In the digital economy, the phrase “not your keys, not your coins” serves as a fundamental security maxim. It advocates for self-custody, the practice of holding your own cryptographic private keys and maintaining absolute control over your assets.

However, the reality of the crypto landscape is that centralized exchanges (CEXs) are indispensable. They act as essential gateways—the on-ramps and off-ramps—allowing you to convert fiat currency (like USD or EUR) into crypto, or to quickly trade between different digital assets. For many users, exchanges offer the liquidity, speed, and user experience required for active trading and initial purchases.

Therefore, for anyone serious about managing digital wealth, the question isn’t simply if you should use a centralized exchange, but how you can use one securely. This guide provides a pragmatic, security-focused roadmap for mitigating risk when trusting a third-party exchange with your funds, ensuring you are prepared for the unique vulnerabilities inherent in custodial services. We will move beyond the ideal of 100% self-sovereignty to focus on the essential best practices for minimizing exposure and protecting your assets during their necessary “transit time” on a custodial platform.

Understanding Custody and Its Risks

Before implementing security protocols, it is crucial to understand exactly what you are doing when you deposit funds into an exchange and what risks you inherit by choosing a custodial solution.

The Core Difference: Who Holds the Private Keys?

Custody refers to the safekeeping and control of your assets. In the cryptocurrency world, control is granted by the private key.

- Self-Custody (Non-Custodial): You hold the private keys. This means only you can approve transactions. If you lose your keys, your funds are gone; if you secure your keys properly, no one can take them from you, regardless of what happens to any exchange or third party. Examples include hardware wallets or desktop wallets where you control the seed phrase.

- Exchange Custody (Custodial): The exchange holds the private keys for the address where your assets reside. When you log in, the exchange authorizes transactions on your behalf, pulling funds from its vast pool of assets. You trust the exchange to manage and secure these keys, and to always honor your withdrawal request.

The fundamental risk of exchange custody is simple: you are an unsecured creditor. If the exchange fails, is hacked, or collapses, your right to withdraw your assets is dependent on the platform’s solvency and integrity.

Identifying the Primary Threats to Exchange Funds

When funds are held by a third party, the risk profile shifts away from protecting your physical key storage and toward protecting the institutional structure itself.

1. Platform Insolvency and Mismanagement

This is arguably the greatest current risk. If an exchange engages in poor financial management, takes on excessive debt, or inappropriately uses customer funds (often termed "rehypothecation"), it can become insolvent. When this happens, customers often face lengthy legal battles to recover a fraction of their deposited assets, as seen in numerous high-profile exchange failures.

2. Institutional Hacks and Exploits

While major exchanges employ sophisticated security teams, they remain massive honeypots for cybercriminals. A successful attack on an exchange’s hot wallet or centralized database can lead to the immediate and irreversible loss of billions in customer funds. Your personal account security (2FA) cannot protect you if the entire exchange infrastructure is breached.

3. Regulatory Seizure or Blacklisting

An exchange operates within a legal framework. If a government or regulator deems an exchange illegal, or requires the seizure of assets linked to specific individuals or regions, the exchange may be legally compelled to freeze or confiscate funds.

Foundational Security Measures for Custodial Accounts

While institutional hacks are outside your control, the vast majority of personal crypto theft still occurs due to user-side error: compromised credentials, weak passwords, or failure to implement proper two-factor authentication (2FA). These steps are your immediate defense against unauthorized access to your trading capital.

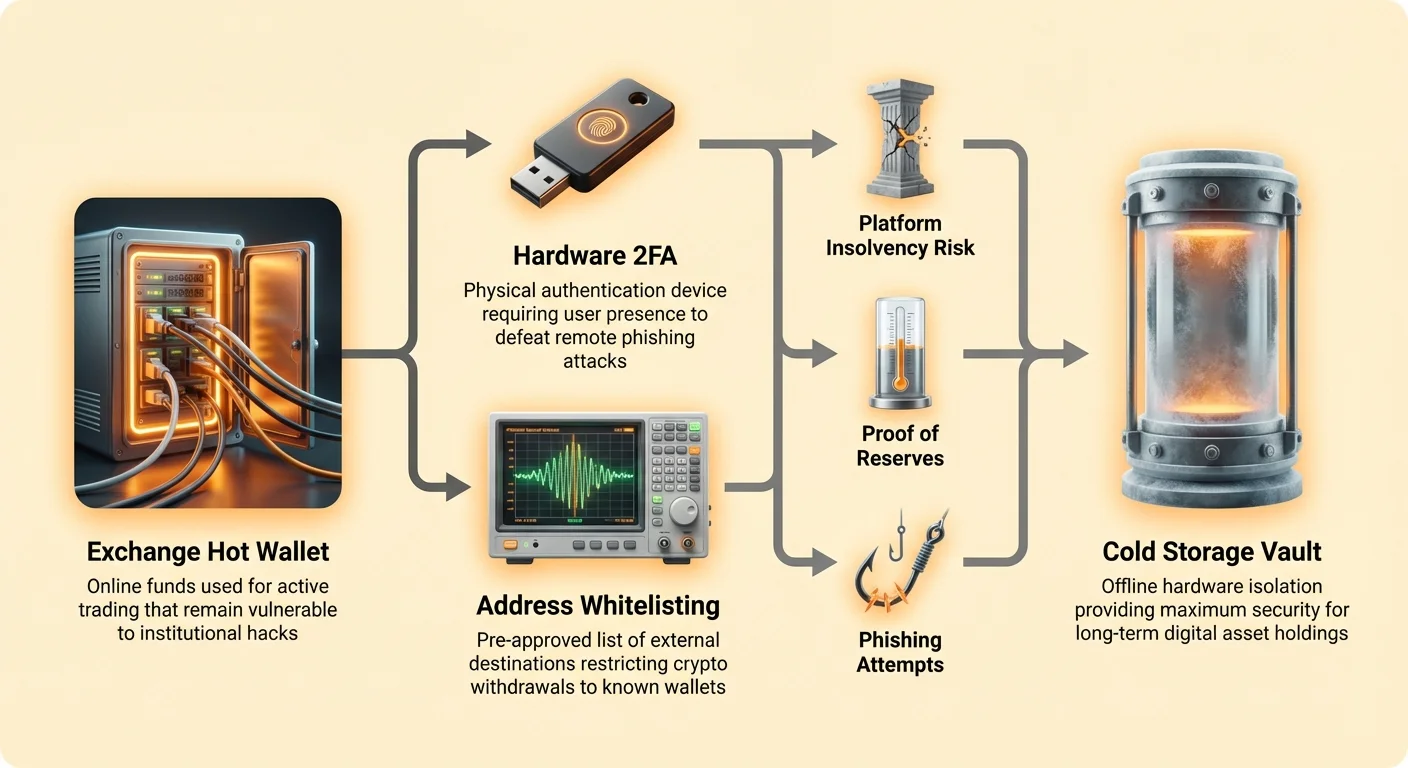

Implementing Robust Multi-Factor Authentication (2FA)

2FA adds a necessary layer of protection beyond a username and password. If a hacker steals your login credentials, they still cannot access your account without a second factor.

The Hierarchy of 2FA Security:

- Unacceptable (SMS/Text): Using SMS for 2FA is widely considered insecure. SIM-swap attacks allow hackers to redirect your text messages to a device they control, bypassing this security layer instantly.

- Acceptable (Authenticator Apps): Time-based One-Time Password (TOTP) apps like Google Authenticator or Authy generate codes locally on your phone. This is a significant improvement over SMS. Best Practice: Ensure you back up your TOTP seeds securely, in case you lose your phone.

- Gold Standard (Hardware Security Keys): Physical devices like YubiKey or Google Titan Keys use the FIDO standard, providing the highest level of security. They require a physical presence (touching the key) to authenticate. Hardware keys are immune to phishing attacks, as the key communicates directly with the legitimate website domain. Use hardware keys for your primary exchange accounts.

Account Whitelisting and Withdrawal Controls

Exchanges provide tools designed to slow down or block a hacker who has gained access to your account. You must activate and utilize these features immediately.

Address Whitelisting

This feature allows you to pre-approve a list of external crypto addresses (typically your own self-custody wallet addresses) to which you can send funds. If a hacker compromises your account, they cannot immediately send your crypto to their own unknown wallet because the withdrawal address has not been whitelisted.

- Actionable Tip: Enable address whitelisting immediately. Set a required security delay (e.g., 24 or 48 hours) for adding a new withdrawal address. This delay provides you with a crucial window to notice unauthorized activity and freeze the account.

Withdrawal Limits and Velocity Checks

Set limits on the maximum amount you can withdraw in a 24-hour period. While this may slightly inconvenience large traders, it drastically limits the damage a hacker can inflict before you detect the breach.

Mastering Phishing and Social Engineering Prevention

Phishing is the act of tricking you into voluntarily giving up your credentials. Exchanges are a prime target for these sophisticated attacks.

- Always Check the URL: Before entering credentials, verify that the URL is 100% correct (e.g.,

exchange.com, notexchange-login.com). Bookmark the official login page and always access it through the bookmark. - Never Click Email Links for Login: Exchanges will often send email notifications, but never click a link in an email to log in. Navigate directly to the site.

- Use a Separate Email: Use a unique, robust, dedicated email address only for your crypto exchange accounts. This reduces the surface area for data breaches from other less secure services.

Evaluating Exchange Reliability and Transparency

Since the security of your funds depends on the integrity of the institution, part of your risk mitigation strategy must involve rigorous due diligence on the platforms you choose.

Proof of Reserves and Auditing Mechanisms

Following several major exchange collapses, the demand for verifiable assurance that exchanges actually hold the assets they claim to hold has intensified.

Proof of Reserves (PoR) is a cryptographic method where an exchange proves that the crypto assets they hold in their reserve wallets match or exceed the liability owed to their customers. This is typically achieved using a Merkle Tree structure, allowing users to verify their specific balance is included in the certified total without revealing the balances of other users.

- What to Look For: Choose exchanges that regularly publish audited Proof of Reserves reports (monthly or quarterly) verified by reputable, independent third-party auditors. PoR doesn't guarantee solvency (the exchange could still have hidden fiat debts), but it provides transparency regarding the crypto assets held.

Internal Security Protocols and Cold Storage Policy

Reputable exchanges segregate customer assets into different storage types based on risk.

- Hot Storage (Online): Used for instant withdrawals and trading liquidity. This is fast but vulnerable to online hacks. Only a small percentage of total assets should be kept in hot storage.

- Cold Storage (Offline): Secured on devices completely disconnected from the internet. This is the safest way to store the vast majority of customer funds.

Due Diligence Questions: While specifics are proprietary, a secure exchange should clearly communicate the percentage of customer funds kept in cold storage (ideally 95% or higher) and detail the robust multi-signature protocols and geographically dispersed vaults they use to secure these offline keys.

Regulatory Compliance and Geographic Factors

The regulatory environment significantly impacts asset security and consumer protections.

- Jurisdiction Matters: An exchange regulated in a jurisdiction with stringent financial oversight (e.g., the US, EU, or specific Asian financial hubs) generally offers greater legal recourse and adherence to AML/KYC standards than an unregulated offshore entity.

- KYC Requirements: While some users seek "No KYC" (Know Your Customer) exchanges for privacy, regulated exchanges require KYC precisely because it provides a legal framework for accountability and fraud prevention, which ultimately adds a layer of institutional security for your deposited funds.

Navigating Insurance, Terms, and Loss Scenarios

A critical step in minimizing exchange risk is understanding what happens when the worst-case scenario (platform failure or institutional hack) occurs. The common misconception is that crypto exchanges are insured like traditional banks.

Understanding Exchange Insurance Policies

Traditional Banks (Fiat): In many countries (like the US with FDIC insurance), your fiat deposits are insured up to a high limit. This insurance covers losses if the bank itself fails or becomes insolvent.

Crypto Exchanges: Exchange insurance is highly nuanced and often misinterpreted.

- Operational vs. Crypto Asset Insurance: Many exchanges carry commercial insurance policies that cover internal operational risks, such as employee theft, gross negligence, or physical loss of cold storage hardware. They typically do not insure against loss due to insolvency, massive market volatility, or sophisticated platform-wide hacks.

- Coverage Specificity: If an exchange advertises insurance, carefully read the policy's fine print. Often, the insurance only covers the portion of assets held in hot wallets, or it is a blanket policy covering the institution, which may not be sufficient to cover all customer losses.

- Fiat vs. Crypto: Any FDIC or equivalent insurance an exchange may mention typically applies only to the fiat currency you hold on the platform, not your digital assets.

Best Practice: Operate under the assumption that your cryptocurrency deposited on an exchange is uninsured against catastrophic platform failure. This mindset reinforces the need for self-custody for long-term holdings.

Regulatory Guarantees vs. Crypto Asset Guarantees

When reviewing Terms of Service (ToS), look closely at how the exchange defines the ownership relationship.

In a traditional brokerage, the assets are held for you. In crypto exchange custody, the relationship can be more ambiguous. Some terms essentially state that once you deposit crypto, the exchange holds the asset and owes you a debt equal to that amount. This distinction is crucial during bankruptcy proceedings, where simple creditors (those owed a debt) are paid back only after secured creditors, often receiving pennies on the dollar.

Minimizing Exposure: The Concept of "Transit Time"

Given the inherent risks of third-party custody, the most effective security strategy is reducing your time exposure. This means treating the exchange as a temporary waystation, not a permanent savings vault.

Defining Hot Funds vs. Cold Storage Workflow

We define your assets based on their immediate purpose:

- Hot Funds (On the Exchange): The minimum amount of crypto or fiat required for active trading, limit orders, or immediate purchases. These funds are exposed to platform risk but grant necessary liquidity.

- Cold Storage (Self-Custody): All long-term holdings, retirement savings, or assets you do not intend to sell or trade in the near future. These funds are secured offline in a hardware wallet, completely insulating them from exchange hacks or failures.

Establishing a Withdrawal Schedule

A disciplined withdrawal schedule is the cornerstone of risk management for exchange users. You should not wait until a crisis to move your assets.

Strategy: The 80/20 Rule. A common professional strategy is to maintain only the 10-20% of your total crypto portfolio that you actively trade on the exchange. The remaining 80-90% should be moved to a self-custody wallet (ideally cold storage).

- Actionable Tip: Set an alert on your exchange account. If your balance exceeds a predefined threshold (e.g., $5,000 or the equivalent of one month of trading capital), execute an immediate withdrawal to your cold storage wallet. Make this a non-negotiable, routine security practice.

The Role of Exchanges as On-Ramps and Off-Ramps Only

View exchanges as transaction utilities, not banks. Their primary, necessary functions are:

- On-Ramp: Converting fiat currency into crypto.

- Trading Engine: Facilitating fast, liquid swaps between various crypto pairs.

- Off-Ramp: Converting crypto back into fiat when necessary.

Any asset that is not actively needed for these functions should be moved off the exchange as quickly and routinely as possible. This pragmatic approach acknowledges the convenience of exchanges while prioritizing the long-term security offered by self-custody.

Zaključek: Uravnoteženje udobja in nadzora

Uporaba centralizirane borze je potreben korak za navigacijo po sodobni kripto ekonomiji, vendar zahteva sprejetje določene stopnje hrambnega tveganja. Prava varnost ni dosežena z izogibanjem borzam v celoti, ampak z minimiziranjem vaše ranljivosti med njihovo uporabo.

Z uvedbo močnih kontrol na strani uporabnika (2FA, belolistiranje), strogo skrbnostjo institucionalne varnosti (dokaz rezerv, politike hladnega shranjevanja) in, kar je najpomembneje, upravljanjem izpostavljenosti sredstvom prek dovršenega urnika dvigov, spremenite tvegano ponudbo v obvladljiv proces.

Na koncu bi moral biti vaš cilj uporaba udobja borze za pridobivanje sredstev, vendar izraba samohranbe za ohranjanje absolutnega nadzora nad svojim bogastvom. Najboljša obramba proti centraliziranemu tveganju je dosledna, načrtovana decentralizacija vaših sredstev.