk apliekamos ilgtermiņa kapitāla pieaugumos, piedāvājot vislielāko nodokļu ietaupījuma potenciālu investoriem, kas koncentrējas uz uzkrāšanu.

Inventory Accounting Methods: The Core of Optimization

When you buy a single cryptocurrency like Bitcoin or Ethereum multiple times over many years, you end up holding several distinct "lots," each purchased at a different price. When you decide to sell 1 ETH, how do you determine which specific $2,000-cost-basis lot gets matched with the sale? This is where inventory accounting methods come into play, and the method chosen can dramatically affect your realized tax liability.

FIFO (First-In, First-Out)

FIFO is the default method used by many tax jurisdictions and reporting software unless you specify otherwise. It operates on the simple principle that the very first unit you bought is the first unit you sell.

- How it works: When you sell 1 BTC, FIFO dictates that you match that sale against the oldest available BTC in your portfolio.

- Tax Implication (Rising Market): If the market has trended upward over time, the oldest coins will likely have the lowest cost basis. Matching a low cost basis against a high sale price results in the highest possible realized capital gain, meaning FIFO is generally the least tax-efficient method in a sustained bull market.

- When it's useful: FIFO is straightforward, easy to track, and may be preferred if you primarily want to ensure your older coins qualify for the preferential long-term capital gains rate.

LIFO (Last-In, First-Out)

LIFO assumes that the most recently acquired units are the first ones sold.

- How it works: When you sell an asset, LIFO matches that sale against the newest available lot in your portfolio.

- Tax Implication (Rising Market): If the market has been rising, your most recent purchases will have the highest cost basis. Matching a high cost basis against a sale price results in the lowest realized gain (or potentially a smaller loss), thus deferring tax.

- Regulatory Status: LIFO is generally not an accepted method for tax reporting in many major jurisdictions (including the USA, for tax purposes generally). This restriction is in place because it allows businesses to artificially depress taxable income during inflationary periods. Always verify the legality of LIFO in your specific tax jurisdiction before attempting to use it.

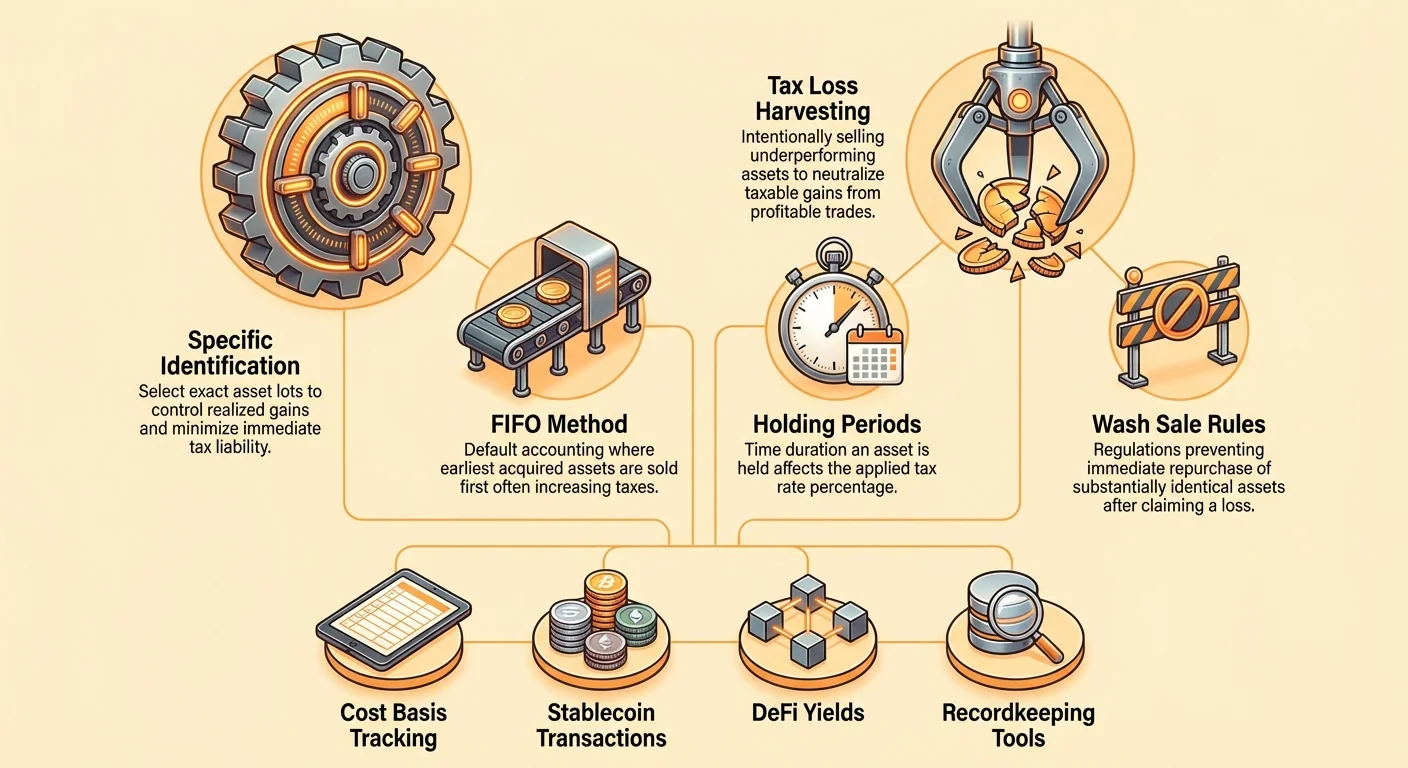

Specific Identification (Spec ID)

Specific Identification (Spec ID) is the gold standard for crypto tax optimization. It allows you to choose exactly which lot (i.e., which specific buy transaction) you wish to sell at the moment of the transaction realization.

The Power of Choice: Instead of being locked into an arbitrary sequence (like FIFO or LIFO), Spec ID gives you control to achieve specific tax goals:

- Goal: Minimize Tax Today (Loss Realization): If you are selling BTC for cash, you can choose to sell the lot that has the highest cost basis (perhaps a purchase made during a recent market high). This minimizes your gain or maximizes your loss, reducing your immediate tax bill.

- Goal: Maximize Long-Term Holding: If you have several lots, some held for 10 months (short-term) and some held for 14 months (long-term), you can choose to sell only the 14-month lots to take advantage of the lower long-term capital gains rate.

- Goal: Zero Out a Gain (Tax Neutrality): If you realized a $500 short-term gain earlier in the year, you can choose to sell a different lot that currently carries a $500 short-term loss, making the net outcome zero for that tax category.

Requirement for Spec ID: To legally use Spec ID, you must maintain impeccable records demonstrating that you specifically identified the asset lot at the time of the sale. This is often handled through integrated crypto accounting software that allows you to tag or select lots prior to generating the tax report. Without rigorous recordkeeping, tax authorities will default you to FIFO.

Deep Dive: Strategic Tax Loss Harvesting

Tax loss harvesting is a proactive strategy that takes advantage of market dips. Instead of simply waiting for your assets to recover, you intentionally sell assets currently trading at a loss to offset any realized gains you have accrued throughout the year.

This strategy is particularly powerful in volatile markets like crypto, where sharp price movements are common. It allows you to "capture" the loss value for tax purposes without necessarily abandoning your investment position.

Definition and Mechanism

Tax loss harvesting involves three steps:

- Identify Realized Gains: Determine the amount of profits you have already realized this year (e.g., from profitable trades, exchange swaps, or selling stablecoins).

- Identify Unrealized Losses: Find assets in your portfolio whose current market value is lower than their cost basis.

- Execute the Harvest: Sell the assets with the unrealized loss. This converts the unrealized loss into a realized capital loss.

The core optimization step is realizing losses, which are then used to reduce or completely eliminate realized capital gains.

Example Use Case:

- Scenario: You sold ETH in March for a $10,000 short-term gain (highly taxed). Later, in October, your portfolio holds 5 BTC purchased for $50,000 each, now trading at $40,000.

- Harvesting Action: You sell those 5 BTC. You realize a $10,000 loss (5 x $10,000 loss per coin).

- Result: This $10,000 realized loss offsets the $10,000 realized short-term gain, reducing your net taxable short-term capital gain to $0 for the year.

When and How to Harvest Effectively

While tax loss harvesting can be done anytime, its effectiveness is optimized when used against short-term gains, which are taxed at higher ordinary income rates.

- Target High-Tax Gains First: Use harvested losses to cancel out short-term gains first. If you still have excess losses, they can then offset long-term gains.

- The $3,000 Annual Deduction: If your total realized losses exceed your total realized gains, in jurisdictions like the US, you are typically permitted to deduct up to $3,000 of the net loss against your ordinary income (wages, salary). Any remaining loss is carried forward indefinitely to offset future capital gains.

- End-of-Year Timing: While you can harvest anytime, many investors execute large harvesting events in the final weeks of the calendar year. This ensures they have a clear picture of their total gains and losses before the tax filing deadline.

Mitigating Risk: The Substitute Asset Strategy

The primary risk of tax loss harvesting is that you liquidate an asset, and immediately afterward, its price spikes, causing you to miss out on the recovery. To manage this, smart harvesters employ the "substitute asset" strategy.

Instead of simply selling the asset and waiting 31 days (if wash sale rules applied, see next section), you immediately rotate the proceeds into a different asset that tracks the same sector or movement but is not technically identical.

- Action: Sell BTC for a loss.

- Immediate Reinvestment: Immediately use the proceeds to buy an equivalent amount of ETH or a BTC-correlated ETF (if available and regulatory compliant).

This approach maintains your exposure to the crypto market upside while realizing the necessary loss for tax purposes. If BTC recovers, ETH or the correlated asset likely will, too, preserving your overall market position.

Navigating Wash Sale Rules: Compliance and Strategy

Tax loss harvesting must be performed with careful consideration of the Wash Sale Rule. This rule is designed to prevent taxpayers from harvesting losses purely for tax purposes without genuine economic change.

The Traditional Wash Sale Rule

In traditional securities markets (stocks, bonds), the Wash Sale Rule prohibits an investor from claiming a loss if they buy the same or a "substantially identical" security within 30 days before or 30 days after the date of sale (a 61-day window). If a wash sale occurs, the loss is disallowed for tax purposes, and the disallowed loss is added to the cost basis of the newly acquired security.

The Crypto Gray Area (USA)

As of the writing of this guide, cryptocurrencies are generally exempt from the traditional Wash Sale Rule in the United States. Since crypto is typically classified as property rather than stock or security, the IRS rule designed for securities does not automatically apply.

The immense strategic implication of this exemption is that U.S. investors can sell BTC at a loss and buy the exact same amount of BTC back one minute later, realize the loss for tax purposes, and retain their position in the market.

CRITICAL WARNING: This exemption is a significant loophole that major governments, including the US, are actively seeking to close. Legislative proposals aimed at applying wash sale rules to digital assets have been introduced.

- Actionable Advice: Treat the absence of wash sale rules as a temporary advantage. If you execute a loss harvest, be prepared for potential future rule changes that could retroactively impact compliance, though this is unlikely. For extreme certainty, adopt the substitute asset strategy discussed above, which insulates you regardless of future wash sale legislation.

Global Variations and Superficial Losses

While the US stands out in its current exemption, many other jurisdictions have similar rules that effectively limit aggressive loss harvesting:

- Canada: Canada employs the Superficial Loss Rule. This rule is broader than the US wash sale rule and applies to many types of property, including crypto. If you repurchase the same asset or a similar asset within 30 days, the loss will be disallowed. Canadians must therefore employ the substitute asset strategy strictly.

- United Kingdom/Australia: These jurisdictions have their own complex rules regarding losses and holding periods. Always consult with a tax professional familiar with your local jurisdiction’s specific definitions of “security” and “property.”

Minimizing Taxes on Everyday Transactions

Most crypto investors focus optimization efforts on large sales, neglecting the dozens of small, often overlooked taxable events that occur daily, particularly involving stablecoins and decentralized finance (DeFi).

The Stablecoin Trap

Stablecoins (like USDC, USDT, DAI) are essential tools for traders because they allow them to exit volatility without converting back to fiat currency. However, a common misconception is that using stablecoins is tax-neutral.

The Reality: If you held ETH and traded it directly for USDC, that transaction is typically a taxable event (ETH-to-USDC is a crypto-to-crypto trade). If the ETH had gained value since you acquired it, you realize a capital gain, even though you immediately moved into a stable asset.

Strategy for Minimizing Stablecoin Taxes:

- Use Spec ID for Stablecoin Conversions: If you need to convert $10,000 worth of BTC into USDC to sit out a volatile period, use the Specific Identification method. Select the BTC lots that have the highest cost basis (or even a loss) to minimize the gain realized upon conversion.

- Purchase Stablecoins with Fiat: If possible, acquire new stablecoins directly using fresh fiat currency. Since the cost basis of the fiat equals the acquisition price of the stablecoin, the initial transaction incurs zero capital gain. You now have tax-free ammunition for trading.

- Minimize Transaction Volume: If you constantly move assets in and out of stablecoins on an exchange, you generate hundreds of taxable events. Consolidate your trading to fewer, more impactful moves to simplify tracking and reporting.

Managing DeFi and Yield Taxes

Interacting with DeFi protocols (staking, providing liquidity, lending) can generate both capital gains and ordinary income, requiring unique strategies:

- Rewards as Income: Income derived from staking rewards, interest, or mining is typically taxed as ordinary income at the moment it is received (or becomes controllable), based on its fair market value at that time.

- Capital Gains on Rewards: If you receive 1 ETH as a staking reward (valued at $3,000 at receipt), your cost basis for that ETH is $3,000. If you sell it later for $4,000, the $1,000 difference is a capital gain.

Optimization Strategy for Yield: Use your oldest, lowest cost basis gained assets (like rewards) first when harvesting losses or needing to realize minimal gains. Since their cost basis is often $0 (if earned via mining/airdrop, and thus only taxed upon receipt), holding them long-term is especially beneficial.

Gifting and Donations

Gifting crypto to family members or donating to charitable organizations can be highly tax-efficient strategies (depending on local regulations regarding gift/estate tax thresholds).

- Charitable Donation (USA Context): If you donate crypto that you have held for more than one year (long-term capital asset), you generally do not have to pay capital gains tax on the appreciation. Furthermore, you may be able to deduct the full fair market value of the donation from your taxable income, effectively providing a double tax benefit.

- Gifting to an Individual: Gifting crypto is usually not a taxable event for the giver (up to annual and lifetime limits). The recipient inherits the giver's cost basis, meaning when the recipient eventually sells, they will be responsible for the capital gains realized from the original purchase price. This can be a strategic way to transfer appreciated assets to family members who may be in a lower income tax bracket.

Stratēģijas īstenošana: Rīki un uzskaite

Labākās nodokļu optimizācijas stratēģijas ir bezjēdzīgas bez precīziem, detalizētiem un verificējamiem ierakstiem. Pāreja no vienkāršas biržas tirdzniecības uz sarežģītām DeFi mijiedarbībām, vairākiem maciņiem un cross-chain apmaiņām eksponenciāli palielina uzskaites grūtību.

Pareizās uzskaites programmatūras izvēle

Mūsdienu kripto nodokļu programmatūras platformas vairs nav tikai kalkulatori; tās ir sarežģīti atbilstības un optimizācijas rīki. Izvēloties platformu, prioritizējiet funkcijas, kas ļauj sarežģītu stratēģisko plānošanu:

- Atbalsts specifiskajai identifikācijai (Spec ID): Tas ir galvenais. Programmatūrai jāļauj piešķirt specifiskas partiju ID pārdojumiem un izsekot izmaksu bāzi tūkstošiem darījumu bezšuvīgi. Ja platforma pēc noklusējuma izmanto tikai FIFO un nepiedāvā Spec ID funkcionalitāti, tā stipri ierobežo jūsu optimizācijas potenciālu.

- Plaša integrācija: Platformai jāconnectē caur API vai CSV augšupielādi uz visām jūsu centralizētajām biržām (CEX), nekustīgajiem maciņiem (pašuzglabāšana) un sarežģītiem DeFi protokoliem (piem., aizdevumi, staking un likviditātes baseini).

- Jurisdikcijas atbalsts: Pārliecinieties, ka platforma precīzi aprēķina nodokļus, balstoties uz jūsu konkrētās valsts noteikumiem (piem., apstrādājot Superficial Loss noteikumu Kanādai vai sarežģītu ienākumu kategorizāciju Lielbritānijai).

- Darījumu marķēšana un klasifikācija: Rīkam jāļauj manuāli pārskatīt un marķēt darījumus (piem., atšķirot «apmaiņu» (apliekams pārdojums) no «pārskaitījuma» (neapliekama kustība starp jūsu paša maciņiem), vai pareizi klasificēt Airdropus, ICO un dāvanas).

Labākās prakses tīriem datiem

Atkritumi iekšā, atkritumi ārā. Jūsu nodokļu ziņojumu precizitāte — un tādējādi jūsu optimizācijas efektivitāte — pilnībā ir atkarīga no jūsu pamatdatu pilnīguma un pareizības.

- Izsekot maciņu pārskaitījumus precīzi: Katru reizi, kad jūs pārvietājat kripto no CEX uz jūsu aparatūras maciņu vai no Maciņa A uz Maciņu B, tas ir neapliekams «pārskaitījums». Tomēr, ja jūsu programmatūra nevar skaidri saistīt avotu un galamērķi, tā var nejauši atzīmēt kustību kā izņemšanu (pārdojumu) un iemaksu (ienākumu), radot fantomu apliekamus notikumus. Manuāli pārbaudiet visus pārskaitījumus.

- Marķēt DeFi darījumus: Kad nodrošināt likviditāti vai veicat staking, pārliecinieties, ka programmatūra pareizi marķē darījumu. Kad izņemat LP žetonus vai atceļat staking, pārbaudiet, vai platforma precīzi aprēķina saistītos uzkrātos ienākumus un kapitāla pieaugumu/zaudējumu pamata aktīviem.

- Uzglabāt ierakstus par izmaksu bāzes ievadi: Ja jūs iegādājāties kripto ar citiem līdzekļiem nekā pirkums (piem., ieguve, alga kripto vai airdrops), uzglabājiet dokumentāciju, kas parāda aktīva godīgo tirgus vērtību (FMV) saņemšanas datumā. Šī FMV kļūst par jūsu izmaksu bāzi, kas ir būtiska nākamo pieaugumu aprēķināšanai, kad jūs beidzot pārdosiet.

Secinājums: Kompleksitātes pārvēršana kapitālā

Pāreja no vienkāršas kripto nodokļu aprēķināšanas uz to stratēģisku optimizāciju prasa fundamentālu skatījuma maiņu. Tas nozīmē skatīt katru darījumu — no liela pārdojuma līdz mazai stabilo monētu apmaiņai — kā iespēju pārvaldīt jūsu izmaksu bāzi un minimizēt jūsu saistības.

Spēcīgākie rīki šajā optimizācijas komplektā ir Specifiskās identifikācijas metode, kas dod jums precīzu kontroli pār partiju izvēli, un proaktīva nodokļu zaudējumu novākšana, kas izmanto tirgus kritumus, lai kompensētu realizētos pieaugumus.

Lai gan digitālo aktīvu regulatorā vide paliek sarežģīta un strauji attīstās, proaktīva atbilstība kopā ar disciplīnu stratēģisko plānošanu nodrošina, ka jūs efektīvi veidojat savu digitālo bagātību. Īstenojot tīras uzskaites prakses, izmantojot progresīvu uzskaites programmatūru un pieņemot apzinātas lēmumus par to, kad un kā realizēt pieaugumus un zaudējumus, jūs pārtraucat minēšanos un sākat būvēt īstu finanšu pašsuverenitāti. Konsultējieties ar kvalificētu nodokļu profesionāli, lai efektīvi piemērotu šīs stratēģijas jūsu konkrētajā jurisdikcijā.