Decentralized finance represents a fundamental shift in how individuals interact with economic systems. By removing intermediaries like banks and brokers, users gain direct control over their assets through software known as decentralized applications. These applications operate on permissionless networks, meaning anyone with a wallet address can participate in lending, trading, or borrowing activities. While this open environment fosters innovation and financial inclusion, it also shifts the burden of security entirely onto the user.

In traditional finance, regulatory bodies and insurance protections often provide a safety net against fraud or bank failures. If a credit card is stolen, the issuer can reverse the transaction. In the decentralized world, transactions are immutable. Once funds are sent to a smart contract or another wallet, the action cannot be undone by a central authority. This reality makes understanding the mechanics of these applications vital for asset preservation.

The potential for high yields and automated financial services attracts millions of users to the blockchain ecosystem. However, the lack of guardrails means that technical competence and vigilance are prerequisites for safety. Security in this space is not just about using strong passwords. It involves vetting protocols, understanding code auditing, and recognizing the subtle signs of malicious interfaces.

To navigate this landscape safely, one must understand the underlying technology that powers these interactions. The risks are not merely theoretical. They range from simple human errors in code to sophisticated social engineering attacks designed to siphon funds from unsuspecting users. Knowledge of these mechanisms is the strongest defense against loss.

The Architecture of Decentralized Applications

Smart Contracts as the Engine

At the core of every decentralized application lies the smart contract. These are computer programs stored on a blockchain that execute automatically when specific conditions are met. They function like digital vending machines. When a user inputs a specific asset and selects an action, the code executes the transaction without the need for a clerk or intermediary. While often associated with Ethereum, smart contracts exist on various networks, including Bitcoin, though with differing levels of complexity.

Ethereum introduced the concept of a "Turing complete" state machine. This allows for highly complex computations that go beyond simple value transfers. Developers can write contracts that mimic intricate financial instruments, create games, or manage supply chains. The defining characteristic of these contracts is that they are "trustless." This does not mean they are unreliable. Instead, it means users do not need to trust a human counterparty to honor an agreement.

The validity of the contract is verified by the network itself. Because the code is typically open source, anyone with the technical knowledge can inspect it to verify its logic. This transparency stands in stark contrast to traditional banking software, which is closed and proprietary. However, this openness also creates a unique security dynamic where attackers can study the code to find weaknesses before users discover them.

The Frontend and Backend Structure

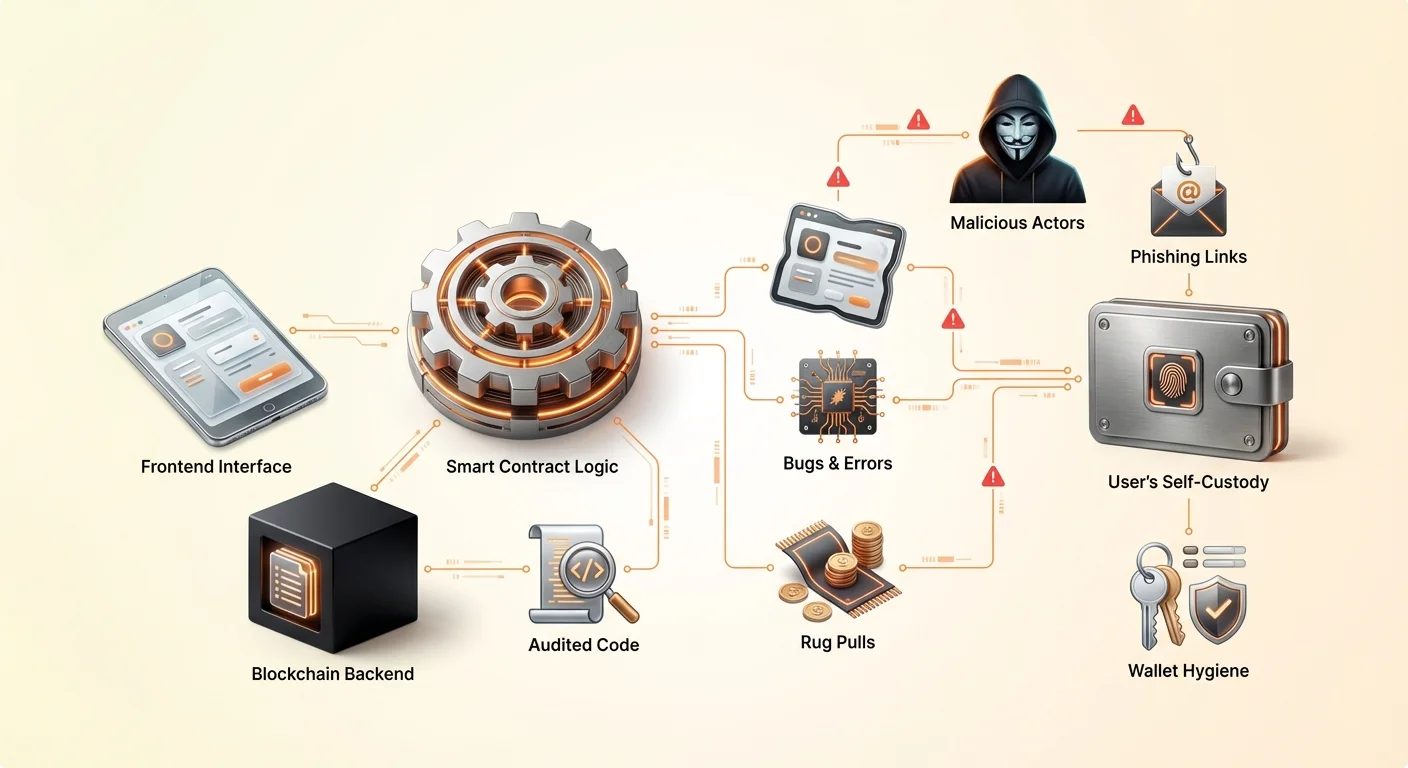

A decentralized application, or DApp, generally consists of two main parts. The backend is the smart contract code living on the blockchain. This handles the logic, state changes, and asset transfers. The frontend is the user interface, usually a website or mobile app, that allows humans to interact with the smart contract easily.

When a user connects their wallet to a DApp, the frontend translates their button clicks into transaction requests. The wallet then asks the user to sign these requests to authorize the smart contract to act. This separation is critical to understand because security flaws can exist in either layer. A perfectly secure smart contract can be compromised if the frontend website is hijacked to send transactions to a thief's address instead of the legitimate contract.

Permissionless Access and Innovation

One of the most powerful features of this architecture is that it is permissionless. In traditional finance, accessing high-yield investment products often requires accreditation or geographic residence in specific jurisdictions. In the decentralized ecosystem, the smart contract does not know a user's identity, credit score, or location. It only recognizes the wallet address and the assets held within it.

This lowers the barrier to entry significantly. A person in a region with limited banking infrastructure can access the same global liquidity pools as a hedge fund manager. This democratization of finance drives efficiency by enabling "crowd-sourced" liquidity. For example, decentralized exchanges incentivize users to deposit assets into trading pools. In return, these users earn a share of the trading fees, effectively becoming the "bank" themselves.

Vulnerabilities in Code Design

The functionality of decentralized applications relies entirely on the quality of the code written by developers. Since smart contracts are deterministic, they will execute exactly as written, even if the code contains a mistake. This leads to the risk of interacting with a poorly designed DApp. Even well-intentioned developers can introduce bugs that jeopardize user funds.

Human error is an unavoidable reality in software development. In centralized tech, a bug might cause an app to crash or a page to load incorrectly. In the blockchain environment, a bug can result in the permanent locking of funds or allow an attacker to drain a liquidity pool. These exploits often occur without any "hacking" in the traditional sense. The attacker simply uses the contract's own logic against it to produce an unintended result.

The open-source nature of these protocols means that the code is available for everyone to see. This is generally a strength, as it allows the community to fix bugs and improve security over time. Protocols that have existed for years tend to be more battle-tested. However, for new projects, this transparency invites scrutiny from black-hat actors looking for immediate exploits before the developers can patch them.

Malicious Projects and Rug Pulls

The Mechanics of a Rug Pull

Beyond accidental bugs, the decentralized space is plagued by deliberate fraud. The most common form is the "rug pull." This occurs when a team of developers creates a project that appears legitimate but is designed to steal user funds. They may launch a new token and pair it with a valuable cryptocurrency like Ethereum or USDC in a liquidity pool to attract traders.

The developers typically control a vast majority of the new token's supply or retain special administrative privileges in the smart contract. Once unsuspecting users purchase the token or deposit assets into the protocol, the developers trigger the trap. They might sell all their tokens at once, crashing the price to zero, or withdraw all the liquidity from the exchange. This leaves investors holding worthless assets while the perpetrators walk away with the valuable cryptocurrency.

Insider Control and Anonymity

A key factor facilitating these scams is the anonymity prevalent in the sector. Unlike traditional corporations where executives are doxxed and liable, many DeFi project founders remain anonymous. While anonymity protects privacy and prevents censorship, it also removes accountability. If an anonymous team abandons a project or executes a scam, there is often no legal recourse for the victims.

Participants must carefully judge whether a smart contract is safe based on code and reputation rather than legal guarantees. Fraudsters often dangle extremely high yield rates to prey on the fear of missing out. Early participants might get paid to create an illusion of legitimacy, but the system is often unsustainable. When the inflow of new capital slows, or the insiders decide to cash out, the project collapses.

Backdoors and Hidden Exploits

In some sophisticated attacks, the malicious intent is hidden deep within the code. A developer might program a "backdoor" that allows them to bypass normal restrictions. For example, a contract might claim to lock liquidity for a year, but a hidden function allows a specific address to unlock it immediately.

Alternatively, the code might allow the creator to mint an infinite number of tokens. They can then dump these tokens onto the market, devaluing everyone else's holdings. These exploits are difficult for the average user to detect without technical auditing skills. The presence of a professional-looking website and an active social media community is not proof that the underlying smart contracts are honest or secure.

The Phishing Threat in Web3

Even if a DApp is well-designed and the team is honest, users face external threats like phishing. This is one of the most pervasive risks in the crypto ecosystem. Phishing involves tricking a user into believing they are interacting with a legitimate service when they are actually communicating with an imposter.

In the context of DApps, attackers often create replica websites. They might register a domain that differs from the original by a single letter or uses a different extension. For instance, if the real site is "exchange.com," the attacker might use "exchange.io" or "exchangé.com." The fake site looks identical to the real one, copying its logos, layout, and user interface perfectly.

When a user connects their wallet to this fraudulent site, they are not connecting to the safe, audited smart contract of the real project. Instead, the site prompts them to approve a transaction that gives the attacker permission to spend their funds. Once the user signs this permission, the attacker can drain the wallet of specific assets. This can happen instantly, regardless of the security of the underlying blockchain.

To avoid this, users must develop a habit of double-checking URLs. Bookmarking known, legitimate sites is safer than relying on search engine results, which can sometimes display ads for phishing sites. Additionally, checking for the lock icon in the browser bar ensures the connection is encrypted, although this alone does not guarantee the site is legitimate—only that the connection to it is secure.

The Role and Reality of Audits

Understanding the Audit Process

To mitigate risks, reputable projects hire third-party security firms to conduct code audits. An audit involves a detailed review of the smart contract code to identify bugs, security vulnerabilities, and logic errors. Auditors use a combination of automated testing tools and manual line-by-line inspection to ensure the contract behaves as intended.

Once the review is complete, the auditing firm issues a report. This report highlights any issues found and classifies them by severity, such as critical, major, or minor. The project developers are then expected to fix these issues before deploying the contract or effectively launching the application. A final report is usually released confirming that the fixes have been implemented.

Why Audits Are Not Fail-Safe

While audits are a crucial layer of security, they are not a guarantee of safety. An audit is a snapshot in time. It verifies the code that was presented to the auditors, but it cannot predict how that code might interact with other protocols in the complex "money lego" ecosystem of DeFi. Furthermore, auditors are human and can miss subtle vulnerabilities.

There have been numerous instances where audited projects were subsequently hacked. Sometimes the exploit involves an economic attack rather than a coding error, which might fall outside the scope of a standard code audit. Additionally, if a project updates its contracts after an audit without getting a re-audit, the new code could introduce vulnerabilities that the original report did not cover.

Evaluating Audit Reports

For users, simply seeing a "Audited" badge on a website is insufficient. It is important to verify who performed the audit. Reputable firms have a track record of thoroughness, while less rigorous services might miss glaring issues. Users should look for the actual audit report, which is often linked in the project's documentation or footer.

Reading the summary of an audit can reveal if the team resolved the identified issues. If a report shows critical vulnerabilities that were "acknowledged" but not fixed, it is a major red flag. Comparing reports from multiple firms also adds a layer of assurance. A project that has been audited by two or three independent firms is generally considered lower risk than one with a single audit or none at all.

Token Distribution and Airdrop Risks

Mechanisms of Airdrops

Airdrops are a popular method for projects to distribute tokens to a wide user base. This process involves sending free assets to wallets that meet certain criteria, such as early usage of a platform or holding a specific NFT. The goal is to bootstrap a community, decentralize governance, and market the project.

Projects typically take a "snapshot" of the blockchain at a specific date. Any usage or holdings recorded before that block number count toward eligibility. This mechanism incentivizes users to remain active across various protocols in hopes of receiving future rewards. Legitimate examples include governance tokens for decentralized exchanges or NFT drops for existing holders.

The Dark Side of Free Tokens

Scammers heavily exploit the excitement surrounding airdrops. A common tactic involves sending unsolicited tokens to random wallets. When the user notices these tokens and tries to trade or sell them, they are directed to a malicious website. Interacting with the smart contract to sell the token often grants the attacker permission to access other funds in the wallet.

Another risk involves "dusting attacks," where tiny amounts of crypto are sent to wallets to track the owner's identity or link multiple addresses together. While less directly dangerous to funds than phishing, it compromises privacy. Users should be extremely skeptical of any token that appears in their wallet unexpectedly. The safest practice is often to ignore these tokens entirely and never attempt to interact with them or the websites they advertise.

Token Sales and Vesting Schedules

Legitimate projects also distribute tokens through sales, sometimes called Initial Coin Offerings (ICOs). Smart contracts govern these sales, defining the price, quantity, and release schedule. This brings transparency to the fundraising process. However, the vesting schedule—the timeline for when tokens are unlocked—is a critical detail for investors.

If a project releases all tokens to early investors or the team immediately, they may dump them on the market, crashing the price. Smart contracts can enforce vesting periods, ensuring that tokens are released gradually over months or years. This aligns the incentives of the team with the long-term success of the project. Verifying these parameters in the contract or documentation is a key part of due diligence.

Navigating DeFi Lending and Trading

Decentralized finance replicates traditional services like lending and trading using autonomous protocols. In a smart contract-based lending platform, users deposit collateral to borrow other assets. To manage risk without a credit check, these loans are typically over-collateralized. For instance, a user might need to deposit $200 worth of Ethereum to borrow $100 worth of stablecoins.

The smart contract monitors the value of the collateral in real-time. If the market price of the collateral drops below a certain threshold, the contract automatically liquidates the asset to repay the loan. This creates a system that remains solvent without human intervention. However, it introduces the risk of liquidation volatility. A sudden market crash can wipe out collateral before a user has a chance to add more funds.

Trading on decentralized exchanges (DEXs) also carries unique nuances. Unlike centralized exchanges where the platform holds custody of assets, DEXs allow users to trade peer-to-peer via smart contracts. This eliminates counterparty risk regarding the exchange's solvency. However, it requires users to manage slippage—the difference between the expected price and the execution price—and network fees.

Comparative Risks of DApps vs. Centralized Apps

When choosing between decentralized and centralized applications, users must weigh distinct trade-offs regarding control, cost, and efficiency.

| Feature | Centralized Applications | Decentralized Applications (DApps) |

|---|---|---|

| Custody | Third-party holds funds | Self-custody (User holds funds) |

| Censorship | Can freeze accounts/transactions | Resistant to censorship |

| Speed | High throughput, fast | Limited by blockchain block times |

| Cost | Often lower (internal databases) | Higher (network gas fees) |

| Security | Single point of failure | Distributed, no single failure point |

Self-Custody and Security Practices

The foundation of using DApps safely is proper self-custody. This means the user controls their own private keys, which are the cryptographic proof of ownership for their assets. If these keys are lost, the funds are unrecoverable. If they are stolen, the funds are gone. There is no "forgot password" button in a decentralized network.

Users should utilize reputable wallets that facilitate connection to DApps via secure bridges. When connecting, it is crucial to review exactly what permissions are being requested. A standard connection usually only asks for the ability to view the wallet address. A transaction request, however, asks for permission to move funds.

Disconnecting from DApps after a session is a good hygiene practice. While staying connected doesn't automatically allow funds to be moved, it reduces the surface area for potential phishing if the DApp's interface is later compromised. For large holdings, using a hardware wallet provides an extra layer of physical security, requiring a button press on a device to approve any transaction initiated by a DApp.

Regulatory and Structural Considerations

While DApps offer censorship resistance, they often exist in a regulatory gray area. Governments are still developing frameworks to classify and regulate decentralized protocols. This creates uncertainty. A protocol could be deemed non-compliant, potentially affecting the value of its associated tokens or the ability of users in certain jurisdictions to access interfaces legally.

Furthermore, the structural limitations of blockchains affect the user experience. Decentralized networks process data slower than centralized servers because every transaction must be verified by multiple nodes. This results in lower throughput and higher costs per transaction. During times of network congestion, fees can spike, making small transactions economically unviable.

The lack of regulation also means there is no consumer protection agency to contact if things go wrong. In traditional finance, fraud can be investigated by law enforcement with subpoenas to banks. In DeFi, the perpetrators are often anonymous and funds are washed through mixers, making recovery nearly impossible. This underscores the reality that in the decentralized world, responsibility is the price of freedom.

Conclusion

Decentralized applications and smart contracts offer a compelling alternative to traditional finance, providing transparency, autonomy, and open access. The ability to trade, lend, and earn yield without intermediaries empowers individuals to become their own banks. However, this freedom is inextricably linked to risk. The immutable nature of the blockchain means that errors are permanent, and the open environment attracts both innovators and predators.

Navigating this space safely requires a shift in mindset. Users cannot rely on brand names or glossy interfaces as guarantees of safety. Instead, they must rely on verification: checking URLs, reading audit summaries, understanding smart contract logic, and maintaining strict wallet hygiene. The technology is powerful, but it is neutral; it secures the assets of the vigilant just as strictly as it enforces the losses of the careless.

You are the only person responsible for the security of your digital assets.