Dobrodošli u kompetitivni svet kripto arbitraže. Iako fundamentalni koncept—kupovina imovine jeftino na jednom mestu i njena trenutna prodaja po višoj ceni na drugom—zvuči varljivo jednostavno, postizanje konstantnog profita zahteva više od pukog uočavanja razlike u ceni. Na današnjim hiper-efikasnim tržištima kriptovaluta, uspeh u potpunosti zavisi od brzine i robusne infrastrukture.

Ovaj vodič ide dalje od jednostavnih definicija arbitražnih botova. Fokusiraćemo se na tehničke zahteve, logističke prepreke i infrastrukturne potrebe neophodne za angažovanje u izvršenju niske latencije preko berzi. To je razlika između uočavanja profitabilne prilike i posedovanja tehnološke sposobnosti da se izvrši trgovina pre nego što to učini bilo ko drugi. Za ozbiljne maloprodajne trgovce koji žele da posluju u ovoj kompetitivnoj niši, razumevanje API ograničenja, upravljanje latencijom servera i strateško alociranje kapitala su prave veštine potrebne za uspeh.

Understanding Crypto Arbitrage: What Are We Trying to Do?

Arbitrage is the act of simultaneously purchasing and selling an asset in different markets to profit from a temporary difference in price. In the highly fragmented cryptocurrency landscape, where thousands of assets are traded across dozens of distinct exchanges globally (such as Coinbase, Kraken, Bitget, etc.), these price discrepancies appear constantly. The challenge, however, is executing the trades before the market corrects itself, which often happens within milliseconds.

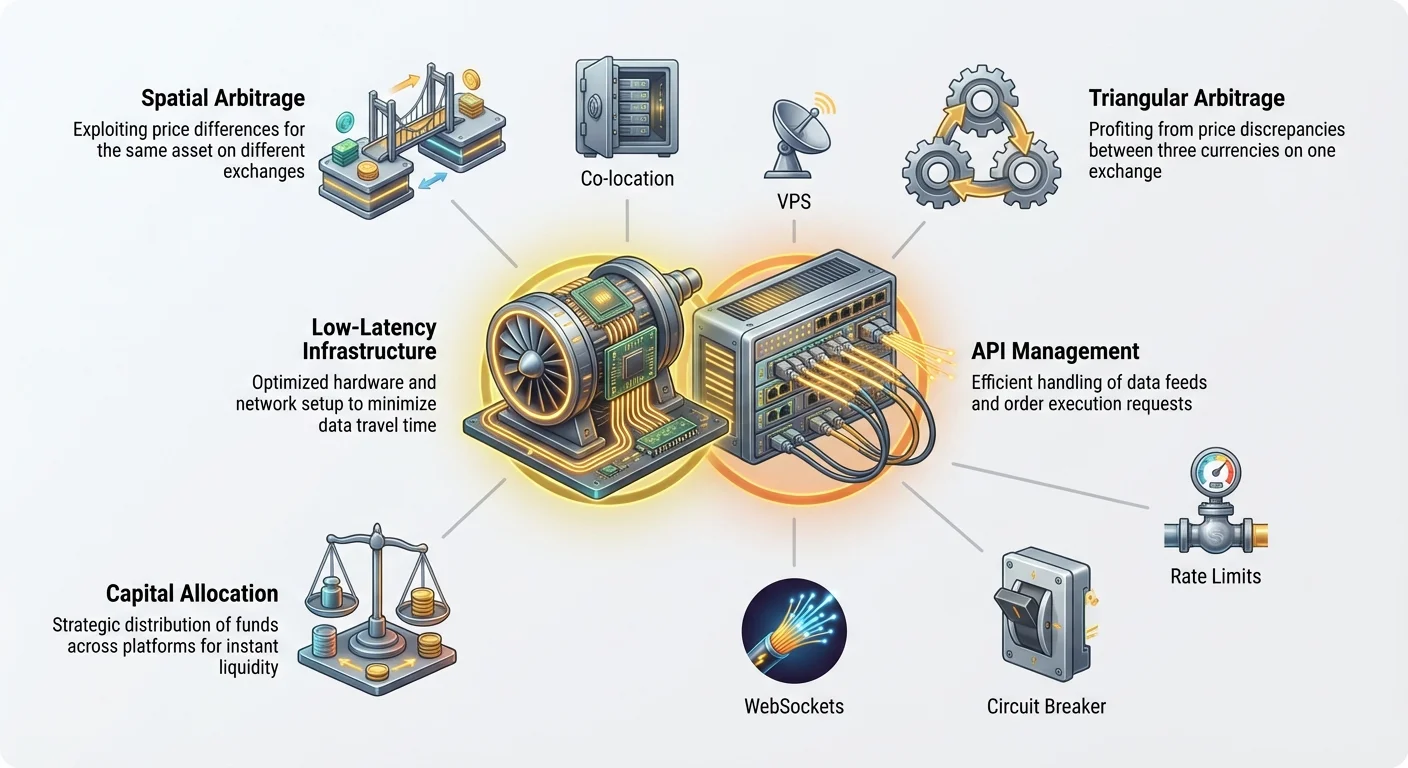

Spatial (Cross-Exchange) Arbitrage

Spatial arbitrage, also known as cross-exchange arbitrage, is the most common and simplest form conceptually. It involves identifying the same asset (e.g., Bitcoin, or BTC) trading at a slightly different price on two distinct exchanges.

Example Use Case: Suppose BTC is trading at $60,000 on Exchange A (a major global platform) and simultaneously trading at $60,015 on Exchange B (a smaller regional platform). The spatial arbitrage opportunity is the $15 difference.

- The system immediately sends a buy order for 1 BTC on Exchange A at $60,000.

- The system immediately sends a sell order for 1 BTC on Exchange B at $60,015.

The gross profit is $15 (minus trading fees and network transfer costs). Since this price difference is immediately visible to all automated systems, the time window for execution is extremely tight—often fractions of a second. This mandates the need for low-latency infrastructure.

Triangular Arbitrage

Triangular arbitrage is more complex as it exploits price inconsistencies between three different currency pairs on the same exchange. Instead of moving assets between platforms, the bot executes a rapid chain of three trades that loop back to the starting asset.

Example Use Case (Using USD as the starting currency):

- Trade 1: Use USD to buy BTC (e.g., $100,000 buys 1 BTC).

- Trade 2: Use the BTC to buy ETH (e.g., 1 BTC buys 15 ETH).

- Trade 3: Use the ETH to sell back for USD (e.g., 15 ETH sells for $100,100 USD).

If the initial cost was $100,000 and the final return is $100,100, the profit is $100. This entire loop must be completed instantaneously to capture the brief inefficiency before the exchange’s internal mechanisms correct the pricing. Since all three trades occur on the same exchange, this strategy is less reliant on external networking speed, but heavily dependent on the API and order book depth of the single exchange being used.

Why Speed is the Only Edge

In any arbitrage scenario, the existence of profit is fleeting. As soon as a price difference appears, two forces immediately work to eliminate it:

- Other bots: Highly optimized, professional trading systems are constantly scanning the same markets. They operate on faster infrastructure and execute orders quicker than the average retail trader.

- Market Efficiency: The buy pressure on the cheaper exchange and the sell pressure on the more expensive exchange quickly push the prices back into alignment.

The moment you identify a $15 opportunity, professional systems have likely already detected and begun closing it. If your execution time is 100 milliseconds and theirs is 50 milliseconds, you will arrive late, potentially failing to execute your trade at the target price, or worse, incurring a loss due to slippage (executing at a worse price than anticipated). Therefore, infrastructure optimization is not optional—it is the prerequisite for viability.

The Core Challenge: Dealing with Latency

Latency, simply defined, is delay. In the context of trading, it is the time taken for information to travel from the exchange’s server to your trading system, and the time taken for your trade order to travel back to the exchange. Minimizing this delay is the single most important factor for low-latency arbitrage.

Defining Latency in Trading

We primarily worry about three types of latency:

- Data Latency: The time it takes for a price update (a new trade or order book change) to leave the exchange and arrive at your computer. If the exchange price is $60,015 but you only receive that update 50 milliseconds late, the opportunity may already be gone.

- Network Latency: The physical time taken for data to travel over the internet cables (from your router, through your ISP, and across continents to the exchange’s data center).

- Execution Latency: The time it takes for your trading system to process the incoming data, calculate the arbitrage profit, construct the buy/sell orders, and send them back to the exchange for filling.

For spatial arbitrage, network latency between two geographically distant exchanges is often the greatest hurdle. For instance, if one exchange is hosted in New York and another in Singapore, the physical travel time for data can easily exceed 150-200 milliseconds, rendering low-latency arbitrage nearly impossible without dedicated network infrastructure.

Co-location and Server Proximity (The Ideal)

The absolute standard for low-latency trading is co-location. This means housing your trading servers within the same physical data center as the exchange’s servers.

Why co-location matters: If your server is in the same building as the exchange server, the signal travels mere feet instead of hundreds or thousands of miles. This reduces network latency from tens of milliseconds (ms) to single-digit or sub-millisecond speeds.

While major exchanges often reserve co-location opportunities for large institutional clients, the retail trader must replicate this advantage as closely as possible using cloud computing infrastructure.

Network Optimization for Retail Traders

Since full co-location is generally out of reach for beginners, retail arbitrage traders must utilize Virtual Private Servers (VPS) strategically placed near the exchange data centers.

Best Practices for VPS Selection:

- Geographic Targeting: Identify the physical locations of your target exchanges' servers. If Exchange A is known to use an AWS data center in Virginia and Exchange B uses a Google Cloud center in London, you need to purchase high-performance VPS instances in both locations.

- Dedicated Resources: Avoid cheap, shared hosting. Low-latency systems require dedicated CPU cores and guaranteed bandwidth. Shared resources can introduce "jitter"—inconsistent processing delays—which is fatal to arbitrage profitability.

- Minimal Hops: Use networking tools (like

pingortraceroute) to check the path data takes from your VPS to the exchange’s API endpoint. Fewer hops (fewer routers and intermediary services) equate to lower latency. Choose VPS providers known for high-quality network backbones. - Operating System Choice: Linux distributions (like Ubuntu or Debian) are standard for trading bots due to their low operating system overhead compared to Windows, which can add unnecessary processing delay (latency) to the execution module.

Actionable Tip: Even if you are operating from your home computer, you must connect to the VPS instances directly. The bot must run 24/7 on the VPS, not on your laptop, ensuring continuous, high-speed connection directly to the exchanges.

Building the Communication Backbone: API Management

After ensuring minimal physical distance (latency), the next critical step is establishing the fastest and most reliable communication pathway to the exchanges. This is done entirely through Application Programming Interfaces (APIs). The API acts as the digital waiter that takes your orders (trades) and brings you the menu (price data).

Understanding REST vs. WebSocket Feeds

Exchanges typically offer two primary methods for interacting with their systems, and understanding the difference is crucial for low-latency trading:

1. REST (Representational State Transfer)

- How it works: This is a traditional request-response model, similar to loading a webpage. You send a specific request (e.g., "What is the current BTC price?") and the exchange sends a static reply.

- Use Case: Ideal for checking account balances, initiating deposits/withdrawals, or sending single, non-time-critical orders.

- Latency Issue: Each REST request requires initiating a new connection and waiting for the full response. This added overhead makes it too slow for real-time price monitoring needed for arbitrage.

2. WebSocket Feeds

- How it works: This establishes a persistent, open connection between your server and the exchange server. Instead of you constantly asking for updates, the exchange pushes real-time price changes (order book updates, completed trades) to your system instantly.

- Use Case: Essential for arbitrage. WebSockets provide the lowest data latency, delivering price feeds as they happen.

- Best Practice: Your data aggregation engine (the scanner) must use WebSockets to monitor the order books of all target exchanges simultaneously.

Handling API Rate Limits

Every exchange imposes rate limits—a cap on how many requests (API calls) your system can send within a specific time window (e.g., 60 requests per second). These limits are designed to prevent malicious denial-of-service (DDoS) attacks and ensure fair access for all users.

The Danger of Rate Limits: If your bot hits the rate limit, the exchange will temporarily blacklist your IP address or throttle your connection, meaning you cannot send or receive price updates or execution orders. This is devastating for an arbitrage strategy where every second counts. If you are halfway through an execution and get rate-limited, the market will move against you, resulting in a guaranteed loss.

Strategies for Mitigation:

- Prioritization and Queuing: Do not spam the API. Implement a sophisticated queuing system that only sends essential requests (primarily execution orders). Price monitoring should rely almost exclusively on the non-rate-limited WebSocket stream.

- Parallel Processing (Carefully): While arbitrage requires simultaneous actions on multiple exchanges, be careful not to create too many concurrent threads to a single exchange's API, which can be mistaken for a DDoS attack.

- Monitor Headers: Exchanges send back HTTP headers that explicitly state how many requests you have remaining before hitting the limit. Your infrastructure must constantly read these headers and dynamically slow down or pause non-critical tasks if the limit is approached.

API Key Security and Best Practices

Your API keys grant your bot full control over your exchange accounts, including the ability to trade and, sometimes, withdraw funds. Securing these keys is paramount.

- Principle of Least Privilege: When generating API keys on the exchange (e.g., Coinbase or Kraken), only enable the necessary permissions: reading account data and trading. Never enable withdrawal permissions unless absolutely required for your specific strategy, as this significantly mitigates risk if your bot or server is compromised.

- Secure Storage: API keys should never be stored in plain text or hardcoded directly into the bot's source code. Use secure environment variables, encrypted key vaults, or dedicated key management services.

- Dedicated Keys: Use unique API keys for each exchange and for each strategy. If one key is compromised, you can revoke it without affecting your access to other platforms.

- IP Whitelisting: If the exchange allows it, configure your API keys so they can only be used from the static IP addresses of your chosen VPS instances. If a hacker steals the key, they still won't be able to use it unless they are also operating from your approved server location.

Dizajn infrastrukture: Komponente arbitražnog sistema

Prebacivanje sa jednostavne skripte na arbitražni sistem proizvodnog nivoa zahteva projektovanje tri različite, ali međusobno povezane, funkcionalne komponente.

1. Mehanizam za agregaciju podataka (Skener)

Ova komponenta je odgovorna za prikupljanje i normalizaciju tržišnih podataka u realnom vremenu sa svih povezanih berzi. Ona je oči i uši sistema.

- Funkcija: Povezuje se putem WebSockets-a sa Berzom A, Berzom B, Berzom C, itd., istovremeno povlačeći podatke knjige naloga (ponude i tražnje), istoriju završenih trgovina i stanja računa.

- Normalizacija: Različite berze različito strukturiraju svoje podatke. Skener mora trenutno prevesti sve dolazne feedove cena u standardizovani format (npr. uvek koristi cenu sa pet decimalnih mesta, uvek koristi simbol BTC/USD) kako bi Mehanizam za odlučivanje mogao da ih pošteno uporedi.

- Praćenje latencije: Skener bi takođe trebalo da meri sopstvenu latenciju podataka—vreme koje je proteklo između objavljivanja promene cene od strane berze i trenutka kada je promena obrađena od strane Skenera. Visoka latencija ovde ukazuje na problem mreže ili VPS-a koji zahteva pažnju.

2. Mehanizam za odlučivanje (Mozak)

Ova komponenta preuzima normalizovane podatke iz Skenera i pokreće vlasničku logiku za identifikaciju i potvrdu profitabilnih arbitražnih prilika.

- Izvršavanje logike: Ovaj mehanizam konstantno vrši složene proračune, upoređujući cene preko berzi (prostorna arbitraža) ili preko tri para na jednoj berzi (trouglasta arbitraža).

- Prag profita: Određuje da li bruto profitna marža (razlika u ceni) premašuje neophodni Prag rentabilnosti (Break-Even Threshold). Ovaj prag mora uključivati sve poznate troškove: naknade za trgovanje, potencijalne naknade za povlačenje i bafer za proklizavanje. Ako je profit $15, a naknade $16, prilika se odmah odbacuje.

- Provera istovremenosti: Za arbitražu preko berzi, Mehanizam za odlučivanje mora potvrditi da adekvatna likvidnost (dovoljan obim u knjizi naloga) postoji na obe berze – kupovnoj berzi i prodajnoj berzi – kako bi se zahtevana veličina naloga trenutno popunila.

3. Modul za izvršenje (Ruke)

Kada Mehanizam za odlučivanje potvrdi izvodljivu priliku iznad praga profita, Modul za izvršenje preuzima kontrolu. Ova komponenta je dizajnirana za brzinu i pouzdanost.

- Istovremeno postavljanje naloga: Modul za izvršenje mora pokrenuti nalog za kupovinu na Berzi A i nalog za prodaju na Berzi B što je moguće bliže istovremeno (proces poznat kao „atomska egzekucija“ u svetu visoke frekvencije).

- Izbor tipa naloga: Za arbitražu se obično koriste tržišni nalozi jer je brzina prioritetnija od sigurnosti cene. Međutim, korišćenje limitiranih naloga neznatno izvan tržišne cene ponekad može smanjiti naknade ako brzina izvršenja nije apsolutno kritična. Većina sistema niske latencije podrazumevano koristi tržišne naloge za garantovano, brzo popunjavanje.

- Sigurnosni mehanizmi i rukovanje greškama: Ovo je verovatno najsloženiji deo. Ako se nalog za kupovinu popuni, ali nalog za prodaju ne uspe (zbog latencije, ograničenja stope ili kretanja tržišta), sistem ostaje držeći imovinu i izložen tržišnom riziku. Modul za izvršenje mora imati trenutne protokole za otkazivanje preostalog naloga i potencijalno izvršenje trgovine za ublažavanje rizika kako bi se pozicija brzo zatvorila i gubici sveli na minimum.

The Logistical Challenge: Capital Allocation

Even with the fastest infrastructure and the most secure APIs, an arbitrage system is useless if the capital is not positioned correctly. The core difficulty of spatial arbitrage is that you need funds ready to execute trades instantly on all target exchanges.

Balancing Funds Across Multiple Exchanges

Arbitrage requires capital to be idle, waiting for an opportunity. You need funds on the "low" side to buy and funds on the "high" side to sell.

The Dilemma of Cross-Exchange Capital: Suppose you target BTC/USD arbitrage between Coinbase and Kraken. You must have:

- USD available on Coinbase to buy BTC.

- BTC available on Kraken to sell for USD.

If an opportunity reverses (Kraken becomes the cheaper source), you immediately need:

- BTC available on Coinbase to sell.

- USD available on Kraken to buy.

This means you must maintain a balanced inventory of both fiat/stablecoins (like USD or USDT) and the target cryptocurrency (like BTC or ETH) across all participating exchanges.

Solution: Automated Capital Rebalancing

A mature arbitrage system includes a sub-module dedicated to capital rebalancing. After a profitable sequence, the net result is an uneven distribution of assets (e.g., more USD on Kraken, less BTC on Coinbase).

- Manual Rebalance: If the profit margin allows, the system must initiate cryptocurrency transfers (BTC, ETH, or sometimes stablecoins) between the exchanges to restore the balanced inventory, preparing for the next trade.

- Stablecoin Preference: Transfers using high-speed, low-fee stablecoins (e.g., USDC or USDT on low-fee networks like Solana or Polygon, if supported by the exchanges) are often preferred for rebalancing, as they minimize volatility risk during the transfer time.

Managing Transaction and Withdrawal Fees

While the gross profit of an arbitrage trade might look appealing, fees can quickly erode the margin. A $15 gross profit quickly disappears if trading fees are $5 (buy) + $5 (sell), leaving only $5.

- Trading Fees: Many exchanges tier their fees based on trading volume. A serious arbitrage setup should aim for high-volume tiers ("Maker-Taker" fees) to minimize cost per trade. Your Decision Engine must incorporate your specific exchange fee structure into its profit calculations.

- Withdrawal Fees: When rebalancing capital, withdrawal and network fees (gas fees) are incurred. Since these fees can be substantial (especially for Ethereum-based tokens), rebalancing must only occur when the accumulated profit significantly outweighs the cost of the transfer. This often means running many small trades to build up enough profit before spending it on a rebalancing transfer.

The Importance of Liquidity

Liquidity refers to how easily an asset can be bought or sold without affecting its price. For arbitrage, high liquidity is non-negotiable.

If you attempt to execute a trade on a low-liquidity exchange, your large market order may instantly "eat up" all the available volume at the advertised price, forcing the remainder of your order to execute at worse prices (slippage).

- Risk: This slippage eliminates the arbitrage profit and can even cause a net loss.

- Mitigation: The Decision Engine must always check the depth of the order book (the volume available at the current price levels) on both sides of the trade. If the available volume is less than your intended trade size, the opportunity should be ignored, regardless of the observed price difference. Focus arbitrage efforts only on high-volume, top-tier centralized exchanges (CEXs) where depth is reliably present.

Security and Risk Mitigation

Operating automated systems that have direct control over significant capital across multiple centralized platforms introduces severe security risks. A single vulnerability can lead to catastrophic loss.

Secure Coding and Environment Practices

Security must be built into the infrastructure from day one.

- Isolation: The production environment (the VPS hosting the live trading system) should be completely isolated from your development or personal machines.

- Firewall Configuration: Configure the VPS firewall (e.g.,

ufwon Linux) to explicitly allow only outgoing connections to the whitelisted exchange API domains, and incoming connections only from your secure management IP (e.g., your home office IP). Block all other unnecessary ports. - Regular Audits: Use external libraries and frameworks (like Python’s CCXT library) that are well-tested for connecting to exchange APIs, rather than trying to build API connectors from scratch. Regularly update all system dependencies to patch known vulnerabilities.

- Logging: Implement detailed, non-sensitive logging. Record every decision made by the system (why a trade was executed, why it was rejected, latency metrics) but never log API keys, secrets, or sensitive credentials.

Implementing Fail-Safes and Circuit Breakers

Automated systems can, and eventually will, encounter unforeseen errors, bugs, or extreme market conditions. A responsible system must have mechanisms to prevent runaway losses.

1. The Circuit Breaker

The circuit breaker is the ultimate safety net. It is a piece of code that, when specific conditions are met, immediately halts all trading activity, cancels open orders, and alerts the operator.

Triggers for the Circuit Breaker:

- Maximum Daily Loss: If the system’s running P&L (Profit and Loss) exceeds a preset daily limit (e.g., losing more than 2% of total capital), the system shuts down.

- Excessive Errors: If the system receives a high volume of unhandled API errors (e.g., rate limit errors or execution failures) within a short time frame, indicating a systemic issue.

- Connectivity Loss: If the system loses connection to one or more critical WebSockets for more than 60 seconds.

2. Position Limits

Always impose strict limits on the maximum size of a single trade and the maximum net exposure (total asset value held) at any given time. This ensures that even a catastrophic error only affects a portion of the capital, not the entire portfolio.

Protecting Your API Keys and Credentials

As discussed briefly in the API section, key management is paramount. Consider using encrypted volumes or specialized secrets management tools (like HashiCorp Vault) to ensure that even if the underlying VPS is breached, the attacker cannot immediately gain access to the raw credentials needed to steal funds or execute malicious trades.

Best Practice: Use two-factor authentication (2FA) wherever possible, even for read-only access to your exchange accounts, and ensure the 2FA method is not tied to the server running the bot.

Zaključak: Utrka protiv nulte dobiti

Potraga za arbitražom niske latencije je kontinuirana borba za marginalne prednosti. Iako je koncept kupovine nisko i prodaje visoko intuitivan, izvršenje zahteva duboku posvećenost tehnološkoj infrastrukturi i rigoroznoj logistici.

Za početnika, uspeh u ovoj niši ne dolazi od pronalaženja „magičnog bota“. Dolazi od savladavanja optimizacije latencije, marljivog upravljanja API interakcijama kako bi se izbegla ograničenja stope, i strateškog alociranja kapitala preko više berzi kako bi se osigurala trenutna likvidnost.

Kako globalna kripto tržišta sazrevaju i profesionalne firme za trgovanje visokih frekvencija sve više ulaze u prostor, prozor profitabilnosti za arbitražu se smanjuje. Utrka protiv nulte dobiti znači da je optimizacija infrastrukture jedini održiv način da se održi prednost. Fokusiranjem na veze niske latencije, sigurno upravljanje API-jem i robusno rukovanje greškama, ozbiljni maloprodajni trgovci mogu izgraditi temelj neophodan za takmičenje, čak i ako je to samo na manjim, brže pokretnim prilikama preko berzi koje i danas postoje.