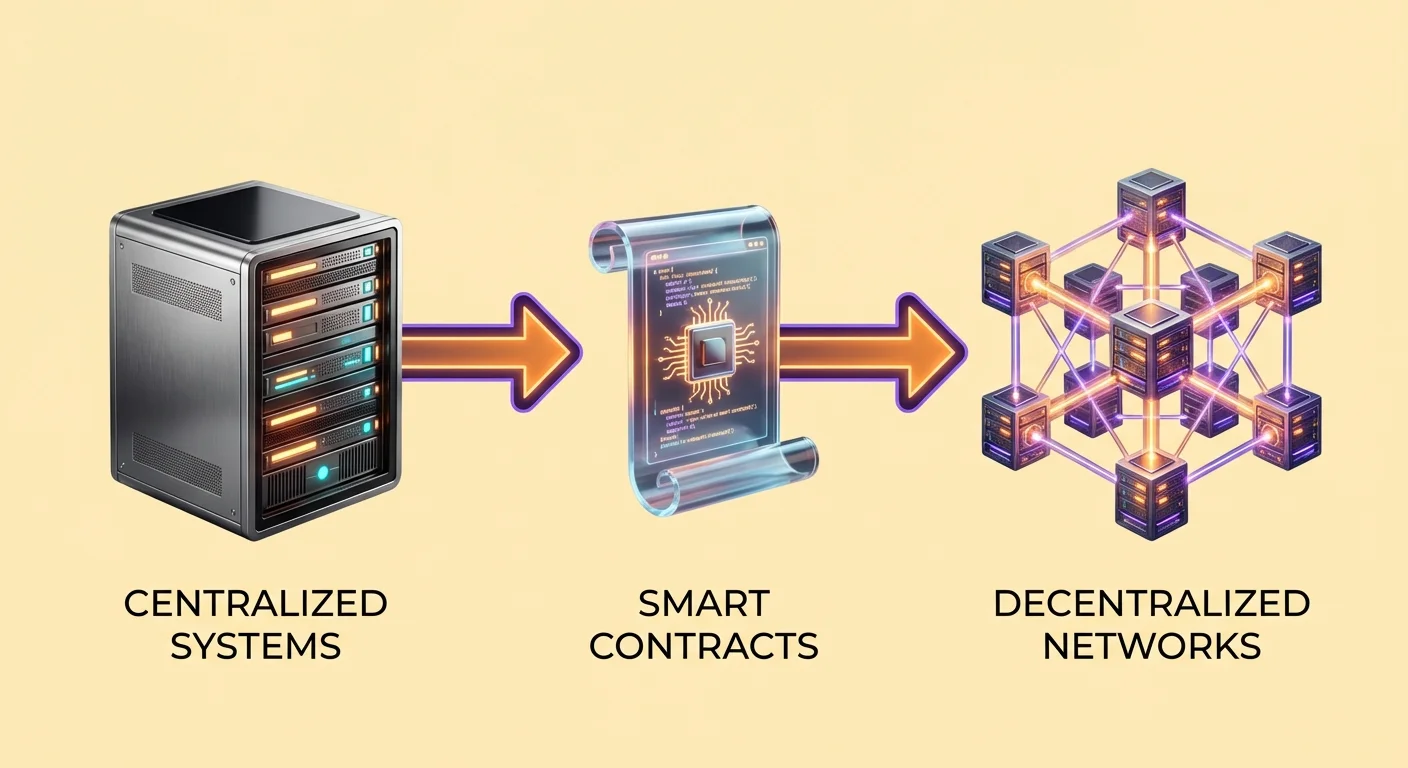

The shift from traditional internet infrastructure to decentralized systems marks a fundamental change in how digital applications operate. In the standard web model, users interact with centralized servers controlled by specific entities. These entities manage data, execute code, and maintain the authority to grant or revoke access.

Web3 introduces a different paradigm where applications run on a peer-to-peer network of computers rather than a single server farm. This infrastructure relies on blockchain technology to maintain a shared, immutable record of transactions and program states. The result is a system where no single party controls the network.

This transition creates an environment that is "trustless." This does not mean the system is unreliable. It means users do not need to trust a third-party institution, such as a bank or a tech company, to act honestly. Instead, trust is placed in code and cryptographic verification. The validity of information and the execution of agreements are verifiable by anyone on the network.

The Architecture of Smart Contracts

Defining the Digital Protocol

At the heart of this decentralized infrastructure lies the smart contract. A smart contract is a computer program stored on a blockchain that runs when predetermined conditions are met. While the concept exists on various networks, platforms like Ethereum accounts and contracts popularized the technology by acting as a "Turing complete state machine." This essentially creates a shared global computer accessible to anyone with an internet connection.

These contracts function as the backend logic for decentralized applications. Unlike standard software where the code sits on a private server, smart contracts live on the public ledger. This ensures that once a contract is deployed, its operation is transparent. Anyone can inspect the code to understand exactly how it will behave under specific circumstances.

The deterministic nature of these contracts is a defining feature. If a user provides input A, the contract will invariably produce output B. This predictability eliminates the ambiguity often found in human-mediated agreements. There are no intermediaries to interpret the rules or alter the outcome based on subjective judgment.

Execution and Interaction

The mechanics of a smart contract rely on address-based interactions. When a developer finishes writing the code, they deploy it to the network. This action creates a specific address for the contract. Users interact with the program by sending assets or data to that address. This transaction triggers the code to execute automatically based on its pre-defined rules.

For example, a simple contract could function as a digital trust fund. The code might specify that a deposit of 1 ETH should be divided into twelve equal parts. The contract would then release one part to a designated beneficiary wallet every month. This process occurs without a lawyer or bank managing the escrow. The code itself holds custody of the funds and enforces the release schedule.

This automation extends to complex financial instruments. In a decentralized lending scenario, the contract manages collateral. If a borrower’s collateral value drops below a set threshold, the contract automatically triggers a liquidation event. It sells the asset to cover the debt, protecting the lender’s capital without human intervention.

Understanding Decentralized Applications (dApps)

Components of a dApp

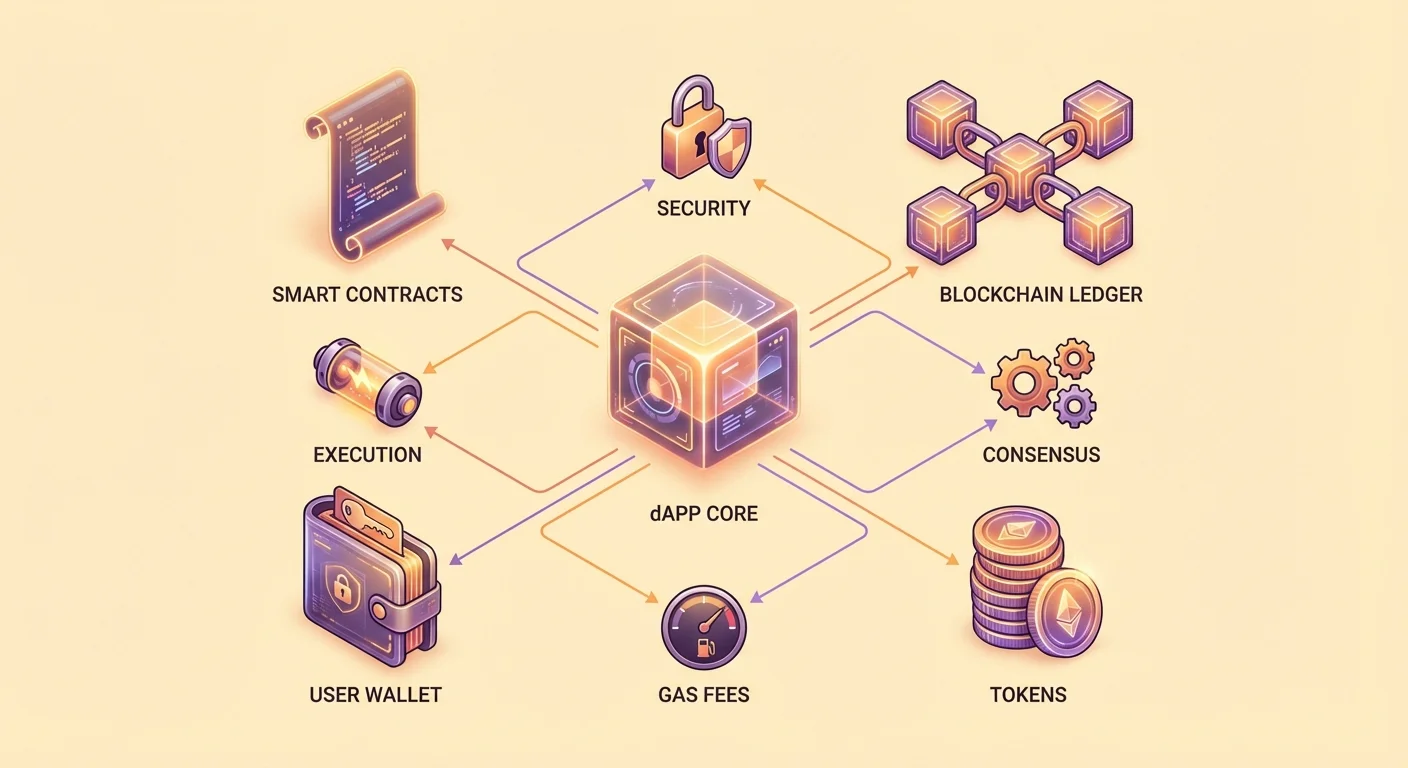

A Decentralized Application, or dApp, combines smart contracts with a user interface. While the backend logic runs on a blockchain, the frontend often resembles a standard website or mobile app. This frontend allows users to interact with the underlying smart contracts without needing to understand complex command-line code.

Most dApps rely on three core components to function. The first is the smart contract collection that defines the business logic. The second is the blockchain itself, which serves as the immutable database and settlement layer. The third component is the token. Actions on a blockchain require "gas," a fee paid in the network's native currency to compensate the computers processing the transaction.

Many dApps also utilize specific tokens to facilitate internal operations. These assets can represent voting rights, partial ownership, or utility within the application. For instance, a dApp might issue a token that grants holders a share of the revenue generated by the platform. This tokenization model aligns the incentives of the developers, the users, and the infrastructure providers.

The Permissionless Ecosystem

A key distinction of dApp infrastructure is that it is permissionless. Traditional financial apps require users to create accounts, verify identities, and gain approval from the service provider. dApps generally require only a crypto wallet. Anyone with a wallet address can connect to the application and interact with its smart contracts.

This openness fosters global accessibility. A user in a region with limited banking infrastructure can access the same financial services as a user in a major financial hub. The application does not discriminate based on geography or status. However, users must remain aware that local regulations regarding finance and taxation still apply to their activities.

Consider a decentralized dice game as a practical example. In a traditional online casino, the code running the game is hidden. Players must trust the casino's claim that the odds are fair. In a dApp version, the game logic resides in an open-source smart contract. A user can inspect the code to verify that the "house edge" is exactly 1% and that the random number generator is functioning correctly.

Infrastructure Trade-offs: Speed vs. Security

The choice to use decentralized infrastructure involves specific trade-offs. Centralized cloud services like Amazon Web Services (AWS) offer immense computing power at low costs. They can process thousands of transactions per second with minimal latency. However, this efficiency comes at the cost of centralization. If the central server fails or the provider decides to censor a user, access is lost.

Decentralized networks prioritize security and transparency over raw speed. Every transaction on a blockchain must be verified by multiple independent nodes spread across the globe. This consensus mechanism ensures that the network history cannot be altered, but it inherently slows down the system. Processing data on a decentralized network is significantly more expensive and slower than on a centralized server.

This dynamic creates a specific use case profile for dApps. They are not currently suitable for high-frequency trading or data-heavy streaming services. Instead, they excel in scenarios where trust and asset ownership are paramount. Applications involving high-value exchanges, digital identity, or immutable record-keeping benefit most from the security guarantees of blockchain infrastructure.

| Feature | Centralized Application | Decentralized Application (dApp) |

|---|---|---|

| Control | Single entity (Company) | Community / Distributed Network |

| Data Storage | Private Servers | Public Blockchain Ledger |

| Trust Model | Trust in Authority | Trust in Code (Verify) |

The Financial Layer: DeFi Architecture

Automated Yield Strategies

Decentralized Finance, or DeFi, represents the largest sector of dApp development. These applications replicate and enhance traditional financial services using blockchain technology. A primary use case is yield generation. In traditional finance, a bank takes customer deposits, lends them out, and keeps the majority of the profit.

In DeFi, users deposit assets directly into smart contracts. These contracts pool capital from various sources and deploy it into yield-generating strategies. For example, the funds might be lent to other users or provided as liquidity for trading. The profit generated from these activities is distributed automatically to the depositors.

The distribution follows strict rules written into the code. The smart contract calculates the exact share of profits owed to each participant based on their contribution. It distributes these rewards at set intervals. This automation reduces the overhead costs associated with physical bank branches and middle management. Consequently, the yields offered in DeFi are often higher than those in traditional savings accounts.

Decentralized Exchange Mechanisms

Another pillar of DeFi infrastructure is the Decentralized Exchange (DEX). These platforms allow users to trade digital assets without handing custody to a third party. In a centralized exchange, users deposit funds into a wallet controlled by the company. The company then executes trades on an internal ledger.

A DEX functions differently. It utilizes smart contracts to facilitate peer-to-peer trading. Users retain control of their private keys throughout the process. The trade occurs directly between the user's wallet and the smart contract. This eliminates the counter-party risk of an exchange becoming insolvent or freezing user funds.

To ensure there are enough assets available for trading, DEXs use liquidity pools. They incentivize users to deposit pairs of assets into smart contracts. These depositors, known as liquidity providers, earn a percentage of the trading fees generated by the protocol. This system crowdsources liquidity, allowing markets to form without a centralized market maker.

Lending Protocols and Risk Management

Smart contract-based lending demonstrates how code serves as a risk manager. In this system, borrowers do not need credit checks. Instead, they must provide collateral. The smart contracts enforce strict collateralization ratios to protect the lenders' capital.

For instance, a protocol might require a 2:1 over-collateralization ratio. To borrow $1,000 worth of a stablecoin, a user might need to deposit $2,000 worth of Ethereum (ETH). The smart contract holds this ETH as insurance. The borrower can use the loan for other purposes while still maintaining exposure to the price movements of their deposited ETH.

The risk management logic is automated. If the market price of ETH falls, the value of the collateral drops. If it falls below a predetermined safety threshold, the smart contract triggers a liquidation. It effectively seizes the collateral to repay the loan. This deterministic process ensures that the system remains solvent even during periods of high market volatility.

Users must understand the implications of this automation. There is no loan officer to negotiate with during a market crash. If the conditions for liquidation are met, the code executes immediately. This removes human bias but also removes human leniency.

Governance and Token Distribution

The Role of Airdrops

Projects often use token distributions to decentralize governance and ownership. An "airdrop" is a common mechanism where a project sends free tokens to user wallets. This strategy serves multiple purposes: it rewards early adopters, distributes voting power, and markets the platform to a wider audience.

Airdrops typically rely on a "snapshot" mechanism. The project developers designate a specific block number or date as the cut-off point. They scan the blockchain history to identify all wallets that interacted with their smart contracts before that time. Qualifying actions might include trading volume, liquidity provision, or holding a specific NFT.

For example, a decentralized exchange might airdrop tokens to anyone who traded on the platform prior to a certain date. This instantly creates a community of token holders who have a vested interest in the protocol's success. These tokens often carry governance rights, allowing holders to vote on changes to the protocol's parameters or fee structures.

Token Sales and Fundraising

Smart contracts also revolutionize fundraising through token sales, often called Initial Coin Offerings (ICOs). In this model, a project creates a smart contract that sells a new token in exchange for an established cryptocurrency like ETH. The contract defines the rules of the sale, including the price, the total supply, and the vesting schedule.

This method democratizes investment access. In traditional venture capital, early investment rounds are often restricted to accredited investors and institutions. A token sale via smart contract can be open to anyone with a wallet. This allows the community to own a piece of the network they use from day one.

However, the ease of creating tokens also introduces risks. Because the process is permissionless, anyone can create and sell a token. This has led to a proliferation of projects with little to no utility. Smart contracts can enforce vesting schedules to prevent developers from selling all their tokens immediately, providing a layer of assurance to investors.

Security Risks in Decentralized Infrastructure

Vulnerabilities in Code

While the concept of "code is law" provides certainty, it also presents significant dangers. Smart contracts are written by humans, and human code often contains bugs. If a smart contract has a vulnerability, hackers can exploit it to drain funds. Unlike a banking app where a fraudulent transaction can be reversed, blockchain transactions are immutable.

Audits are a critical defense mechanism. Reputable projects hire third-party security firms to review their code before deployment. These auditors look for logic errors and known vulnerabilities. However, an audit is not a guarantee of security. Even audited contracts have been exploited when unforeseen interaction vectors are discovered.

The open-source nature of dApps creates a double-edged sword. On one hand, it allows the community to verify the code and fix bugs over time. On the other hand, it gives attackers a blueprint of the system. They can study the contracts in detail to find weaknesses to exploit before the developers notice them.

Phishing and Malicious Interfaces

Security risks also exist at the user interface level. A common attack vector is the phishing dApp. Scammers create websites that look identical to legitimate DeFi platforms. They might change one letter in the URL or buy ads to appear at the top of search results.

When a user connects their wallet to a phishing site, they believe they are interacting with a trusted protocol. However, the site prompts them to sign a malicious transaction. Instead of depositing funds into a yield-generating contract, the transaction grants the attacker permission to move the user's assets. Once signed, the attacker drains the wallet.

Users must exercise extreme caution with URLs and permissions. Verifying the website address and checking for security certificates are essential habits. Additionally, users should be wary of new or unaudited projects. A "rug pull" occurs when developers of a malicious dApp intentionally leave a backdoor in the code or simply steal the liquidity they promised to lock.

Future Applications of Web3 Infrastructure

The utility of smart contracts extends beyond finance. As the technology matures, it is being applied to supply chain management. A product's journey from factory to consumer can be tracked on a blockchain. Smart contracts can verify authenticity at every step, reducing counterfeiting and ensuring transparency in logistics.

Voting and governance represent another frontier. Traditional voting systems are often opaque and difficult to audit. A blockchain-based voting system uses smart contracts to tally votes. This ensures that every vote is counted correctly and that the results are verifiable by any observer. This could revolutionize corporate governance and eventually public elections.

Decentralized identity is also gaining traction. Currently, users rely on centralized authorities like Google or Facebook to manage their digital identities. Smart contracts allow users to own their identity data. They can prove their credentials or age to a third party without revealing unnecessary personal information or relying on a tech giant as an intermediary.

Conclusion

The transition to decentralized infrastructure represents a significant shift in how digital value and data are managed. By replacing centralized intermediaries with smart contracts, dApps offer a transparent and permissionless alternative to traditional systems. This technology empowers users to retain custody of their assets, verify the rules of engagement, and participate in global financial markets without barriers.

However, this autonomy requires a higher level of personal responsibility. The immutable nature of blockchain transactions means that errors cannot be easily rectified. Users must navigate the risks of technical exploits and social engineering with vigilance. As the ecosystem evolves, the balance between the efficiency of centralized systems and the security of decentralized networks will continue to define the digital landscape.

True ownership in Web3 requires verifying the code you trust and securing the keys you hold.