Cryptocurrencies have evolved significantly from their origins as experimental digital assets. While many market participants view digital currencies primarily as investment vehicles for long-term holding, the utility of these assets as a medium of exchange continues to expand. The ability to transact peer-to-peer without centralized intermediaries was the founding promise of blockchain technology. Today, that promise is realized through a growing ecosystem of merchants, integrated payment solutions, and sophisticated wallet technologies that facilitate daily commerce.

The journey of commercial crypto adoption is often traced back to May 22, 2010. On this date, an early enthusiast successfully traded 10,000 bitcoins for two pizzas. This event, now celebrated annually as Bitcoin Pizza Day, marked the first documented exchange of cryptocurrency for tangible goods. It established a precedent that digital assets could hold real-world purchasing power. Since that moment, the infrastructure supporting these transactions has matured from forum-based bartering into a streamlined global economy.

Modern spending involves more than just direct transfers between individuals. It encompasses a wide array of payment rails, ranging from direct merchant acceptance to debit cards that convert crypto to fiat currency at the point of sale. Major online retailers, travel booking platforms, and digital service providers now integrate these payment methods. This shift allows users to utilize their digital wealth for everything from booking international flights to purchasing video games or household items.

The Mechanics of Digital Transactions

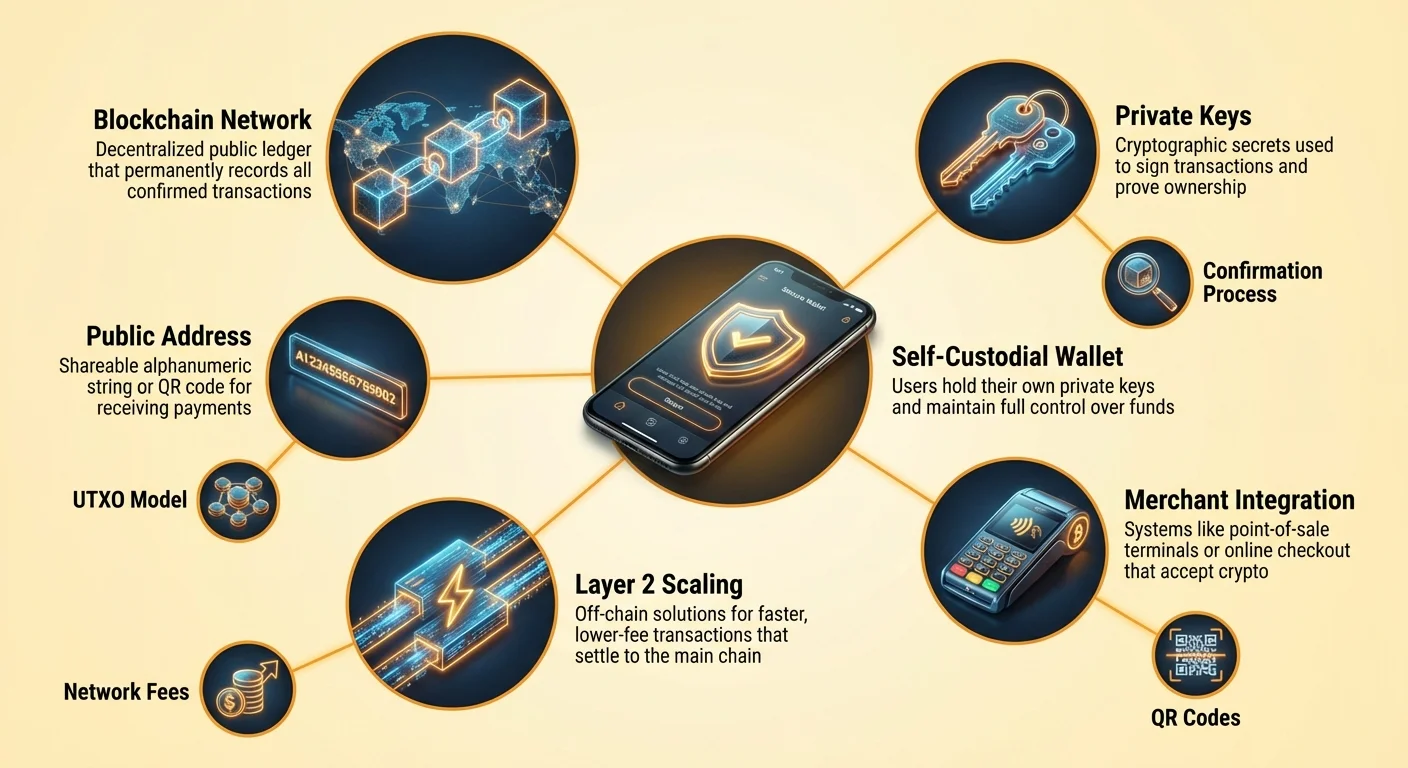

Understanding how to spend cryptocurrency requires a grasp of the underlying transaction mechanisms. Unlike a credit card swipe, which authorizes a pull of funds from a bank, a crypto transaction is a push of digital value. The user actively sends the assets to the merchant. This process begins with the recipient's address. A Bitcoin address functions similarly to a bank account number or an email address for money. It is a unique string of alphanumeric characters that identifies the destination for the funds.

Address Formats and QR Codes

In a retail or online shopping environment, manually typing a long string of random characters is impractical and prone to error. To solve this, the industry relies heavily on Quick Response (QR) codes. These two-dimensional barcodes encode the destination address and often the specific amount required for the purchase. When a user scans a merchant's QR code with their mobile wallet app, the fields for the destination and amount are automatically populated. This reduces the friction of the transaction to a matter of seconds, comparable to tapping a contactless card.

Address formats have also evolved to improve efficiency and reduce fees. Legacy addresses, which start with the number "1," are being supplanted by newer formats like SegWit (starting with "3" or "bc1") and Taproot (starting with "bc1p"). These modern formats are optimized to take up less space on the blockchain data structure. This optimization is crucial for daily spending because smaller transaction sizes often correlate with lower network fees. Using the most current address format supported by a wallet can result in significant cost savings over time.

The Role of Public and Private Keys

At the core of every spend transaction is the relationship between public and private keys. The public key is used to derive the address that you share with merchants to receive goods or refunds. It is safe to disclose this information. The private key, however, functions as the digital signature that authorizes the movement of funds. When a user taps "send" in their wallet, the software uses the private key to mathematically sign the transaction.

This signature proves ownership of the funds without revealing the private key itself. It is the cryptographic equivalent of signing a check, but with mathematical certainty that cannot be forged. For the spender, this means that security is paramount. If the private key is lost, the funds are inaccessible. If it is stolen, the thief has total control. Modern wallets manage these keys automatically, often encrypting them on the device and allowing users to back them up via a recovery phrase or cloud service.

Wallet Selection for Active Spenders

Choosing the right interface is critical for anyone intending to use cryptocurrency for daily purchases. A wallet is not a storage container for coins but rather a keychain management tool. It stores the credentials needed to access funds that live on the blockchain. For frequent spending, users typically prioritize convenience and speed, which leads to different choices compared to long-term investors who prioritize cold storage.

Software vs. Hardware Wallets

Software wallets, often called "hot wallets," exist as applications on mobile devices or desktops. These are the primary tools for daily spending because they are always connected to the internet and ready to broadcast transactions. A mobile app allows a user to carry their balance in their pocket, making it easy to scan QR codes at a coffee shop or checkout counter. They strike a balance between security and utility, offering features like biometric login to prevent unauthorized access if the phone is unlocked.

Hardware wallets, or "cold wallets," are physical devices that keep private keys offline. While they offer the highest level of security against online threats, they are less convenient for buying a cup of coffee. To spend from a hardware wallet, the user must connect the device to a computer or phone and physically approve the transaction. Consequently, many users adopt a tiered approach: keeping large savings in a hardware wallet and transferring smaller "walking around money" to a mobile software wallet for daily use.

Custodial vs. Self-Custodial Solutions

The distinction between custodial and self-custodial wallets is fundamental to the ethos of spending crypto. A self-custodial wallet places the user in full control. The private keys are generated and stored on the user's device. No third party can freeze the account, decline a transaction, or impose limits on spending. This aligns with the concept of digital cash. The user is the sole custodian and bears full responsibility for backup and security.

Custodial wallets are provided by centralized exchanges or third-party services. In this model, the service provider holds the keys and the user logs in with a username and password. This experience mimics traditional banking. While it may offer easier account recovery if a password is lost, it introduces counterparty risk. The provider could halt withdrawals or block payments. For daily spending, self-custodial wallets are often preferred to ensure that funds are available 24/7 without permission from a central authority, reflecting the Spectrum of Custody Risks.

| Wallet Type | Control Level | Best Use Case | Risk Factor |

|---|---|---|---|

| Self-Custodial App | Full User Control | Daily spending & active use | User error (lost keys) |

| Hardware Wallet | Full User Control | Long-term savings & security | Physical loss of device |

| Custodial Account | Third-Party Control | Trading & fiat on/off ramps | Platform freeze or hack |

Understanding Transaction Costs

Every transaction on a public blockchain like Bitcoin incurs a network fee. Unlike credit card networks where fees are charged to the merchant, crypto network fees are paid by the sender. These fees are not determined by the dollar value of the transaction but by the data size of the transaction in bytes. This distinction is vital for anyone spending crypto regularly. Sending $10 worth of bitcoin can cost the same in fees as sending $1 million if the data size is identical.

The UTXO Model Explained

To understand data size, one must understand the Unspent Transaction Output (UTXO) model. Bitcoin functions similarly to physical cash in this regard. If a user has received three separate payments of 0.5 BTC, 0.2 BTC, and 0.3 BTC, they hold three distinct "digital coins" or UTXOs. If they wish to buy an item costing 0.9 BTC, the wallet must bundle these three inputs together to form the payment, illustrating the UTXO Model and Transaction Lifecycle.

Bundling multiple inputs increases the data size of the transaction, which in turn increases the fee. Conversely, if a user holds a single UTXO worth 1.0 BTC, spending 0.9 BTC requires only one input, resulting in a smaller transaction size and lower fee. Active spenders should be aware that receiving many small micro-transactions (like mining payouts or faucet rewards) can lead to higher fees later when they attempt to spend those accumulated funds. This is often referred to as the "dust" problem.

Customizing Fees for Urgency

Network fees fluctuate based on congestion. When many people are trying to transact simultaneously, block space becomes premium real estate. Users bid for this space via the attached fee. Most self-custodial wallets allow users to customize this fee based on urgency. If a purchase needs to be confirmed immediately, the user can select a "Fast" or "Priority" fee rate. This attaches a higher incentive for miners to include the transaction in the next block.

For less urgent transfers, such as moving funds between personal wallets or paying a merchant who accepts unconfirmed transactions, users can select an "Eco" or "Slow" setting. This creates a significant cost-saving opportunity. Paying a high fee is unnecessary if the recipient does not require immediate confirmation. Advanced users can even set custom fee rates measured in satoshis per byte, ensuring they never overpay for blockchain space.

Integrated Merchant Solutions

The landscape of places to spend cryptocurrency has grown dramatically. While direct acceptance is the gold standard, bridge solutions have filled the gaps, allowing crypto holders to shop almost anywhere. Direct acceptance occurs when a merchant integrates a crypto payment processor or manages their own wallet infrastructure. This is common in tech-centric sectors but is expanding into travel, luxury goods, and general retail.

Direct Crypto Acceptance

Prominent online retailers have integrated crypto payments directly into their checkout flows. Major electronics stores and general marketplaces allow users to select cryptocurrency as a payment method alongside credit cards. In the travel industry, specialized booking platforms act as crypto-native agencies. These services allow travelers to book flights, hotels, and accommodations using dozens of different digital assets.

The advantage of using these direct channels is often the availability of loyalty programs. Some crypto-travel sites offer rewards back in cryptocurrency, creating a circular economy where spending earns more crypto. Furthermore, paying directly often avoids the foreign exchange fees associated with using credit cards internationally. The transaction is borderless, settling between the user and the merchant without currency conversion intermediaries taking a cut.

The Gift Card Bridge

For retailers that do not yet directly accept digital assets, gift cards serve as an effective bridge. Integrated wallet features and standalone marketplaces allow users to purchase gift cards for thousands of major brands using cryptocurrency. This effectively opens up the entire retail ecosystem to crypto spending. A user can convert bitcoin into a digital gift card for a grocery store, clothing retailer, or restaurant chain instantly, often using this technique for Gift Card Arbitrage.

This method is particularly useful for daily necessities. While a local supermarket may not have a Bitcoin point-of-sale terminal, they almost certainly accept their own gift cards. The process within modern wallets is seamless: the user selects the brand and amount, pays in crypto, and receives a barcode on their screen that can be scanned at the physical register. This workaround enables a "bankless" lifestyle where crypto funds cover ordinary living expenses.

Denominations and Value Perception

As the value of a single unit of cryptocurrency like Bitcoin has risen to tens of thousands of dollars, the practicality of denominating daily goods in whole coins has diminished. It is cognitively difficult for consumers to evaluate the price of a coffee at 0.00015 BTC. This issue is known as unit bias. Humans naturally prefer whole numbers and can struggle with high-precision decimals.

Thinking in Satoshis

To address this, the ecosystem is increasingly adopting the "satoshi" or "sat" as a standard unit for commerce. One bitcoin is divisible into 100 million satoshis. This divisibility allows for granular pricing without handling unwieldy decimals. Instead of pricing an item at 0.00005000 BTC, it can simply be priced at 5,000 sats. This shift helps align crypto pricing more closely with traditional fiat math, making it easier for spenders to assess value at a glance.

Wallets are adapting to this shift by offering display settings that toggle between BTC and sats. For daily spending, viewing balances in sats helps users feel they are transacting with manageable units rather than microscopic fractions of a high-value asset. This psychological shift is crucial for the transition of crypto from a store of value to a medium of exchange.

Shared Wallets for Household Spending

For families or organizations managing a budget in cryptocurrency, shared wallets offer a robust solution. Also known as multisig (multi-signature) wallets, these require approval from multiple devices to authorize a transaction. This digital structure mirrors a joint bank account but with programmable rules that enhance security and oversight.

In a household setting, a shared wallet might be configured as a "2-of-3" scheme. The three participants could be two partners and a secure backup device. To spend funds, two of the three keys must sign the transaction. This setup allows either partner to initiate a purchase, but it requires the second partner (or the backup) to approve it if the rule is strict, or it can be set up to require consensus for large purchases.

This mechanism protects against the "single point of failure" problem. If one person loses their phone or private key, the funds are not lost because the remaining participants can still move the assets. It also prevents impulsive spending or theft, as a thief would need to compromise multiple devices and security codes simultaneously to drain the wallet.

Security and Privacy in Transactions

Spending cryptocurrency leaves a permanent record on the public blockchain. Unlike a bank statement which is private to the account holder, blockchain transactions are visible to anyone with an internet connection. This transparency is a feature of the technology, ensuring trust and verifiability, but it imposes a responsibility on the user to manage their privacy.

Address Management

A best practice for privacy is to avoid address reuse. If a user receives all their income and makes all their purchases from a single address, it becomes trivial for an observer to map their entire financial life. Modern HD (Hierarchical Deterministic) wallets handle this automatically by generating a fresh address for every new transaction. When receiving change from a purchase, the wallet sends it to a newly created change address rather than the original sending address.

This creates a "moving target" that obfuscates the user's total holdings. While the transactions are still public, linking them all to a single identity becomes significantly more difficult. Users should verify that their wallet software supports this feature and avoids reusing old addresses for incoming payments.

Avoiding Payment Fraud

The irreversible nature of crypto transactions means there is no chargeback mechanism. Once funds are sent, they cannot be recalled. This makes vigilance against fraud essential. Phishing scams often attempt to trick users into sending funds to the wrong address or revealing their private keys. Attackers may impersonate merchant support teams or create fake websites that look identical to legitimate retailers.

When spending, users should always double-check the URL of the payment gateway. Bookmarking trusted merchants and avoiding links in unsolicited emails are critical defense habits. Additionally, users must be wary of "double your money" offers or merchants demanding payment via direct message on social media. Legitimate commerce happens through secure checkout processors, not via anonymous chat requests.

The Role of Layer 2 Scaling

While the base layer of blockchains like Bitcoin provides unmatched security, it can be slow and expensive for small, frequent purchases. This is where Layer 2 solutions, such as the Lightning Network, become relevant for the spender. These secondary protocols sit on top of the main blockchain and allow for instant, near-zero-fee transactions, providing a Practical Lightning Network implementation.

For a user buying a digital download or a coffee, waiting 10 minutes for a block confirmation is impractical. Layer 2 networks solve this by creating payment channels between users. Transactions occur off-chain and are only settled to the main blockchain when necessary. This enables high-volume, low-value transactions that were previously economically unviable.

Wallets that support Lightning or similar scaling technologies are essential for anyone attempting to use crypto as a true daily currency. They provide the speed of a credit card swipe with the settlement assurance of a bearer asset. As merchant adoption of these Layer 2 nodes increases, the friction of paying with crypto continues to decrease, making it competitive with traditional fiat payment rails.

Conclusion

The ecosystem for spending cryptocurrency has matured into a diverse landscape of wallets, merchant solutions, and scaling technologies. Moving beyond simple investment, digital assets now offer a viable alternative for daily commerce, empowered by user-friendly mobile applications and extensive integration with global retailers. Whether through direct wallet transfers, gift card bridges, or Layer 2 protocols, the mechanisms for value transfer are more accessible than ever.

Success in this economy requires a shift in mindset—from passive holding to active management of keys, fees, and privacy. By understanding the technical nuances of UTXOs, selecting the appropriate self-custodial tools, and practicing rigorous security hygiene, individuals can reclaim control over their financial interactions. The infrastructure is in place; the next step is for users to confidently utilize these tools to transact freely using an optimal sending strategy.

Spending crypto is no longer just a novelty but a practical reality, provided users master the tools of self-custody and secure transaction management.