Welcome to the foundational comparison that defines the modern financial discussion. When people first encounter Bitcoin, they inevitably ask, "How is this different from the money I already use?" That money is called fiat currency—think U.S. Dollars (USD), Euros (EUR), or Japanese Yen (JPY).

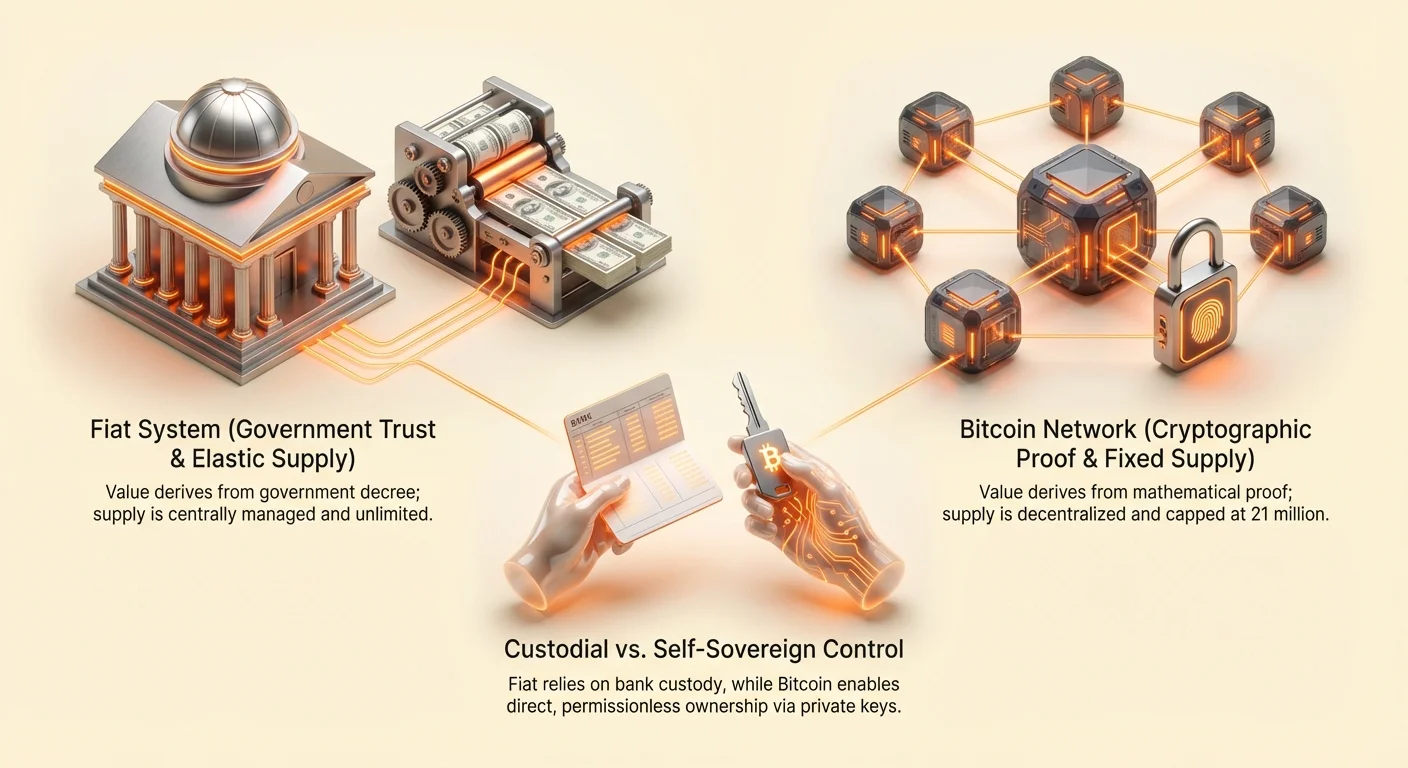

Fiat currency is traditional government-issued money, deriving its value primarily from government decree and public trust in the issuing authority. Bitcoin, conversely, is a purely digital, decentralized currency created by cryptographic proof and governed by immutable rules set in code. They are fundamentally different systems, built on opposing philosophies regarding trust, ownership, and value creation.

This guide provides a detailed, feature-by-feature comparison of these two monetary architectures. Our goal is not to declare a winner, but to equip you with the knowledge necessary to understand the unique properties of each system, satisfying the intent of those researching genuine alternatives to the existing financial landscape.

1. The Foundation of Value: Trust and Centralization

The most significant difference between Bitcoin and fiat currency lies in who controls the system and what guarantees its operation.

Centralization vs. Decentralization

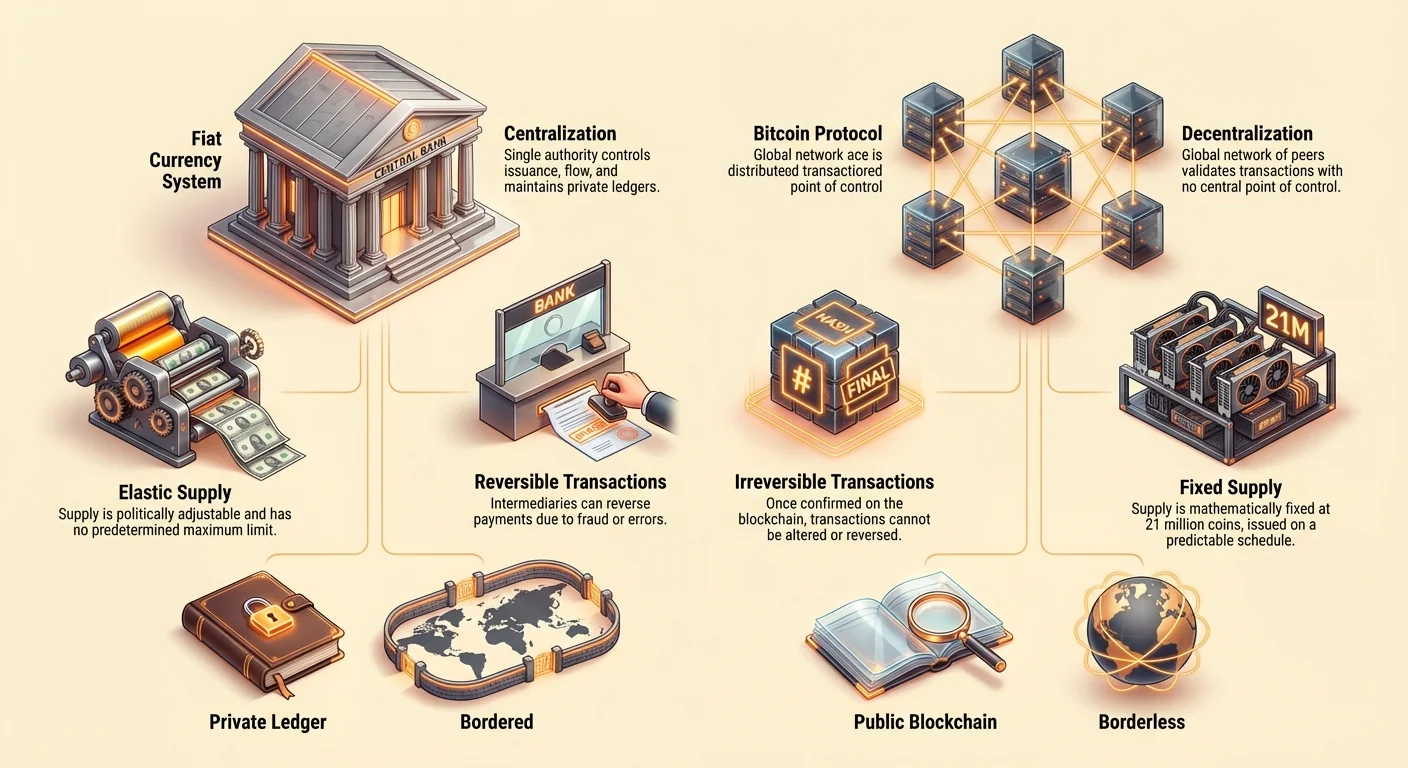

Fiat systems are inherently centralized. A single entity, typically a central bank (like the Federal Reserve in the U.S. or the European Central Bank), governs the issuance, flow, and supply of the currency. Banks act as trusted intermediaries, maintaining private ledgers of all transactions.

| Feature | Fiat Currency (e.g., USD) | Bitcoin (BTC) |

|---|---|---|

| Control | Highly Centralized | Fully Decentralized |

| Issuer | Government / Central Bank | None (Mined by global participants) |

| Ledger | Private (Controlled by banks) | Public (The Blockchain) |

| Operation | Requires trusted intermediaries | Trustless (Relies on cryptographic proof) |

Bitcoin, by contrast, operates on a decentralized network. No single person, company, or government controls the Bitcoin blockchain. Instead, thousands of individual computers (nodes and miners) around the world validate transactions and maintain a shared, public ledger. This distribution of power eliminates the single point of failure and removes the necessity of trusting a middleman.

The Role of Trust

In the fiat system, the entire structure requires trust in authority. You trust the government not to debase the currency excessively, you trust the banks not to lose your funds, and you trust the regulatory system to enforce contracts. This is often called trust-based finance.

Bitcoin was designed to replace this reliance on human authority with verifiable, transparent code. The network operates on a trustless basis. You do not need to trust any third party; instead, you rely on the mathematics and cryptographic security embedded in the protocol. If a transaction follows the established rules, it is validated and recorded, regardless of who is sending or receiving it.

Practical Example: If you send a wire transfer (fiat), the bank verifies the transaction, updates its private ledger, and charges a fee for the service. If you send Bitcoin, the global network of nodes verifies the cryptographic signature, confirms the transaction according to the fixed rules, and records it on the public blockchain for a fee paid to the miners (the network operators).

2. Monetary Policy: Supply and Scarcity

The rules governing the issuance and quantity of money have profound economic consequences, particularly concerning inflation and long-term purchasing power. This is where Bitcoin’s architecture provides its clearest distinction.

Fixed vs. Elastic Supply

Fiat currencies operate under an elastic supply model. Central banks have the authority—and often the mandate—to print or inject new money into the system as they deem necessary to manage economic growth, employment, and interest rates. This expansion of the money supply is often referred to as Quantitative Easing (QE).

The supply of fiat money is therefore political and flexible, changing based on the decisions of a small group of policymakers. There is no predetermined maximum limit, meaning the currency’s scarcity is uncertain.

Bitcoin, however, operates under a fixed and predictable supply rule. The Bitcoin protocol dictates that only 21 million BTC will ever be created.

New bitcoins are released into circulation through a process called mining, following a predictable schedule that halves approximately every four years (the "halving event"). This rule is written into the foundational code and cannot be changed unless a vast majority of the network agrees to modify the protocol—a highly unlikely event given the consensus mechanism. This verifiable scarcity is Bitcoin's most defining economic feature.

Inflation and Purchasing Power

Inflation, the general increase in prices and the corresponding fall in the purchasing value of money, is a direct consequence of expanding the money supply faster than economic output grows. Because fiat supply is elastic, it is susceptible to continuous, systemic inflation. Over time, your fiat savings lose purchasing power.

Since Bitcoin has a fixed cap and a decreasing issuance rate (it is deflationary in its issuance schedule), it is structurally resistant to inflationary supply shocks. It is designed to be a hard asset—analogous to digital gold—that retains its value over long time horizons due to its provable scarcity.

Actionable Insight: Understanding this concept is crucial for long-term planning. Fiat currency is optimized for spending (it encourages velocity because holding it means losing purchasing power), while Bitcoin is optimized for saving (its scarcity encourages holding, acting as a potential store of value).

3. Transaction Mechanics: Speed, Cost, and Finality

Moving value around the globe reveals significant operational differences between traditional banking and the decentralized network.

Settlement Finality

In traditional banking, transactions are often not final immediately, even if the funds appear in your account. Large transfers can take days to clear due to internal bank settlement processes. Moreover, many transactions (like credit card purchases or certain bank wires) are reversible. This is known as "counterparty risk" because there is always a middleman who can intervene or reverse the transaction.

Bitcoin transactions, once confirmed by the network and added to the blockchain (usually taking 10-60 minutes depending on network congestion and required security confirmations), are irreversible and final. There is no authority to call and initiate a chargeback or reversal. This feature is critical for high-value transactions, cross-border commerce, and establishing true ownership without relying on legal frameworks to enforce settlement.

Transparency and Auditability

When you look at your bank statement, you see the transactions you made. The bank, however, maintains the entire ledger privately, only accessible to authorized personnel and government regulators. The process is opaque to the public.

When you look at your bank statement, you see the transactions you made. The bank, however, maintains the entire ledger privately, only accessible to authorized personnel and government regulators. The process is opaque to the public. Bitcoin’s ledger—the blockchain—is completely public and auditable by anyone in the world. Every transaction ever made is recorded permanently. However, unlike a bank statement linked to your legal identity, Bitcoin transactions use cryptographic addresses (long strings of letters and numbers). This provides pseudonymity, meaning the transaction data is public, but the real-world identity of the user behind the address is not explicitly revealed unless linked externally.

This public auditability ensures that the 21 million supply limit is mathematically verifiable by anyone running a Bitcoin node, eliminating the possibility of hidden inflation.

Borderless Payments and Fees

The fiat system relies heavily on correspondent banking networks and messaging systems like SWIFT for cross-border transfers. These systems are slow, often requiring 3–5 business days, and involve multiple intermediaries, each adding fees. This makes moving large or small amounts internationally expensive and time-consuming.

Bitcoin is inherently global and borderless. Sending value from Tokyo to Toronto costs the same (a network transaction fee, regardless of the amount sent) and takes the same time (10-60 minutes for security confirmation) as sending it across the street. The network operates 24 hours a day, 7 days a week, 365 days a year, unaffected by banking holidays or time zones.

Key Takeaway: Bitcoin offers superior censorship resistance and 24/7 global reach because it does not rely on jurisdictional permissions to operate. Fiat systems rely heavily on slow, geographically constrained infrastructure.

4. Accessibility and Control: Ownership and Self-Sovereignty

The concept of self-sovereignty—the ability to control your own funds without permission—is central to the crypto movement and starkly contrasts with the custodial nature of traditional banking.

Self-Custody vs. Custodial Banking

In the traditional fiat system, when you deposit money into a bank account, you are effectively granting the bank custody of your funds. The bank then uses that money for lending and investment, and you become an unsecured creditor. While insured by government programs (like the FDIC in the U.S.), access and control remain conditional. The bank holds the keys to your money.

Bitcoin enables self-custody. When you hold Bitcoin in a non-custodial wallet, you possess the private keys (the cryptographic secret) that prove ownership. This means you, and only you, have access to and control over the funds. The famous crypto adage, "Not your keys, not your coins," highlights this fundamental difference.

| Ownership Aspect | Fiat Currency in a Bank | Bitcoin in Self-Custody |

|---|---|---|

| Control | Conditional (Bank can freeze) | Absolute (Only key holder has access) |

| Access | Limited by bank hours/policies | 24/7/365 |

| Security Risk | Counterparty risk, Policy risk | Key loss risk, Technical failure risk |

Censorship Resistance

Because traditional bank accounts operate within legal jurisdictions and rely on trusted intermediaries, they are susceptible to financial censorship. Governments or institutions can freeze, seize, or block access to funds based on legal orders, political actions, or sanctions.

Bitcoin, due to its decentralized nature and reliance on self-custody, is highly resistant to this type of censorship. Since there is no central authority to issue a freezing order, stopping a transfer or seizing funds requires physically gaining access to the owner's private keys. This makes Bitcoin a crucial tool for those operating in politically unstable regions or those seeking to protect assets from government overreach.

5. Risks and Trade-Offs

While Bitcoin addresses many deficiencies of the fiat system, it introduces new challenges, while fiat has its own specific risks that users often overlook.

Volatility and Adoption Risk (Bitcoin)

The most immediate and apparent risk associated with Bitcoin is its price volatility. Because it is a young asset, still seeking widespread adoption and dealing with intense speculation, its price can fluctuate dramatically, making it a challenging medium of exchange or short-term store of value for the risk-averse.

Furthermore, Bitcoin operates within a still-developing regulatory framework. The risk of adverse regulation or a massive technical failure (though highly improbable given its 15+ years of uptime) are risks unique to a groundbreaking technological system.

Counterparty Risk and Policy Risk (Fiat)

Fiat systems carry risks often hidden by familiarity and government guarantees:

- Inflation Risk: The guaranteed erosion of purchasing power due to continuous money supply expansion.

- Counterparty Risk: The risk that the bank or financial institution holding your money fails (though often mitigated by deposit insurance).

- Policy Risk: The risk that government policy changes—such as imposing capital controls (limits on how much money citizens can move out of the country) or utilizing bail-ins (using depositor funds to recapitalize a failing bank)—affect your savings.

In short, while Bitcoin exposes users to market volatility risk, fiat exposes users to political and institutional risk.

Jargon Buster:

- Hash Rate: The total computing power dedicated to securing the Bitcoin network. It is a measure of the network's security; higher hash rate means greater security.

- Fiat: Latin for "let it be done." Money that has value because a government says it does.

Comparative Summary: Bitcoin vs. Fiat

| Feature | Fiat Currency | Bitcoin |

|---|---|---|

| Supply Policy | Elastic (Infinite) | Fixed (21 Million Cap) |

| Inflation Pressure | High/Systemic | Low/Predictable Deflationary Issuance |

| Governance | Central Banks / Governments | Decentralized Network Consensus |

| Ledger Access | Private / Permissioned | Public / Permissionless |

| Transaction Finality | Reversible, Slow Settlement | Irreversible, Fast Settlement (After Confirmation) |

| Jurisdiction | Confined by Borders | Global / Borderless |

| Censorship Risk | High (Accounts can be frozen) | Low (Only keys needed to transact) |

Conclusion: Evaluating Your Needs

Bitcoin and fiat currency are two radically different approaches to managing value. Fiat excels as a medium of exchange supported by vast, established regulatory systems, offering stability (at the cost of long-term value preservation) and widespread acceptance. It is the necessary currency for daily economic life today.

Bitcoin, however, excels as a censorship-resistant, verifiable digital store of value. It trades the political flexibility and stability of central authority for the mathematical certainty of code and the absolute control of self-custody.

As you continue along your crypto roadmap, the key is to determine which properties matter most for your financial goals. If you prioritize long-term, inflation-resistant savings and self-sovereignty, Bitcoin offers a robust architectural alternative to the trust-based systems that define fiat currency.