Welcome to the world of professional cryptocurrency trading. While many retail traders focus on directional bets—buying low and hoping to sell high—the market's fundamental infrastructure relies on a more sophisticated strategy: Market Making (MM). Market making is the process of continuously offering to buy and sell an asset, thereby providing the essential ingredient for any healthy market: liquidity.

This guide is designed to take you from a basic understanding of market mechanics to the professional requirements of high-frequency liquidity provision. Market making is not simply setting a bot and walking away; it is a sophisticated business involving rigorous risk management, deep understanding of market microstructure, and high-performance technological infrastructure.

We will explore how market makers capture profits by exploiting the narrow space between the buy and sell prices (the spread), and crucially, how they manage the inventory risk inherent in constantly holding assets. For those seeking to move beyond simple algorithmic trading and build a sustainable, professional trading operation in the crypto space, mastering market making strategies is the critical next step.

The Foundation of Market Making: What is Liquidity?

Before diving into strategy, we must understand the core concept that market makers provide: liquidity. Liquidity refers to how easily an asset can be bought or sold without significantly affecting its price. A highly liquid market (like BTC/USD) means large orders can be executed quickly and efficiently. A highly illiquid market means a single large order could crash the price significantly and requires liquidity and slippage mastery.

Market makers are the backbone of liquidity. By constantly placing orders on both sides of the order book, they ensure that whenever a buyer or seller enters the market, there is always someone ready to take the other side of the trade immediately.

The Role of the Bid-Ask Spread

The heart of market making profit lies in the bid-ask spread.

The Bid price is the highest price a buyer is currently willing to pay for an asset. The Ask (or Offer) price is the lowest price a seller is currently willing to accept for that asset.

The difference between the highest bid and the lowest ask is the bid-ask spread.

Example: If the highest bid for Bitcoin (BTC) is $60,000, and the lowest ask is $60,002, the spread is $2.

A market maker profits by simultaneously placing a bid (e.g., $60,000.50) and an ask (e.g., $60,01.50). If a trade executes successfully on both sides (they buy at $60,000.50 and immediately sell the same amount at $60,001.50), they capture the $1 spread, minus any trading fees. This rapid, repeated capture of the spread is the goal of professional market making, demanding minimizing trading costs.

Market Takers vs. Market Makers

It is crucial to differentiate between two primary types of participants who interact with an exchange’s order book:

- Market Takers (Takers): These traders execute orders immediately. If you place a "Market Order," you are immediately taking the best available price from the existing orders on the book. Takers prioritize speed and certainty of execution over price. They typically pay higher fees (Taker Fees) because they are consuming liquidity.

- Market Makers (Makers): These traders place "Limit Orders" that rest on the order book, waiting to be filled. By waiting, they provide liquidity to the market. Makers prioritize maximizing their captured spread and minimizing fees. Exchanges often reward market makers with lower fees, or even fee rebates, because they are providing a valuable service.

Actionable Insight: Professional market making strategies rely entirely on being rewarded as a "Maker." Even small fees can erode the tight profit margins generated by capturing tiny spreads, so minimizing or even earning rebates on fees is essential for profitability.

MM vs. Scalping: A Critical Distinction

While both market making and scalping are high-frequency strategies designed to capture small profits quickly, their roles and intentions are fundamentally different:

| Feature | Market Making | Scalping |

|---|---|---|

| Primary Goal | Provide liquidity; capture the bid-ask spread repeatedly. | Profit from short-term directional price movements. |

| Order Type Focus | Limit Orders (Maker) to rest on the book. | Market Orders or aggressive Limit Orders (Taker). |

| Risk Focus | Inventory Risk (holding unwanted assets). | Directional Risk (price moving against the trade). |

| Market Role | Essential infrastructure provider. | Speculator. |

| Holding Period | Extremely short, often milliseconds (just long enough to fill the other side). | Seconds to minutes. |

A market maker is indifferent to the ultimate direction of the price; they just need the price to bounce back and forth quickly so their buy and sell orders are filled sequentially. A scalper, conversely, is trying to predict where the price will move next, even if only by a fraction of a percent.

Understanding the Market Making Strategy

The core strategy in market making is simple: continuously place limit orders near the current market price. The complexity arises in dynamically adjusting where those orders are placed and how much volume is committed.

The Goal: Capturing the Spread

A successful market maker must ensure that their orders are positioned optimally:

- Close Enough to the Center: The orders must be near the current best bid/ask so they get filled frequently. If your bid is too low, you’ll never buy anything.

- Wide Enough Spread: The distance between your bid and ask must be large enough to cover trading fees and latency costs, leaving a net profit.

Market makers earn profit from the volume they process. Instead of making 10% on one trade, they aim to make 0.01% on thousands of trades per day. This requires high trading volume and extreme efficiency.

Example Scenario (Micro-Profit):

- Exchange Fee (Maker Rebate): 0.01%

- BTC Price: $60,000

- MM Bid: $59,998 (Buy 1 BTC)

- MM Ask: $60,002 (Sell 1 BTC)

- Spread Captured: $4.00

- Fees Paid (Rebates Earned): If the exchange offers a small rebate, the net profit might be $4.50 per round trip (buy and sell).

This calculation highlights why large capital pools and high-frequency execution are necessary to make this strategy viable at a professional level.

The Two Primary Architectures: Order Books vs. AMMs

Market making strategies differ significantly depending on the underlying structure of the trading platform:

1. Centralized Exchange Order Books (CEX)

In a traditional CEX (like Coinbase Pro or Kraken), trading is facilitated by a centralized order book. Market makers directly compete with all other participants for the best price placement.

Key Requirements:

- Speed: Low latency is crucial. Even a delay of a few milliseconds can mean another bot captures the profitable spread before you. This leads to the requirement for High Frequency Trading (HFT) crypto setups.

- Infrastructure: Requires direct, secure API connections and often dedicated, close proximity servers (co-location) to the exchange’s matching engine.

- Strategic Depth: Requires algorithms to detect subtle shifts in market momentum and rapidly update orders to avoid adverse selection (being filled only when the price is about to move against you).

2. Automated Market Makers (AMM)

Decentralized Exchanges (DEXs), like Uniswap or SushiSwap, often use AMMs. Instead of an order book, trading occurs against a pooled contract (liquidity pool). Providers who deposit assets into this pool are the de facto "market makers."

Key Requirements:

- Passive Provision: The pricing mechanism is governed by mathematical formulas (e.g., $x * y = k$). The provider is typically passive, earning trading fees from the pool as trades happen.

- Impermanent Loss (IL): This is the AMM equivalent of inventory risk. If the price of one asset in the pool dramatically changes compared to the other (e.g., ETH rockets up while USDC stays stable), the pool automatically sells the rising asset for the stable asset, leaving the provider with fewer tokens than if they had simply held the initial assets.

- Strategy: Strategies involve determining optimal fee tiers, leveraging concentrated liquidity (placing funds only within a small price range), and actively managing the pool to mitigate IL risk.

While AMM provision is technically "market making," professional crypto market making typically refers to high-frequency, active management on centralized order books due to the higher potential for leveraged, high-volume spreads.

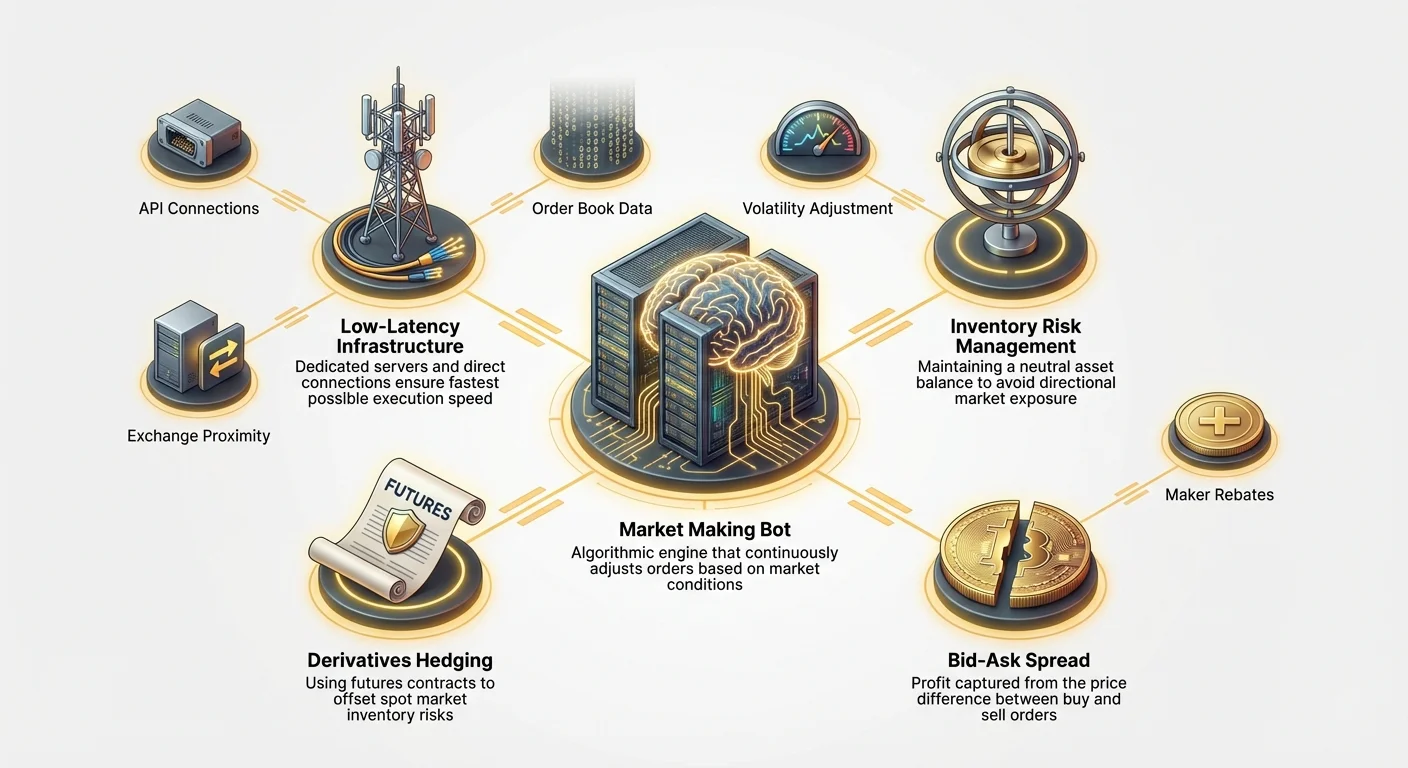

The Toolkit: Market Making Bots and Automation

Manual market making is impossible due to the speed required. Professional market making necessitates specialized software—MM bots—capable of processing real-time data and executing orders faster than humanly possible.

Essential Components of an MM Bot

A robust market making system is complex, but it relies on three core operational modules:

1. The Market Data Engine

This module connects via the exchange’s WebSockets API to receive real-time data streams: the full order book (depth), recent trades, and account balances. Speed is paramount. The bot must ingest and process this data with minimal latency to determine the true current best bid and ask.

2. The Strategy Engine

This is the "brain" of the bot, containing the logic for placement, cancellation, and inventory management. It calculates the optimal spread width based on factors like volatility, market depth, and current inventory skew.

Basic Logic:

- If current inventory is balanced (50% BTC, 50% USD), place symmetric orders around the midpoint.

- If current inventory is heavy on BTC, skew the spread aggressively (lower the ask, raise the bid) to encourage selling BTC and buying USD, thus rebalancing the inventory.

3. The Execution Engine (Order Management)

This module sends limit orders, updates existing orders, and cancels them instantly using the exchange’s REST API. It must handle exchange errors, manage order IDs, and ensure that orders are canceled immediately if a counter-party takes one side of the spread to prevent adverse inventory skew.

Low-Latency and Connectivity Requirements (The HFT Component)

The pursuit of minimal latency is the key differentiator between casual algorithmic trading and professional market making (often called high frequency trading crypto). Time is literally money in this environment.

Why Latency Matters

Imagine two market makers, Bot A and Bot B, both targeting a $2 spread on BTC.

- Bot A has 100 milliseconds (ms) latency.

- Bot B has 5 ms latency.

A massive buy order hits the market, instantly pushing the price up by $50. Bot B, seeing the price movement 95ms earlier than Bot A, instantly cancels its old buy order and places its new orders at the higher price midpoint. Bot A, delayed, might have its old buy order filled right before the price jumps, saddling it with BTC that is now instantly less profitable—this is called "getting picked off."

Professional Setup Requirements:

- Direct API Connections: Use specialized exchange APIs designed for high throughput and low latency, avoiding standard consumer interfaces.

- Dedicated Hardware: Running bots on high-specification, dedicated servers with minimal background processes.

- Co-Location or Proximity Hosting: For the most extreme HFT operations, servers are physically placed within the same data center (co-located) as the exchange’s matching engine. While often impractical for smaller firms, using dedicated cloud servers physically near the exchange’s known server locations (proximity hosting) is a standard competitive advantage.

Strategy Implementation: Simple Grid vs. Adaptive Spreads

MM bots implement strategies ranging from the very simple to the extremely complex:

1. Simple Grid (Passive MM)

This is the simplest form, often used by retail tools. The bot places a fixed quantity of orders spaced equally above and below a central price point, forming a "grid."

- Pros: Easy to implement, runs well in ranging, low-volatility markets.

- Cons: Fails spectacularly in trending markets, as the bot will continuously buy on the way down and sell on the way up, leading to massive inventory risk.

2. Adaptive Spreads (Professional MM)

Professional strategies dynamically adjust the distance of the orders (the spread width) based on real-time factors:

- Volatility: If volatility spikes, the spread is widened to compensate for the higher risk of sudden price moves (adverse selection).

- Depth: If the order book is very thin (low depth), the bot might widen the spread or pull orders entirely until liquidity returns.

- Directional Indicators: Advanced bots might use momentum indicators or external data feeds to slightly tilt the placement of orders—placing a bit more sell pressure if they expect a small price drop, but always keeping the core purpose of market making intact.

The Primary Challenge: Managing Inventory Risk

For professional market makers, the greatest threat to profitability is not the spread width or latency, but inventory risk.

Defining Inventory Risk (Holding the Wrong Assets)

Inventory risk is the danger that a market maker ends up holding a disproportionate amount of one asset, and the price of that asset moves adversely before they can offload it.

Example of Inventory Risk: A market maker starts with 1 BTC and $60,000 USD (balanced).

- The market starts trending heavily down.

- Every time a seller hits the market, the market maker's buy order (the Bid) is filled.

- The market maker keeps accumulating BTC, but nobody is buying their sell order (the Ask).

- Soon, they have 5 BTC and $30,000 USD. The price of BTC drops from $60,000 to $55,000.

- The market maker now has a massive paper loss on their 4 excess BTC, wiping out days or weeks of tiny spread profits.

Inventory management is the mechanism used to constantly steer the portfolio back toward a desired neutral state (usually 50% base currency, 50% quote currency by dollar value).

Neutralizing Exposure with Hedging Strategies

To truly operate as a professional liquidity provider, market makers cannot afford to take large directional bets. The spread profit is their margin; they must use hedging instruments to neutralize the directional price risk of their inventory.

This is done using derivatives, specifically Futures or Perpetual Contracts.

Hedging Example (Maintaining a Delta-Neutral Position):

- The Problem: Our market maker is now long 4 extra BTC due to the inventory skew. If BTC drops, they lose money.

- The Solution: The market maker immediately sells 4 BTC worth of a BTC/USD Perpetual Futures contract on a separate derivatives exchange.

| Action | Spot Exchange (MM Bot) | Derivatives Exchange (Hedge) | Net Result |

|---|---|---|---|

| Inventory Skew | Long 4 BTC in inventory. | Zero position. | Exposed to $ decline. |

| Hedging Move | Continues MM operations. | Short 4 BTC Perpetual Contract. | Delta Neutral. |

| Market Outcome | BTC price drops $1,000. | Spot inventory loses $4,000. | Perpetual short gains $4,000. |

By maintaining this delta-neutral position, the market maker is protected from price swings. Their sole focus returns to capturing the bid-ask spread, independent of the asset’s direction. This integration of spot market making with futures hedging is a hallmark of professional crypto market making.

Adjusting Spreads Based on Inventory Skew

While external hedging (using derivatives) manages the risk, internal spread adjustment helps manage the flow and rebalance the inventory passively:

- Skewing the Spread: If the bot is excessively long BTC, it will automatically shift its orders. It will aggressively lower the Ask price and slightly raise the Bid price, narrowing the spread on the sell side and widening it on the buy side. This encourages market takers to buy BTC from the MM and discourages them from selling BTC to the MM.

- Order Size Adjustment: The bot might also increase the size of its sell orders and decrease the size of its buy orders, making it easier to offload the excess inventory.

- Automatic Shutdown: If inventory skew exceeds a predetermined threshold (e.g., 80/20 split), a well-designed MM bot will automatically pull its orders or enter a "risk reduction mode," only placing orders that help return the inventory to neutral, until the skew is manageable again.

Professional Infrastructure and Execution

Moving from a hobbyist bot to a professional market making operation requires a significant upgrade in security, reliability, and connectivity.

API Key Management and Security Protocols

API keys are the digital gateway to the market maker’s capital. A security lapse is catastrophic.

Required Security Measures:

- Granular Permissions: API keys should only have the exact permissions required (e.g., Trade and Read balances), never Withdrawal permissions.

- IP Whitelisting: Keys should be restricted so they can only be used from a specific, whitelisted IP address (the dedicated server). If a key is stolen, it is useless unless the thief is using the whitelisted server.

- Encryption: All communication between the bot and the exchange must use strong encryption (TLS/SSL).

- Bot compartmentalization: Separate keys and separate execution environments (sub-accounts) should be used for different strategies or different exchanges. This limits the damage if one specific strategy is compromised.

Co-location and Dedicated Servers

As mentioned previously, latency is paramount, particularly for high frequency trading crypto where milliseconds determine success.

Server Requirements:

- CPU Power: While MM isn’t strictly CPU-bound, the speed of processing market data feeds and strategy calculations must be maximized. High core clock speed is more important than high core count.

- Memory (RAM): Sufficient RAM is necessary to hold the full historical and real-time order book data in memory for instant look-up.

- Internet Connectivity: Dedicated, stable, low-jitter network connections are non-negotiable. Public cloud providers (AWS, Google Cloud) often offer dedicated proximity hosting zones near major financial data centers, which is a common setup for professional operations.

By minimizing the physical distance and optimizing the network path to the exchange, professional market makers gain the crucial time advantage needed to cancel losing orders or post profitable new ones before the competition.

Choosing the Right Exchange and Trading Pair

Not all liquidity is created equal. The choice of venue and asset pair determines the viability of the strategy.

Exchange Considerations:

- Fee Structure: The primary factor. Professional MMs seek exchanges that offer significant Maker Rebates, meaning they are paid a small fraction of the trade value for providing liquidity. A 0.01% rebate significantly boosts profitability compared to a 0.05% fee.

- Reliability and Uptime: Exchange downtime means lost profits and, worse, potentially stuck positions that cannot be hedged or managed.

- API Quality: Does the API support high-frequency order modification, cancellation, and granular data access without rate limiting or excessive buffering?

- Colocation Access: Does the exchange offer premium access or proximity benefits for large volume traders?

Trading Pair Selection:

Professional market makers generally target pairs that exhibit specific characteristics:

- Tight Spreads: Highly liquid major pairs (BTC/USD, ETH/USD) offer tiny spreads, requiring high volume and low latency.

- Mid-Cap Volatility: Certain mid-cap altcoin pairs might have wider, more profitable spreads, but the risk of inventory skew is higher due to lower volume.

- Arbitrage Opportunities: Sometimes, MM bots are deployed on specific illiquid pairs where the MM can act as a bridge, arbitraging the difference between the exchange's price and the global index price.

Advanced Market Making Strategies

Once the foundational infrastructure is secured and basic risk management is in place, professional firms employ highly sophisticated strategies to maximize the capture rate and minimize adverse selection.

Volatility Skew and Spread Pricing

Simple MM bots use a fixed spread width (e.g., always $2 away from the center). Advanced systems use predictive models to determine the optimal spread dynamically.

Volatility Adjustment:

If the market is currently quiet, a MM might aggressively narrow the spread to $1.50 to ensure they are the first to get filled. If a major economic announcement is due, volatility is expected to spike, and the spread might be widened to $5 to protect against getting filled just before a sharp, unfavorable move.

Price Skewing (Micro-Momentum):

Sophisticated bots analyze the momentum of executed trades. If the market is seeing continuous, high-volume buying over the past second, this suggests temporary upward pressure. The bot might immediately:

- Cancel its current buy orders (Bids).

- Raise its sell orders (Asks) slightly higher to capture the expected imminent rise.

- Re-deploy the Bids higher after the upward pressure subsides.

This adaptive response attempts to avoid adverse selection, which is the bane of market making—only getting filled when the market is moving against your position.

Cross-Exchange Market Making (Arbitrage Integration)

While market making focuses on a single exchange's spread, the activity is often integrated with low-latency arbitrage strategies.

If a market maker detects a price imbalance—say, BTC is trading for $60,000 on Exchange A but $60,010 on Exchange B—they can use their infrastructure to profit from the difference while simultaneously providing liquidity.

- Scenario: Market Maker is operating on Exchange A.

- They see a temporary arbitrage opportunity on Exchange B.

- The MM bot places aggressive bids on Exchange B while simultaneously maintaining its neutral inventory position on Exchange A via hedging or spot sales.

In the professional realm, market making and cross-exchange arbitrage are often executed by the same systems, leveraging the identical low-latency infrastructure to switch instantly between providing liquidity and exploiting pricing inefficiencies across venues.

Dealing with Slippage and Front-Running

In illiquid markets, or when dealing with large volumes, slippage and front-running pose significant dangers.

Slippage

Slippage occurs when an order is executed at a worse price than expected because the liquidity at the intended price level was insufficient. For a professional MM, slippage is usually a problem for the market takers, not the maker. However, MMs must calculate their spread based on the anticipated volume they can fill without causing the market to move against their position.

Front-Running (The latency battle)

Front-running is a major issue in decentralized finance (DeFi) and, in a more technical sense, on centralized order books. It occurs when a faster bot detects a large incoming order and jumps ahead, placing its own orders to profit from the guaranteed price movement caused by the initial large order.

Professional high frequency trading crypto firms constantly fight front-running by:

- Minimizing Latency: The fastest bot wins.

- Iceberg Orders: Breaking up large volume orders into smaller, hidden chunks that are slowly revealed to the market, concealing the true intent.

- Intelligent Placement: Placing orders in non-obvious spots in the order book (not always directly at the best bid/ask) to fish for specific types of flow.

Conclusion

Professional crypto market making is far removed from the casual use of retail trading bots. It is a high-stakes, high-volume business model focused purely on optimizing execution speed, minimizing fees (ideally earning rebates), and meticulously managing inventory risk through sophisticated hedging strategies.

For those serious about building a high-frequency trading operation, the roadmap is clear:

- Master Risk: Prioritize inventory management and deploy robust, non-directional hedging using derivatives.

- Optimize Infrastructure: Invest in low-latency connectivity, dedicated servers, and secure API management.

- Adaptive Strategy: Move beyond simple grid strategies toward adaptive spread pricing based on real-time volatility and micro-momentum analysis.

By understanding that the market maker’s true product is liquidity, and their profit is earned through efficiency and risk control, aspiring professional traders can begin laying the foundation for a sustainable and sophisticated operation in the complex digital asset landscape.