The shift from traditional finance to cryptocurrency introduces a fundamental change in how individuals perceive and manage assets. In the legacy banking system, money is almost always held by a third party. You do not physically hold the digital dollars in your bank account; the bank holds them and grants you permission to access them. Cryptocurrency, particularly Bitcoin, offers an alternative where the user can hold digital value directly, without any intermediary. This capability creates a spectrum of custody options, ranging from fully trusted third-party solutions to complete self-sovereignty.

Understanding where you fall on this spectrum is the first step in securing your digital wealth. The choice between custodial exchanges and self-custodial wallets dictates not only how you access your funds but also the specific risks you face. Newcomers often default to familiar structures that mimic banks, while seasoned users tend to migrate toward solutions that offer mathematical proof of ownership. This article explores the technical and practical differences between these storage methods to help you make an informed decision about your portfolio's security.

The Mechanics of Digital Ownership

To understand custody, one must first understand what a cryptocurrency wallet actually does. A common misconception is that a wallet stores tokens or coins inside the software or device, similar to how a physical leather wallet holds cash. This is not the case. A wallet does not store digital assets; it stores the cryptographic keys that allow you to move assets on the blockchain. The coins themselves always live on the public ledger (the blockchain), not on your device.

A wallet manages two distinct pieces of information: the public key and the private key. The public key is used to derive your receiving address. You can think of this like an email address or a bank account number. It is safe to share this string of characters with anyone who needs to send you funds. It serves as a destination on the network where assets can be directed.

The Role of Private Keys

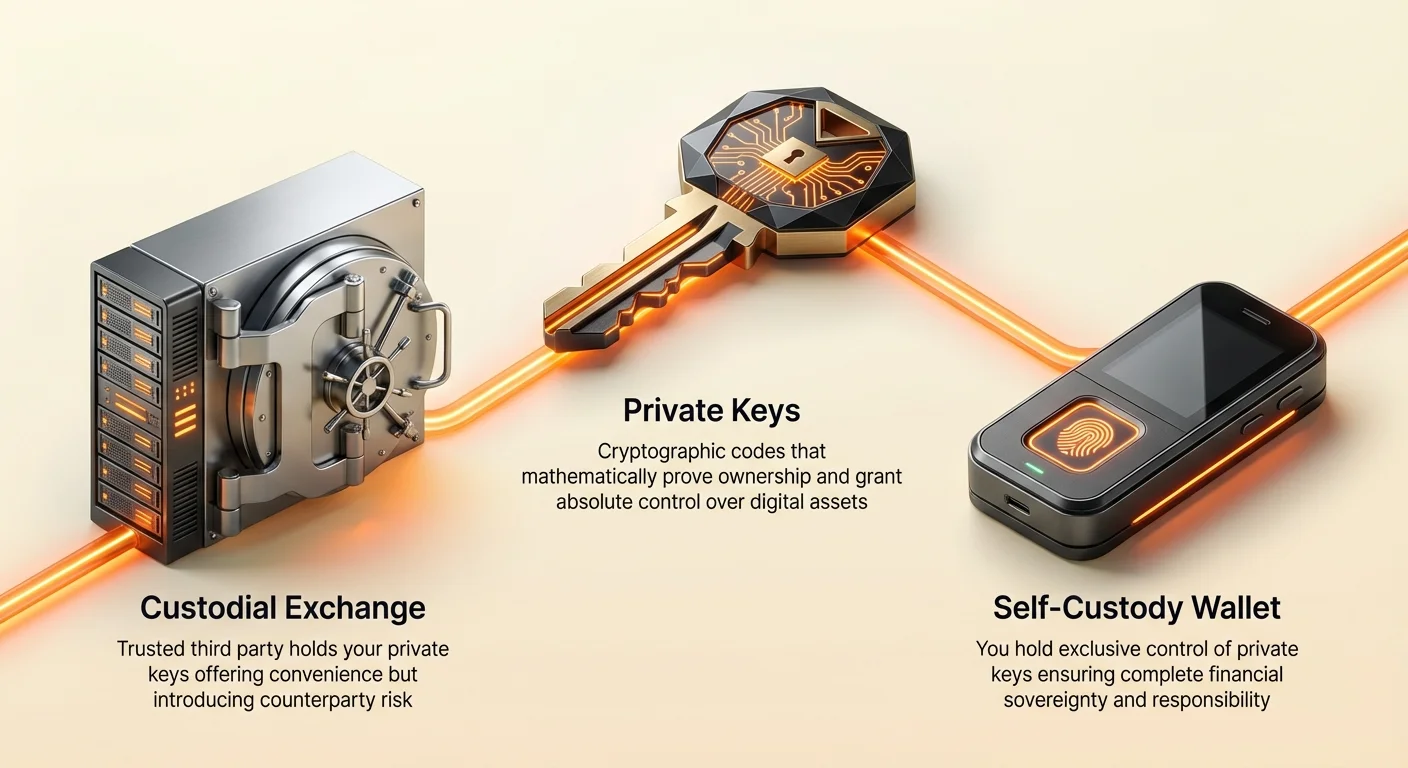

The private key acts as the password or digital signature for that specific address. It is a 256-bit secret number that mathematically proves you have the right to spend the funds located at the corresponding public address. Whoever possesses the private key has absolute control over the assets. If a thief gains access to your private key, they can transfer your funds to their own wallet, and because blockchain transactions are irreversible, there is no customer service department to reverse the theft.

The Recovery Phrase

Because raw private keys are long, complex strings of hexadecimal characters, they are difficult for humans to handle without error. Modern wallet standards use a recovery phrase, also known as a seed phrase. This is a list of 12 to 24 random words generated by the wallet software. These words can be used to mathematically reconstruct the private keys. This human-readable backup method ensures that even if you lose your phone or break your hardware device, you can restore access to your funds on a new device as long as you have those words.

The Custodial Model: Trusting Third Parties

When users first enter the cryptocurrency space, they often start with a centralized exchange (CEX). These platforms function similarly to traditional stock brokerages. You create an account, verify your identity, and transfer fiat currency to buy crypto. In this scenario, the exchange creates a wallet for you, but they retain control of the private keys. You are given a login and password to access the platform, but you do not have direct access to the blockchain.

The Bank Analogy

Using a custodial wallet is comparable to keeping money in a bank. The institution holds the assets on your behalf. When you log in to your account, the balance you see is effectively an IOU. The exchange promises to give you that amount of cryptocurrency when you ask for it. For many, this is convenient because it places the burden of security on the company. If you forget your password, the exchange can help you reset it, just like a bank would.

Regulatory Friction

However, this convenience comes with significant trade-offs. Because centralized exchanges are regulated businesses, they must comply with Know Your Customer (KYC) and Anti-Money Laundering (AML) laws. This means you must provide government identification, proof of address, and other personal data to use their services. This links your real-world identity directly to your crypto holdings, removing the privacy that many users seek in digital assets.

Counterparty Risk

The most critical risk in the custodial model is counterparty risk. If the exchange is hacked, mismanages funds, or goes bankrupt, you may lose access to your assets permanently. History is replete with examples of exchanges failing and users losing everything. Furthermore, because the exchange controls the keys, they can freeze your account at any time. They may delay withdrawals for days or deny them entirely based on internal policies or government pressure. In a custodial setup, you must ask for permission to use your own money.

| Feature | Custodial Wallet (Exchange) | Self-Custodial Wallet |

|---|---|---|

| Control of Keys | Exchange holds keys | User holds keys |

| Permission | Must request withdrawal | Permissionless access |

| Privacy | Requires KYC/ID | No ID required |

| Recovery | Password reset available | User handles backup |

| Risk Type | Exchange failure/freeze | User error/key loss |

The Self-Custodial Standard

Self-custody, often referred to as non-custodial storage, aligns with the original ethos of cryptocurrency: "Not your keys, not your coins." In a self-custodial wallet, the software generates the private keys on your device, and they never leave that environment. The wallet provider does not have access to your keys, your funds, or your transaction history. You are the sole custodian of your assets.

Permissionless Access

The primary advantage of self-custody is sovereignty. You never have to ask for permission to send a transaction. The software connects directly to the blockchain network to broadcast your transfers. There are no withdrawal limits, no waiting periods, and no account freezes. You can send funds to anyone, anywhere in the world, at any time of day. This is essential for users who live in jurisdictions with unstable banking systems or restrictive capital controls.

Direct Blockchain Interaction

Self-custodial wallets also open the door to the broader ecosystem of decentralized finance (DeFi). Because you hold the keys, you can interact directly with smart contracts. You can trade on decentralized exchanges (DEXs), earn yield through staking, or use your assets as collateral for loans without a middleman. Custodial exchange accounts generally limit you to buying, selling, and holding within their closed ecosystem.

However, this power comes with "great responsibility." If you lose your recovery phrase and your device breaks, no one can help you recover your funds. The wallet provider cannot reset your access because they never had it in the first place. Therefore, proper backup management is the single most important skill for self-custody users.

Navigating Wallet Types

Within the realm of self-custody, there are different types of wallets designed for various security needs. The two main categories are software wallets (often called "hot" wallets) and hardware wallets (often called "cold" wallets).

Software Wallets

Software wallets are applications that run on general-purpose devices like smartphones, desktops, or web browsers. They are excellent for everyday spending and frequent interactions because they are always connected to the internet. Users can send and receive funds quickly using QR codes or copy-paste functionality. Modern software wallets often include biometric security, allowing you to unlock the app with a fingerprint or face scan.

While convenient, software wallets are theoretically more vulnerable to malware or viruses because they exist on internet-connected devices. If your computer is infected with a virus that records keystrokes, a hacker could potentially steal your recovery phrase when you type it in. Therefore, software wallets are best suited for smaller amounts of cryptocurrency that you intend to access regularly, rather than life savings.

Hardware Wallets

Hardware wallets are physical devices built specifically to secure private keys. They look similar to USB drives. The critical distinction is that a hardware wallet keeps the private keys offline at all times. When you want to send a transaction, you connect the device to a computer or phone. The transaction data is sent to the hardware wallet, signed internally by the private key, and then the signed transaction is sent back to the computer to be broadcast to the network.

Because the private key never leaves the physical device, it is immune to computer viruses and online hackers. Even if you plug a hardware wallet into an infected computer, the keys remain safe. This makes hardware wallets the gold standard for long-term storage of significant value. The trade-off is that they are less convenient for quick transactions and require an upfront purchase cost.

Paper Wallets

A paper wallet is a low-tech form of cold storage. It involves generating a public and private key pair on a computer (preferably offline) and printing them out on a piece of paper. To spend the funds, you must import the private key into a software wallet. While secure from hackers, paper wallets are fragile. Paper can degrade, burn, or be lost. Additionally, printing keys requires trust in the printer's memory and the computer used to generate them. They are largely considered obsolete compared to modern hardware wallets but remain a valid option for specific use cases like gifting.

Transaction Economics and Network Data

Regardless of which wallet type you choose, sending cryptocurrency involves interacting with the network and paying fees. These are not fees paid to the wallet provider but rather to the miners or validators who secure the network.

Understanding Fees

Network fees act as an incentive for miners to include your transaction in the next block. They also serve as an anti-spam mechanism to prevent the network from being clogged with useless data. During periods of high congestion, fees can rise significantly. Users competing to get their transactions confirmed quickly will offer higher fees.

Most quality self-custodial wallets allow users to customize these fees. You can choose a "fast" fee to get confirmed in the next block (usually ~10 minutes for Bitcoin) or a "slow" fee if you are not in a rush. Setting a fee too low does not mean you lose your funds; it simply means the transaction may sit in the "mempool" (the waiting area) for hours or days until network traffic drops. If it is never picked up, the funds effectively remain in your wallet.

The UTXO Model

Bitcoin transactions use a model called Unspent Transaction Output (UTXO). This is similar to paying with physical cash. If you have a $10 bill and buy a $3 item, you don't tear a piece off the bill. You hand over the $10 and receive $7 in change.

In Bitcoin, your "balance" is actually a collection of unspent outputs from previous transactions. If you have received five different payments of 0.2 BTC each, your wallet shows a balance of 1.0 BTC. If you try to send 1.0 BTC, your transaction data must include all five of those inputs. This increases the size of the transaction data (measured in bytes).

Since fees are calculated in satoshis per byte, a transaction with many inputs (like a piggy bank full of pennies) will cost more to send than a transaction with one single input (like a $100 bill), even if the total value sent is the same. Custodial exchanges handle this complexity behind the scenes, often charging a flat withdrawal fee that is higher than the actual network cost to ensure they cover their expenses.

Security Vectors and Fraud Prevention

Taking control of your assets means you must also be your own security team. The irreversibility of blockchain transactions attracts scammers who rely on social engineering rather than breaking encryption.

Phishing Tactics

Phishing is the most common threat. Attackers create fake websites that look identical to legitimate exchanges or wallet portals. If you enter your login credentials or, worse, your recovery phrase into these sites, the attackers gain full access. Always check the URL carefully and ensure the site uses HTTPS. Bookmark legitimate sites rather than relying on search engine results, which can sometimes display malicious ads at the top of the page.

Social Engineering

Scammers often pose as customer support agents on social media platforms like Twitter, Telegram, or Discord. They may claim your account is frozen or that you need to "validate" your wallet to receive a giveaway. A legitimate wallet provider or exchange will never ask for your private key or recovery phrase. If anyone asks for these details, it is a scam.

Another common fraud involves "doubling" schemes, where scammers promise to send back double the amount of crypto you send them. These are always fraudulent. Valid transactions do not require you to send funds first to receive funds later.

Cloud Backups vs. Manual Backups

To mitigate the risk of losing recovery phrases, some modern wallets offer encrypted cloud backups. This feature allows you to store an encrypted version of your recovery phrase in your Apple iCloud or Google Drive, protected by a custom password. This provides a safety net if you lose your physical paper backup. However, it reintroduces a level of third-party reliance. If you choose this route, ensure your cloud account is secured with strong passwords and two-factor authentication to prevent unauthorized access to the backup file.

Advanced Security: Multisignature Wallets

For individuals or organizations managing large sums, a standard single-signature wallet may not offer enough security. This is where multisignature (multisig) wallets come into play. A standard wallet has one private key that can sign and authorize a transaction. A multisig wallet is like a vault that requires multiple keys to open.

Shared Control

In a multisig setup, you designate a number of participants and a threshold for approval. For example, a "2-of-3" wallet has three associated private keys, but any two of them are required to send funds. This eliminates the single point of failure. If one key is lost or stolen, the funds are still safe because the thief cannot move them without a second key. Conversely, if you lose one key, you can still access your funds using the remaining two.

Redundancy and Use Cases

This structure is ideal for shared family funds, where spouses might want joint control, or for corporate treasuries where no single employee should have unilateral power to move company assets. It protects against both external theft and internal errors or accidents. While more complex to set up than a standard wallet, multisig provides the highest level of assurance for asset protection on the Bitcoin network.

Privacy Considerations

While Bitcoin addresses do not contain your name, the ledger is public. Anyone can view the balance and transaction history of a specific address using a block explorer. If you share your main address publicly or use it for every transaction, it becomes easier for observers to cluster your activity and estimate your net worth.

To maintain privacy, it is recommended to use a new address for every transaction. Modern HD (Hierarchical Deterministic) wallets handle this automatically. They generate a fresh address for every receive request, yet all those addresses are still controlled by your single recovery phrase. This prevents outside observers from easily seeing your entire financial history just by knowing one of your addresses.

Conclusion

Choosing between custodial and self-custodial wallets requires balancing convenience against control. Custodial exchanges offer a familiar, bank-like experience that is easy for beginners but exposes users to counterparty risks, regulatory freezes, and potential loss of funds through exchange mismanagement. It involves trusting a third party with the keys to your wealth.

Self-custody places the power directly in your hands. It offers immunity from bank runs and censorship, granting you absolute control over your digital assets. However, it demands a higher level of personal responsibility regarding backup management and security hygiene. For many, a hybrid approach works best: using exchanges for trading and buying, while moving long-term holdings to a secure, self-custodial hardware or software wallet.

True ownership in crypto means holding your own keys, ensuring that your assets remain yours regardless of what happens to any exchange or institution.