Managing digital wealth requires a fundamental shift in how we think about ownership and access. In the traditional financial world, losing a bank card or forgetting a password is a minor inconvenience resolved by a phone call and identity verification. The institution holding your funds acts as a safety net, retaining control and the ability to restore access upon request.

In the realm of cryptocurrencies and digital assets, this dynamic is often inverted. The defining characteristic of decentralized assets is the removal of intermediaries. While this grants unparalleled financial sovereignty and censorship resistance, it imposes a strict responsibility on the owner, fostering the self-custody mindset. If you are the sole custodian of your assets, there is no customer support line to call if you lose your access credentials.

This reality creates a significant challenge for inheritance and contingency planning. When an investor passes away or becomes incapacitated, their digital wealth does not automatically transfer to their next of kin. Without a specific plan that bridges the gap between physical estate planning and digital cryptography, millions of dollars in assets can become permanently inaccessible.

The "black hole" of lost cryptocurrency is a well-documented phenomenon, often resulting from a lack of knowledge rather than malicious theft. To prevent your digital legacy from becoming a statistic, you must understand the mechanics of the technology you use. Building a robust contingency plan starts with mastering the tools of digital asset security.

The Foundation of Digital Ownership

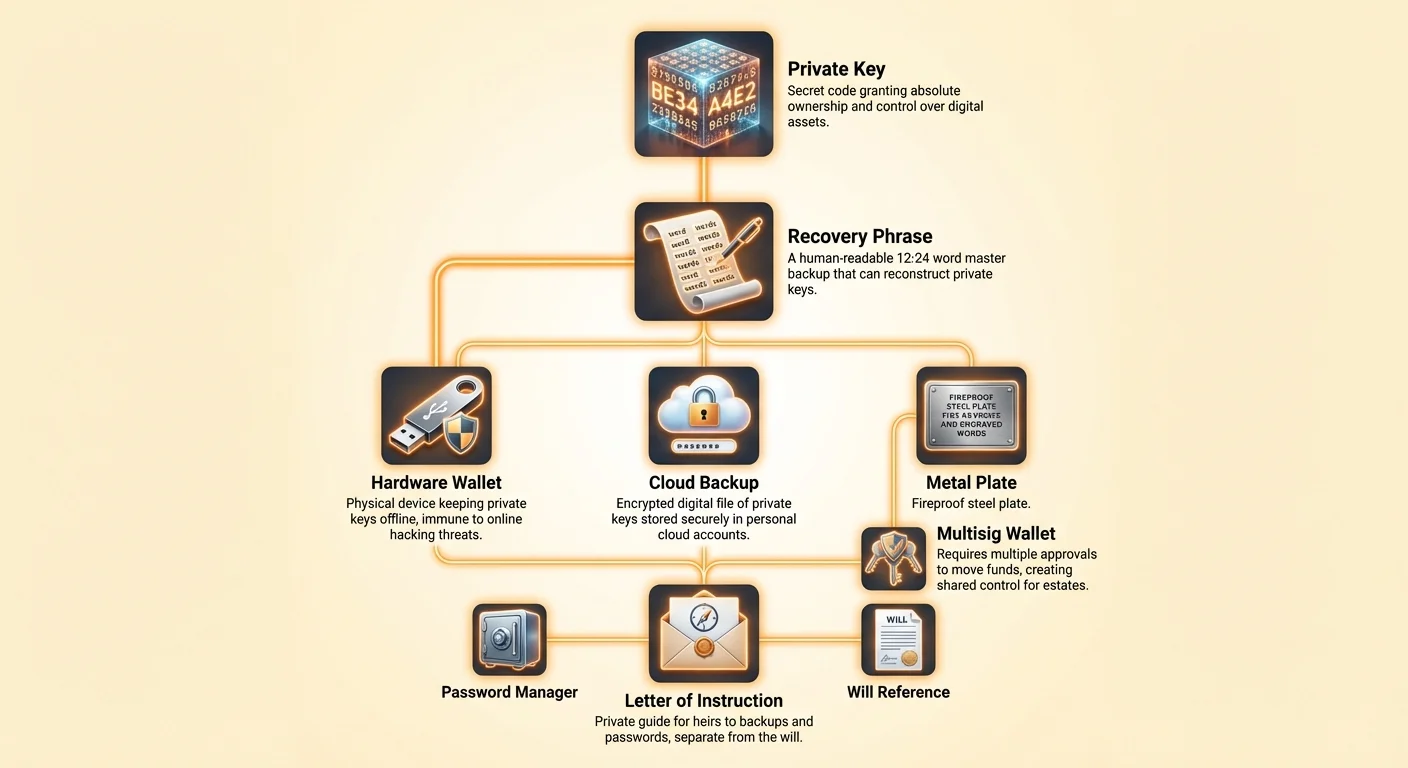

To create a plan for the future, one must first understand what they actually own. When you acquire cryptocurrency, you do not hold digital coins in a file on your computer or smartphone. Instead, you hold a "private key." This key is a secret code that grants ownership and control over a specific address on the blockchain.

The Role of Private Keys

A private key is essentially a long, randomly generated string of alphanumeric characters. It functions similarly to a password for a bank account, but with much higher stakes. In the traditional system, the bank has a copy of your password or a way to reset it. In cryptocurrency, the private key is the only thing that verifies your right to spend the funds.

This key is mathematically linked to a public key, which acts as your receiving address. Think of the public key as a mailbox slot where anyone can deposit mail. The private key is the only physical key that opens the box to retrieve the contents. If that key is lost, the mailbox remains locked forever, and the contents are effectively destroyed.

The Connection to Wallets

A crypto wallet is the interface that manages these keys for you. It is a common misconception that a wallet stores the actual currency. It does not. A Bitcoin wallet, for example, is a device or software program that stores your private keys and allows you to interact with the blockchain network.

The wallet uses your private key to digitally sign transactions. This signature proves to the network that you own the funds without revealing the private key itself. Because the wallet handles this sensitive operation, the security of the wallet software or device is paramount to the security of the assets.

The Critical Role of the Recovery Phrase

Since raw private keys are long strings of hexadecimal characters, they are difficult for humans to read, write down, or remember without error. To solve this, modern wallets utilize a standard known as a recovery phrase, also called a seed phrase or secret passphrase.

This phrase usually consists of 12 to 24 random words generated by the wallet during the initial setup. These words are a human-readable representation of your private key. If your phone is lost, destroyed, or wiped, entering these words into a new wallet device or application will reconstruct your private keys and restore access to your funds.

For inheritance purposes, the recovery phrase is the "master key" to your digital vault. If your beneficiaries have access to this list of words, they can access your funds from anywhere in the world, regardless of whether they have your original phone or computer. Conversely, if they cannot find this phrase, the assets are likely gone.

However, the power of the recovery phrase introduces severe risks. Anyone who sees these words has full access to your funds. They do not need your phone, your PIN, or your fingerprint. Therefore, the storage of this phrase is the single most critical element of your contingency plan. It must be accessible to your heirs but completely hidden from everyone else.

Custodial Versus Self-Custodial Implications

The strategy for passing on digital assets depends entirely on where those assets are held. There are two primary models for holding cryptocurrency: custodial and self-custodial. Each requires a completely different approach to estate planning.

The Custodial Model

A custodial wallet is provided by a centralized exchange or brokerage. In this scenario, the company holds the private keys on your behalf. You access the account through a login and password, much like online banking.

In an inheritance scenario, a custodial account is treated similarly to a traditional bank account. Your executor would likely need to provide a death certificate, a copy of the will, and other legal documents to the exchange to prove their authority. The exchange would then transfer control of the account.

While this process is familiar to estate lawyers, it carries specific risks. You are trusting the exchange to remain solvent and operational. If the platform goes bankrupt or is shut down by regulators, your heirs may inherit nothing but a claim in a lengthy legal proceeding. Furthermore, the exchange has the power to freeze withdrawals or deny access based on internal policies.

The Self-Custodial Model

A self-custodial wallet puts the user in complete control. You possess the private keys, usually stored on your mobile device or a hardware wallet. No third party—including the wallet developer—has access to your funds.

This model aligns with the core philosophy of cryptocurrency: you are your own bank. This means there is no account approval process and no one to ask for permission to move funds. However, it also means there is no one to help your heirs if you fail to leave instructions.

For self-custodial assets, the inheritance plan is purely technical, not legal. Your will can declare who should own the assets, but only the private keys or recovery phrase can actually grant them possession. Without the keys, the legal rights granted by a will are practically useless.

Backup Strategies for Contingency

Creating a reliable backup is the first step in ensuring your assets outlive you. A backup ensures that if your primary device is lost or if you are unable to unlock it, the funds can still be recovered. There are two main approaches to backups: manual and automated cloud storage.

| Feature | Manual Backup | Cloud Backup |

|---|---|---|

| Method | Writing down 12-24 words on paper | Encrypted file stored in Google/Apple drive |

| Security | Physical security required | Protected by a custom password |

| Risk | Physical loss, damage, or theft | Phishing or forgetting the decryption password |

Manual Paper Backups

The traditional method involves physically writing down the recovery phrase on a piece of paper. This is often considered "cold storage" because the paper is offline, removed from internet-connected threats like hackers or malware.

For an inheritance plan, paper backups present logistical challenges. Paper can be destroyed by fire, water, or simple decay. If you hide the paper too well, your heirs may never find it. If you don't hide it well enough, a burglar might find it.

A common best practice is to make copies of the paper backup and store them in separate secure locations. For example, one might be in a home safe, while another is stored in a safety deposit box or at a trusted relative's house. This geographic distribution protects against local disasters like a house fire, supporting effective deep cold storage strategies.

Automated Cloud Backups

Modern wallets, such as the Bitcoin.com Wallet app, have introduced automated cloud backup services to mitigate the risks of physical paper. In this system, the wallet creates a backup file of your private keys, encrypts it with a single custom password of your choosing, and stores it in your personal cloud account (Google Drive or iCloud).

This simplifies the inheritance process significantly. Instead of needing to find a hidden piece of paper, your heirs would need access to your cloud account and the specific password you created for the backup.

This method effectively consolidates the complexity. Rather than managing 12 random words for every different cryptocurrency you own, you manage one strong password that unlocks everything. If you choose this route, your contingency plan must ensure your heirs can access your email account and know the decryption password.

Advanced Security and Shared Access

For those with significant holdings, simple backups may not offer enough security or flexibility. Advanced features like multisignature wallets and hardware devices can provide robust solutions for contingency planning.

Multisig Wallets

A multisignature (multisig) wallet is a powerful tool for creating shared control. Unlike a standard wallet that requires one signature to authorize a transaction, a multisig wallet requires approval from multiple parties.

For example, you could set up a "2-of-3" multisig wallet. This wallet has three participants, and any two of them must agree to move funds. This structure is ideal for family estates. You could hold one key, your spouse could hold one, and a family attorney could hold the third.

In the event of your passing, your spouse and the attorney could combine their keys to access the funds. This prevents any single person from running off with the assets while ensuring that the funds are not lost if one person loses their key. This setup protects against both loss and theft, acting as a digital form of a joint bank account with checks and balances.

Hardware Wallets

Hardware wallets are physical devices designed solely to store private keys offline. They look like USB drives and connect to a computer or phone only when you need to sign a transaction. Because the keys never leave the device, they are immune to computer viruses and online hackers.

Incorporating a hardware wallet into your estate plan adds a physical token that must be transferred. Your plan would need to direct your heirs to the physical location of the device and provide the PIN code required to unlock it. Hardware wallets also generate a recovery phrase, which serves as the ultimate backup if the device itself fails.

Constructing the Access Protocol

The goal of your plan is to create a roadmap that allows your trusted beneficiaries to recover your assets without exposing those assets to theft while you are alive. This requires a careful balance of secrecy and accessibility.

Documentation Without Exposure

You should never list your actual recovery phrase or private keys directly in a will. Wills often become public records upon probate. If your 12-word phrase is written in a public document, anyone who reads it can instantly drain your wallet.

Instead, your will should reference the existence of digital assets and point to a separate, private document or secure location where the access credentials are kept. This private document is your "Letter of Instruction."

The Letter of Instruction

This document serves as a guide for your heirs. It should not just list codes but explain the process. Remember that your heirs may not be familiar with cryptocurrency concepts.

The letter should explain what software to download (e.g., a specific wallet app), where to find the backup (e.g., "in the blue safe" or "on my Google Drive"), and the necessary passwords or PINs. It is helpful to explain the difference between the PIN used to unlock your phone and the password used to decrypt a cloud backup.

Redundancy and Updates

A static plan is a failing plan. You may change wallet software, move funds to a new address, or update your passwords. If your contingency plan lists an old password that you changed years ago, your heirs will hit a dead wall.

Review your digital asset plan annually. Check that your backups are still legible and that your location instructions are current. If you use a cloud backup, verify that the file is still present in your drive and that you remember the decryption password.

Password Management Best Practices

Whether you rely on cloud backups or simply need to secure the digital list of instructions, password management is the glue that holds your security architecture together. A weak password can undermine the most sophisticated crypto security setup.

Avoiding Digital Storage Risks

You should never store your passwords or recovery phrases in plain text on a computer or smartphone. Taking a screenshot of your seed phrase or saving it in a "Notes" app opens you up to hackers. If your device is compromised, automated scripts can scan for these files and steal your funds in seconds.

If you must store information digitally, it must be encrypted. Password manager applications can be useful here, provided the master password for the manager is itself secure and known to your heirs.

The Physical Component

For many, the safest strategy remains low-tech: pen and paper. Writing down your passwords and phrases removes the threat of online attackers. However, this reintroduces physical risks.

To mitigate this, consider using durable materials. Some investors record their seed phrases on metal plates that are fireproof and waterproof. This ensures that even in a catastrophic event like a house fire, the keys to the inheritance survive.

Navigating the Risk of Exchange Insolvency

While self-custody is often recommended for security, many investors still keep funds on centralized exchanges for convenience or trading. If you choose this path, you must be aware of the specific risks regarding inheritance.

If an exchange holds your funds, you are technically an unsecured creditor. In the event of the exchange's bankruptcy, you are at the back of the line. Legal proceedings can take years, and asset recovery is rarely 100%.

Ideally, the bulk of your long-term holdings—the inheritance you plan to leave behind—should be moved to a self-custodial wallet. This removes the counterparty risk. You are no longer relying on a company to exist in 20 or 30 years; you are relying on the mathematics of the blockchain and your own backup protocol.

If you must keep funds on an exchange, ensure your heirs know which exchange you use and have the necessary login details or at least knowledge of the account's existence so they can initiate a formal claim.

The Psychological Barrier

One of the biggest hurdles in creating a digital inheritance plan is the psychological weight of the responsibility. In the self-custodial model, the realization that "only I can access this" is empowering but also terrifying.

It is easy to procrastinate on creating a backup plan because it requires facing one's mortality and dealing with technical complexity. However, ignoring the problem practically guarantees the loss of assets.

Start small. Back up your current wallet today. Write down the recovery phrase and put it in a secure place. Tell one trusted person that you own digital assets and where they can find the instructions if something happens to you. You do not need to give them the keys now, just the map to find them later.

Integrating with Traditional Estate Planning

Digital assets do not exist in a vacuum. They should be integrated into your broader financial estate plan. Inform your attorney or estate planner that you hold digital assets, even if you do not provide them with the access keys.

They can help you draft the appropriate language in your will to transfer legal title. This creates a clear legal basis for your heirs to own the assets, even if the transfer mechanism (the keys) is handled separately.

This is particularly important for significant amounts. If tax authorities or other family members contest the ownership of the crypto, having a clear legal paper trail combined with the technical access keys provides the strongest possible protection for your beneficiaries.

Conclusion

The challenge of inheriting digital assets is not merely a technical problem; it is a problem of continuity in a trustless system. By design, cryptocurrencies resist external control. This feature, which makes them so valuable for security and privacy, makes them incredibly fragile in the context of mortality. Without a conscious effort to create a bridge, the cryptographic walls you build to keep thieves out will eventually keep your family out as well.

Solving the "$1 million problem" requires a multi-faceted approach. It demands a shift to self-custody to ensure true ownership, rigorous backup procedures to protect against data loss, and a clear, documented communication strategy for your heirs. Whether you utilize paper seed phrases, encrypted cloud backups, or multisig wallets, the core principle remains the same: redundancy and clarity. You must create a system that survives your absence.

The tools for secure digital inheritance exist today. Hardware wallets offer physical safety, cloud backups offer convenience, and multisig setups offer democratic control. The responsibility lies with the investor to combine these tools into a coherent plan. By taking action now, you transform your digital assets from a potential loss into a lasting legacy.

If you don't possess the private keys, you don't own the crypto, and neither will your heirs.