The evolution of the cryptocurrency market has created a global financial ecosystem that operates twenty-four hours a day. While digital assets move seamlessly across borders on blockchain networks, the interface between these digital currencies and local fiat money remains a critical friction point. This is where peer-to-peer (P2P) platforms have emerged as essential infrastructure.

These platforms serve as localized bridges, connecting the global crypto economy with regional banking systems and payment networks. Unlike centralized order books that match trades automatically, P2P platforms facilitate direct interaction between buyers and sellers. This human element allows for a degree of flexibility that rigid centralized systems cannot match.

For many users in regions with strict banking regulations or limited financial infrastructure, these platforms are not just an alternative but a primary gateway. They provide the necessary liquidity to convert digital earnings into spendable cash. This process, known as an "off-ramp," is vital for the practical utility of cryptocurrency.

Understanding the mechanics, risks, and benefits of localized P2P access is essential for any trader looking to move funds efficiently. It involves navigating reputation systems, understanding escrow mechanisms, and recognizing the nuances of regional payment methods. This guide explores how these platforms function and their role in the broader financial landscape.

The Mechanics of Peer-to-Peer Trading

Peer-to-peer trading fundamentally differs from the automated matching engines found on standard centralized exchanges. On a traditional exchange, an algorithm matches buy and sell orders based on price and time priority. The user rarely knows who is on the other side of the trade.

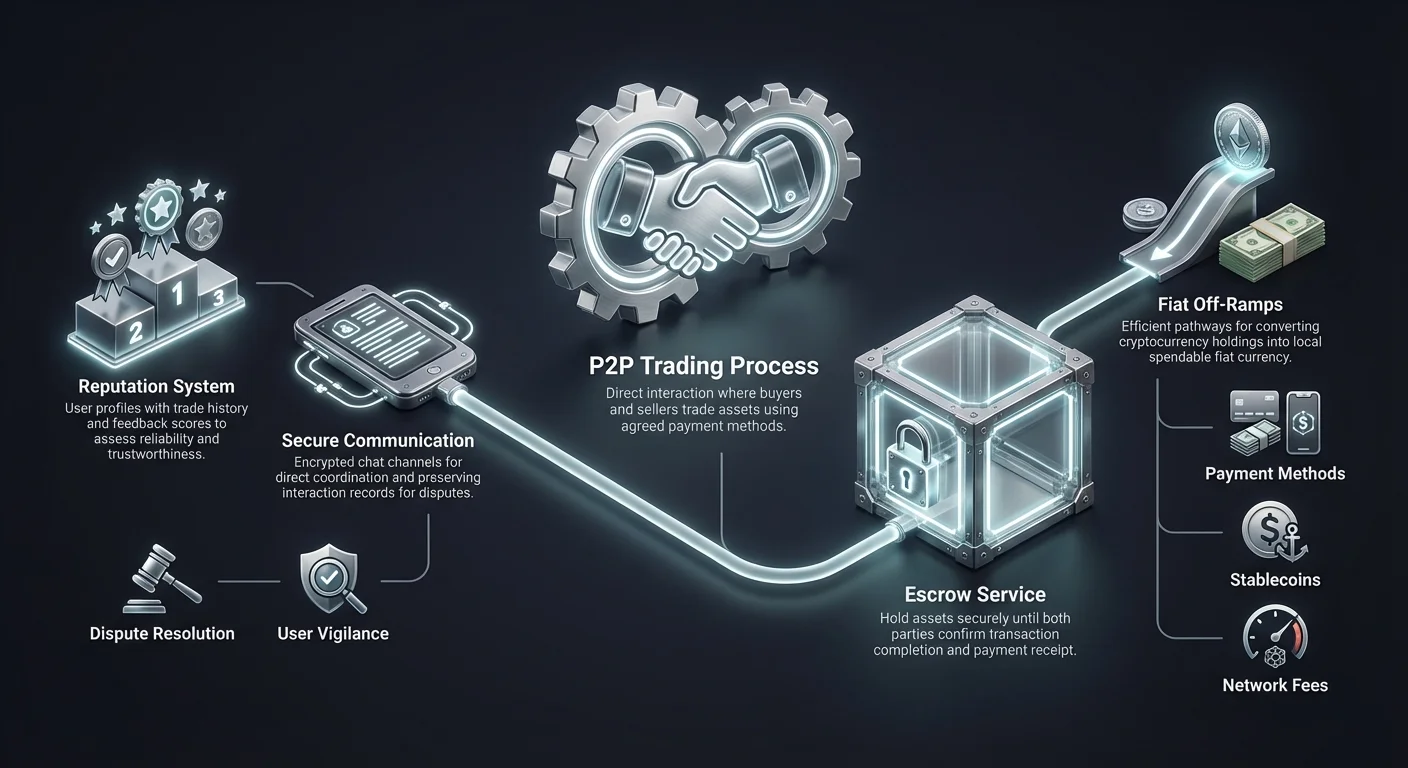

In a P2P environment, the process is more akin to a classified advertisement board. Sellers post advertisements detailing the amount of cryptocurrency they wish to sell, the price they are asking, and the payment methods they accept. Buyers browse these listings and select a merchant that fits their specific needs.

Once a trade is initiated, the platform facilitates the exchange but does not necessarily process the fiat payment itself. Instead, the fiat transfer happens outside the platform, directly between the bank accounts or digital wallets of the two parties. This separation of crypto settlement and fiat settlement is the defining characteristic of P2P trading.

The Role of Escrow Services

Trust is the most significant challenge in a trade where one party sends money before receiving the asset. To solve this, P2P platforms utilize escrow services. When a trade is opened, the seller’s cryptocurrency is temporarily locked by the platform. It is removed from the seller's control but not yet credited to the buyer.

This escrow state ensures that the cryptocurrency is secure while the fiat payment is processed. The buyer sends the agreed-upon fiat currency using the selected payment method. Once the payment is sent, the buyer marks the trade as paid on the platform.

The seller then verifies that the funds have arrived in their bank account or digital wallet. Upon confirmation of receipt, the seller releases the cryptocurrency from escrow. The platform then instantly credits the digital assets to the buyer's wallet, completing the transaction.

Direct Communication Channels

A unique feature of P2P platforms is the ability for counterparties to communicate directly via encrypted chat systems. This communication channel is vital for clarifying payment details or resolving minor delays. It adds a layer of human interaction that can help build trust and facilitate smoother transactions.

The chat function also serves as a record of the interaction in case of a dispute. If a disagreement arises regarding payment, platform administrators can review the chat history to adjudicate the issue. This transparency encourages professional behavior between trading partners.

However, this direct communication also requires vigilance. Users must be cautious about sharing sensitive personal information that is not required for the transaction. Platforms typically advise keeping all communication within the official chat interface to ensure safety and proper documentation.

Regional Access and Financial Inclusion

One of the primary drivers for P2P adoption is the need for localized financial access. Centralized exchanges often rely on international banking partners to process deposits and withdrawals. These partners may not support every local currency or regional bank, leaving many users without a direct way to purchase crypto.

P2P platforms solve this by crowdsourcing liquidity. Local traders act as market makers, using their own domestic bank accounts to facilitate trades. This effectively decentralizes the banking connection, allowing users to transact using domestic payment networks that international exchanges cannot access.

This structure is particularly important for financial inclusion in unbanked or underbanked regions. In areas where credit card penetration is low or international wire transfers are prohibitively expensive, P2P markets thrive. They utilize local mobile money solutions and cash deposit networks that are already familiar to the local population.

By leveraging these local payment rails, P2P platforms lower the barrier to entry. A user does not need a multi-currency bank account or access to SWIFT transfers. They simply need a local payment method and an internet connection to participate in the global digital asset economy.

Fiat Off-Ramps: Converting Crypto to Cash

An "off-ramp" refers to the process of converting cryptocurrency back into fiat currency. While buying crypto (on-ramping) is often streamlined to encourage investment, selling crypto for cash can be more complex. This complexity arises from banking regulations and the scrutiny placed on incoming transfers from crypto-related entities.

P2P platforms are often the most reliable off-ramps in restrictive jurisdictions. Because the fiat transfer appears as a standard person-to-person bank transfer, it is less likely to be flagged or blocked compared to a transfer from a known corporate crypto exchange. This allows users to liquidate their holdings even in challenging regulatory environments.

The flexibility of P2P off-ramps extends to the speed of settlement. While international bank withdrawals can take several business days to clear, domestic P2P transfers are often instant. In many countries, instant payment networks allow sellers to receive cash for their crypto within minutes of initiating a trade.

Furthermore, P2P off-ramps support a granularity of transaction sizes that centralized institutions may avoid. Users can find offers for very small amounts or very large blocks, depending on the available liquidity providers. This scalability makes P2P useful for both casual users cashing out small earnings and larger traders managing liquidity.

Security Protocols in Localized Markets

Security in P2P markets relies on a combination of code-based protection and social engineering safeguards. Unlike centralized exchanges where the platform holds custody of all funds, P2P security is focused on ensuring the fair exchange of assets between two individuals who do not trust each other.

The primary line of defense is the escrow system previously discussed. However, escrow alone is not enough to prevent all forms of fraud. Platforms implement rigorous identity verification and risk management algorithms to detect suspicious behavior patterns before a trade occurs.

Two-factor authentication (2FA) is a standard requirement for releasing funds from escrow. This prevents unauthorized access to a seller's account. Even if a malicious actor gains access to a user's login credentials, they would still need the second factor to finalize any release of cryptocurrency.

Reputation and Feedback Systems

To mitigate the risk of dealing with strangers, P2P platforms utilize comprehensive reputation systems. Every user builds a public profile based on their transaction history. Key metrics typically include the total number of trades, the completion rate, and the average release time.

Buyers can review these statistics before initiating a trade. A high completion rate indicates reliability, while a high volume of trades suggests experience. Feedback comments from previous trading partners provide qualitative data about a user's responsiveness and honesty.

Traders with high reputation scores often charge a slightly higher premium for their services. This premium reflects the value of safety and reliability. New users or those with lower scores may offer better rates to attract business and build their reputation, presenting a risk-reward trade-off for the counterparty.

Dispute Resolution Mechanisms

Despite all precautions, disagreements can occur. A buyer might claim they sent payment when they haven't, or a seller might refuse to release crypto after receiving funds. To handle these scenarios, platforms provide dispute resolution services.

When a dispute is raised, the cryptocurrency remains locked in escrow. A support agent enters the chat and requests evidence from both parties. This evidence usually includes proof of payment, such as bank receipts or transaction screenshots, and video recordings of account history.

The platform administrators review the evidence to determine the truth. Once a decision is made, the administrator forces the release of the funds to the rightful owner. This arbitration process is critical for maintaining the integrity of the marketplace and deterring bad actors.

Payment Methods and Flexibility

The versatility of P2P platforms lies in their ability to support hundreds of different payment methods. While centralized exchanges are often limited to wire transfers and credit cards, P2P marketplaces can accommodate almost any form of value transfer that can be verified.

Digital wallets and e-money services are extremely popular on these platforms. Services like PayPal, Wise, Skrill, and various regional equivalents provide fast and convenient ways to move fiat currency. These methods are favored for their speed, often settling instantly, which allows for rapid trade turnover.

Cash-in-person trades are another option available in some regions. This method involves the buyer and seller meeting physically to exchange cash for a crypto release. While this offers high privacy and immediate settlement, it introduces physical security risks that users must carefully consider.

Local bank transfers remain the backbone of high-volume P2P trading. Domestic banking networks often offer free or low-cost transfers between accounts. In many regions, these transfers are now instant, making them highly efficient for larger transactions where digital wallet limits might be restrictive.

| Payment Category | Speed | Risk Level | Typical Limits |

|---|---|---|---|

| Digital Wallets | Instant | Moderate (Chargebacks) | Low to Medium |

| Bank Transfers | Instant to 1-3 Days | Low | High |

| Cash in Person | Immediate | High (Physical Safety) | Variable |

Choosing the right payment method involves balancing speed, cost, and risk. Methods that are reversible, like certain digital wallet transfers, often carry higher premiums to compensate sellers for the risk of chargeback fraud. Irreversible methods like wire transfers usually command better exchange rates.

Privacy and Anonymity Considerations

Privacy is a significant factor for many cryptocurrency users. Traditional financial systems and centralized exchanges typically require extensive Know Your Customer (KYC) verification. This involves submitting government IDs, proof of address, and sometimes even facial scans.

P2P platforms occupy a spectrum regarding privacy. Some platforms enforce strict KYC requirements similar to centralized exchanges. These compliant platforms offer a higher degree of safety against scams but less privacy. They are often the best choice for users prioritizing security and legal compliance.

On the other end of the spectrum are platforms that allow for no-KYC or "lite" verification trading. These platforms may only require an email address or phone number to start trading. They appeal to users who live in regimes with oppressive financial surveillance or those who simply value their digital privacy.

However, improved privacy often comes with reduced liquidity and higher risks. Without identity verification, it is harder to hold bad actors accountable. Users on anonymous platforms must rely heavily on reputation systems and on-chain escrow mechanisms to ensure safety.

Furthermore, while the P2P platform itself might not require ID, the payment method used often does. Sending a bank transfer or using a digital wallet usually leaves a paper trail linking the transaction to a real-world identity. True anonymity in P2P trading is difficult to achieve when fiat currency is involved.

The Role of Stablecoins in P2P

Stablecoins have revolutionized P2P trading by providing a non-volatile medium of exchange. In the early days of crypto, P2P markets were dominated by Bitcoin. The volatility of Bitcoin meant that the value of a trade could fluctuate significantly during the time it took to process a bank transfer.

Today, stablecoins like USDT (Tether) and USDC are the primary assets traded on P2P markets. These tokens are pegged to the value of the US Dollar, ensuring price stability. This allows traders to move in and out of fiat positions without worrying about market crashes occurring during the transaction window.

For off-ramping, stablecoins serve as a secure holding spot. A trader can convert their volatile altcoins into stablecoins on a centralized exchange and then move those stablecoins to a P2P platform to cash out. This separates the investment decision from the liquidity event.

Stablecoins also facilitate cross-border arbitrage and remittances. A user can buy stablecoins in one currency and sell them for another currency, effectively using the P2P market as a foreign exchange service. This utility has made stablecoins the most liquid assets on many regional P2P platforms.

Analyzing Fees in P2P Markets

Fee structures on P2P platforms can be more complex than standard exchange fees. Users need to look beyond the platform's stated service fee to understand the true cost of a transaction. The total cost is usually a combination of platform fees, payment processing fees, and the exchange rate spread.

Most platforms charge a fee to the user who posts the advertisement (the "maker"). The user who responds to the ad (the "taker") often pays zero platform fees. This model encourages liquidity providers to populate the order book with offers.

However, the exchange rate offered in the advertisement often includes a hidden markup. A seller might list Bitcoin at a price 2% or 3% higher than the global spot price. This premium covers the seller's profit margin and the risk of volatility.

Network Fees

When moving cryptocurrency from a personal wallet to the P2P platform's escrow wallet, users must pay blockchain network fees. These fees go to miners or validators, not the platform. During times of network congestion, these fees can be significant.

Some P2P platforms operate internal wallets. If both users keep their funds within the platform's ecosystem, transfers can be off-chain and free. However, withdrawing funds to an external self-custody wallet will always incur network costs.

Payment Method Fees

The financial institution processing the fiat transfer may also charge fees. Sending money internationally or between different banks often incurs a cost. Digital wallets may charge a percentage for commercial transactions or transfers.

Traders must calculate these external costs when determining profitability. A trade that looks profitable on the platform might result in a net loss if the banking fees are too high. Savvy P2P traders select payment methods that offer free or low-cost domestic transfers to maximize efficiency.

Risks Specific to P2P Trading

While P2P trading empowers users, it shifts the responsibility of security onto the individual. The lack of a centralized intermediary handling the fiat means that users must be vigilant against social engineering and fraud. Understanding common scams is the first step in prevention.

One prevalent risk is the "chargeback" fraud. This occurs when a buyer completes a trade and receives the cryptocurrency, only to later contact their bank or payment provider to reverse the fiat transaction. They might claim the transaction was unauthorized. Since crypto transactions are irreversible and fiat transactions often are not, the seller loses both the money and the assets.

Another common tactic is the "fake receipt" scam. A buyer might manipulate a screenshot or generate a fake banking confirmation email to convince the seller that payment has been sent. If the seller releases the crypto without verifying the balance in their actual bank account, the funds are lost.

Man-in-the-Middle Attacks

A more sophisticated threat involves a man-in-the-middle attack. In this scenario, a scammer opens a trade with a victim on a P2P platform. Simultaneously, the scammer opens a trade with a third party on a different platform or context. They trick the victim into sending money to the third party, thinking they are paying the scammer.

The scammer then claims the payment from the third party, leaving the victim without their crypto. To prevent this, platforms warn users not to accept payments from third-party accounts. The name on the bank account sending the money must match the verified name on the P2P profile.

Regulatory Hurdles

Regulatory risk is another consideration. Governments in some regions may crack down on P2P trading or freeze bank accounts suspected of being involved in crypto transactions. Traders operating with high volumes are particularly susceptible to having their banking relationships terminated if their activity triggers anti-money laundering flags.

Users must be aware of the legal status of crypto trading in their specific jurisdiction. Operating a P2P business without proper licensing can lead to legal consequences in countries with strict financial regulations.

P2P vs. Centralized Exchange Off-Ramps

Deciding between a P2P platform and a centralized exchange (CEX) for off-ramping depends on the user's specific needs regarding speed, cost, and privacy. Each method has distinct advantages and disadvantages that cater to different user profiles.

Centralized exchanges offer convenience and high liquidity. For users in jurisdictions with integrated banking support, withdrawing fiat from a CEX to a linked bank account is seamless and often automated. The fees are transparent, and the process requires little active management.

However, CEX withdrawals can be slow, taking several days to clear via traditional banking rails. They also require full identity verification, leaving a definitive record of the user's crypto activities. In times of high market stress, centralized exchanges may pause withdrawals due to liquidity crunches or technical issues.

P2P platforms, conversely, offer speed and flexibility. Funds can often be accessed in minutes, even on weekends or holidays when traditional banks are closed. The decentralized nature of the liquidity means that even if one seller runs out of funds, others are available.

| Feature | Centralized Exchange (CEX) | P2P Platform |

|---|---|---|

| Speed | 1-5 Business Days | Minutes to Hours |

| Privacy | Low (Full KYC) | Variable (KYC to No-KYC) |

| Cost | Fixed Fees | Spread + Fees (Variable) |

The cost of P2P trading is generally higher due to the premiums charged by sellers. Users effectively pay for the convenience, speed, and privacy that the peer-to-peer model provides. For large institutional transfers, CEXs are usually more cost-effective, while P2P dominates the retail market for smaller, faster transactions.

Regulatory Landscape for Regional Platforms

The regulatory environment for P2P platforms is evolving rapidly. As governments seek to bring the cryptocurrency industry under compliance frameworks, P2P platforms face increasing pressure to implement strict monitoring.

In some regions, P2P trading operates in a gray area. It is not explicitly illegal, but banks may be hostile toward it. In these environments, P2P platforms serve as a vital lifeline, allowing the crypto ecosystem to function despite the lack of official support.

Conversely, some jurisdictions have embraced P2P platforms, establishing clear licensing regimes. These regulated P2P marketplaces offer high security but reduced privacy. They act as formal money service businesses, reporting suspicious activity to financial intelligence units.

This patchwork of regulations means that the availability and features of P2P platforms vary significantly by country. A platform that is dominant in Southeast Asia might be unavailable in the United States due to different legal requirements. Users must navigate this landscape by choosing platforms that are compliant and operational within their specific region.

Conclusion

Localized P2P platforms and fiat off-ramps are indispensable components of the global cryptocurrency infrastructure. They provide the necessary flexibility for users to move between the digital and physical financial worlds. By leveraging local payment networks, escrow systems, and reputation mechanics, these platforms solve the complex problem of global financial access.

Success in P2P trading requires a proactive approach to security and a clear understanding of market mechanics. Traders must weigh the benefits of speed and accessibility against the potential risks of scams and higher fees. As the regulatory landscape shifts, these platforms will likely continue to evolve, bridging the gap for the unbanked and providing liquidity where it is needed most.

Peer-to-peer platforms are the vital capillaries of the crypto system, delivering liquidity to regions that centralized arteries cannot reach.