Bitcoin, the first and most valuable cryptocurrency, was designed primarily as a peer-to-peer electronic cash system and a store of value. Its scripting language is intentionally limited to prioritize security and stability, which restricts its ability to support complex smart contracts natively.

However, the rise of decentralized finance (DeFi) on platforms like Ethereum created a demand to use Bitcoin’s massive liquidity in lending, borrowing, and trading applications. This necessity led to the creation of "wrapped" assets and bridging solutions.

These mechanisms allow Bitcoin to be represented on other blockchains, effectively transporting its value across incompatible networks. By locking bitcoin on the main chain and issuing a representative token on a destination chain, users can engage with the broader crypto ecosystem without selling their holdings.

While this innovation unlocks capital efficiency, it introduces significant complexity and risk. The security of these assets no longer depends solely on the Bitcoin network but relies on the bridging architecture, custody models, and smart contracts of the secondary layer. Understanding the mechanics of these bridges is essential for any participant in the multi-chain economy.

The Mechanics of Asset Wrapping

The Two-Way Peg System

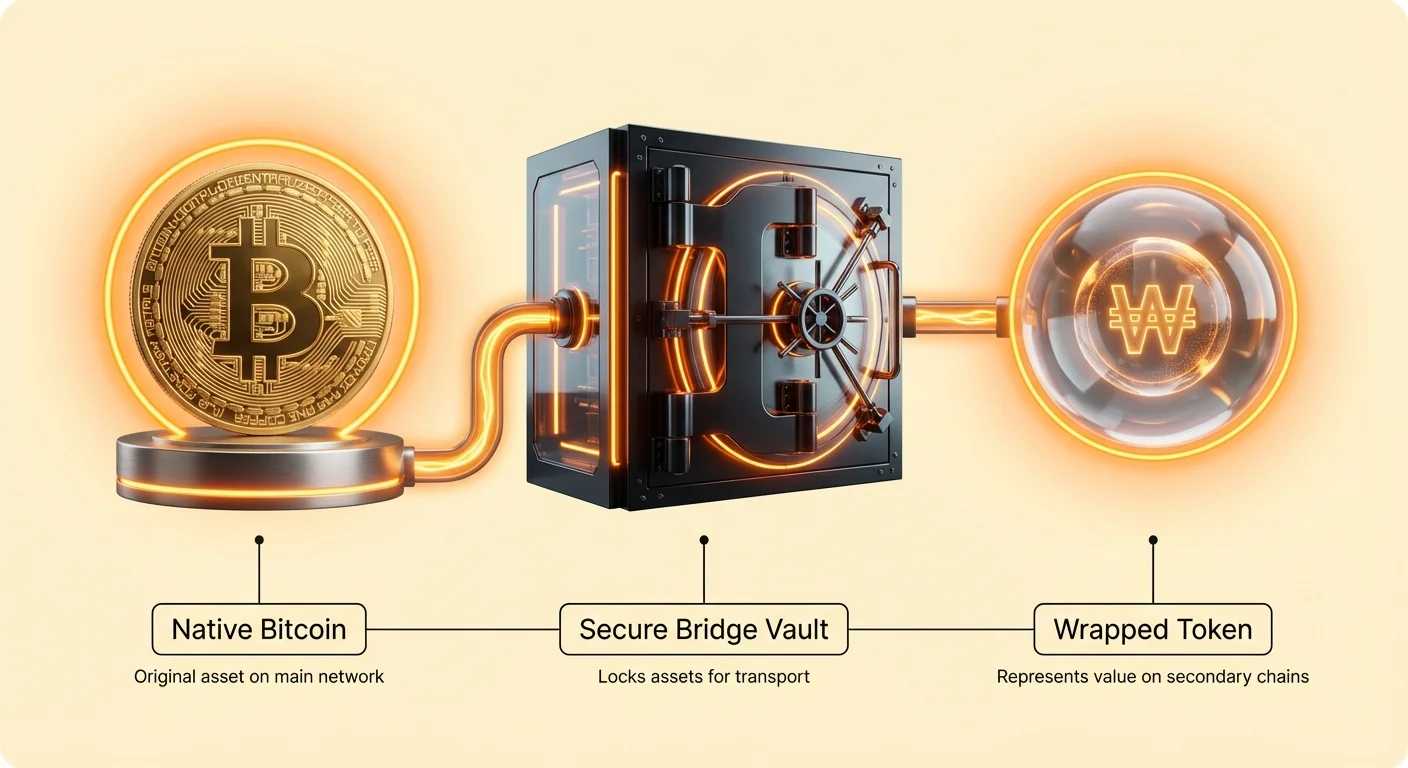

The fundamental technology enabling the transfer of assets between blockchains is known as the two-way peg. Since blockchains are distinct ledgers that cannot directly read or write to one another, the asset does not literally move from one chain to another. Instead, the asset is immobilized on the source chain, and a proxy token is issued on the destination chain.

To initiate a transfer, a user sends bitcoin to a designated address on the Bitcoin network. This address functions as a digital lockbox. Once the transaction is confirmed and the funds are secured, the bridge protocol verifies the deposit. Upon verification, the protocol mints an equivalent amount of tokens on the secondary chain.

These new tokens are legally or algorithmically pegged to the value of the original asset. To retrieve the original bitcoin, the process is simply reversed. The user burns or returns the wrapped tokens on the secondary chain. The protocol detects this action and releases the locked bitcoin back to the user’s address on the main network.

Locking and Minting Protocols

The integrity of a wrapped asset depends entirely on the security of the locking mechanism. If the lockbox on the Bitcoin network is compromised and the backing funds are stolen, the wrapped tokens on the secondary chain become worthless. This creates a critical point of failure that does not exist when holding native bitcoin.

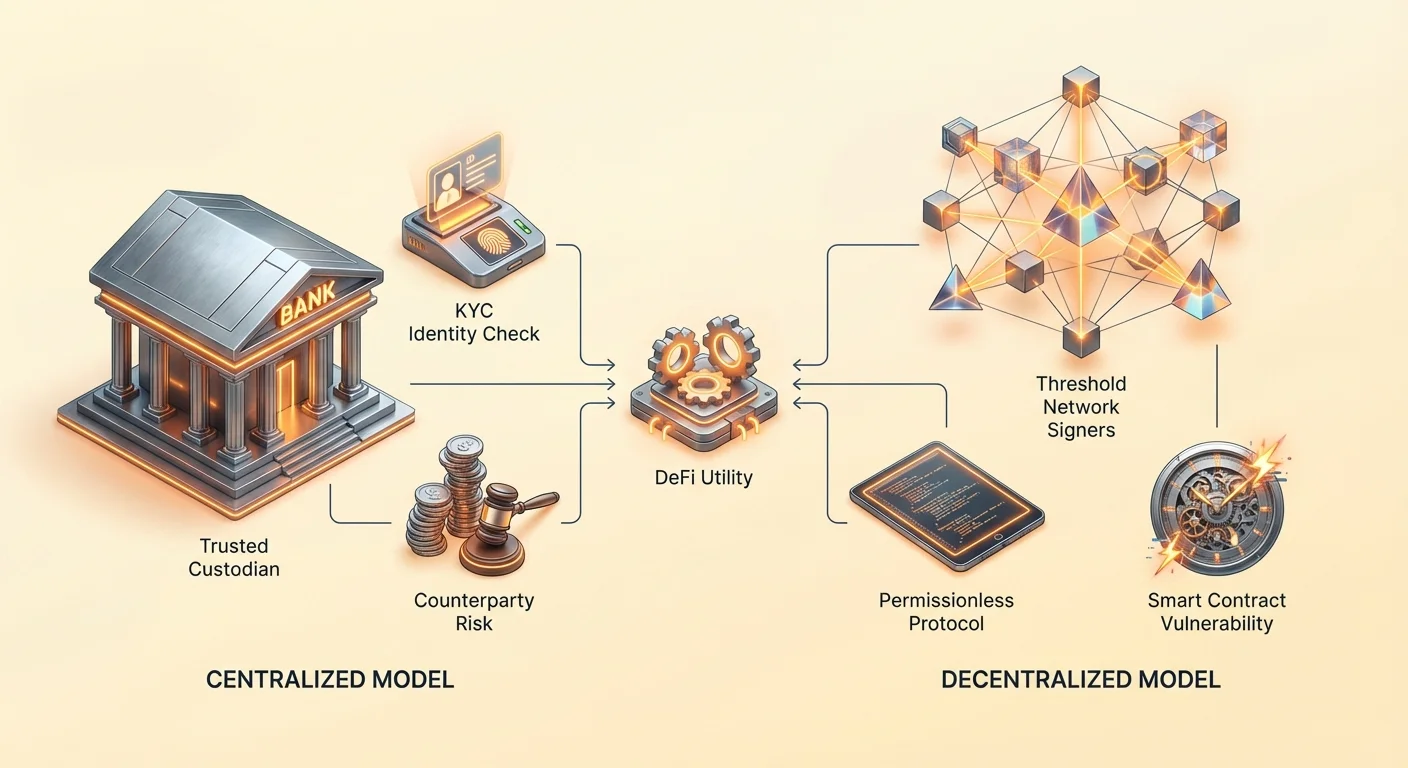

Different protocols handle this locking and minting process in varied ways. Some rely on a single trusted entity to manage the lockbox, while others use a federation of signers or decentralized algorithms. The method chosen determines the level of trust required by the user and the overall censorship resistance of the asset.

In a centralized model, the user must trust that the custodian will not abscond with the funds or freeze the assets due to regulatory pressure. In decentralized models, the risk shifts to code vulnerability and the potential for consensus failure among the network of signers.

Centralized Custody: The WBTC Model

Architecture of Wrapped Bitcoin

Wrapped Bitcoin (WBTC) is the most widely adopted solution for bringing bitcoin to the Ethereum network. It operates as an ERC-20 token backed 1:1 by physical bitcoin held in reserve. The system was designed to bring liquidity to DeFi protocols that require a stable and valuable form of collateral.

The architecture of WBTC is distinctly centralized and relies on a permissioned group of entities to function. It is not a trustless protocol where any user can interact directly with the smart contracts to mint tokens. Instead, it establishes a consortium of trusted partners who manage the supply and custody of the underlying assets.

This model prioritizes efficiency and regulatory compliance over decentralization. By utilizing known entities, WBTC provides institutional investors with a sense of security regarding the legal status of the assets. However, it reintroduces the counterparty risk that Bitcoin was originally designed to eliminate.

The Merchant and Custodian Split

WBTC separates the operational roles into two distinct categories: merchants and custodians. This separation of duties is intended to create checks and balances within the centralized system. Merchants are the user-facing entities that handle the distribution and collection of tokens.

To mint WBTC, a user must go through a merchant. The merchant performs Know Your Customer (KYC) and Anti-Money Laundering (AML) checks on the user. Once the user’s identity is verified, they transfer bitcoin to the merchant. The merchant then initiates a transaction with the custodian.

The custodian is the entity that actually holds the keys to the Bitcoin wallets. Upon receiving the bitcoin from the merchant, the custodian mints the equivalent amount of WBTC on Ethereum and sends it to the merchant. The merchant then transfers the WBTC to the user.

This structure means that users never interact directly with the custodian or the smart contracts. They are dependent on the merchant to facilitate the swap. Furthermore, the custodian holds the ultimate power over the backing assets, creating a single point of failure if the custodian’s keys are compromised or if they act maliciously.

Decentralized Bridging: The tBTC Protocol

Minimizing Trust Through Code

In contrast to the centralized model, tBTC (Threshold Bitcoin) aims to provide a permissionless and decentralized alternative. It is built on the premise that users should not have to trust a company or a legal entity to access their funds. Instead, tBTC relies on mathematics and game theory to secure the bridge.

tBTC allows anyone to mint tokenized bitcoin on Ethereum without undergoing KYC checks or relying on a middleman. The protocol replaces the centralized custodian with a dynamic network of node operators. These operators work together to secure the deposited bitcoin using threshold cryptography.

This approach aligns more closely with the ethos of the blockchain industry. It seeks to extend the censorship resistance of Bitcoin into the DeFi ecosystem. By removing the need for permission, tBTC ensures that the bridge remains open to all users, regardless of their geographic location or identity.

Threshold Signatures and Signer Groups

The core technology behind tBTC is the use of threshold signatures. Instead of a single private key controlling a Bitcoin wallet, the key is mathematically split into multiple shares. These shares are distributed among a group of node operators on the Threshold Network.

To move the locked bitcoin, a specific subset or "threshold" of these operators must agree to sign the transaction. No single operator has access to the full private key, meaning no single person can steal the funds. The signers are selected randomly from a large pool of stakers who have provided collateral to participate in the network.

The randomness of signer selection is critical. It prevents malicious actors from coordinating to take control of a specific wallet. Furthermore, the system rotates signers and wallets periodically, a process known as sweeping. This limits the exposure of any single group of signers and ensures that the security of the funds is constantly refreshed.

Comparing Trust and Security Models

| Feature | Centralized Model (e.g., WBTC) | Decentralized Model (e.g., tBTC) |

|---|---|---|

| Custody | Single entity or small federation | Distributed network of nodes |

| Access | Permissioned (KYC required) | Permissionless (No KYC) |

| Backing | 1:1 Physical Bitcoin | 1:1 Bitcoin + Node Collateral |

| Transparency | Proof of Reserves (Trust based) | On-chain verifiable |

| Risk Type | Counterparty/Regulatory | Smart Contract/Technical |

| Minting Speed | Slower (Manual processing) | Faster (Automated) |

Evaluating Counterparty Risk

When choosing between bridging solutions, the primary consideration is often the nature of the risk the user is willing to accept. In centralized models, the primary risk is counterparty failure. This refers to the possibility that the custodian could go bankrupt, be hacked, or face government seizure of assets.

If a major custodian fails, the legal recourse may be slow and uncertain. Users hold a token that is a claim on an asset, but they do not hold the asset itself. If the backing bitcoin is lost, the token on the secondary chain loses its peg and becomes valueless.

Decentralized models mitigate this specific risk by removing the single counterparty. There is no CEO to arrest and no headquarters to raid. However, this does not eliminate risk entirely; it merely shifts it to a different domain.

Assessing Technical Vulnerabilities

The risks in decentralized systems are primarily technical. These protocols rely on complex smart contracts and cryptographic primitives to function. If there is a bug in the code or a flaw in the economic incentives, the system can fail.

Smart contract exploits have historically been a common vector for attacks in the DeFi sector. If a hacker finds a vulnerability in the minting logic or the signature scheme, they could potentially drain the funds without needing to compromise any physical location or person.

Additionally, decentralized systems rely on the honesty of the majority of the network nodes. While mechanisms like over-collateralization and slashing are designed to punish bad behavior, extreme market volatility could theoretically undermine these economic security guarantees.

Sidechains and Federated Pegs

The Liquid Network Approach

Sidechains offer another method for scaling Bitcoin and enabling complex functionality. A sidechain is an independent blockchain that runs in parallel to the main Bitcoin network. It has its own consensus mechanism and rules but maintains a bridge to the main chain to allow asset transfers.

The Liquid Network is a prominent example of a Bitcoin sidechain. It utilizes a federated two-way peg. In this system, a federation of functionaries—typically cryptocurrency exchanges and trading desks—manages the locking and unlocking of funds.

This federation operates similarly to a multisignature wallet. A transaction to move funds from the main chain to the sidechain requires the approval of a majority of the federation members. This model offers faster transaction speeds and confidential transactions, features that are not natively available on Bitcoin.

Trade-offs in Federated Security

The security of a sidechain is not derived directly from Bitcoin’s proof-of-work. Instead, it relies on the consensus of the sidechain’s validators or federation. If the federation colludes, they can censor transactions or steal funds.

This means that while sidechains allow for experimentation and scalability, they do not offer the same level of security as the main Bitcoin network. Users must trust the federation members to act honestly.

However, for traders and institutions who need to move large amounts of capital quickly between exchanges, the speed and privacy benefits of Liquid often outweigh the reduced security guarantees compared to mainnet Bitcoin.

Emerging Variations of Tokenized Bitcoin

Exchange-Issued Assets

Major centralized exchanges have introduced their own versions of wrapped Bitcoin to keep liquidity within their ecosystems. For example, tokens like cbBTC allow users to utilize their bitcoin holdings in decentralized finance applications on specific networks supported by the exchange.

These assets function similarly to WBTC but are typically managed by a single exchange entity. The custody is handled internally, and the minting and burning processes are integrated into the exchange’s user interface. This offers a seamless experience for users already within that exchange's ecosystem.

The risk profile here is tied directly to the solvency and operational security of the specific exchange. If the exchange faces insolvency or a security breach, the wrapped assets issued by it could be jeopardized. This creates a "walled garden" effect where the asset's utility is high within the ecosystem but carries specific issuer risk.

Synthetic Bitcoin Implementations

Synthetic assets represent a different approach to bringing Bitcoin exposure to other chains. Instead of being backed by physical bitcoin held in a vault, synthetic bitcoin is backed by other assets—often the native token of the host chain or stablecoins.

Protocols like Synthetix allow users to mint tokens that track the price of Bitcoin using price oracles. These tokens, such as sBTC, maintain their peg through over-collateralization and liquidation mechanisms rather than direct redeemability for BTC.

This model eliminates the need for a Bitcoin bridge entirely, as no actual bitcoin needs to be locked. However, it introduces distinct risks related to oracle failures and collateral volatility. If the value of the collateral crashes rapidly, the synthetic asset may lose its peg.

The Broad Spectrum of Custody Risks

Vulnerabilities in Cross-Chain Bridges

Cross-chain bridges have historically been one of the most vulnerable components of the crypto infrastructure. The complexity of managing state across two different blockchains creates a large attack surface for hackers.

Many high-profile exploits have targeted the smart contracts that manage the lockbox on the source chain or the minting rights on the destination chain. If an attacker can trick the contract into thinking a deposit has been made, they can mint unbacked tokens. Conversely, if they can unlock the real assets without burning the wrapped tokens, they drain the bridge's reserves.

These incidents highlight the importance of rigorous auditing and formal verification of bridge code. Users should be wary of new or untested bridge protocols and consider the track record of the team and the security audits performed.

Regulatory and Censorship Concerns

As the crypto industry matures, regulatory scrutiny on bridging assets has increased. Centralized issuers of wrapped tokens are subject to the laws of the jurisdictions in which they operate. This means they can be compelled to freeze assets associated with illicit activity.

For a user holding a wrapped token, this introduces the possibility that their funds could be rendered unusable if the underlying address is blacklisted. This is a fundamental departure from the censorship resistance of native Bitcoin.

Decentralized protocols aim to mitigate this through privacy technologies and distributed governance, but they too face potential regulatory challenges. The tension between compliance and permissionless access remains a central theme in the evolution of bridging infrastructure.

Future Trends in Interoperability

Layer 2 Integration

The evolution of Bitcoin includes the development of Layer 2 solutions that aim to scale the network while preserving its security properties. Networks like the Lightning Network use state channels to enable instant, low-cost payments without requiring a separate token or a custodial bridge.

While Lightning is primarily for payments, other Layer 2 projects are exploring ways to introduce smart contract functionality directly on top of Bitcoin. This could eventually reduce the need for wrapping bitcoin onto entirely different blockchains like Ethereum.

By building execution environments that settle directly on Bitcoin, developers hope to bring DeFi to the Bitcoin ecosystem natively. This would allow users to lend, borrow, and trade without ever entrusting their coins to a third-party bridge or custodian.

Native Opcode Proposals

Proposals to upgrade Bitcoin’s scripting language, such as OP_CAT, could further enhance the network's ability to verify external events and manage complex covenants. These technical improvements might enable more secure and trust-minimized bridging designs in the future.

If Bitcoin can natively verify proofs from other chains or enforce more complex spending conditions, the reliance on federations and multisig wallets could be reduced. This would pave the way for "trustless" bridges where the security is guaranteed by the Bitcoin protocol itself rather than an external set of validators.

As these technologies develop, the landscape of Bitcoin bridging is likely to shift toward solutions that offer better security guarantees and less friction for the end user.

Conclusion

The ability to bridge Bitcoin to other blockchain networks has fundamentally expanded the utility of the world's largest cryptocurrency. By transforming a passive store of value into an active collateral asset, wrapped tokens like WBTC and tBTC have integrated Bitcoin into the vibrant ecosystem of decentralized finance. This integration allows capital to flow more freely, increasing liquidity and opportunities for yield generation across the entire crypto landscape.

However, this functionality comes at the cost of increased risk and complexity. Whether choosing the regulatory certainty of a centralized custodian or the permissionless innovation of a decentralized protocol, users must trade the absolute security of the Bitcoin mainnet for the utility of the secondary chain. Understanding the nuances of custody models, smart contract security, and peg mechanisms is vital for anyone navigating this interconnected environment.

Bridging Bitcoin transforms idle capital into active liquidity, but requires users to carefully evaluate the security trade-offs involved.