The explosion of digital assets has forced professional financial institutions—including crypto hedge funds, venture capital firms, traditional financial advisors, and corporate treasuries—to confront a massive operational challenge: managing compliance at scale. Unlike retail investors who might handle a few hundred transactions annually, institutional investors process tens of thousands, sometimes millions, of trades across dozens of disparate venues, complex DeFi protocols, and bespoke investment structures.

Navigating this complexity requires moving far beyond simple, off-the-shelf tax calculators. Enterprise-grade crypto accounting software is not merely a tool for generating tax returns; it is critical financial infrastructure designed to handle the velocity, volume, and inherent complexity of institutional digital asset management. This software provides the necessary foundation for accurate reporting, rigorous auditability, and adherence to sophisticated global accounting standards (such as GAAP and IFRS).

This guide is designed for financial professionals transitioning into the digital asset space, offering a framework for evaluating and selecting institutional solutions capable of supporting high-volume, multi-asset strategies while minimizing operational risk and ensuring robust regulatory compliance.

The Core Difference: Retail vs. Institutional Reporting

To understand the needs of enterprise software, it is essential to first differentiate between the compliance requirements of a casual individual investor and a professional financial firm managing third-party capital.

Transaction Volume and Complexity

Retail tax software is generally optimized to connect with one or two major centralized exchanges and calculate simple spot trades (buying and selling Bitcoin or Ethereum). However, professional firms often engage in strategies that generate immense data volume, placing extreme stress on standard systems.

Institutional strategies often involve:

- High-Frequency Trading (HFT): Generating millions of trades per year, requiring software capable of ingesting and reconciling real-time data streams without failure.

- Multi-Venue Trading: Utilizing prime brokers, dozens of centralized exchanges (CEXs), and over-the-counter (OTC) desks, each with unique data formats.

- Complex Asset Structures: Dealing with locked tokens, vesting schedules, LP (Limited Partner) interests in VC funds, derivatives, and sophisticated decentralized finance (DeFi) activities like liquidity pooling, yield farming, and collateralized lending.

An enterprise solution must be able to categorize, value, and track the cost basis for every single event, not just simple transactions, ensuring data integrity across enormous datasets.

Scope of Assets and Accounting Standards

A retail investor generally focuses on calculating capital gains and losses for local tax filing. A professional firm, however, must adhere to stringent financial accounting standards that impact its balance sheet, P&L (Profit and Loss) statements, and reporting to auditors and investors.

Institutional firms require software that can apply formal accounting methodologies, such as:

- GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards): Digital assets must be classified correctly (e.g., intangible assets, inventory, or financial instruments).

- Fund Administration: Calculating investor capital calls, distributions, management fees, and performance fees (carried interest) based on the realized and unrealized gains of the portfolio.

- Valuation Methodology: Accurately assigning fair market value to highly illiquid assets, such as early-stage token allocations or VC equity stakes, which often lack a readily available exchange price.

The software must handle not just the calculation of tax liability, but the creation of full, auditable financial statements ready for institutional review.

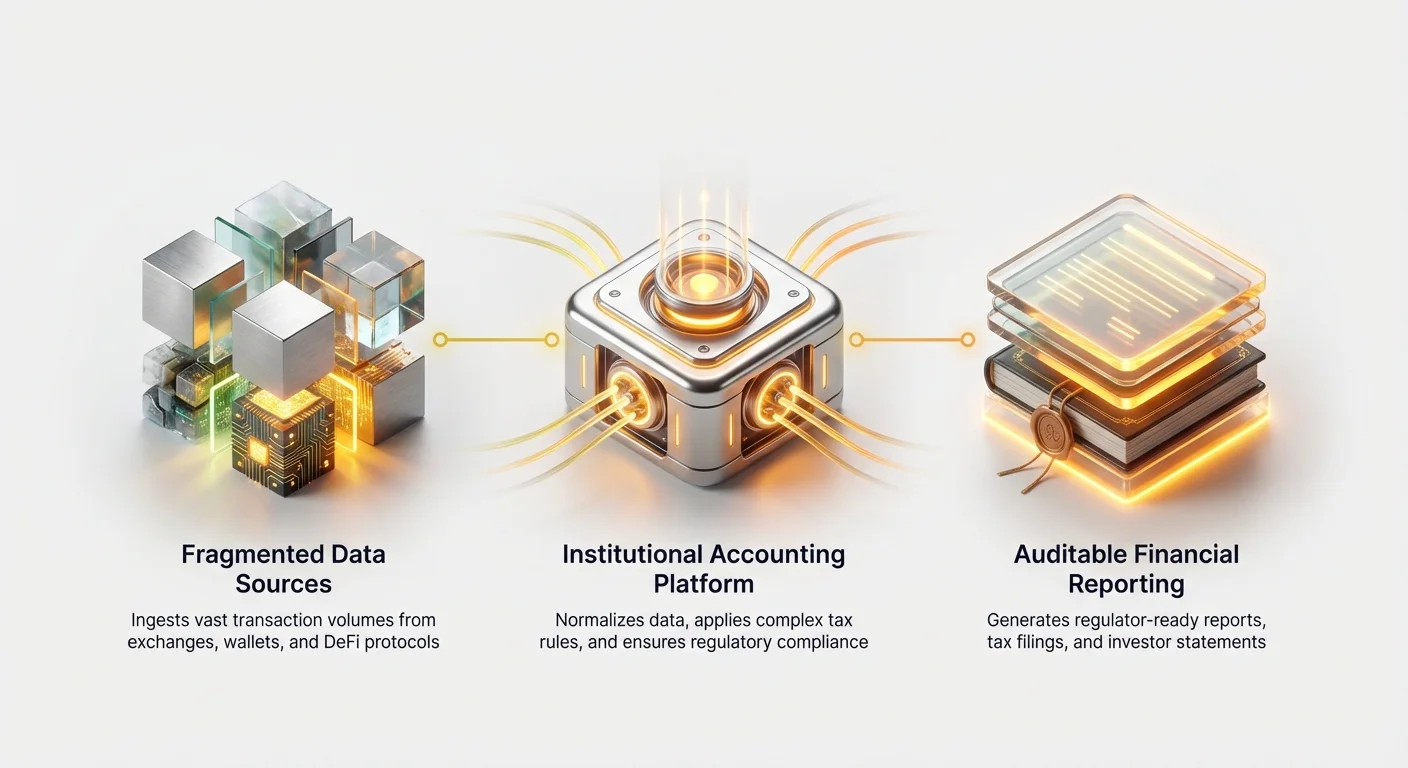

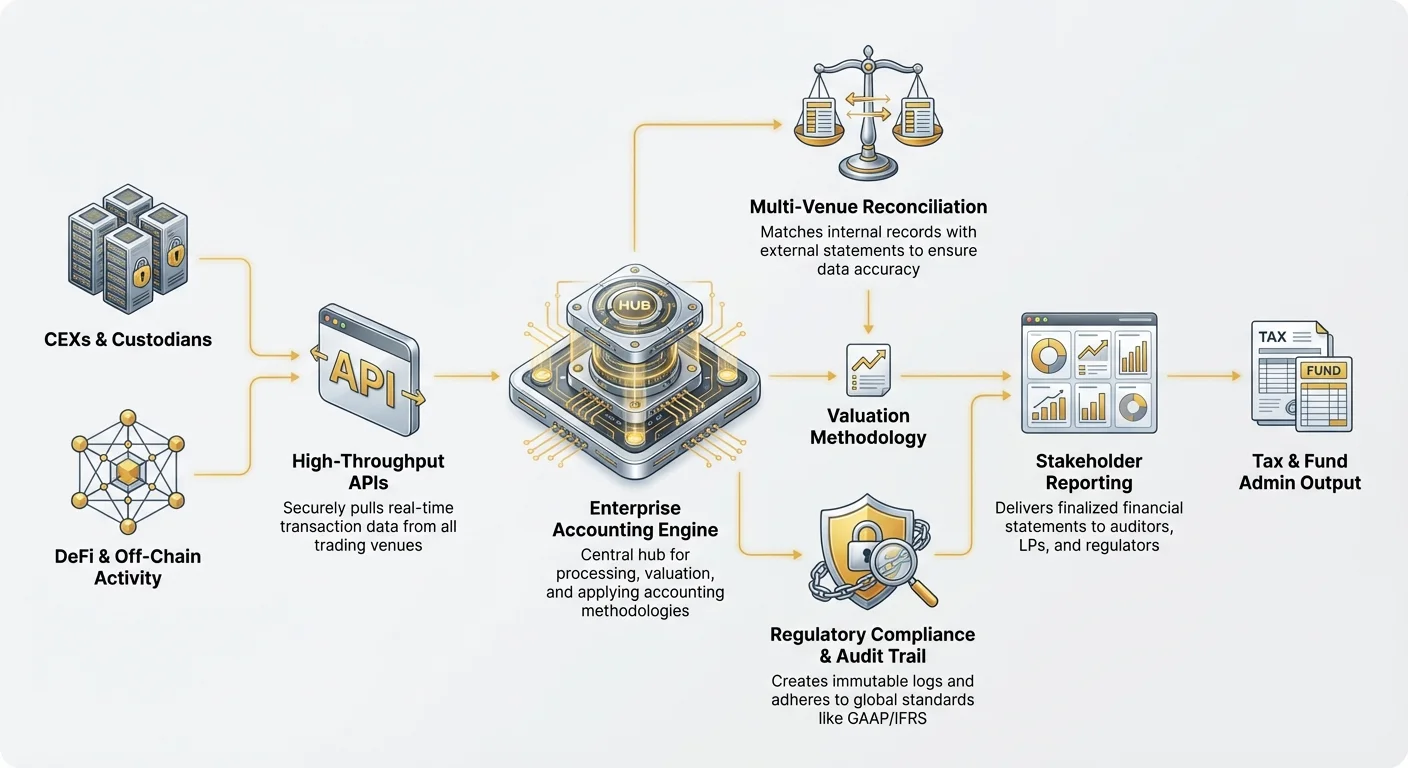

Foundational Requirement: Seamless Data Integration and API Access

The cornerstone of any effective enterprise crypto accounting solution is its ability to reliably and securely ingest massive amounts of data from diverse sources. Reliance on manual CSV uploads—a common practice for retail users—is entirely unfeasible for institutional operations.

API Depth and Reliability

Professional firms require deep integration via Application Programming Interfaces (APIs) that can pull structured data directly from all trading and holding venues. When evaluating software, priority must be given to systems offering:

- High-Throughput APIs: The ability to handle thousands of requests per second, crucial for firms engaged in high-frequency trading where latency and data loss are unacceptable.

- Robust Exchange Coverage: Pre-built, maintained connections to all major CEXs (e.g., Coinbase Prime, Binance Institutional) and, increasingly, proprietary brokerage platforms.

- Real-Time Data Streams: The capacity to track transactions as they occur, providing continuous portfolio monitoring and valuation, rather than relying on delayed nightly batch processes.

If an institution must resort to exporting and normalizing data manually because an API fails or limits transaction retrieval, the operational efficiency gains are lost, and the risk of human error skyrockets.

Multi-Venue Reconciliation and Data Normalization

Crypto trading is inherently fragmented. A large fund might hold assets in a multi-signature hardware wallet, trade spot contracts on Exchange A, use derivatives on Exchange B, and stake assets via a proprietary node.

The chosen software must excel at reconciliation, the process of ensuring that the internal records match the external statements from all venues.

- Standardization: Different exchanges report data (timestamps, fees, asset names) differently. Enterprise software must normalize this input into a single, standardized format internally, ensuring that ‘XBT’ from one venue is correctly matched with ‘BTC’ from another.

- Handling Off-Chain Activity: The system needs mechanisms to account for transactions that occur outside of public blockchain ledgers (e.g., OTC trades settled off-chain or internal transfers between firm wallets) and tie them back to the overall ledger using internal identifiers.

- DeFi Tracking: The integration should extend beyond centralized platforms to track interactions with decentralized protocols. This often requires complex smart contract analysis to interpret activities like depositing collateral, claiming rewards, or liquidating positions, translating these into recognizable accounting events.

Addressing Data Gaps and Error Handling

No data feed is perfect. Institutional systems must include sophisticated error-handling features:

- Gap Identification: Automatically flagging missing transaction IDs, mismatched balances, or sequence breaks that indicate potential data loss or manipulation.

- Manual Adjustment with Audit Trail: Providing the ability for fund administrators to manually input or correct data gaps (e.g., historical records from a newly acquired custodian), while simultaneously creating an immutable log of who made the correction, when, and why—preserving the audit trail.

Ensuring Compliance: The Importance of Auditability and Standards

For financial institutions, auditability is non-negotiable. Regulators, LPs, and internal risk officers must be able to trace every penny, validating the valuation and reporting methodologies used.

Generating a Complete, Immutable Audit Trail

The crypto platform audit trail is perhaps the most critical feature differentiating institutional from retail software. Every transaction and every calculation must be traceable back to its origin.

An enterprise audit trail must capture:

- Source Traceability: Linking the calculated event (e.g., a capital gain) directly back to the raw data input (e.g., the specific API pull from Exchange X).

- Methodology Transparency: Documenting the precise accounting method (e.g., FIFO, LIFO, Specific Identification) used for that specific asset or trade lot, and demonstrating how the software applied this rule.

- Change Log: Recording every user modification, adjustment, or override applied to the data, including timestamps and authorizations.

This level of detail moves beyond simple "tax summaries." It provides the forensic data required to withstand deep scrutiny by a Big Four accounting firm or government regulators like the IRS or SEC.

Calculating Complex Cost Basis Methods at Scale

Cost basis calculation—determining the original price paid for an asset—is foundational to calculating gains and losses. While retail users often default to simple methods like FIFO (First-In, First-Out), institutional firms require flexibility and precision.

Specific Identification (SpecID) is often preferred for optimizing tax liability. This method allows the firm to choose which specific lot of cryptocurrency (e.g., the lot purchased at the highest price) was sold, minimizing taxable gains. Enterprise software must:

- Support Dynamic Methodologies: Allow the fund administrator to apply different calculation methods (FIFO, LIFO, HIFO, SpecID) across various asset classes or trading strategies within the same firm.

- Execute Mass SpecID: Efficiently apply Specific Identification to millions of transactions automatically, rather than requiring manual selection, which is impossible at volume.

- Handle Wash Sale Rules: Automatically detect and flag potential wash sales (if applicable in the jurisdiction), where an asset is sold at a loss and repurchased quickly, ensuring compliance with local tax code restrictions.

Support for Global and Multijurisdictional Reporting

Institutional investment often spans borders. A venture fund might have US LPs, European management, and assets held in offshore trusts. The chosen institutional crypto tax solution comparison must evaluate which vendors excel in handling international complexity.

The software should offer:

- Multi-Currency Reporting: Tracking and reporting gains and losses relative to multiple base currencies (e.g., USD, EUR, JPY) simultaneously.

- Jurisdictional Flexibility: Generating tax forms and reports compliant with different regulatory bodies (e.g., Forms 8949 and 1099-B for the US, specific schedules for the UK or Singapore).

- Localized Tax Treatment: Accurately applying regional tax laws, such as distinguishing between short-term and long-term capital gains, or correctly classifying yield farming income versus capital appreciation based on local rules.

(Note: For more detailed information on specific compliance challenges, refer to our related guide: Global Digital Asset Tax Compliance: Multijurisdictional Reporting.)

Operational Considerations: Scale, Performance, and Security

Beyond data inputs and regulatory output, firms must assess the software’s operational reliability—its speed, security, and the level of professional support provided.

Speed and Computational Power

Enterprise reporting needs often spike dramatically at quarter-end or tax deadlines. A slow or computationally weak platform can delay crucial reporting to LPs and auditors, potentially causing regulatory issues.

A key indicator of an institutional platform's capability is its ability to perform recalculation. If a fund administrator discovers a single missing transaction from three months ago, the system must be able to quickly reprocess every single subsequent trade that relied on the resulting cost basis, often involving millions of data points, in a matter of minutes, not hours or days.

Enterprise-Grade Security and Access Controls

Institutions handle highly sensitive proprietary trading data, investment strategies, and client financial records. Security cannot be compromised.

Look for platforms that adhere to established security certifications:

- SOC 2 Compliance: Ensuring the software provider meets high standards for security, availability, processing integrity, confidentiality, and privacy.

- ISO 27001 Certification: Demonstrating a systematic approach to managing sensitive company information.

- Robust Access Controls: Implementation of multi-factor authentication (MFA), strict role-based access controls (RBAC), and segregation of duties. For instance, ensuring that a junior accountant can view transaction data but cannot finalize and export the official tax schedules.

Dedicated Customer Support and Professional Services

Enterprise clients require more than a chatbot or an online FAQ. Given the complexity of institutional crypto strategies (e.g., handling novel DeFi protocols or specialized derivatives), funds need access to expert assistance.

A high-quality vendor offers:

- Dedicated Account Management: A named professional who understands the firm’s specific investment structure and reporting deadlines.

- Crypto-Native Accountants: Support staff who are experts in digital asset accounting principles, not just general software troubleshooting.

- Implementation Services: Assistance with the initial setup, historical data migration, and integrating the software into existing traditional accounting systems (e.g., QuickBooks Enterprise, SAP).

Cost Analysis and Vendor Selection Strategies

The investment in institutional crypto accounting software is substantial, typically costing significantly more than retail solutions, but offering exponentially greater risk mitigation and efficiency.

Understanding Pricing Models

Enterprise pricing is rarely simple, flat-rate subscriptions. Vendors structure their fees based on factors that reflect the computational load and complexity:

- Tiered Transaction Volume: The most common model, where pricing increases based on the number of API calls or total transaction count processed annually.

- Asset Class Add-ons: Premium fees for integrating complex activities, such as DeFi lending, specialized derivatives tracking, or NFT valuation.

- Jurisdictional Seats: Fees associated with generating reports for multiple distinct tax jurisdictions or for supporting multiple investment vehicles (e.g., Fund A, Fund B, Corporate Treasury).

- Custom Enterprise Agreements: Large institutions often negotiate bespoke contracts that include guaranteed uptime, integration support, and fixed pricing for multi-year commitments.

Firms must analyze not just the monthly fee, but the all-in cost of handling their projected volume growth over the next 3–5 years.

Build vs. Buy: When to Opt for a Third-Party Solution

Some large quantitative funds or financial institutions with deep tech resources consider building proprietary in-house solutions. While this offers maximum customization, it comes with immense risk and cost.

When to Buy (Use Third-Party Software):

- When speed-to-market is critical.

- When the firm is not primarily a software developer.

- When the complexity of regulatory change management is high (tax codes change frequently; third-party vendors are responsible for keeping up).

- For VC firms and funds focused on investment rather than operational technology.

When to Build (Proprietary Solution):

- Only for firms whose trading strategies are so unique (e.g., highly proprietary settlement layers or complex internal cross-book transfers) that no commercial tool can integrate reliably.

- When the security and compliance requirements exceed commercial offerings (rare).

In most cases, partnering with a specialized vendor provides superior flexibility and scalability while shifting the burden of regulatory maintenance.

Practical Tip: The Proof-of-Concept Test

Before committing to a high-cost, long-term contract, a professional firm should insist on a rigorous proof-of-concept (POC) test.

The POC should involve:

- Historical Data Load: Loading a substantial portion of the fund's historical transactions (e.g., the most complex quarter) into the vendor's test environment.

- Reconciliation Drill: Requiring the vendor to reconcile balances and gains/losses against the firm's existing, verified accounting records.

- Audit Trail Review: Having the firm's internal or external auditor review the generated audit trail to ensure it meets institutional standards for transparency and compliance.

If the software cannot successfully handle the firm’s most complicated or high-volume data set during the POC, it should be immediately disqualified as an enterprise crypto accounting software candidate.

Conclusion

The shift towards digital assets introduces profound data management and compliance challenges for professional finance. Choosing the right enterprise-grade accounting and tax software is an operational necessity, serving as a protective layer against regulatory penalties and investor scrutiny.

Professional firms must prioritize solutions defined by their scale, depth of API integration, and unwavering commitment to generating a comprehensive, auditable trail. By focusing on these enterprise-specific features—rather than adopting tools designed for simpler retail use cases—institutions can ensure they maintain high standards of governance, manage risk effectively, and position themselves to scale their digital asset strategies successfully into the future.