Bitcoin is frequently discussed in the context of its market performance, often dominating headlines due to its price volatility and rapid appreciation over the last decade. While price attracts attention, it often distracts from the fundamental technological innovation that gives the asset its staying power. At its core, Bitcoin represents a shift in how value is stored, transferred, and secured in a digital environment. It introduces the concept of an asset that is resistant to seizure, censorship, and debasement by central authorities.

This quality of being "unconfiscatable" sets it apart from traditional financial instruments. Money held in a bank account is technically the property of the bank, represented as an IOU to the depositor. That value can be frozen, reversed, or restricted by the institution or government jurisdiction that controls the ledger. Bitcoin operates on a different paradigm. It is a bearer asset, similar to physical cash or gold, but it exists entirely in the digital realm. Ownership is defined not by a bank's permission, but by the possession of cryptographic keys.

The utility of this asset extends far beyond speculation. For individuals living under authoritarian regimes, facing hyperinflation, or dealing with broken banking infrastructure, these properties offer a lifeline. The ability to hold wealth outside of the traditional financial system provides a form of economic insurance. By removing the need for trusted intermediaries, the network creates a system where the rules are enforced by code rather than by human discretion.

The Foundation of Digital Sovereignty

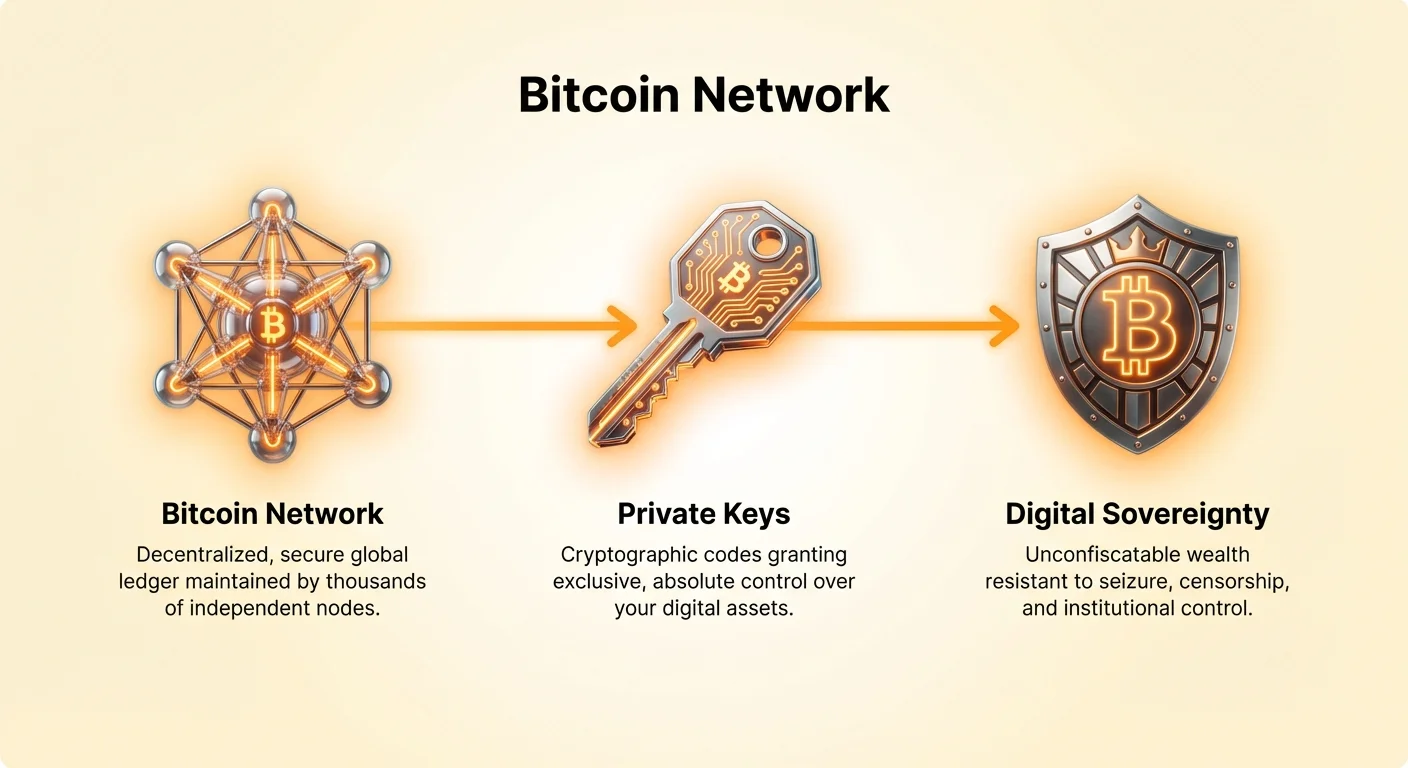

The primary value proposition of Bitcoin lies in its decentralized architecture. Traditional financial systems rely on a central point of authority. A bank, credit card company, or central bank maintains the ledger of who owns what. This central point is efficient, but it also creates a single point of failure. If the central authority is compromised, coerced, or corrupt, the users of that system suffer the consequences. Security in a centralized system depends entirely on trusting the people running it.

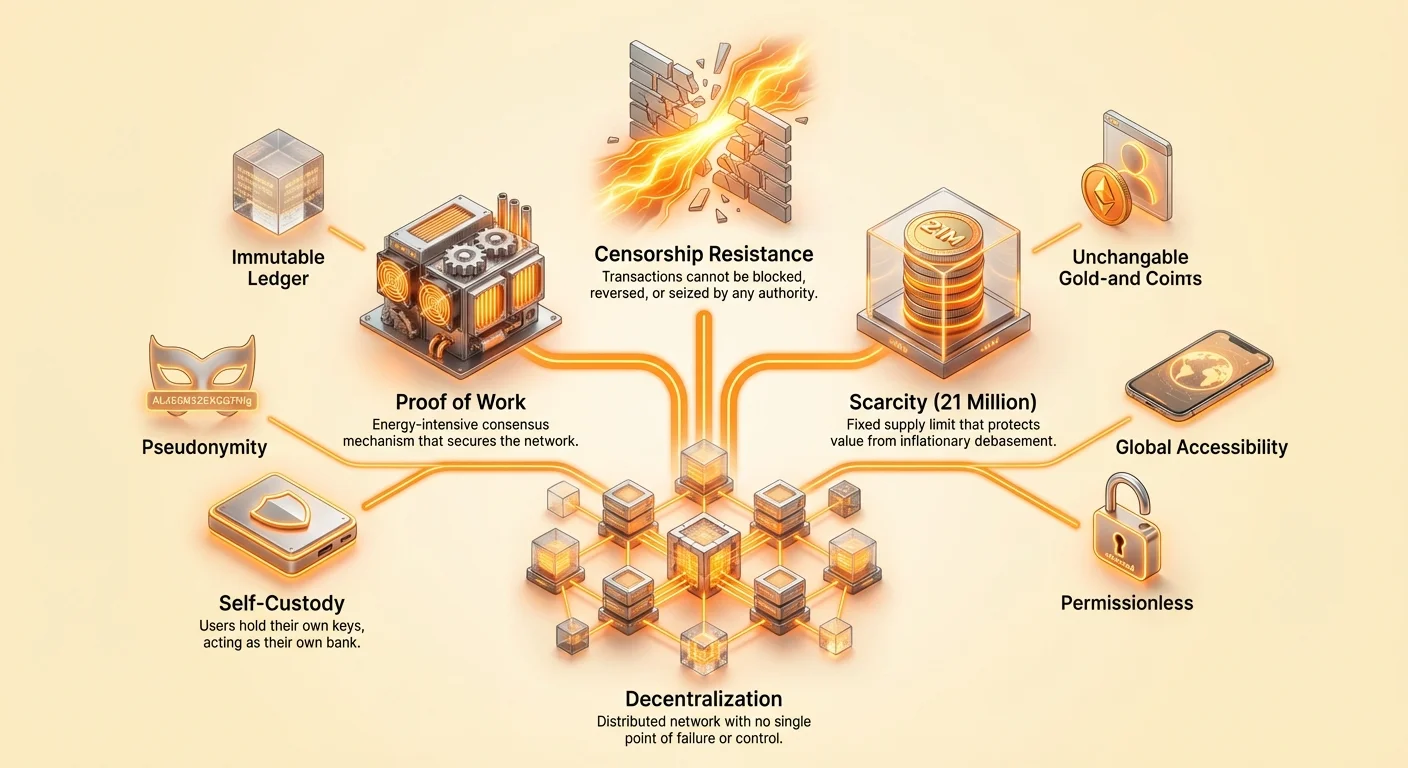

Bitcoin removes this central point of failure by distributing the ledger across thousands of computers, known as nodes, worldwide. Each node maintains a complete copy of the transaction history and independently verifies that every new transaction follows the rules of the protocol. No single entity controls the network. There is no CEO to arrest, no server farm to shut down, and no headquarters to raid. This distribution makes the network incredibly resilient against attacks that would cripple a centralized entity.

This structure creates a "trustless" model. Users do not need to trust a bank to process their transaction honestly. They do not need to trust a government to manage the money supply responsibly. Instead, they trust the open-source software and the mathematical rules that govern the network. These rules are transparent and verifiable by anyone with an internet connection. This shift from institutional trust to verification is a defining characteristic of the asset.

Understanding Censorship Resistance

Censorship resistance is often cited as the most critical property of Bitcoin. In the context of finance, censorship refers to the ability of a third party to preventing a transaction from occurring or to seize assets. In the traditional banking system, censorship is a feature, not a bug. Banks are required to monitor transactions and block those that violate internal policies or government regulations. While this can prevent crime, it also allows for financial exclusion based on political views, geography, or lawful but "high-risk" activities.

Censorship resistance in crypto rests on three pillars. The first is the freedom to transact. On the Bitcoin network, any valid transaction that pays the required fee will be processed by the network. Miners, who secure the network, are incentivized by profit to include transactions in blocks. Even if one miner refuses to process a transaction due to external pressure, another miner in a different jurisdiction is likely to include it to collect the fee.

The second pillar is freedom from confiscation. Because ownership is tied to cryptographic keys rather than an account with a custodian, assets cannot be seized remotely. To take someone's bitcoin, you need their private key. If that key is secured properly, perhaps memorized or stored on a hardware device, the assets are mathematically inaccessible to anyone else. This makes it uniquely difficult to seize compared to real estate, gold bullion, or bank deposits.

The third pillar is the immutability of transactions. Once a transaction is confirmed and buried under subsequent blocks of data, it becomes practically impossible to reverse. There is no "chargeback" mechanism in the protocol. This finality ensures that commerce can occur between strangers without the risk of fraud that plagues traditional credit card payments. It effectively functions as a digital version of handing someone physical cash.

The Mechanics of Unseizability

The concept of self-custody is central to Bitcoin's utility as an unconfiscatable asset. In the traditional world, securing wealth usually means relying on a third party. You trust a vault to hold your gold or a bank to hold your dollars. If that third party fails or is ordered to freeze your assets, you lose access. With Bitcoin, the user has the option to be their own bank. This is achieved through the management of private keys.

A digital wallet does not actually "hold" coins in the way a physical wallet holds cash. Instead, it holds the private keys that allow the user to move coins on the blockchain. These keys are essentially long strings of numbers and letters, often represented as a 12 or 24-word recovery phrase. Whoever possesses this phrase has absolute control over the associated funds. This is why the phrase "not your keys, not your coins" is prevalent in the industry.

This model puts the responsibility of security entirely on the user. There is no customer support hotline to call if a private key is lost. However, it also grants the user absolute sovereignty. A refugee fleeing a war zone cannot easily cross borders with bars of gold or stacks of cash, which are heavy and easily confiscated by border guards. However, they can cross a border with billions of dollars in value simply by memorizing a 12-word phrase.

Scarcity and Value Preservation

While censorship resistance protects the access to wealth, scarcity protects the value of that wealth over time. History is replete with examples of fiat currencies failing due to hyperinflation. When governments print money to pay off debts or fund spending, the supply of currency increases, and the purchasing power of each unit decreases. This is a form of silent confiscation, where the value of savings is eroded without physically taking the money.

Bitcoin addresses this through a fixed monetary policy enforced by code. There will only ever be 21 million bitcoins. This limit is hard-coded into the protocol and cannot be changed without the consensus of the entire network. New coins are released into circulation at a predictable rate, which is cut in half approximately every four years in an event known as the "halving." This makes the asset disinflationary by design.

This mathematical scarcity draws frequent comparisons to gold. Gold has served as a store of value for millennia because it is durable, divisible, and difficult to produce. Bitcoin mimics these properties but improves upon them in the digital age. It is more portable than gold, more easily verifiable, and has a supply cap that is perfectly known, unlike the unknown total supply of gold in the earth.

The following table compares Bitcoin with traditional stores of value:

| Feature | Bitcoin | Gold | Fiat Currency |

|---|---|---|---|

| Supply Limit | Fixed (21 Million) | Unknown (Physical) | Unlimited |

| Portability | High (Digital) | Low (Physical) | High (Digital/Physical) |

| Verifiability | Instant | Difficult/Slow | Easy |

This scarcity provides utility as a hedge against monetary debasement. As central banks expand their money supplies, assets with fixed supplies tend to appreciate in nominal terms. For investors and savers, Bitcoin offers a way to opt out of a system where currency devaluation is a standard policy tool.

The Role of Decentralized Consensus

The mechanism that keeps Bitcoin secure and decentralized is known as Proof of Work (PoW). This is the consensus algorithm that allows thousands of nodes to agree on the state of the ledger without trusting each other. Miners compete to solve complex mathematical problems using specialized computer hardware. The winner of this competition gets to add the next block of transactions to the blockchain and is rewarded with newly minted bitcoin.

This process is energy-intensive by design. The requirement to expend energy creates a "cost of production" for the asset and makes it prohibitively expensive to attack the network. To reverse transactions or rewrite history, an attacker would need to control more than half of the network's computing power. As the network grows, this becomes increasingly difficult and costly, to the point of being economically unfeasible for even nation-state actors.

Proof of Work is what ties the digital asset to the physical world. It effectively converts electricity into digital security. While this energy consumption is often criticized, proponents argue that it is a necessary expense to secure a global monetary network that requires no central authority. Furthermore, the system increasingly utilizes stranded or wasted energy sources, such as flared natural gas or excess hydroelectric power, turning waste into economic value.

Privacy Nuances in a Public Ledger

A common misconception is that Bitcoin is anonymous. In reality, it is pseudonymous. Every transaction is recorded on a public blockchain that is viewable by anyone. Transactions are linked to addresses—strings of alphanumeric characters—rather than names or email addresses. This offers a baseline level of privacy, as a user's identity is not immediately visible on the ledger.

However, this privacy is fragile. If a user's real-world identity is ever linked to their Bitcoin address, their entire financial history associated with that address becomes visible. This linkage often happens at the "on-ramps" and "off-ramps" of the ecosystem, such as centralized exchanges that require Know Your Customer (KYC) verification. Once an exchange knows that a specific address belongs to a specific person, that privacy is compromised.

Sophisticated blockchain analysis firms work with governments and corporations to track the flow of funds. They analyze patterns to identify users and trace coins. To maintain privacy, users must employ specific best practices. This includes avoiding address reuse, using privacy-focused wallets, or utilizing tools like coin mixers that obscure the trail of funds.

Despite these challenges, the network remains more private than the traditional banking system. In the legacy system, the bank and the government have a complete view of all transaction activity. With Bitcoin, the user has control over what information they reveal. Privacy is possible, but it requires active effort and understanding of the technology.

Comparisons with Traditional Finance

When analyzing the utility of Bitcoin, it is helpful to contrast it with fiat currency and other digital assets. Fiat currencies, such as the US Dollar or Euro, are issued by government decrees. Their value is derived from trust in the issuing government and its economy. While fiat is excellent for daily commerce due to its stability and wide acceptance, it is a poor store of value over long time horizons due to inflation.

Bitcoin serves a different purpose. It acts as a settlement layer. It is often slower and more expensive to use for small purchases compared to a Visa swipe, but it offers finality that credit cards cannot. A credit card transaction can be reversed weeks later; a Bitcoin transaction is final within an hour. This makes it superior for large, international settlements where trust between parties is low.

Compared to other cryptocurrencies like Ethereum, Bitcoin's design philosophy is distinct. Ethereum is designed as a platform for decentralized applications and smart contracts. It is a "world computer" that prioritizes programmability. Bitcoin prioritizes security and sound money characteristics. Its code is intentionally rigid and difficult to change to preserve its stability. While Ethereum behaves like a tech stock or a utility platform, Bitcoin behaves more like digital gold or base money.

The Cost of Security

The environmental impact of the network is a frequent topic of debate. Critics point to the total energy consumption, which rivals that of small countries. However, energy consumption must be weighed against the utility provided. The network provides a secure, permissionless financial system available to anyone on the planet. The energy used is the cost of maintaining that security without a central authority.

It is also important to distinguish between energy consumption and carbon emissions. The network seeks the cheapest electricity available. Often, this leads miners to renewable sources like hydro, wind, and solar, which are often located in remote areas where supply exceeds local demand. In these cases, mining acts as a buyer of last resort for renewable energy producers, potentially making green energy projects more economically viable.

Furthermore, the traditional financial system also consumes vast amounts of energy. This includes the power required to run bank branches, corporate headquarters, data centers, and the transportation of cash and employees. The difference is that Bitcoin's energy usage is transparent and easy to measure, while the traditional system's footprint is opaque and distributed across many sectors.

Accessibility and Inclusion

One of the most profound utilities of the asset is its permissionless nature. To open a bank account, a person needs identification, proof of address, and the approval of the bank manager. Billions of people globally lack these documents or live in regions with underdeveloped banking infrastructure. These "unbanked" populations are effectively shut out of the global economy.

Bitcoin requires none of this. All that is needed is a smartphone and an internet connection. A user can download a wallet app, generate an address, and begin transacting in minutes. This lowers the barrier to entry for financial participation. It allows a freelancer in a developing nation to receive payment from a client in Europe without losing a large percentage to remittance fees or waiting days for a wire transfer to clear.

This accessibility also promotes democracy and human rights. Activists and NGOs operating in hostile environments have used the network to receive funding when their bank accounts were frozen by the government. By providing a parallel financial rail that is open to all, the network acts as a check on financial power and a tool for economic freedom.

The Future of Digital Property

As the network matures, its utility continues to evolve. Layer 2 solutions, such as the Lightning Network, are being developed to address scalability. These layers allow for instant, nearly free transactions by settling them off the main blockchain, while still retaining the security of the base layer. This development could enable Bitcoin to function effectively as a medium of exchange for daily purchases, competing directly with payment processors like Visa.

Innovations are also expanding the types of data that can be anchored to the blockchain. Protocols are emerging that allow for the creation of unique digital assets and tokens on top of the secure Bitcoin network. This expands the scope of the asset from strictly money to a broader settlement layer for various forms of digital property.

However, the core value proposition remains its unconfiscatable nature. As the world becomes increasingly digital, the definition of property rights is shifting. Bitcoin proves that it is possible to own something in the digital realm that cannot be copied, deleted, or taken away by a system administrator. This represents a fundamental change in the relationship between individuals and their wealth.

Conclusion

Bitcoin has evolved from an obscure cryptographic experiment into a global asset class that challenges traditional notions of money and property. Its utility goes far beyond its price action on a trading chart. By providing a decentralized, censorship-resistant, and scarce form of digital money, it offers a solution to the historical problems of inflation, confiscation, and financial exclusion. It empowers individuals to be their own banks, securing their wealth with mathematics rather than institutional trust.

The network's resilience, powered by Proof of Work, ensures that it remains an open and neutral system for global value transfer. While it faces challenges regarding scalability and regulatory scrutiny, its foundational principles remain intact. As users continue to seek alternatives to centralized financial systems, the ability to hold an asset that is truly unconfiscatable becomes increasingly valuable. Bitcoin stands as a technological guarantor of property rights in the digital age.

Bitcoin is the only asset you can truly own, take anywhere, and transfer without asking anyone for permission.