Imagine possessing wealth that cannot be taken, frozen, or blocked by any government, bank, or centralized authority. For centuries, our financial lives have relied upon trusted third parties (TTPs)—banks holding our savings, payment processors confirming our transactions, and governments enforcing the rules of the system. While this structure offers convenience, it demands a steep price: the forfeiture of absolute control over one’s own financial resources.

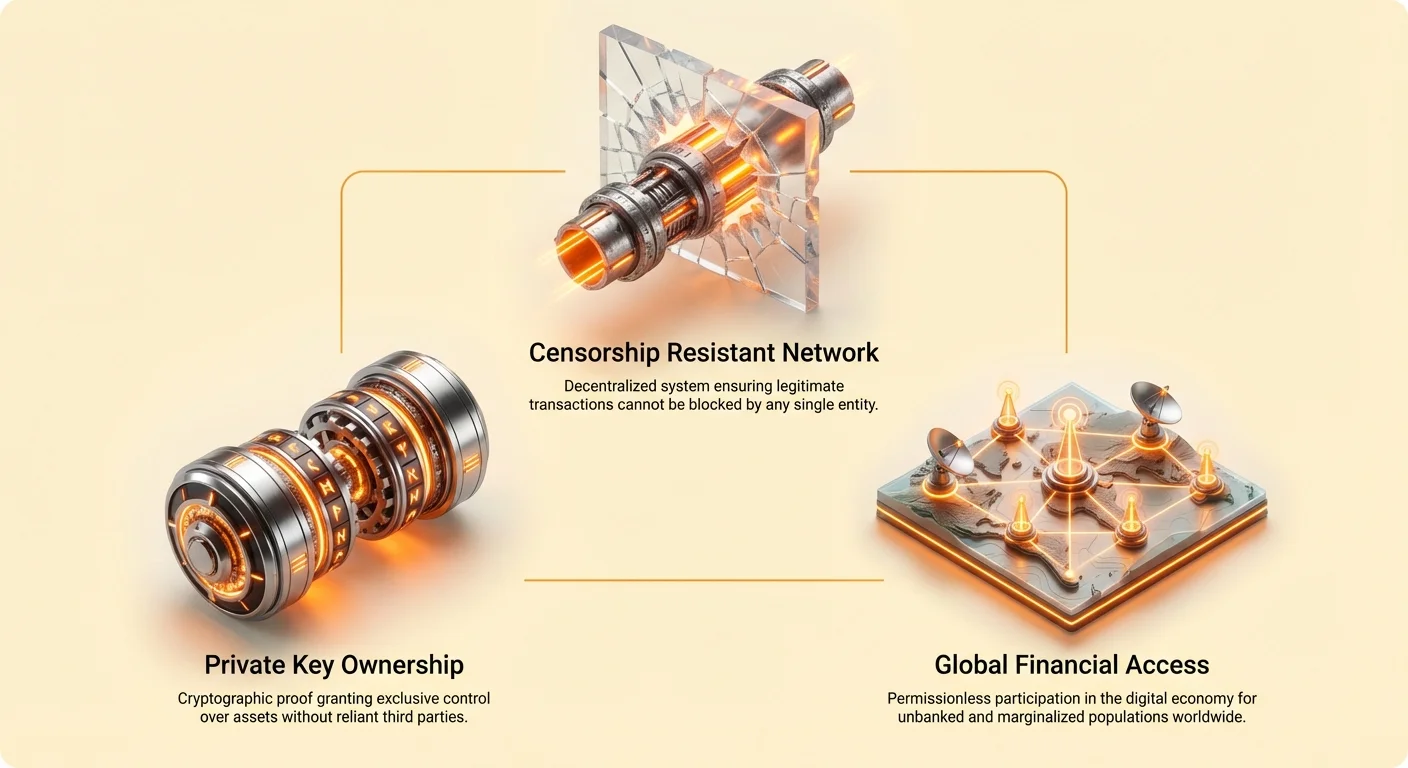

The advent of digital assets, particularly Bitcoin, introduced a radical concept: self-sovereignty. This term refers to the state of having complete control and ultimate authority over one’s finances without needing permission from external entities. This revolution is made possible by two core technical features: unseizability and censorship resistance.

This guide explores what these concepts mean in practical terms, moving beyond technical definitions to examine how unseizable money offers critical utility, not just for investors, but for humanitarian organizations, political dissidents, and anyone seeking genuine financial freedom in an increasingly monitored digital world. Understanding self-sovereignty is the first crucial step on the path toward becoming your own bank.

I. The Technical Core: Defining Censorship Resistance

To understand why Bitcoin is considered "unseizable," we must first define its primary defense mechanism: censorship resistance. In simple terms, a system is censorship resistant if no single entity can stop a legitimate transaction from being processed or confirmed.

In traditional finance, if you try to send money to a person or country deemed hostile by your bank or government, the transaction will be intercepted and stopped. The bank acts as a central gatekeeper, exercising censorship based on political or regulatory demands.

Bitcoin, however, operates differently. It is built on a distributed network of computers (nodes) that all agree on the rules of the network. These rules are mathematical and applied equally to everyone, meaning political or social biases cannot be enforced to block a payment.

Centralized Gatekeepers vs. Decentralized Networks

In the fiat world, money flows through central banks and commercial banks. These entities have the legal and technical authority to pause, reverse, or freeze accounts. If the U.S. government, for example, issues a sanction against an individual, major financial institutions worldwide are obligated to comply by freezing any associated assets. The institution acts as the point of centralization, making it highly vulnerable to pressure.

Bitcoin’s network has no central headquarters. Transactions are broadcast to thousands of independent computers (nodes) across the globe. For a transaction to be confirmed and added to the blockchain (the public ledger), it must only adhere to the established rules of the Bitcoin protocol (e.g., the sender must prove ownership via their private key). As long as the transaction is mathematically valid, the decentralized consensus mechanism ensures it is processed. There is no single "off switch" or central administrator capable of blocking the transfer.

Defining "Invalid" vs. "Censored"

It is important to clarify that censorship resistance does not mean "anything goes." The Bitcoin network strictly rejects invalid transactions. An invalid transaction might be one where the sender tries to spend coins they do not own, or one that breaks the cryptographic signing rules.

However, the network is designed to resist censorship—the denial of service based on the identity, location, or purpose of the sender or receiver. Nodes and miners operate based on objective cryptographic proof, not subjective human judgment. If you prove ownership of the funds, the network processes the transaction, regardless of who you are trying to pay.

The Prohibitive Cost of Denial

The ultimate defense against censorship is the sheer cost of attack. To successfully censor transactions on the Bitcoin network, an entity would need to control more than 51% of the total computing power (hash rate) securing the network. Gaining and maintaining control over the majority of global mining resources is practically impossible, requiring billions of dollars in hardware, electricity, and coordination. This economic reality ensures that the network is protected from unilateral hostile takeover by governments or mega-corporations, guaranteeing its neutrality.

II. The Fiat Contrast: Why Assets Are Seizable Today

To appreciate the value of unseizable money, we must first recognize the vulnerability inherent in traditional finance. All modern banking and payment systems are built on an implicit trust framework, where financial intermediaries act as custodians of your assets and arbiters of your financial permissions.

The Vulnerability of Trusting Third Parties (TTPs)

When you deposit money in a bank, you legally transfer custodianship of those funds to the institution. The bank promises to return the funds when requested, but in the interim, it maintains technical and legal control. This relationship is often summarized by the phrase: "Not your keys, not your coins." When a bank or brokerage holds your assets, they are the ones who possess the private keys to that financial institution’s holdings, giving them the final say.

This system works well when trust is maintained, but it creates profound vulnerabilities in situations where:

- Political Instability: Governments may impose capital controls, preventing citizens from withdrawing or moving their money out of the country.

- Legal Disputes: Courts can issue garnishment orders, legally forcing banks to hand over assets to satisfy a debt or judgment.

- Institutional Failure: If the bank or brokerage collapses, your access to funds may be delayed or limited, even in systems with deposit insurance.

Case Studies in Asset Freezes and Financial Exclusion

The theoretical risk of seizure has played out repeatedly in the modern era, creating clear use cases for unseizable money:

1. Political Protests and Financial De-Platforming

During political protests in various developed nations in recent years, governments utilized banking regulations to freeze the funds of individuals participating in or donating to the movements. By issuing court orders to financial institutions, authorities were able to deny protestors access to their savings, effectively shutting down their ability to pay for fuel, food, or legal defense. This demonstrated that financial freedom is conditional, dependent on political compliance.

2. Capital Controls and Economic Collapse

In countries experiencing hyperinflation or severe economic instability (such as Lebanon, Argentina, or Cyprus), governments have restricted the ability of citizens to withdraw or transfer foreign currency, trapping their savings within a depreciating local system. For the average citizen, the money shown in their bank account is merely an entry in a database controlled by the very government causing the economic hardship.

3. Cross-Border Restrictions and Humanitarian Bottlenecks

Moving large sums of money, even for legitimate purposes like charity or business investment, requires meticulous regulatory compliance. Anti-Money Laundering (AML) and Know-Your-Customer (KYC) regulations, while crucial for law enforcement, often result in legitimate funds being delayed, flagged, or blocked entirely when crossing international borders, creating huge bureaucratic burdens for aid organizations.

III. Self-Sovereignty in Practice: The Unseizable Wallet

Bitcoin flips the script on financial control. It moves the authority from the institution (the bank) to the individual (the private key holder). True financial self-sovereignty is achieved when the user alone holds the means to access and spend their funds.

Private Keys as Absolute Ownership

The key to unseizable money lies in cryptography. When you own Bitcoin, you do not physically possess a digital coin; you possess a private key. This key is a secret, long string of letters and numbers (often represented by a 12 or 24-word seed phrase) that acts as the cryptographic proof of ownership.

If you maintain sole custody of this private key, no one—not your government, your bank, or the network's developers—can move your Bitcoin. They can see the balance associated with your public address on the blockchain, but they cannot authorize a transaction. This simple technological fact creates absolute financial sovereignty.

Analogy: If bank money is like a title deed stored in a government registry, self-sovereign money is like a safe deposit box key that only you possess, where the location of the safe is known to everyone, but the contents are impenetrable without your specific key.

The Critical Role of Self-Custody

For an asset to be truly unseizable, it must be held in self-custody—meaning you, and only you, control the private keys.

If you purchase Bitcoin and leave it on a centralized cryptocurrency exchange (CEX) like Coinbase or Binance, the asset is not self-sovereign. The exchange holds the private keys, making it a trusted third party. Just like a bank, the exchange must comply with legal orders, freezing or seizing the assets if mandated by a court.

True self-sovereignty demands that you move your assets into a dedicated, non-custodial wallet (often a hardware wallet or a robust software wallet). In this environment, the digital asset is effectively immune to institutional seizure, providing the user with unprecedented control.

Plausible Deniability and Portable Wealth

Self-sovereignty offers practical utility in situations of extreme distress, such as fleeing political persecution or conflict. A significant amount of wealth—potentially millions of dollars worth of Bitcoin—can be secured by memorizing a 12- or 24-word seed phrase.

This creates plausible deniability for wealth storage. Unlike gold, diamonds, or physical cash, which can be searched for, confiscated, or taxed at the border, a seed phrase is intangible. A person can cross any international boundary, carrying only their knowledge, and later regenerate their entire life savings using a new wallet and an internet connection anywhere in the world. This portability is a foundational aspect of self-sovereign money.

IV. Global Utility: Who Needs Censorship Resistance?

While financial self-sovereignty offers powerful advantages to everyone, its most profound utility is realized by those historically excluded or oppressed by centralized systems. Censorship resistance is not merely a feature for investors; it is a critical tool for human rights, economic stability, and freedom.

Supporting Dissidents and Political Opposition

In authoritarian regimes, one of the first tactics used to crush dissent is financial cut-off. Governments can swiftly identify, locate, and freeze the funds of opposition leaders, non-profits, or activist groups, suffocating their ability to organize, communicate, or pay staff.

Bitcoin offers a lifeline. Dissidents can accept donations from international supporters without needing a bank account, an intermediary, or official permission. These funds can be stored outside the country's jurisdiction and spent peer-to-peer, bypassing the dictator's control over the financial system. This financial resilience strengthens the position of those fighting for democracy and human rights.

Humanitarian Aid in Conflict Zones

Humanitarian organizations often face immense challenges operating in conflict zones or areas with highly volatile governance. Banks may refuse to process transactions to certain regions due to sanctions risk, or local governments may commandeer aid funds through corruption or outright seizure.

Using a censorship-resistant asset allows organizations to:

- Ensure Direct Delivery: Funds can be sent directly to individuals or local community leaders using simple mobile wallets, bypassing centralized financial choke points.

- Minimize Bureaucracy: Transfers are processed regardless of time zones, political boundaries, or banking hours, speeding up emergency aid deployment.

- Preserve Value: In areas where the local currency is collapsing, receiving aid in a relatively stable digital asset provides better long-term security for the recipients.

Financial Inclusion for the Unbanked

Approximately 1.7 billion adults globally are unbanked, meaning they lack access to formal financial services. Often, this is because they lack government-issued identification, live in remote areas, or cannot meet minimum balance requirements.

Self-sovereign crypto networks offer immediate financial inclusion. Anyone with a smartphone can download a non-custodial wallet and participate in the global economy. No permission, credit check, or government ID is required to create a Bitcoin wallet. This access allows individuals who were previously financially invisible to save, transact, and receive remittances, giving them a tangible stake in their own economic future.

V. Responsibility and Risk: Becoming Your Own Bank

The concept of self-sovereignty is synonymous with extreme responsibility. When you eliminate the intermediary (the bank), you gain ultimate control, but you also assume all the associated risks that the bank traditionally managed. For a beginner, this transition requires a fundamental shift in mindset.

Your Private Key Is Your Bank Vault

In the fiat world, if you forget your password, the bank can verify your identity and reset your account access. If you get defrauded, the bank or payment processor might be able to reverse the transaction or insure your losses.

In the world of self-sovereign money, there is no customer service line, no government insurance, and no reversal button.

- If you lose your private key (seed phrase), your funds are permanently lost. They cannot be recovered by anyone, as no central database holds a copy.

- If your private key is stolen, your funds are permanently stolen. Once a thief spends your Bitcoin, the transaction is immutable (cannot be reversed).

This immutability is the trade-off for unseizability. The features that make the money impossible for a government to seize also make it impossible for you to recover if you mismanage the key.

Security Best Practices for Self-Custody

Achieving and maintaining self-sovereignty requires rigorous adherence to security protocols:

1. Prioritize Physical Security of the Seed Phrase

The 12 or 24 words of your recovery seed phrase are the physical representation of your private key.

- Do not store it digitally (no screenshots, cloud storage, or plain text files on a computer). Digital copies are highly vulnerable to hacking.

- Write it down on specialized paper or etch it into metal. Metal backups are recommended for long-term storage as they are resistant to fire and water damage.

- Store the physical backup in a secure, hidden location (e.g., a safe or bank vault).

2. Utilize Hardware Wallets

For beginners and those holding non-trivial amounts of money, a hardware wallet (like Trezor or Ledger) is the gold standard for self-custody. A hardware wallet keeps your private key isolated offline, ensuring it never touches an internet-connected device. Even if your computer is infected with malware, the key remains protected inside the device, requiring physical confirmation (pressing a button) for any transaction.

3. Practice Test Transactions

Before moving a significant amount of wealth, practice the entire process: move a very small amount of Bitcoin into your new self-custody wallet, then wipe the wallet software (or reset the hardware device), and practice restoring the funds using only your seed phrase. Only once you have successfully demonstrated that you can restore your funds should you move larger sums.

The Double-Edged Sword of Immutability

The unseizable nature of self-sovereign money means that transaction finality is absolute. Once a Bitcoin transaction is confirmed on the blockchain, it is immutable—it is recorded forever and cannot be changed or reversed.

While this immutability provides censorship resistance, it also means mistakes are permanent. If you accidentally send funds to the wrong address, or if you fall for a scam and send money voluntarily, there is no recourse. This requires users to be meticulous, double-checking addresses and amounts before broadcasting any transaction. This high standard of care is the price of total self-sovereignty.

Conclusion: Reclaiming Financial Freedom

Self-sovereignty, realized through the technical properties of unseizable money and censorship resistance, represents the most fundamental shift in finance in decades. It moves authority away from centralized institutions—which operate based on shifting political winds and bureaucratic demands—and places it squarely in the hands of the individual.

This shift provides practical utility: it protects dissidents from having their funding cut off, offers humanitarian organizations a reliable pathway for aid, and grants billions of unbanked individuals access to the global digital economy for the first time.

However, self-sovereignty is not a passive state; it is an active practice. Becoming your own bank means accepting full liability for security and storage. For those willing to accept this responsibility and master the necessary security steps, the reward is genuine, unconditional financial freedom—a powerful tool for self-determination in the new digital economy.