The world of finance is undergoing a fundamental transformation, driven by the transparency and decentralized nature of blockchain technology. For decades, accessing global markets—whether stocks in Tokyo, gold futures in London, or currencies in New York—required specialized accounts, central brokers, and adherence to strict trading hours.

Synthetic assets change this paradigm entirely.

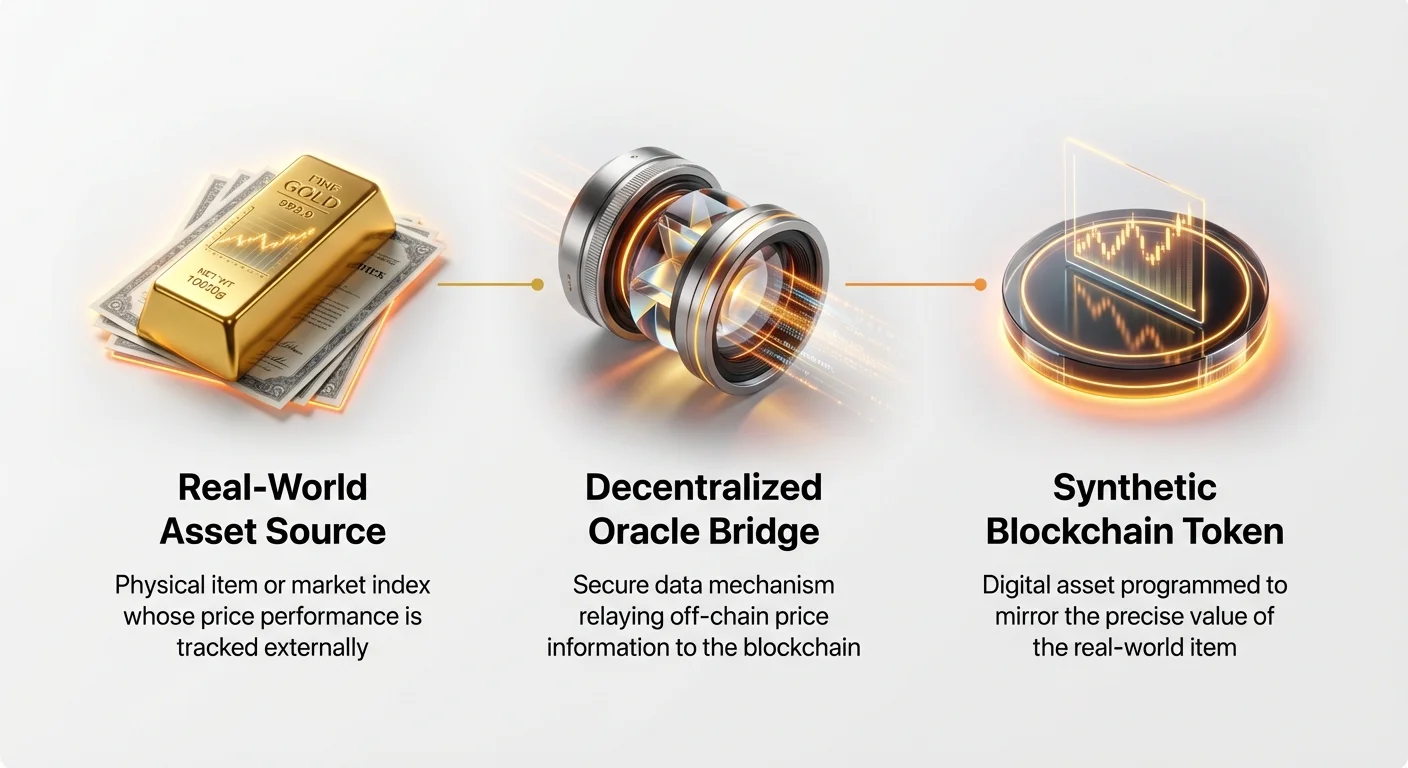

A synthetic asset is essentially a blockchain-based token designed to track or mirror the value of a physical, real-world asset (RWA). Think of it as a crypto proxy for something you can’t physically put on the blockchain, such as a share of Tesla stock, an ounce of silver, or the exchange rate between the Euro and the US Dollar. These assets are built using complex but highly robust Decentralized Finance (DeFi) mechanisms, allowing users 24/7 access to traditional market exposure without ever having to leave the crypto ecosystem.

This guide provides a comprehensive, beginner-friendly exploration of the core mechanics that power synthetic assets, focusing on how these systems maintain their value, manage risk, and ultimately bridge the gap between traditional finance (TradFi) and the decentralized future.

Decoding Synthetic Assets: The Blockchain Mirror

To understand synthetic assets, it helps to first understand what they are not. When you buy a tokenized share of Apple stock (often labeled sAAPL), you do not legally own a fractional share of Apple Inc., nor are you entitled to voting rights or dividends. Instead, you own a blockchain token whose value is programmed to move identically to the actual price of Apple stock on the Nasdaq.

Synthetic assets are purely financial derivatives. They exist to provide price exposure. They derive their value from the performance of an underlying real-world asset (RWA) but are entirely collateralized and managed by smart contracts on a decentralized network.

Definition and Purpose of Synthetic Assets

The primary purpose of synthetic assets is accessibility and interoperability. They unlock traditionally closed markets for crypto users globally, offering censorship resistance and removing geographical barriers.

Synthetic assets are categorized by what they mirror:

- Tokenized Equities (Stocks): Tracking the price of individual stocks (e.g., Google, Amazon) or indices (e.g., S&P 500).

- Tokenized Commodities: Tracking the price of physical goods (e.g., Gold, Oil, Silver).

- Tokenized Currencies (FX Futures): Tracking the exchange rates between fiat currencies (e.g., sEUR/sUSD).

Crucially, because these tokens live on a public blockchain, they can be traded, leveraged, and used as collateral in other DeFi protocols—a functionality traditional derivatives typically lack.

How Synthetics Differ from Traditional Derivatives

While both synthetic assets and traditional derivatives (like futures contracts or Contracts for Difference, or CFDs) allow speculation on price movements, their underlying structures are fundamentally different, especially concerning risk management and custody:

| Feature | Synthetic Assets (DeFi) | Traditional Derivatives (TradFi) |

|---|---|---|

| Issuer/Counterparty | Smart Contracts and the Debt Pool | Centralized Bank, Broker, or Exchange |

| Settlement/Custody | Decentralized, on-chain | Centralized clearing house |

| Trading Hours | 24/7/365 | Tied to specific market hours |

| Collateral | Over-collateralized crypto assets (e.g., ETH, native token) | Cash margin or underlying security |

| Transparency | High (All debt and collateral are public on-chain) | Low (Broker books are private) |

For beginners, the key takeaway is this: Traditional derivatives rely on trust in an institution; synthetic assets rely on trust in audited, open-source code and verifiable collateral.

How Oracles Price Synthetic Assets

The most critical challenge in creating synthetic assets is ensuring the token’s price accurately reflects the real-world asset it tracks. Blockchains are natively closed systems; they cannot "look up" the current price of gold or the US Dollar exchange rate. This is where Oracles come into play.

Oracles are essential middleware—decentralized data feeds that securely retrieve off-chain information and relay it to the smart contracts that govern the synthetic assets. If an oracle fails or provides bad data, the synthetic asset's peg (its link to the real-world price) could instantly break, leading to catastrophic losses.

The Oracle's Critical Function in Pricing

The smart contract that controls the synthetic asset needs a constant stream of reliable data. For instance, if you hold sXAU (synthetic Gold), the smart contract needs to know the exact, up-to-the-second price of physical gold to determine the token's value.

Oracles perform this vital data bridge function. They constantly monitor traditional market exchanges (such as the NYSE, COMEX, or FOREX exchanges) and package that data into a format usable by the blockchain. This data is then used in two primary ways:

- Setting the Initial Minting Price: Defining how much collateral is needed to create a new unit of the synthetic asset.

- Triggering Liquidation: Monitoring the collateral value against the minted asset value to ensure the system remains safe (discussed further in the next section).

The Importance of Decentralized Data Feeds

Relying on a single source for data is incredibly risky. If one entity provides a manipulated or inaccurate price feed, the entire system built upon it becomes compromised. This is why leading synthetic asset platforms utilize decentralized oracle networks (like Chainlink or custom network solutions).

Decentralized Oracle Networks operate through consensus:

- Multiple Nodes: Many independent data providers (nodes) collect the same price data from various premium data aggregators.

- Aggregation: The network averages or weights these multiple data points.

- Consensus: Only when a majority of the nodes agree on a specific price is that price submitted to the blockchain.

This decentralized aggregation makes the pricing data far more robust, difficult to manipulate, and accurate, ensuring that the synthetic asset tracks its underlying value reliably.

Addressing Latency and Pricing Delay

Traditional markets change prices instantly, often many times per second. Blockchains, however, are inherently slower, constrained by block times (the time it takes for a transaction to be confirmed, which can range from seconds to minutes). This creates a latency challenge known as the "oracle problem."

Synthetic platforms manage this trade-off by balancing update frequency with cost. Every time an oracle updates the price on the blockchain, the network incurs a transaction fee (gas). Strategies used to mitigate latency include:

- Deviation Thresholds: The oracle only updates the price when the real-world price has moved by a specific, pre-defined percentage (e.g., 0.5%). This saves on gas fees while ensuring the price remains generally accurate.

- Layer 2 Solutions: Deploying synthetic assets on faster, lower-cost scaling networks (Layer 2s) allows for more frequent and immediate price updates, minimizing the risk of price discrepancies between the synthetic asset and the real asset.

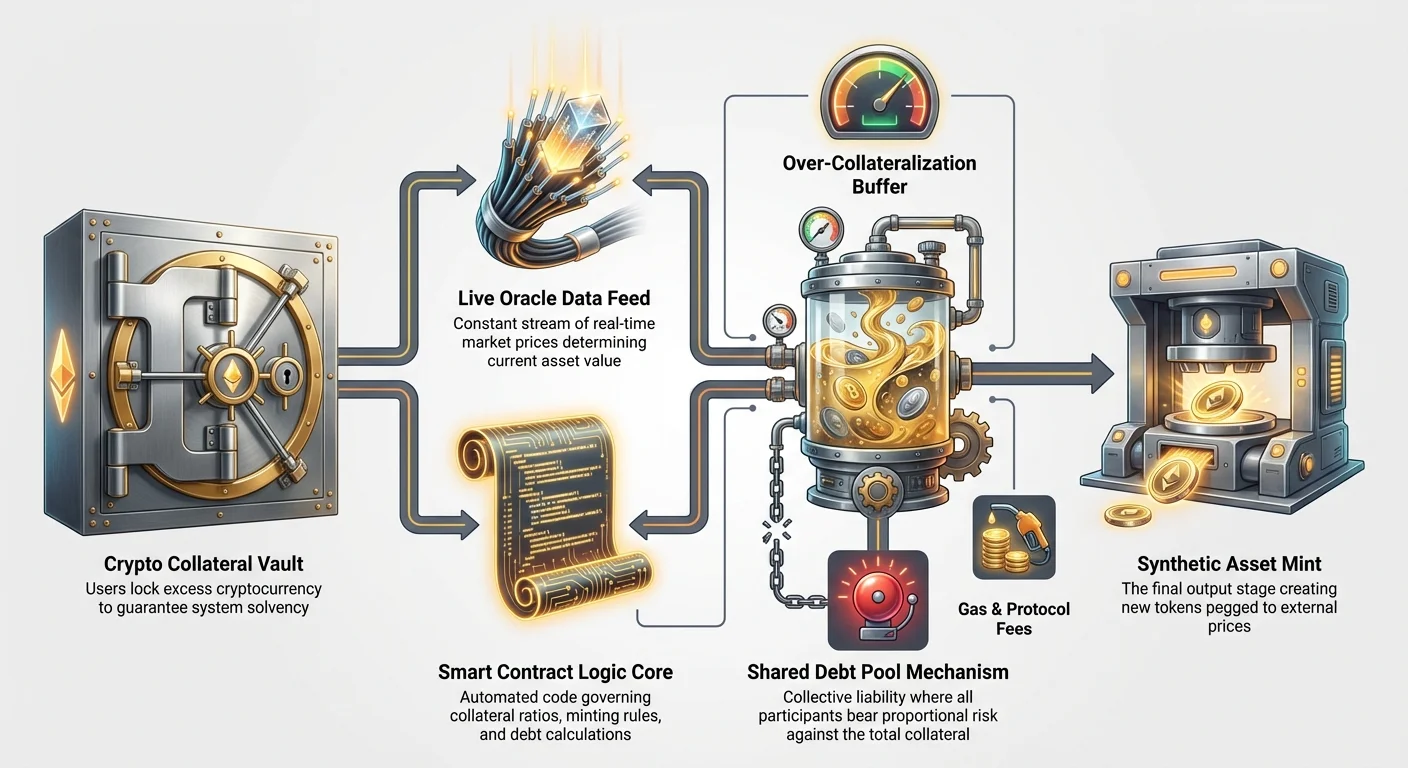

The Engine Room: Collateralization and Debt Pools

The core security mechanism underlying all decentralized synthetic assets is collateralization. Since there is no physical share or physical barrel of oil backing the synthetic token, the system must use crypto assets—typically highly liquid cryptocurrencies like Ethereum (ETH) or the platform's native token—as financial guarantees.

Why Collateral is Necessary (Over-Collateralization)

The process of creating a synthetic asset is often called "minting." To mint $100 worth of synthetic Apple stock (sAAPL), a user must lock up substantially more than $100 worth of crypto collateral. This practice is known as over-collateralization.

For example, a platform might require a Collateralization Ratio (CR) of 400%. This means to mint $100 of sAAPL, the user must lock up $400 worth of ETH.

Why such a high buffer?

- Volatility Buffer: The collateral (ETH) is itself volatile. If the price of ETH drops quickly, the system needs ample time to liquidate the collateral before the debt exceeds the locked value.

- System Solvency: The over-collateralization ensures the system always holds more value locked up than the total value of all synthetic tokens in circulation, guaranteeing that any token holder can eventually cash out.

If the value of the collateral falls below the required minimum CR (e.g., $150 in our example), the smart contract automatically triggers a liquidation, selling off a portion of the collateral to cover the debt and restore the system’s health.

The Role of the Shared Debt Pool

Unlike traditional derivatives, where one counterparty (the broker) directly guarantees the trade, synthetic DeFi platforms often utilize a Shared Debt Pool. This is the most conceptual, and perhaps most crucial, aspect of synthetic asset mechanics.

When a user mints a synthetic asset (e.g., sTSLA), they are effectively taking a financial position against the entire pool of collateral and, by extension, against everyone else who has minted a synthetic asset.

How the Debt Pool Works (Zero-Sum Game):

- Total Collateral Locked: This is the total value of all crypto deposited into the system (e.g., 10,000 ETH).

- Total Synthetic Value: This is the summed value of all synthetic tokens minted (e.g., $40 million in sAAPL, sGOLD, sEUR, etc.).

- The Debt Obligation: When User A mints sAAPL, they are taking on a proportional share of the system's total liability. If sAAPL goes up 10%, User A’s specific debt increases. If sGOLD goes down 10%, User B’s debt decreases.

The beauty of the debt pool is that it is a zero-sum system. If the value of all tokenized stocks goes up, the value of all tokenized commodities or currencies must, proportionally, go down in terms of their standing against the collateral pool. The collective risk is distributed among all minters, ensuring the system remains balanced and solvent.

Minting and Burning Mechanics

The supply of synthetic assets is dynamic and controlled by smart contracts responding to demand and collateral availability.

- Minting (Creation): A user deposits collateral and requests to create a specific synthetic asset (e.g., sEUR). The smart contract checks the CR and, if satisfactory, mints the sEUR token and adds the corresponding debt obligation to the user’s account within the debt pool.

- Burning (Destruction): To retrieve their locked collateral, the user must first "burn" the synthetic asset they hold (or an equal amount of debt if they bought the asset on the open market). Burning removes the asset from circulation and settles the user's outstanding debt against the pool. Once the debt is cleared, the collateral is unlocked and returned.

This constant minting and burning process is what keeps the synthetic supply elastic and the token's price pegged to the real-world asset.

Synthetic Asset Risk Management for Beginners

While synthetic assets offer incredible opportunities for market access and diversification, they introduce unique risks that traditional investors may not be familiar with. These risks largely center on technical mechanics and regulatory ambiguity.

Maintaining the Peg (The Core Financial Risk)

The most immediate financial risk is the de-pegging event. This occurs when the synthetic token’s price drastically deviates from the price of the real-world asset it tracks.

Causes of De-Pegging:

- Low Liquidity: If there are not enough buyers or sellers for the synthetic token, or if the arbitrage opportunities are poor, the market price can drift away from the oracle price.

- Oracle Failure: If the oracle providing the price data fails, provides stale data, or is successfully manipulated, the smart contract relies on bad information, causing the peg to break.

- Market Imbalance: If there is extreme, one-sided trading pressure (e.g., everyone simultaneously trying to sell sOil due to market panic), the underlying collateral mechanisms may be severely stressed, making arbitrage difficult.

Synthetic platforms deploy incentives (e.g., paying higher fees to arbitrageurs) to encourage external traders to buy under-pegged tokens or sell over-pegged tokens, thereby pulling the price back into alignment with the oracle feed.

Liquidation Risk in Over-Collateralization

Liquidation risk is inherent in any leveraged or collateralized system, but it takes on a specific meaning in the context of synthetic assets. You face liquidation risk from two fronts:

- Collateral Asset Volatility: Your collateral (e.g., ETH) might suffer a massive price crash. Even if the synthetic asset you minted (sAAPL) is stable, the value of your locked guarantee asset falls, dropping your CR below the minimum threshold and triggering liquidation.

- Synthetic Asset Price Fluctuation: If you minted sTSLA and its price soars, your total debt obligation to the pool increases rapidly. Even if your collateral (ETH) remains stable, the debt might grow so large that your CR falls too low, forcing liquidation to restore the system balance.

Beginners must actively monitor their CR and deposit more collateral (a process called "topping up" or "re-collateralizing") whenever market movements put them near the mandatory minimum ratio.

Regulatory and Smart Contract Risks

Beyond market mechanics, two major non-financial risks exist:

- Smart Contract Risk: Synthetic assets rely entirely on complex, audited code. A bug, vulnerability, or exploit in the smart contract code—even if unintentional—could lead to the permanent loss of all locked collateral. While audits minimize this risk, they do not eliminate it entirely.

- Regulatory Risk: The legal status of tokenized stocks remains unclear across many jurisdictions. Financial regulators may classify tokenized securities as unregistered securities, leading to platform shutdowns, freezes, or mandated asset unwinding. This is a non-technical risk that must be considered when utilizing synthetics based on traditional equities.

Practical Applications: Accessing Traditional Markets via Tokenized Derivatives

The core value proposition of synthetic assets is providing seamless, borderless access to markets previously restricted by geography or stringent brokerage requirements. For crypto natives, synthetics offer critical tools for hedging, diversification, and arbitrage.

Tokenized Equities and Indices

Tokenized stocks are perhaps the most popular application of synthetics, allowing global access to the world’s largest companies.

Use Case: Portfolio Diversification A user who holds 100% of their wealth in volatile cryptocurrencies (like BTC or altcoins) can use a synthetic platform to mint sSPX (synthetic S&P 500 index). This provides immediate, on-chain exposure to a traditionally stable, diversified index, allowing the user to hedge against crypto volatility without moving any funds back into fiat or opening a traditional brokerage account.

Tokenized equities also enable fractional ownership, making it possible for investors to buy tiny pieces of high-priced stocks (like Amazon or Berkshire Hathaway) that would be cost-prohibitive in traditional markets.

Synthetic Commodities and Currencies (FX)

Synthetic commodities and foreign exchange (FX) are equally transformative, enabling 24/7 exposure to global macroeconomic trends.

Use Case: Hedging Inflation An investor worried about fiat inflation can mint sXAU (synthetic Gold) using their stablecoins as collateral. This allows them to maintain a decentralized position in a traditional inflation hedge, bypassing the physical complexities, storage fees, and limited trading hours associated with physical gold or gold futures contracts.

Similarly, tokenized FX pairs (e.g., sGBP/sUSD) allow traders to speculate on currency movements, facilitating leveraged trading of global currencies directly through DeFi liquidity pools.

Strategic Implementation for Diversification

Synthetic assets are powerful components for building complex, diversified strategies entirely on-chain:

- Long/Short Strategies: A trader can use tokens like sTSLA to go "long" (betting the price will rise) while simultaneously using a tokenized index like sNDX (synthetic Nasdaq) to go "short" (betting the price will fall) via an automated strategy. This ability to mix and match global assets within a single, interconnected ecosystem is unprecedented.

- Yield Generation: Synthetic assets, like any other crypto token, can often be deposited into decentralized liquidity pools or lending protocols, allowing the holder to earn yield on their exposure to traditional markets, a feat impossible with typical brokerage accounts.

Best Practices for Trading Synthetic Assets

Synthetic assets are sophisticated instruments that require meticulous management. Beginners should approach them with caution, prioritizing risk management and education before allocating significant capital.

1. Master the Collateralization Ratio

Always maintain a substantial buffer above the minimum required Collateralization Ratio (CR). If the platform requires 300%, aiming for 400% or 500% provides safety against sudden, unexpected volatility in your underlying collateral asset (e.g., if ETH crashes 20% overnight).

- Actionable Tip: Set internal alerts. Use portfolio tracking tools to notify you immediately if your CR drops to 1.5 times the minimum liquidation threshold, giving you time to top up your collateral before auto-liquidation occurs.

2. Understand Debt Pool Exposure

Remember that when you mint a synthetic asset, you are taking on generalized risk in the entire debt pool, not just the risk of the asset you minted. If you mint a stable asset (like sUSD) but the rest of the pool is heavily skewed toward high-volatility tokenized stocks, those stocks moving wildly can still affect your overall debt obligation and CR.

- Actionable Tip: Research the specific platform's debt pool composition. Platforms focusing solely on commodities may have different risk profiles than those heavily focused on volatile, tech-heavy equities.

3. Verify Oracle Robustness and Security

The system is only as good as the data it receives. Before engaging with a synthetic platform, spend time verifying its oracle infrastructure:

- Does the platform use a decentralized oracle network?

- How frequently does the price feed update, and what is the deviation threshold?

- Are there emergency mechanisms (circuit breakers) in place to halt trading if the oracle data fails?

4. Start Small and Test Arbitrage

Before making a large commitment, mint or trade small quantities of the synthetic asset. Monitor its trading behavior over several days, specifically looking for how tightly the market price adheres to the oracle price. If the token frequently trades far below or above its peg, it indicates potential liquidity or oracle stability problems.

- Actionable Tip: Practice with a demo account or use very small amounts of capital to understand the mechanics of liquidation and debt tracking before committing significant funds.

Conclusion

Synthetic assets represent a crucial evolution in finance, transforming traditional securities into transparent, programmable, and globally accessible blockchain tokens. By leveraging the power of smart contracts, over-collateralization, and decentralized oracle networks, these systems offer a powerful mechanism to bridge the massive liquidity of traditional markets with the speed and efficiency of Decentralized Finance.

For the beginner investor, synthetic assets provide unparalleled opportunities for diversification and hedging, but they demand a deep understanding of their technical underpinnings. Mastering concepts like the Collateralization Ratio and recognizing the critical role of oracles are not optional—they are essential skills for navigating the complex but rewarding world of on-chain tokenized derivatives. As regulation evolves and DeFi infrastructure matures, synthetic assets are poised to become a foundational pillar of the global financial landscape.