The shift from traditional financial systems to cryptocurrency represents more than just a technological upgrade. It is a fundamental change in how individuals perceive ownership and responsibility. In the conventional banking world, money is stored in accounts managed by third parties. Users have a legal claim to these funds, but they do not possess the actual assets. Access relies entirely on the permission of the institution holding the money.

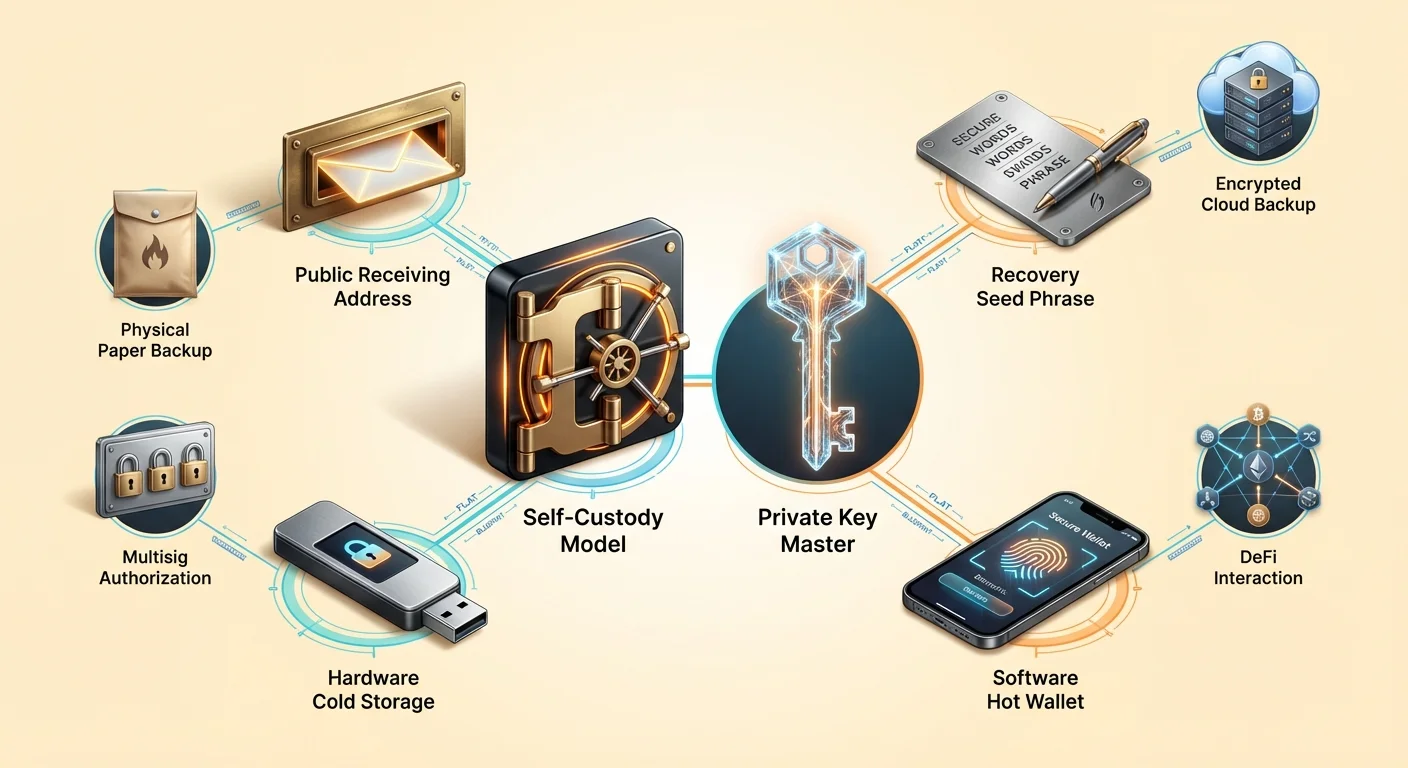

Digital sovereignty flips this model upside down. When utilizing cryptocurrencies like Bitcoin or Ethereum in a self-custodial manner, there is no intermediary. The user does not ask for permission to transact. Instead, they interact directly with a global, decentralized ledger. This capability is often described as being your own bank. It offers immense freedom but requires a specific mindset focused on security and deliberate management of digital keys.

The concept of peer-to-peer value transfer is central to this shift. In this system, assets can be sent anywhere in the world without routing through a central authority. This absence of a middleman means that security responsibilities usually handled by a bank now fall squarely on the individual. Understanding the mechanics of this responsibility is the first step toward true digital independence.

The Mechanics of Digital Ownership

To understand self-custody, one must first understand what a crypto wallet actually does. A common misconception is that a wallet stores cryptocurrency files inside the device, similar to how a physical wallet holds cash. In reality, the coins never leave the blockchain network. They exist as entries on a public ledger that tracks ownership changes over time. The wallet does not hold the asset; it holds the tools required to move the asset.

These tools are known as cryptographic keys. Every wallet generates pairs of keys that function mathematically to secure funds. The relationship between these keys defines ownership. Without the specific key associated with an address on the blockchain, the funds at that address are effectively unmovable. This is why the loss of a wallet's keys equates to the permanent loss of the funds they control.

The most critical component in this system is the private key. This is a randomly generated string of characters, often 256 bits in length. It acts as the ultimate password. While the public address tells the world where to send funds, the private key is the only thing that can authorize funds to leave that address. It creates a digital signature for every transaction, proving to the network that the legitimate owner is initiating the transfer.

Public Keys vs. Private Keys

The relationship between public and private keys is often compared to a mailbox. The public key, or the wallet address derived from it, is like the mail slot or the street address. Anyone can drop a letter (or cryptocurrency) into it. You can share this address safely with the entire world without compromising the security of the contents inside the mailbox.

The private key acts as the physical key that opens the mailbox. Only the person holding this key can retrieve the contents or send them elsewhere. If you give someone your mailbox key, they have full control over your mail. Similarly, if a third party acquires your private key, they have total control over your digital assets. This is why private keys must remain secret and should never be shared online or with support staff.

Because raw private keys look like long, confusing strings of hexadecimal characters, modern wallets use a standard to convert them into a human-readable format. This is known as the recovery phrase, seed phrase, or secret passphrase. It usually consists of 12 to 24 random words taken from a specific dictionary. These words are much easier for humans to record and verify than a string of random numbers and letters.

The Spectrum of Custody

In the cryptocurrency ecosystem, not all wallets offer the same level of control. The primary distinction lies between custodial and self-custodial (or non-custodial) services. This distinction determines who actually holds the private keys and, by extension, who owns the assets. Understanding this difference is vital for assessing risk.

Custodial wallets are typically provided by centralized exchanges or brokerages. When a user buys crypto on these platforms, the exchange holds the private keys. The user logs in with a username and password, similar to an online bank account. While convenient, this model reintroduces the risks of traditional finance. The user is relying on the exchange's solvency, security measures, and willingness to process withdrawals.

Risks of Third-Party Custody

History in the crypto space has shown that custodial services carry significant counterparty risk. If a centralized platform goes bankrupt, users often find themselves as unsecured creditors with little hope of recovering their full deposits. The recovery process, if it happens at all, can take years. During this time, funds remain inaccessible regardless of market movements.

Furthermore, custodial services are subject to regulatory pressures. Governments can pressure centralized entities to freeze accounts or block transactions to certain destinations. This occurred in traditional finance during the Greek debt crisis, where withdrawals were severely limited. Similar restrictions can be applied to custodial crypto accounts, negating the censorship-resistant properties of the underlying asset.

The Self-Custodial Advantage

Self-custodial wallets eliminate these third-party risks. In this model, the software or hardware device generates and stores the private keys locally. The service provider who created the wallet software has no access to the user's funds. They cannot freeze accounts, reverse transactions, or lose the user's money through corporate mismanagement.

This approach grants the user direct access to the public blockchain. Transactions are broadcast directly to the network. This ensures that the user can always move their assets as long as the blockchain network itself is operational. It also opens the door to the wider world of decentralized applications (dApps), which often require a self-custodial connection to function.

Securing the Digital Vault

With the power of self-custody comes the absolute necessity of proper security practices. Since there is no bank help desk to reverse a fraudulent transaction or reset a forgotten private key, the user must implement robust defense strategies. The first line of defense is the protection of the recovery phrase.

When setting up a new self-custodial wallet, the software will display the recovery phrase. This list of words is the master key. If the phone or computer running the wallet is lost, damaged, or stolen, the funds can be recovered on a completely new device using this phrase. However, if the phrase is lost and the device is also inaccessible, the funds are gone forever.

Manual vs. Cloud Backups

Traditionally, the standard advice was to write the recovery phrase on paper and store it in a fireproof safe or a secure location. This is known as a manual backup. It keeps the keys offline, protecting them from digital theft. However, paper can degrade, be thrown out by accident, or be destroyed by physical disasters like floods or fires.

| Backup Method | Security Profile | Convenience |

|---|---|---|

| Manual (Paper) | High (Offline) | Low (Hard to manage) |

| Cloud Backup | High (Encrypted) | High (Automated) |

| Metal Plate | Very High (Durable) | Low (Expensive) |

Newer wallet solutions offer automated cloud backups. In this system, the wallet encrypts the recovery phrase and stores it in a cloud service like Google Drive or iCloud. The user sets a custom password that decrypts this file. This hybrid approach offers a balance of security and convenience. The cloud provider holds the file but cannot read it without the password, while the user doesn't have to worry about physical paper storage.

Password Management

Regardless of the backup method chosen, password hygiene is critical. For cloud backups, the decryption password must be strong and unique. Using a weak password exposes the backup to brute-force attacks if the cloud account is compromised. Similarly, the device running the wallet app should be secured with biometrics (FaceID or fingerprint) or a complex PIN to prevent unauthorized physical access.

Users should never store passwords or recovery phrases in unencrypted digital notes or take screenshots of them. Malware scanning a device often looks specifically for image files containing text or documents with keywords like "recovery phrase." Keeping sensitive data off the clipboard and out of photo libraries is a basic but essential security step.

Hardware and Software Solutions

Self-custody tools fall into two broad categories: software wallets and hardware wallets. Software wallets, often called "hot wallets," run on general-purpose devices like smartphones or laptops. They are connected to the internet, making them highly convenient for frequent trading, spending, or interacting with Web3 applications.

Hardware wallets, or "cold storage," are physical devices dedicated solely to managing private keys. They look like USB drives and keep the keys offline at all times. When a user wants to send a transaction, the unsigned transaction is sent to the hardware device. The device signs it internally using the private key and returns the signed data to the computer to be broadcast. The private key never touches the internet-connected computer.

For large amounts of capital, a combination of these methods is often recommended. A "checking account" logic applies to the software wallet: keep only what is needed for near-term use. The "savings account" portion of a portfolio should reside in cold storage, where the risk of remote hacking is virtually eliminated.

Advanced Wallet Features

As the ecosystem matures, wallets have evolved beyond simple storage tools. They now include features that allow for greater control over how assets are managed and used. One such feature is fee customization. Public blockchains require transaction fees to pay the miners or validators who secure the network.

Advanced wallets allow users to select the fee rate based on urgency. If a transaction is not time-sensitive, a user can select a lower fee and wait longer for confirmation. Conversely, urgent transactions can be prioritized by paying a higher rate. This level of control is rarely available in custodial exchange accounts, which typically charge a flat, often inflated, fee for withdrawals.

Multisignature Security

For enhanced security, particularly for organizations or families, multisignature (multisig) wallets offer a powerful solution. A standard wallet requires one signature to authorize a transaction. A multisig wallet requires multiple signatures from different keys to move funds.

For example, a "2-of-3" multisig setup creates three keys. To spend funds, at least two keys must sign the transaction. This structure eliminates the single point of failure. If one key is lost or stolen, the funds remain safe, and the remaining keys can still move the assets. This setup is ideal for corporate treasuries requiring board approval for spending or for family savings where no single individual should have unilateral access.

Interacting with DeFi

The utility of a self-custodial wallet extends into Decentralized Finance (DeFi). DeFi applications run on smart contracts—code that executes automatically on the blockchain. These applications allow for trading, lending, borrowing, and earning interest without a bank. To use these applications, a user must connect a self-custodial wallet. Custodial exchange accounts generally cannot interact with DeFi protocols directly. By holding their own keys, users gain access to a vast ecosystem of financial derivatives, prediction markets, and yield-generating opportunities that operate 24/7 without geographic restrictions.

To use these applications, a user must connect a self-custodial wallet. Custodial exchange accounts generally cannot interact with DeFi protocols directly. By holding their own keys, users gain access to a vast ecosystem of financial derivatives, prediction markets, and yield-generating opportunities that operate 24/7 without geographic restrictions.

Choosing the Right Wallet

Selecting a wallet is a decision that impacts the safety of one's entire portfolio. The first criterion is reputation. Users should look for wallets with a long track record and positive feedback from the community. Forums and app store reviews can provide insights into the reliability of a specific software.

Open-source code is another strong indicator of trustworthiness. When a wallet's code is public, security researchers can audit it for vulnerabilities or backdoors. Closed-source wallets require users to trust the developers implicitly, which contradicts the "don't trust, verify" ethos of crypto.

Platform Compatibility

The choice also depends on the specific assets being held. Some wallets are Bitcoin-only, while others are multichain, supporting Ethereum, Solana, and hundreds of other tokens. A multichain wallet simplifies management by keeping diverse assets under one interface with a single backup phrase.

Additionally, users should consider the user interface and ease of use. Features like personal notes for transactions, display currency toggles, and address books improve the daily experience. However, convenience should never come at the expense of non-negotiable security features like private key export and encryption.

The Responsibility of Sovereignty

Adopting a self-custody mindset requires accepting that safety is an active process. In the banking world, fraud protection departments monitor transactions for suspicious activity. In the blockchain world, the user is the fraud department.

Phishing scams are the most common threat to self-custody users. Attackers create fake websites or send emails pretending to be wallet support teams, asking for the recovery phrase. A self-custody user must understand that no legitimate company will ever ask for this phrase. Recognizing these social engineering attacks is just as important as the technical security of the wallet itself.

Regular maintenance is also required. This involves checking that backups are still accessible and legible. If a paper backup fades or a cloud password is forgotten, the safety net dissolves. Periodic checks ensure that the recovery path remains open should an emergency arise.

Conclusion

Shifting from a banking mindset to a self-custody mindset is a journey toward financial independence. It replaces the comfort of institutional safety nets with the power of cryptographic guarantees. By holding private keys, individuals ensure that their assets remain truly theirs, immune to bank failures or arbitrary freezes.

This transition demands education and vigilance. From understanding the difference between a public address and a private key to mastering backup strategies, every step strengthens digital sovereignty. As the world becomes increasingly digitized, the ability to secure and control one's own value without intermediaries is becoming a vital skill for preserving economic freedom.

Your private keys are the only proof of ownership; protect them as if they were the assets themselves.