Welcome to the cutting edge of digital asset management. If you’ve mastered the basics of buying and selling crypto (known as ‘spot’ trading), you are ready to explore the systematic, high-speed world of advanced trading. This field moves beyond manually executed trades and focuses on quantitative strategies, automation, and the disciplined use of complex financial instruments called derivatives.

For the novice, the world of high-frequency trading (HFT) and complex portfolio structuring can seem intimidating, full of jargon and intense mathematics. However, the core principles revolve around two simple goals: increasing execution speed and managing risk systematically.

This guide serves as your technical roadmap. We will dissect the difference between common retail trading and institutional-grade algorithmic execution, explore the necessary technological infrastructure (APIs), and introduce the advanced risk models used by professionals to structure robust, systematic crypto portfolios. By the end of this journey, you will possess the foundational knowledge required to transition from a manual trader to a structured, advanced portfolio manager.

Deconstructing Advanced Trading: HFT vs. Traditional Retail Trading

The most fundamental distinction in the trading world is between a human-driven decision process and a machine-driven one. While both are trying to profit from price movements, their methods, timelines, and required technology are vastly different.

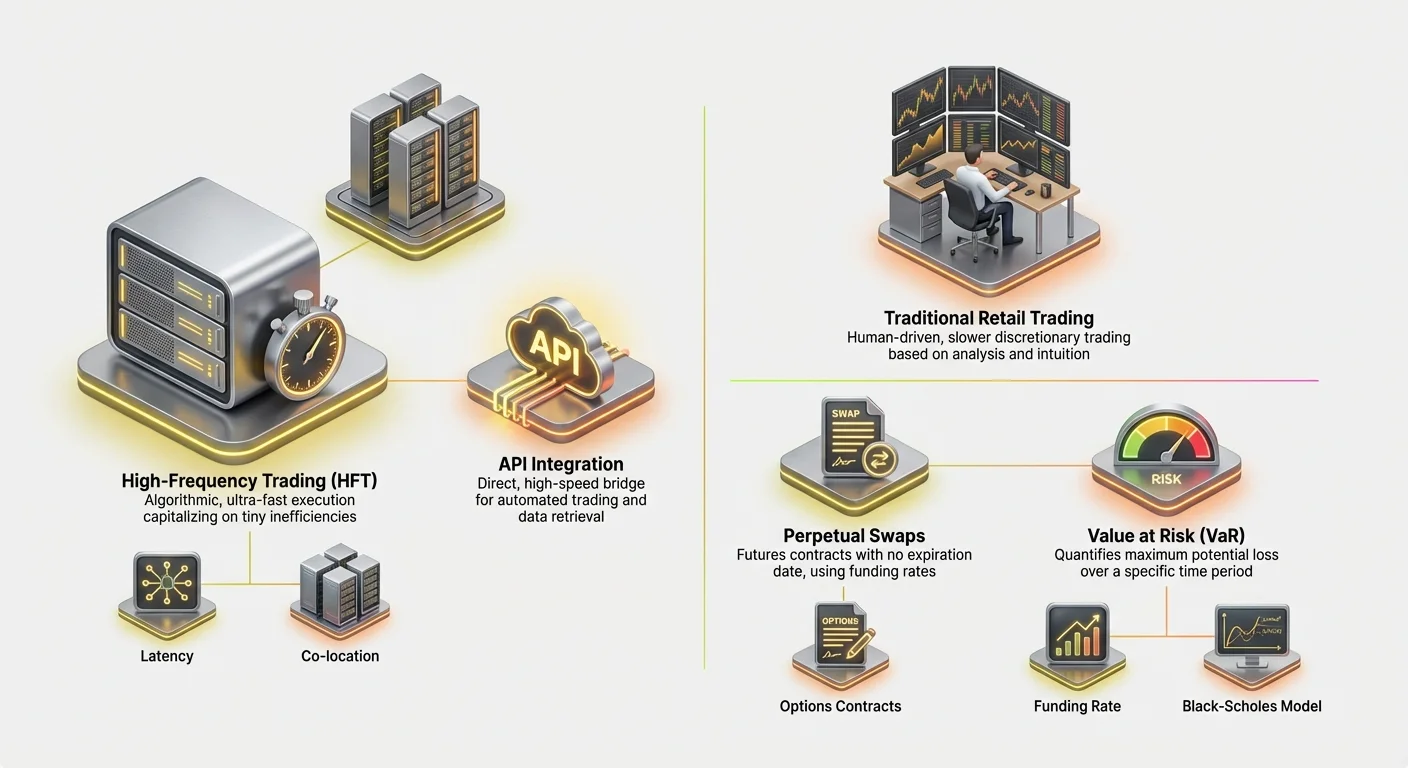

High-Frequency Trading (HFT) Defined

High-Frequency Trading (HFT) is a type of algorithmic trading characterized by extremely short holding periods and high turnover rates. HFT firms utilize powerful computer programs to execute thousands of orders across various exchanges in mere milliseconds.

The goal of HFT is often not to predict long-term market trends, but to capitalize on tiny, temporary inefficiencies in pricing (like minuscule differences in price between Exchange A and Exchange B—a practice known as arbitrage).

Key characteristics of HFT strategies include:

- Speed (Latency): Every microsecond counts. Strategies require direct, low-latency connections to exchanges, sometimes requiring servers physically located near the exchange’s own servers (co-location).

- Volume: HFT strategies execute a massive number of trades, often holding positions for seconds or minutes, aiming for small profits on each trade that accumulate into significant returns over time.

- Complex Algorithms: These systems rely on sophisticated mathematical models to interpret incoming market data (order book depth, transaction speed, volatility indicators) and automatically generate executable orders.

Day Trading and Swing Trading: The Manual Approach

In contrast, traditional retail trading methods, such as day trading and swing trading, are typically human-executed, discretionary, and slower.

Day Trading involves opening and closing positions within the same trading day. While fast compared to investing, a day trader’s execution time is measured in seconds or minutes, relying on charting, technical analysis, and human intuition.

Swing Trading involves holding assets for several days or weeks, attempting to capture medium-term price "swings." Both methods rely on a deep understanding of market psychology and chart patterns, but they lack the raw speed and systematic rigor of HFT.

The crucial difference for a beginner to grasp is that high-frequency trading is not just fast day trading; it is a completely different approach based on systemic advantage (speed, technology, and math) rather than discretionary advantage (skill, intuition, and chart reading).

The Critical Role of Speed and Latency

In advanced trading, speed—or lack thereof, known as latency—is a tradable commodity. Latency is the delay between when an event occurs (e.g., a price change) and when your system receives the data, processes it, and sends an order back to the exchange.

In the highly competitive world of crypto derivatives trading, where sophisticated bots are always running, a latency advantage of even a few milliseconds can mean the difference between filling an order at a favorable price and missing the opportunity entirely.

Reducing latency involves optimizing several factors: the code running the algorithm, the physical distance to the exchange servers, and the efficiency of the connection (the API). This technological focus is what truly separates advanced systematic trading from manual retail activity.

The Core Instruments: Understanding Crypto Derivatives

Advanced portfolio structuring relies heavily on financial tools known as derivatives. A derivative is a contract whose value is derived from an underlying asset (like Bitcoin or Ethereum). They allow traders to speculate on price movements or hedge risks without actually owning the underlying asset.

Derivatives are essential to advanced trading because they facilitate leverage, allow for precise short selling, and enable sophisticated risk management strategies.

Futures Contracts: Standardized Speculation

A futures contract is an agreement to buy or sell an asset at a predetermined price on a specified date in the future.

Example: If you buy a three-month Bitcoin futures contract at $70,000, you are obligated to purchase Bitcoin at $70,000 when the contract expires, regardless of whether the market price is $65,000 or $75,000 at that time.

Futures contracts are highly standardized and traditionally used for hedging (e.g., a Bitcoin miner selling futures to lock in the price of their production) or pure speculation. Since they are settled on a fixed date, advanced traders must constantly manage the rollover risk—the cost and hassle of closing an expiring contract and opening a new one.

Perpetual Swaps: Futures Without Expiration

The perpetual swap (often just called "perpetuals" or "perp futures") is the dominant derivative instrument in the crypto world. Its structure is identical to a traditional futures contract with one critical difference: it has no expiration date.

This feature makes perpetual swaps incredibly appealing for leverage trading and algorithmic strategies because traders do not have to worry about rolling over positions.

To keep the price of the perpetual swap tethered to the current spot price of the asset, exchanges use a mechanism called the Funding Rate.

- The Funding Rate Mechanism: Every few hours (e.g., every eight hours), traders holding perpetual contracts either pay or receive a small fee based on the difference between the perpetual contract price and the spot price.

- If the perpetual price is higher than the spot price (meaning more people are long), long position holders pay a fee to short position holders.

- If the perpetual price is lower (meaning more people are short), short position holders pay a fee to long position holders. The funding rate is the primary mechanism advanced strategies use to exploit price discrepancies and manage systematic risk, forming the basis for cash-and-carry or basis trading strategies.

Options: Managing Risk and Buying Choice

Options contracts give the buyer the right, but not the obligation, to buy or sell an asset at a set price (the strike price) on or before a certain date.

- Call Options: Give the holder the right to buy the asset. Traders buy calls if they expect the price to rise.

- Put Options: Give the holder the right to sell the asset. Traders buy puts if they expect the price to fall (or to hedge an existing long position).

Options are crucial in advanced portfolio structuring because they allow traders to manage volatility and define their maximum risk exposure precisely. For a fixed premium (the cost of the option), a trader can cap their downside risk while retaining unlimited upside potential—a form of insurance for their portfolio.

Building the Engine: API Integration and Execution

To execute high-frequency strategies, you cannot rely on a website interface. The engine of advanced trading is the Application Programming Interface (API)—a technical bridge that allows your custom software to communicate directly with the exchange’s trading servers.

What is a Trading API and Why is it Necessary?

Think of the exchange website as a manual typewriter, and the API as a direct, high-speed fiber optic cable. The API allows your custom algorithms to:

- Retrieve Data: Pull real-time market data (order books, last trades, price history) faster than a human could refresh a screen.

- Manage Accounts: Check balances, margin requirements, and open positions.

- Execute Trades: Send complex orders (limit, stop-loss, take-profit) to the exchange instantly.

For HFT, the API is essential because it eliminates the latency associated with web browsers and allows for automated decision-making.

Best Practices for API Security and Resilience

API access is akin to handing over the keys to your trading account. Security and reliability are paramount.

1. Robust Key Management

When you generate API keys on an exchange, you receive a Public Key (used for identification) and a Private Key (used for signing transactions).

- Restrict Permissions: Always generate keys with the minimum necessary permissions. If you only need to read market data and place orders, disable withdrawal permissions. This prevents hackers from draining your funds if the key is compromised.

- Secure Storage: Never store API secrets in plain text or directly in your code. Use environment variables or encrypted secret managers (vaults) to protect the private keys.

2. Managing Rate Limits and Errors

Exchanges impose "rate limits"—the maximum number of requests your algorithm can send per second. Exceeding this limit results in errors, which can halt your strategy or cause poor execution.

Advanced traders must build robust error handling into their algorithms to:

- Respect Limits: Track the number of requests sent and slow down if the limit is approached.

- Handle Failures: If an order fails due to a network error or exchange issue, the algorithm must immediately confirm whether the order was actually executed or not (to prevent double-ordering) and attempt reconnection. Resilience is key to surviving high-volatility events.

Execution Strategy: Limit Orders, Market Orders, and Co-location

The API facilitates advanced execution methodologies that go far beyond standard buy/sell actions.

Limit Orders and Order Book Depth

High-frequency traders rarely use simple market orders (orders executed instantly at the current best price), as these incur high fees and can suffer from slippage (getting a worse price than expected). Instead, they rely on Limit Orders (orders placed at a specific price) to act as market makers, adding liquidity to the order book.

Advanced execution systems constantly monitor the order book (the list of current limit buy and sell orders) to determine the ideal placement for their orders, often adjusting them every few milliseconds to stay ahead of the competition.

The Concept of Co-location

For truly ultra-low latency trading, the concept of co-location becomes relevant. This means physically placing the trading server hardware inside or extremely close to the data center where the exchange servers reside. This minimizes the geographical distance data must travel, measured in fractions of a mile, shaving off critical milliseconds of latency that provide an edge in HFT strategies.

While often prohibitively expensive for retail traders, understanding co-location highlights the extreme measures taken in HFT where proximity to the market equals profitability.

Structuring the Advanced Crypto Portfolio

A structured crypto portfolio is not just a collection of assets; it is a systematically managed engine designed to achieve specific risk-adjusted returns through automated strategies. Structuring an advanced portfolio involves defining risk tolerance, correlating assets, and rigorously testing hypotheses.

Defining Alpha and Beta in Crypto Portfolios

In traditional finance, portfolio performance is often broken down into two components:

- Beta (): The portfolio’s exposure to systematic market risk (e.g., how much your portfolio moves when the overall crypto market, represented by Bitcoin, moves). If your portfolio has a Beta of 1.0, it moves exactly with the market. If it is 0.5, it is half as volatile.

- Alpha (): The performance of the portfolio that is independent of the overall market movement. Alpha represents the skill of the trader or the effectiveness of the algorithm.

The Goal of Advanced Structuring: Systematic traders primarily seek to generate Alpha. They aim to create strategies (like arbitrage, basis trading, or market making) that profit regardless of whether Bitcoin is going up or down. A successful HFT portfolio often seeks to be "market neutral"—low Beta—while delivering high Alpha.

Strategies for Diversification and Correlation Management

Diversification is crucial, but simply holding 10 different altcoins is not effective if they all move in lockstep with Bitcoin.

1. Correlation and Regime Shifts

Advanced traders manage correlation—how closely different assets move together. During periods of extreme bullishness (risk-on), most cryptocurrencies tend to have high correlation (they all rise). During crashes (risk-off), correlation also typically spikes (they all fall).

Effective diversification means identifying assets or, more importantly, strategies that perform well when traditional assets perform poorly.

2. Strategy Diversification (The Preferred Method)

In systematic trading, true diversification comes from running multiple, uncorrelated strategies simultaneously, rather than just holding uncorrelated assets.

- Example: A structured portfolio might include:

- Strategy A (Market Making): High-frequency bot providing liquidity for Ethereum/USD. This generates steady fees (Alpha) regardless of major market direction.

- Strategy B (Basis Trading): Algorithm capturing the difference between Bitcoin spot price and its perpetual future price. This strategy is also market-neutral.

- Strategy C (Momentum Trading): A slower algorithm that takes leveraged positions when high-volatility breakouts occur. (Higher Beta exposure).

By combining strategies with different risk profiles and return drivers, the overall portfolio's volatility can be smoothed, and risk concentrated to specific, calculated areas.

Backtesting and Simulation: Proving the Strategy

No advanced strategy is deployed live without extensive testing. Backtesting is the process of simulating a strategy using historical market data to see how it would have performed.

Data Quality is Key

The success of backtesting hinges entirely on the quality and granularity of the historical data. HFT strategies require tick-level data (every price change and order book update) to accurately model execution, slippage, and fees. Using only daily or hourly data will provide a false sense of security.

Parameters and Optimization

Backtesting helps optimize critical parameters, such as:

- Entry/Exit Signals: At what specific price or indicator level should the trade occur?

- Stop-Loss Placement: Where is the maximum acceptable loss?

- Position Sizing: How much capital should be allocated to this specific trade relative to the total portfolio?

If a strategy performs well in simulation across various market conditions (bull, bear, volatile, sideways), it moves closer to live deployment. If it only works during the last six months of a bull market, it is deemed fragile and requires refinement.

Essential Risk Management Frameworks

Risk management is the defining characteristic of a professional advanced trader. Unlike retail trading, where risk is often managed through arbitrary stop-loss placements, systematic trading requires quantitative, mathematical frameworks to measure, allocate, and limit risk across the entire portfolio.

Margin Management and Liquidation Prevention

When using derivatives, especially perpetual swaps, traders employ leverage. Leverage allows you to control a large position with a relatively small amount of capital (known as margin). While leverage amplifies gains, it equally amplifies losses, leading to the risk of liquidation.

Liquidation occurs when the losses on your leveraged position cause your available margin to drop below the required maintenance margin level set by the exchange. The exchange then automatically closes the position to prevent your account balance from going negative, resulting in the total loss of the initial margin placed on that trade.

Advanced risk management involves:

- Dynamic Margin Calculation: Algorithms constantly monitor the portfolio’s current margin level in real-time, calculating the exact price at which liquidation would occur for every open position.

- Cross-Margin vs. Isolated Margin: Understanding whether margin is shared across all open positions (cross-margin, higher risk but more flexibility) or dedicated to a single position (isolated margin, lower risk of total account loss).

- Buffer Allocation: Never trading at maximum leverage. Systematic traders allocate only a fraction of their capital to margin, creating a substantial "buffer" against adverse price movements to ensure the liquidation price remains far from the current market price.

(For detailed calculations, see our related guide: Leverage Trading Mechanics: Calculating Margin, Liquidation, and Risk Ratios)

Value at Risk (VaR): Quantifying Potential Loss

Value at Risk (VaR) is one of the most widely used risk metrics in institutional finance. VaR attempts to answer a crucial question: What is the maximum amount I can expect to lose over a given time period with a certain degree of confidence?

How VaR Works (Simplified)

VaR is usually expressed using two parameters: a time horizon and a confidence level.

Example: A portfolio might have a 1-Day VaR of $5,000 at a 99% confidence level.

This statement means that, based on historical volatility and current market conditions, there is only a 1% chance (or 1 day out of 100) that the portfolio will lose more than $5,000 in a single day.

VaR Implementation in Crypto Portfolios

Calculating VaR for crypto portfolios is complex due to the extreme volatility and "fat tails" (rare, high-impact events) common in the market. Advanced systems use historical simulations (looking at past losses) or mathematical models (like variance-covariance matrices) to estimate VaR.

The primary use of VaR is not to avoid all risk, but to ensure that the allocated risk budget matches the firm’s or individual’s capacity for loss. If the calculated VaR exceeds the acceptable risk limit, the algorithm automatically reduces position sizes or hedges existing exposure.

Understanding Option Pricing: The Black-Scholes Model

While VaR is used for portfolio-wide risk assessment, the Black-Scholes Model is fundamental for pricing options contracts and managing their inherent volatility risk.

The Black-Scholes model uses five primary inputs to determine the fair theoretical price of an option:

- Current Price of the Asset (e.g., BTC spot price)

- Strike Price (The price at which the option can be exercised)

- Time to Expiration (How many days until the option expires)

- Risk-Free Interest Rate (Usually the rate on a short-term government bond)

- Volatility (The expected fluctuation of the asset price, often the most subjective input)

For the advanced trader, Black-Scholes provides the theoretical benchmark. Any difference between the Black-Scholes price and the actual market price of an option represents a potential mispricing opportunity that an algorithm can exploit.

Furthermore, the model helps isolate and manage the famous "Greeks"—metrics that measure the sensitivity of the option's price to changes in the inputs (e.g., Delta measures sensitivity to price changes, Vega measures sensitivity to volatility changes). Systematic options traders use the Greeks to maintain precise, balanced risk exposure.

Navigating the Regulatory Landscape for Derivatives

As crypto trading matures and moves into institutional territory, regulatory compliance becomes a non-negotiable component of advanced portfolio structuring, particularly concerning derivatives.

Regulatory guidelines vary dramatically based on the trader’s location, the location of the exchange, and the specific instrument being traded (futures, options, or perpetual swaps).

Jurisdiction Matters: Why Location Dictates Access

The most significant constraint for advanced trading is geography. Many of the leading, high-liquidity derivatives exchanges are not fully regulated in jurisdictions like the United States.

- US Restrictions: US residents often face restrictions on accessing certain high-leverage perpetual swaps offered by offshore platforms. They are generally limited to US-regulated exchanges (like Coinbase or regulated futures markets like the CME), which may offer lower leverage and different products.

- Offshore Operations: Algorithms designed to capitalize on the high liquidity and lower fees of offshore exchanges must ensure strict compliance with local regulations, often requiring proof of non-US residency or the formation of specialized offshore entities.

For a beginner, the key takeaway is that your legal access to specific derivatives tools and leverage levels is dictated by where you live. Attempting to circumvent these geographical restrictions introduces massive compliance and legal risk.

KYC/AML and Reporting Requirements

Know Your Customer (KYC) and Anti-Money Laundering (AML) checks are standard for virtually all centralized exchanges globally. However, for advanced traders managing large, high-frequency positions, the scrutiny increases:

- Source of Funds: Exchanges may require detailed proof of the source of wealth for traders executing high-volume trades.

- Tax Obligations: Trading derivatives, especially high-frequency volume, results in thousands of taxable events. Advanced traders must use sophisticated accounting software to accurately track profits, losses, and fees to meet tax reporting obligations, which vary widely by country.

- Large Trader Reporting: In some regulated jurisdictions, firms exceeding certain volume thresholds are required to report their trading activity directly to regulatory bodies, providing a full audit trail of their positions.

The Evolving Status of Crypto Derivatives

Regulators worldwide are actively defining whether perpetual swaps, options, and futures contracts based on cryptocurrencies should be classified as securities, commodities, or unique digital assets.

This classification is crucial because it determines which regulatory body has jurisdiction (e.g., the SEC or the CFTC in the US). Systematic traders must remain agile, as sudden regulatory shifts can immediately impact the products available, the leverage permissible, and the fees charged by exchanges.

The successful advanced trader builds strategies with sufficient flexibility to adapt quickly to changing legal landscapes, ensuring that the technology and capital allocation models can be seamlessly ported to new, compliant venues if necessary.

Conclusion

The journey from manual retail trader to advanced portfolio structurer is a shift from discretionary decision-making to systematic, quantitative execution. Advanced crypto trading is defined by its reliance on technology, specifically high-speed API integration, and its disciplined use of sophisticated financial instruments like perpetual swaps and options.

To successfully structure a high-frequency portfolio, a trader must master three critical areas:

- Technological Mastery: Ensuring ultra-low latency execution and robust API security to capitalize on speed.

- Quantitative Rigor: Employing risk models like VaR and Black-Scholes to precisely measure and manage portfolio risk exposure.

- Compliance and Structuring: Understanding the impact of leverage, managing liquidation risk, and remaining compliant with evolving international derivatives regulations.

By prioritizing technology, systematic risk management, and the relentless pursuit of Alpha, the modern trader can build robust, automated strategies designed to navigate the highly volatile and complex digital asset markets. This toolkit provides the conceptual roadmap; the next step is applying these concepts to the specific mechanics of derivative instruments and algorithmic strategy implementation.