The cryptocurrency world was born from the desire to create a parallel financial system, independent of traditional institutions. Yet, as the digital asset space has matured, large-scale capital managers—from institutional funds to sophisticated corporate treasuries—have struggled with one key challenge: connecting volatile digital assets to predictable, stable income streams found in the traditional economy.

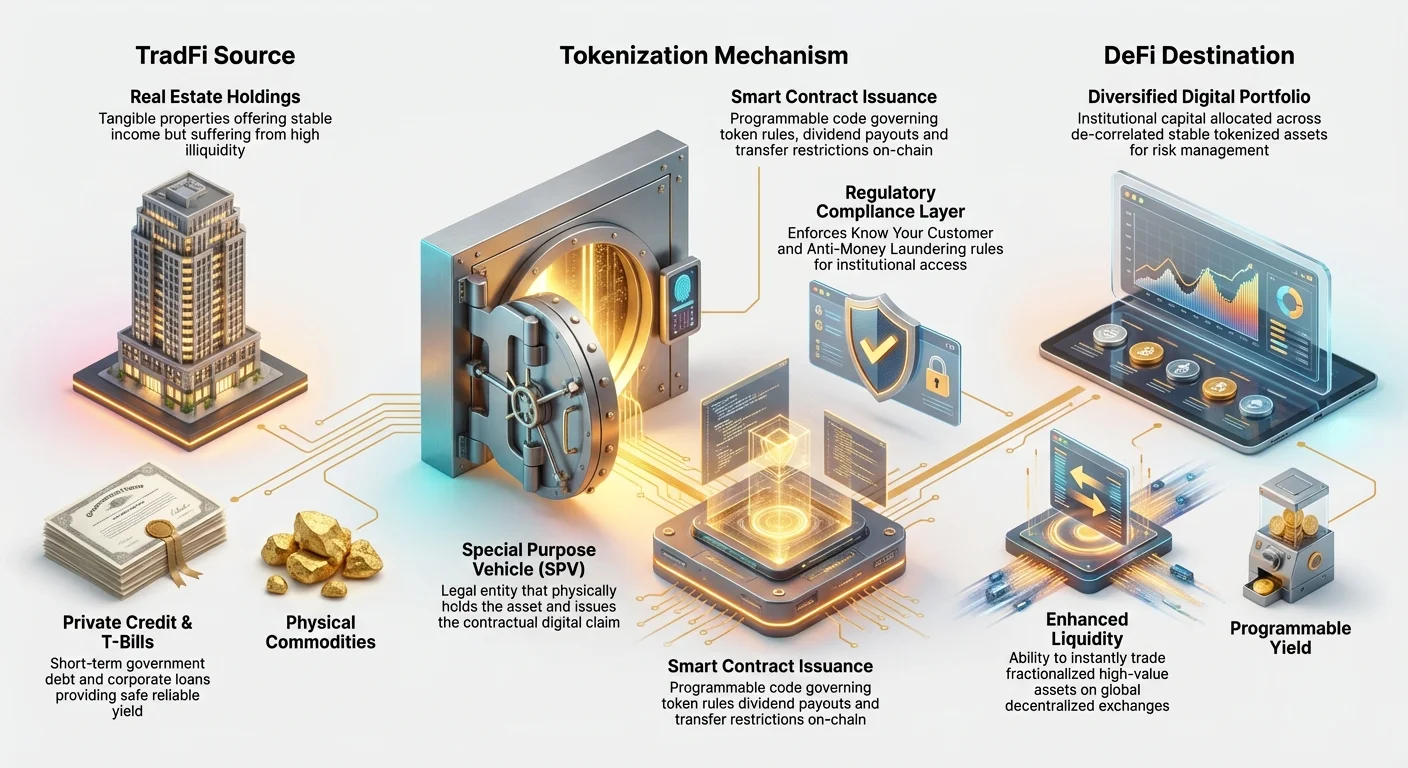

This challenge has given rise to one of the most significant trends in modern finance: the tokenization of Real World Assets (RWAs). RWAs refer to tangible or verifiable assets that exist outside the blockchain—everything from real estate and private credit to gold and intellectual property. By converting the ownership rights of these assets into secure, tradeable tokens, institutions are creating a powerful bridge between the stability of traditional finance (TradFi) and the efficiency of decentralized finance (DeFi).

For fund managers, large private investors, and financial institutions, RWAs are not just an interesting technological development; they are becoming an essential tool for sophisticated capital management. They offer a mechanism to stabilize portfolio volatility, unlock liquidity from otherwise frozen assets, and integrate compliant, yield-generating instruments directly into digital strategies. This deep dive explores how RWAs are transforming institutional crypto portfolios and the legal, technological, and strategic framework required to utilize them effectively.

Understanding Real World Assets (RWAs) and Tokenization

Before diving into complex portfolio strategies, it is essential to grasp the fundamental concepts of what RWAs are and how the process of tokenization works. At its simplest, an RWA is any asset that has value and existence independent of the blockchain network it may be represented on.

The Bridge Between Traditional Finance (TradFi) and Decentralized Finance (DeFi)

Historically, traditional assets—such as a piece of commercial property, a corporate bond, or a portfolio of loans—have suffered from inherent inefficiencies: they are illiquid (hard to buy or sell quickly), fragmented (difficult to fractionally own), and slow to settle (transferring ownership takes days or weeks).

The value proposition of tokenizing these assets is straightforward: to bring the transparency, efficiency, and programmability of blockchain technology to assets that currently reside in slow, opaque, and centralized legal systems.

When an institution decides to manage capital, they typically allocate funds across different asset classes—stocks, bonds, real estate, and alternatives. Crypto assets, like Bitcoin or Ether, often fall into the "alternative" bucket and introduce high volatility. RWAs allow managers to introduce low-volatility, income-generating traditional assets into a digital portfolio, thereby stabilizing overall risk while retaining the benefits of 24/7 blockchain liquidity and instantaneous settlement. They function as a crucial middle ground, offering the utility of digital assets without the dependency on pure crypto market speculation.

How Tokenization Works: The Digital Title Deed

Tokenization is the process of creating a digital representation—a token—on a blockchain that signifies verifiable legal ownership or economic rights over a specific real-world asset. This token acts much like a digital title deed or a fractional share.

The process involves several critical steps:

- Legal Structuring: The real-world asset (e.g., a commercial mortgage) is first placed into a traditional legal entity, often a Special Purpose Vehicle (SPV) located in a favorable jurisdiction. This SPV legally owns the physical asset.

- Due Diligence: Comprehensive audits, appraisals, and legal vetting are performed on the asset to verify its value and clean title.

- Token Issuance (Minting): The SPV then contracts a specialized tokenization platform to issue digital tokens on a chosen blockchain (like Ethereum or Solana). The total number of tokens issued equals the total value or fractional units of the underlying asset.

- Linking: Crucially, the smart contract governing the token is programmed to reference the legal documentation tying the token back to the physical asset held by the SPV.

- Distribution: These tokens can now be sold, traded, or used as collateral globally, instantly, and permissionlessly (depending on regulatory requirements).

The token itself is not the asset; it is a compliant, fractional claim on the asset’s legal owner (the SPV), which simplifies secondary trading and management.

The Institutional Imperative: Why RWAs are Crucial for Capital Management

For institutions dealing with hundreds of millions or billions in digital assets, capital management requires robust strategies that prioritize risk control, compliance, and sustained yield. RWAs address these demands directly, offering solutions that purely native crypto assets cannot.

Diversification and De-Correlation

A fundamental goal for institutional portfolio managers is diversification—spreading risk so that a single market downturn doesn't wipe out the entire portfolio. In traditional finance, managers rely on assets that are "de-correlated," meaning their prices move independently of one another.

Pure cryptocurrency prices, however, are often highly correlated with each other, meaning a significant dip in Bitcoin often pulls the entire market down. By incorporating tokenized RWAs—such as fractional ownership in stable real estate markets or secure government bonds—managers introduce assets whose price movements are tied to entirely different macro-economic factors (interest rates, geographical demand, local credit markets) rather than purely crypto sentiment.

Example: During a rapid decline in the digital asset market, the value of tokenized US Treasury bills remains stable because their value is governed by the creditworthiness of the U.S. government, providing a reliable hedge or safe harbor within the digital portfolio. This de-correlation is paramount for maintaining long-term financial stability for large asset holders.

Enhanced Liquidity for Illiquid Assets

Many high-value traditional assets—commercial real estate, fine art, private equity shares—are inherently illiquid. If an institution holds a $50 million investment in a private credit fund, they usually face years-long lockup periods and difficulty selling fractional pieces quickly.

Tokenization instantly solves this illiquidity problem. By fractionalizing the asset into thousands of tokens, it becomes accessible to a far wider range of global buyers. An institution holding $50 million in tokenized real estate can sell $100,000 worth of tokens in minutes on a decentralized exchange (DEX), rather than spending months arranging a full property sale. This enhanced liquidity allows institutional crypto managers to optimize their capital efficiency, reducing the "time-to-cash" and making asset allocations far more flexible.

Regulatory Clarity and Compliance

One of the biggest hurdles for established financial institutions entering the crypto space is navigating ambiguous global regulations regarding native crypto assets. Many traditional investors, constrained by strict internal mandates, can only hold assets that qualify as registered securities or follow recognized asset standards.

Tokenized RWAs often fall under existing securities or property laws because the underlying asset is already regulated. The token merely serves as a digital wrapper around a legally compliant investment structure (the SPV).

By working with established tokenization platforms, institutional investors can ensure:

- Know Your Customer (KYC) and Anti-Money Laundering (AML): Access to the tokens can be restricted to verified wallets or accredited investors, fulfilling stringent regulatory requirements crucial for institutional adoption.

- Tax Reporting Simplicity: Since the underlying yield (e.g., rental income or bond coupons) is generated from a legally recognized source, calculating capital gains, income tax, and withholding is often simpler, leveraging existing crypto tax software that integrates RWA data.

This regulatory certainty significantly reduces the compliance risk, making RWAs an appealing, low-friction entry point for institutions wishing to leverage blockchain technology without violating mandates.

Legal and Structural Foundations of Tokenized Assets

The true sophistication of institutional RWA adoption lies not in the technology of the token itself, but in the rigorous legal structures that underpin it. For capital management, trust hinges on the legal guarantee that the digital token truly represents the physical asset.

The RWA Tokenization Platforms (The 'Minting' Process)

RWA tokenization platforms are specialized service providers that handle the complex interplay between legal contracts, custodial services, and smart contract issuance. They are the gatekeepers ensuring institutional-grade compliance.

These platforms manage the full lifecycle of the asset:

- Custody and Verification: They verify the legal title of the asset, often working with third-party fiduciaries (trustees or custodians) who physically hold the asset or the legal deeds on behalf of the token holders.

- Smart Contract Design: They code the smart contracts that govern the token. These contracts dictate rules, such as dividend payout schedules (using the yield generated by the RWA), lock-up periods, and transfer restrictions (e.g., preventing transfer to a non-KYC-verified wallet).

- Ongoing Management: They manage the operational lifecycle, including collecting real-world income (like rent or interest payments) and ensuring those funds are automatically distributed to token holders via the smart contract.

For an institutional investor, choosing a robust, legally sound platform is paramount, as the platform’s governance determines the security and compliance of the entire investment.

Addressing Legal Ownership and Jurisdiction

The central legal challenge of tokenization is the gap between the digital world and the physical world. In most jurisdictions, physical property ownership is still defined by traditional paper deeds and centralized government registries, not by a blockchain entry.

To bridge this, institutional-grade RWA structures rely heavily on the Special Purpose Vehicle (SPV) structure mentioned earlier.

- The SPV's Role: The SPV is the formal, legal owner of the physical asset (e.g., the building). It issues a contractual claim—the token—to investors.

- Trust Law: The SPV is often established in jurisdictions with mature trust and securities laws (like the Cayman Islands, Delaware, or Switzerland). The relationship between the SPV, the trustee (custodian), and the token holders is explicitly defined in legal documents, ensuring that even if the tokenization platform fails, token holders retain their legal claim on the underlying asset.

This layered legal framework—physical asset ownership held by an SPV, governed by a trust, represented by a cryptographic token—provides the necessary safety net for traditional institutional capital to participate.

Handling Compliance and KYC/AML

Institutional investment requires stringent adherence to Know Your Customer (KYC) and Anti-Money Laundering (AML) standards. While many native crypto assets are permissionless and fully decentralized, tokenized RWAs often incorporate permissioned layers to ensure compliance.

For tokens representing regulated securities (like shares in a private credit fund):

- Whitelisting Wallets: The RWA smart contract may be coded to only allow transfers between crypto wallets that have been verified and whitelisted by the issuer (the SPV or the platform).

- Geographic Restrictions: The contract can enforce geographic restrictions, preventing tokens from being traded in jurisdictions where they are not legally registered.

This "controlled decentralization" is vital for institutions. It allows them to benefit from blockchain efficiency while satisfying the due diligence frameworks required by their regulators and investors.

Key RWA Use Cases in Institutional Portfolios

RWAs offer institutional investors a massive selection of previously inaccessible yield sources, providing tailored solutions for various capital management objectives, from liquidity preservation to long-term income generation.

Tokenized Real Estate: Fractional Ownership

Real estate is a classic stable asset, known for steady income and inflation hedging. However, its high capital requirement and extreme illiquidity make it inaccessible for many investors and difficult for institutions seeking portfolio flexibility.

Tokenizing real estate allows institutions to:

- Fractionalize Large Holdings: An institution can tokenize a $100 million commercial building into 100,000 tokens, selling off portions as needed to rebalance the portfolio without a full divestiture.

- Global Access: The property, located in New York, can be instantly offered to institutional investors in Asia or Europe, dramatically expanding the potential buyer pool.

- Programmable Yield: Rental income collected by the SPV can be converted to stablecoins (USDC, USDT) and automatically distributed to token holders' wallets monthly via smart contract, bypassing slow bank wires and administrative costs.

For capital managers, this transforms a rigid, long-term asset into a granular, tradeable income stream.

Tokenized Private Credit and Treasury Management

Perhaps the most actively adopted RWA sector by institutions is tokenized private credit, particularly U.S. Treasury bills (T-Bills). T-Bills are short-term government debt instruments considered among the safest investments globally.

- Stablecoin Reserves: Large stablecoin issuers and corporate treasuries require ultra-safe, liquid assets to back their digital liabilities. Tokenizing T-Bills allows these entities to hold the safety of U.S. government debt directly on-chain.

- Yield Generation: Institutions can earn interest (the yield from the bond) directly in their digital wallets, merging their digital liquidity with traditional safe-haven yield.

- Private Credit Pools: Funds can pool tokenized trade receivables (invoices owed by corporations) or supply chain finance debt. This allows institutional capital to participate in secured, short-duration corporate lending, generating high yield while utilizing the transparency of blockchain technology to track the underlying collateral.

This use case directly addresses the institutional need for yield generation and liquidity preservation, making it essential for managing large pools of operational or reserve digital capital.

Tokenized Commodities and IP

Beyond traditional financial assets, tokenization is expanding into more specialized areas:

- Commodities (Gold, Silver): Tokenized physical gold, where each token is backed by a verifiable quantity of stored metal, offers an inflation hedge that is instantly transferable, unlike traditional physical gold custody.

- Intellectual Property (IP) and Royalties: Institutions investing in entertainment, music, or patents can tokenize the future revenue streams (royalties). A capital manager could invest in a token that entitles them to a percentage of future streaming revenue from a hit song, providing a unique digital asset tied to real-world creative economy performance.

Drivers of Institutional Adoption and Future Trends

The integration of RWAs is not a passing trend; it is a structural shift driven by the persistent institutional demand for operational efficiency and regulatory certainty within the digital asset ecosystem.

Scalability, Efficiency, and Cost Reduction

Traditional asset transfers—especially cross-border—involve multiple intermediaries (brokers, custodians, clearing houses), generating high fees and requiring several business days (T+3 settlement).

Tokenization drastically reduces this complexity:

- 24/7 Global Access: Tokenized assets can be traded immediately, regardless of time zone or weekend closures, accelerating capital deployment.

- Atomic Settlement (T+0): The transfer of the asset (the token) and the transfer of payment (the stablecoin) happen simultaneously within the smart contract. This "atomic settlement" eliminates counterparty risk and drastically cuts operational costs.

For institutions managing massive trading volumes, the speed and efficiency gains offered by RWA tokenization translate directly into millions saved in operating expenses and reduced market risk exposure.

Integrating RWAs into DeFi Protocols

One of the most compelling strategic advantages of RWAs for capital managers is their potential use within the Decentralized Finance (DeFi) ecosystem. DeFi is a vast collection of protocols offering decentralized lending, borrowing, and trading.

While DeFi offers high yields, it traditionally requires over-collateralization with volatile crypto assets. RWAs introduce stable, income-generating collateral.

Use Case: Stable Borrowing: An institutional fund holding tokenized Real Estate (RWA) can use that token as collateral in a DeFi lending protocol to borrow stablecoins (like USDC). Because the underlying asset is highly verifiable and low-volatility, the protocol can offer better loan-to-value ratios than it would for highly volatile native crypto assets. This allows institutions to retain exposure to their RWA holdings while unlocking instant, flexible working capital digitally.

This integration bridges the compliance and stability of TradFi with the efficiency and automation of DeFi, creating sophisticated new opportunities for large-scale capital optimization.

Risk Management Frameworks for RWA Investment

As RWAs mature, institutional due diligence frameworks must evolve beyond standard crypto risk assessment. While native crypto risk focuses on smart contract security and market manipulation, RWA risk focuses on the link to the physical world.

Sophisticated capital managers must analyze:

- Oraclization Risk: How reliably is the real-world data (e.g., property valuation, loan performance) delivered to the blockchain via oracles? Inaccurate data could lead to misplaced trust and devaluation.

- Custodian Risk: Who legally holds the asset, and what are the legal recourse procedures if the SPV or custodian defaults or mismanages the asset?

- Jurisdictional Risk: Are the legal protections in the asset's physical jurisdiction strong enough to enforce the token holder’s rights?

Addressing these complex risks requires institutional-grade expertise, often involving specialized legal counsel and rigorous third-party auditing of both the physical asset and the tokenization smart contract. This focus on verifiable and structured compliance is the final hurdle that will drive widespread institutional confidence in the RWA market.

Conclusion

The tokenization of Real World Assets represents a fundamental evolution in how large capital pools are managed in the digital age. By integrating assets like sovereign debt and real estate directly onto the blockchain, institutions can achieve unparalleled levels of portfolio diversification, liquidity, and operational efficiency.

For crypto novices and new investors, understanding RWAs offers a critical perspective on the future of finance: a future where the stability and regulatory compliance of traditional assets are combined with the speed and transparency of decentralized technology. As tokenization platforms mature and global regulators provide clearer guidance, RWAs will transition from being an emerging trend to a foundational component of modern, sophisticated capital management strategies.