Dobrodošli u novo doba digitalnih imovina. Godinama je svijet kriptovaluta funkcionirao uglavnom izvan tradicionalnog financijskog sustava, stekavši reputaciju „Divljeg zapada“. To doba završava. Dok se kripto sazrijeva od nišne tehnologije do imovinske klase vrijedne bilijuna dolara, globalne vlade i regulatorna tijela preuzimaju definiranje pravila angažmana.

Za sofisticiranog investitora, financijskog profesionalca ili ozbiljnog korisnika self-custodyja, razumijevanje ovog promjenjivog regulatornog krajolika više nije opcionalno – to je ključna nužnost za stratešku učinkovitost, upravljanje rizicima i dugoročno sudjelovanje. Ove regulative određuju gdje možete trgovati, kako transaktirati i koje obveze snosite kao nositelj imovine.

Ovaj sveobuhvatan vodič ide izvan jednostavne transakcijske usklađenosti kako bi pružio napredno usmjereno analize ključnih regulatornih okvira koji definiraju budućnost kripta, s posebnim fokusom na smjernice Financijske radne skupine za borbu protiv pranja novca (FATF), prekretnicu Markets in Crypto-Assets (MiCA) regulative u Europi te nadolazeće trenja vezane uz self-custody i decentralizirane financije (DeFi). Ovladavanje ovim regulatornim okruženjem ključ je izgradnje samo-suvereniteta u digitalnoj ekonomiji.

Globalni čuvari: Razumijevanje FATF-a i njegovog mandata

Na temelju gotovo svih globalnih regulacija kriptovaluta leži potreba za sprječavanjem nezakonitih financijskih aktivnosti, prvenstveno pranja novca i financiranja terorizma. Organizacije odgovorne za postavljanje ovih međunarodnih standarda djeluju kao arhitekti usklađenosti diljem svijeta.

Što je Financijska akcijska radna skupina (FATF)?

Financijska akcijska radna skupina (FATF) neovisno je međuvladino tijelo koje razvija i promiče politike za borbu protiv pranja novca (AML) i financiranja terorizma (CFT). Ona sama nije tijelo koje donosi zakone; već postavlja globalne standarde koje se očekuje da njihove članice (koje uključuju većinu glavnih svjetskih ekonomija) implementiraju kroz svoje nacionalne zakone.

Kada FATF izda smjernice, efektivno stvara globalni predložak za regulatorne akcije. Za kripto industriju, smjernice FATF-a bile su transformativne, zahtijevajući od zemalja da tretiraju digitalne imovine i usluge izgrađene oko njih istim strogim mjerama usklađenosti koje se primjenjuju na tradicionalne banke i financijske institucije.

Definiranje pružatelja usluga virtualnih imovina (VASP-ova)

Najutjecajniji korak FATF-a bilo je definiranje kategorije poduzeća podložnih njegovim pravilima: Pružatelji usluga virtualnih imovina (VASPs).

VASP je svaka osoba ili entitet koji provodi jednu ili više sljedećih aktivnosti ili operacija u ime ili za račun druge fizičke ili pravne osobe:

- Razmjena između virtualnih imovina i fiat valuta.

- Razmjena između jedne ili više oblika virtualnih imovina.

- Prenos virtualnih imovina.

- Čuvanje i/ili administracija virtualnih imovina ili instrumenata koji omogućavaju kontrolu nad virtualnim imovinama.

- Sudjelovanje u i pružanje financijskih usluga povezanih s ponudom i/ili prodajom virtualne imovine emitenta.

U praktičnim smislu, ova klasifikacija uključuje centralizirane burze kriptovaluta (CEX-ove) poput Coinbase ili Kraken, čuvare kriptovaluta, brokere i potencijalno čak i određene pružatelje hostanih novčanika. Ključno je da ih kategorizirajući kao VASP-ove, FATF podvrgava ove entitete obvezatnim KYC (Poznaj svog klijenta) i AML zahtjevima.

Ključna uloga IOSCO-a

Dok se FATF strogo fokusira na AML/CFT, drugi ključni igrač je Međunarodna organizacija komisija za vrijednosne papire (IOSCO). IOSCO igra ulogu sličnu onoj globalnog postavljača standarda za tržišta vrijednosnih papira.

Ako se kriptovaluta smatra „vrijednosnim papirom“ (određenje koje varira po zemljama), regulatorni okviri postavljeni od strane IOSCO-a su ključni. IOSCO se fokusira na zaštitu investitora, osiguranje integriteta tržišta i smanjenje sustavskog rizika. Njihove smjernice utječu na to kako se tretiraju stablecoini, DeFi protokoli za zaduživanje i tokenizirane tradicionalne imovine—često zahtijevajući objave prospekta, pravilno upravljanje i pravila protiv manipulacije tržištem.

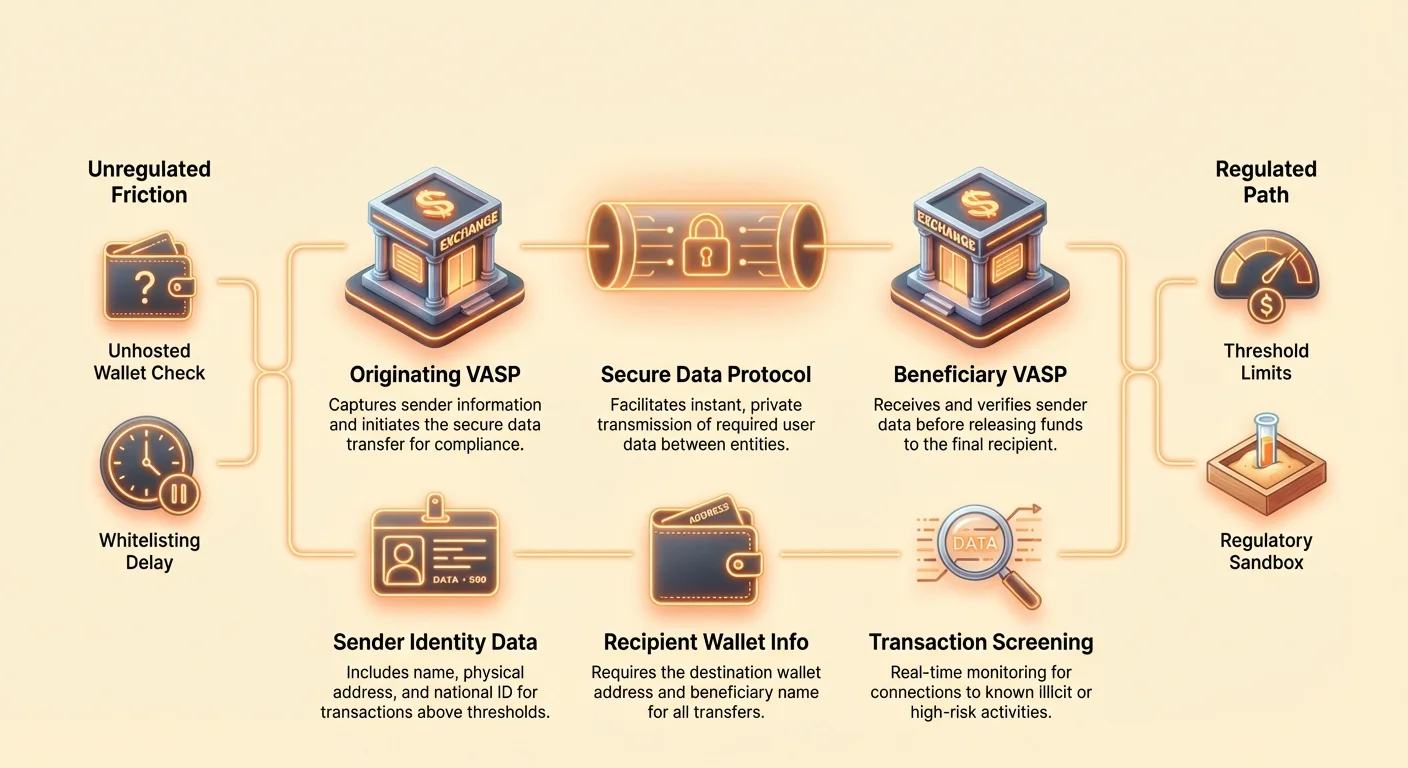

Implementacija globalnog suzbijanja pranja novca: FATF Travel Rule

Jedna najdisruptivnija regulatorna implementacija proizašla iz smjernica FATF-a je Preporuka 16, često nazvana „Travel Rule“. Ovo pravilo dizajnirano je za sprječavanje loših aktera u slanju anonimnih transfera preko VASP platformi.

Dekonstrukcija preporuke 16

Travel Rule zahtijeva od VASP-ova da pribave, zadrže i prenose određene obvezne informacije o podrijetlu i korisniku na protustranu VASP prilikom prenosa digitalnih imovina iznad određenog praga (obično 1.000 ili 3.000 USD, ovisno o jurisdikciji).

Obvezne informacije za podrijetlo (pošiljatelja):

- Ime

- Adresa novčanika

- Fizička adresa (ili jedinstveni nacionalni identifikacijski broj/datum i mjesto rođenja, ovisno o jurisdikciji)

Obvezne informacije za korisnika (primatelja):

- Ime

- Adresa novčanika

Ova regulativa nalaže da kripto transakcije, kada se kreću između reguliranih entiteta, moraju nositi identifikacijske podatke, baš kao i tradicionalni žičani transferi. Namjera je jasna: osigurati praćenje sredstava kroz globalni ekosustav.

Tehnološki izazovi za usklađenost

Travel Rule postavlja ogromne tehnološke prepreke jedinstvene za kripto. Tradicionalni bankovni transferi kreću se sporo (sati ili dani) i koriste uspostavljene, sigurne kanale poruka (poput SWIFT-a). Kripto transferi su trenutni, bez dopuštenja i unakrsno granice po defaultu.

Za usklađenost, VASP-ovi moraju implementirati složene nove protokole sposobne za:

- Identifikacija protustrane VASP-a: Utvrđivanje pripada li primajući novčanik drugom reguliranom VASP-u i ako da, kom.

- Sigurni prijenos podataka: Dijeljenje osjetljivih, osobno identificirajućih informacija (PII) trenutno i sigurno izvan javne blockchain mreže.

- Segmentacija po jurisdikcijama: Rukovanje različitim pragovima i zahtjevima podataka na temelju lokacije VASP-a.

Rješenja poput TRISA (Travel Rule Information Sharing Architecture) i Shyft Networka pojavljuju se za olakšavanje sigurnog, off-chain, peer-to-peer prijenosa podataka između VASP-ova, ali postizanje globalne međusobne kompatibilnosti ostaje ogroman izazov.

Utjecaj na centralizirane burze (CEX-ove)

Za korisnike CEX-ova, Travel Rule značajno mijenja iskustvo isplate. CEX-ovi su obvezni provesti due diligence na adresama odredišta, što dovodi do praktičnih promjena usklađenosti:

- Bijeloliste: Mnoge burze sada zahtijevaju od korisnika da „bijeloliste“ ili registriraju vanjske adrese novčanika (čak i self-custody novčanike) prije isplate velikih iznosa. To često uključuje ručno verifikaciju vlasništva ili objašnjenje prirode transakcije.

- Verifikacija VASP-na-VASP: Ako šaljete sredstva s burze A na burzu B, obje burze moraju razmijeniti PII o vama i primatelju (često vama samom, ako posjedujete oba računa) prije oslobađanja sredstava. Ako primajući VASP ne pruži obvezne podatke, sljučajni VASP može zaustaviti ili odbiti transakciju.

- Isplate na unhosted novčanike: Iako Travel Rule strogo ne sprječava isplate na unhosted novčanike, zahtijeva od podrijetla VASP-a da prikupi detaljne informacije o korisniku koji šalje sredstva i često zahtijeva pojačanu due diligence za transakcije iznad praga.

Praktični vodič za usklađenost s Travel Rule-om za korisnike

Za strateškog kripto nositelja, navigacija kroz Travel Rule zahtijeva pripremu:

- Očekujte kašnjenja: Transferi visoke vrijednosti između CEX-ova, posebno međunarodnih, možda više neće biti trenutni. Planirajte vrijeme za obveznu verifikaciju VASP handshake-a.

- Verificirajte odredište: Ako šaljete sredstva na drugi VASP račun koji posjedujete, osigurajte da primajuća burza podržava protokol usklađenosti s Travel Rule-om korišten od strane pošiljatelja.

- Održavajte dokumentaciju: Čuvajte jasne zapise velikih transfera, posebno kada premještate imovine s CEX-a na svoj self-custody novčanik, jer CEX može zatražiti dokaz da ste korisnik odredišne adrese.

- Svijest o pragovima: Budite svjesni lokalnih pragova Travel Rule-a. Razbijanje velike transakcije na manje, odvojene transfere kako biste izbjegli prag često se smatra „strukturanjem“ i može izazvati regulatornu istragu.

Europe’s Landmark Legislation: The Markets in Crypto Assets Regulation (MiCA)

While FATF provides the framework for global anti-money laundering, the Markets in Crypto Assets Regulation (MiCA) proposed by the European Union is the most comprehensive, jurisdiction-specific legal framework for digital assets yet devised. MiCA is set to fully apply across the EU by late 2024/early 2025 and is acting as a global template for holistic crypto regulation.

MiCA’s Scope and Purpose

MiCA’s primary goal is not just to prevent money laundering, but to establish legal certainty, support innovation, and protect consumers across the entire EU single market. Before MiCA, crypto firms had to adhere to 27 different sets of national laws. MiCA harmonizes these rules, creating a "passporting" system similar to traditional finance, allowing licensed crypto firms to operate across all EU member states with a single authorization.

The regulation covers three major categories of digital assets:

- Asset-Referenced Tokens (ARTs): Tokens backed by several fiat currencies or assets (like a basket of currencies).

- E-Money Tokens (EMTs): Tokens primarily backed by a single fiat currency (like EUR or USD stablecoins).

- Utility Tokens: Tokens intended to provide access to a good or service.

Significantly, Bitcoin and Ethereum (when used as pure decentralized assets without an identifiable issuer) are generally exempted from MiCA’s issuance rules, but the service providers handling them must still comply.

Key Requirements for Issuers and Service Providers

MiCA imposes rigorous requirements on any entity seeking to issue tokens or provide crypto services within the EU:

1. Authorization and Governance

Crypto Asset Service Providers (CASPs—MiCA’s version of VASPs) must obtain authorization from a national regulatory authority. This requires robust governance rules, clear organizational structures, and minimum capital requirements designed to ensure the CASP can withstand operational and market risks.

2. Investor Protection and Disclosure

For token issuers, MiCA introduces requirements for publishing a detailed "crypto-asset white paper." This paper must be filed with regulators, outline the risks, features, and technology, and be presented fairly and accurately. Misleading information could lead to civil liability. This mimics traditional prospectus requirements for securities.

3. Stablecoin Regulation

MiCA imposes stringent rules on stablecoins (ARTs and EMTs), requiring issuers to maintain a legal entity in the EU, hold adequate and liquid reserves (1:1 backing), and undergo regular audits. This regulation is crucial for managing the systemic risks associated with large, widely used stablecoins.

MiCA and Unhosted Wallet Transactions

One of MiCA’s most controversial extensions deals with transfers involving unhosted wallets (sometimes called self-custody or non-custodial wallets). While FATF guidelines recommend VASP reporting, MiCA—along with new, stringent updates to the EU’s Anti-Money Laundering Regulation (AMLR)—has adopted rules that dramatically increase scrutiny:

- Mandatory Identity Verification: Transfers of any amount (zero threshold) between a CASP (e.g., a CEX) and an unhosted wallet must be verified. If a user tries to withdraw funds from a CEX to an unhosted wallet, the CEX must now verify that the user controls that self-custody wallet.

- Enhanced Monitoring: For transfers exceeding €1,000 to an unhosted wallet, CASPs must implement enhanced due diligence and monitoring, including checking the source of funds and the destination address for ties to known illicit activities.

- The "Sunrise Issue": These comprehensive requirements pose significant integration problems, especially concerning the automatic collection of PII, solidifying the regulatory wall between the centralized ecosystem and self-custody.

MiCA and Global Precedent

MiCA is often cited by regulators in the US, UK, Singapore, and other major financial hubs. Its comprehensiveness and pan-national scope make it the de facto global gold standard for balancing innovation with regulation. Countries drafting their own legislation often use MiCA as a starting point, meaning its structure is likely to influence policy worldwide for the next decade.

The Frontier of Friction: Decentralization Meets Compliance

The core tension in crypto regulation exists at the interface between centralized, identifiable institutions (VASPs/CASPs) and decentralized, pseudonymized systems (DeFi, P2P networks, and self-custody wallets). Regulators are adapting their rules to reach into these previously unregulated spaces.

The Regulatory Treatment of Unhosted (Self-Custody) Wallets

An unhosted wallet (like MetaMask, Ledger, or Trezor) is a wallet where the user, and only the user, holds the cryptographic private keys. Regulators view transactions involving these wallets as high risk because they are inherently outside the purview of the regulated VASP ecosystem.

The goal of regulators is generally not to outlaw self-custody, but to prevent it from becoming a funnel for anonymous criminal finance. The key regulatory push, highlighted by MiCA and the enforcement of the Travel Rule, is to make the transfer out of the regulated space subject to severe scrutiny.

Implications for the User: If you routinely transfer large sums from a CEX to your self-custody wallet, expect more intrusive questions about the source of the funds and mandatory, verifiable proof that you own and control the receiving wallet. This creates a compliance burden aimed at deterring actors who wish to "off-ramp" or "on-ramp" anonymously through the decentralized ecosystem.

Challenges for P2P and DEX Activity

Peer-to-Peer (P2P) exchanges and Decentralized Exchanges (DEXs) are the most difficult entities for regulators to capture under the VASP model because there is often no central intermediary.

P2P Exchanges

In pure P2P trading, two individuals transact directly. Since there is no VASP facilitating the exchange, there is no regulated entity to enforce KYC/AML. Regulatory efforts often target the software providers or the interface developers who build the P2P marketplace, attempting to classify them as service providers, even if they never hold custody of the funds.

Decentralized Exchanges (DEXs)

DEXs operate via automated smart contracts. Who exactly is the VASP? The liquidity providers? The protocol founders? The front-end interface operators?

Regulatory focus has shifted to the accessible, centralized elements surrounding the protocol:

- Front-End Regulation: Regulators increasingly target the centralized web interface (the URL) that makes interacting with the DEX easy. If an interface operator restricts access based on geographical location or imposes KYC barriers to use their front-end, they might be classified as a regulated service.

- Gateway Providers: Services that bridge DeFi with traditional finance (e.g., tokenizing real-world assets or providing fiat on-ramps) are clearly VASPs and subject to full compliance.

- Protocol Founders/Developers: If developers maintain significant control over the protocol (e.g., multisig control over treasury funds or upgrade keys), they risk being treated as the regulated entity, forcing them to implement KYC at the protocol level—a concept often antithetical to DeFi principles.

The Impact of U.S. Legislation and Infrastructure

While MiCA sets the framework for Europe, the U.S. approach—often delivered through interpretations by agencies like the SEC and FinCEN—focuses on classifying assets and activities.

The implications stemming from the U.S. Infrastructure Bill, which initially sought to broadly define "broker" to include miners, developers, and protocol operators, illustrate the regulatory intent to cast a wide net. Although the final wording was softened, it signaled a clear future where any party profiting from facilitating crypto transactions will be pressured toward compliance. This ambiguity means that highly sophisticated users must constantly monitor court rulings and agency guidance to avoid legal risk.

Strategic Implications for the Self-Sovereign User

As regulatory scrutiny intensifies, self-sovereignty requires responsible action:

- Audit Your Assets: Understand which of your assets (e.g., stablecoins, utility tokens, governance tokens) might fall under securities laws or MiCA requirements in different jurisdictions.

- Isolate Transactions: Avoid "commingling" funds between wallets used for high-risk DeFi activity (which might later be scrutinized) and wallets used for transparent, compliant interactions with CEXs.

- Compliance Bridge: When moving funds from a regulated CEX to an unhosted wallet, treat the CEX interaction as the required compliance check-point. Ensure the CEX has all necessary KYC/AML data before the withdrawal.

- Understand Jurisdiction: Recognize that using a DEX front-end hosted in a different country does not necessarily shield you from the laws of your own jurisdiction.

Navigating the Future: Regulatory Innovation and Strategic Compliance

The relationship between regulators and the crypto industry is not purely adversarial. Many jurisdictions are actively seeking ways to incorporate blockchain technology while mitigating risks. This approach fosters innovation, legitimacy, and, ultimately, institutional trust.

Regulatory Sandboxes and Innovation Hubs

A "regulatory sandbox" is a defined space where businesses can test innovative products, services, and business models under relaxed regulatory requirements. Regulators oversee these tests, allowing firms to experiment with new technologies (like implementing the Travel Rule on a complex P2P structure) without immediately incurring the full weight of compliance costs.

Value for the Industry:

- De-Risking Innovation: Allows startups to ensure their technology is compliant before a full market launch.

- Regulatory Education: Helps regulators learn how new DeFi protocols function in real-world scenarios.

- Attracting Talent: Jurisdictions with active sandboxes (like the UK, Singapore, or parts of Switzerland) attract innovative firms seeking clear regulatory guidance.

The creation of these sandboxes demonstrates a global recognition that applying century-old banking laws directly to programmable money is impractical, necessitating tailored, innovative compliance solutions.

Compliance as a Competitive Advantage

For sophisticated users and institutional investors, regulation is not merely a hurdle—it is a filtering mechanism that brings credibility. Institutional capital, pension funds, and major corporate treasuries require regulatory clarity and compliance guarantees before entering an asset class.

The implementation of frameworks like MiCA signals market maturity, lowers counterparty risk, and facilitates the creation of audited, regulated financial products (like crypto ETFs or structured derivatives).

Strategic Takeaway: Firms and individuals who embrace and master complex compliance—such as integrating advanced Travel Rule solutions or maintaining meticulous audit trails—will be the first to attract regulated institutional partnerships and capital flow. Compliance shifts from a cost center to a key competitive advantage.

Future Compliance Trends to Monitor

Keeping ahead of the regulatory curve requires tracking specific areas that are likely to evolve rapidly:

- DeFi and AI-Driven Surveillance: Regulators will increasingly rely on sophisticated blockchain analytics and AI tools to monitor DeFi protocols for suspicious activity, focusing less on individual identity and more on the flow of illicit funds. This means protocol interactions linked to high-risk addresses will be flagged, regardless of the user's KYC status.

- Global Harmonization: Expect greater cooperation between FATF member states to standardize the Travel Rule implementation, making seamless VASP-to-VASP communication mandatory worldwide.

- Green Compliance: Following MiCA’s lead, we anticipate greater pressure on crypto service providers (especially mining and staking pools) to disclose and mitigate environmental impact, turning sustainability into a compliance requirement.

- Taxation Integration: Regulatory bodies (like the OECD) are pushing for automated information sharing regarding crypto holdings and transactions. This links the regulatory sphere (KYC/AML) directly to the tax compliance sphere, making comprehensive global tax reporting mandatory.

Zaključak

Prijelaz iz nereguliranog sektora u definiranu financijsku industriju ključan je za dugoročnu održivost digitalnih imovina. Okviri poput FATF-ovog Travel Rule-a i EU-ine MiCA-e predstavljaju fundamentalne promjene, premještajući kripto od nišne anonimnosti prema globalnoj, reguliranoj odgovornosti.

Za ozbiljnog sudionika u kriptu, ovaj dubinski regulatorni uvid naglašava jedinu istinu: samo-suverenitet u digitalnoj ekonomiji postiže se ne izbjegavanjem regulacije, već ovladavanjem usklađenošću. Razumijevanjem ključnih mandata globalnih postavljača standarda, strateškom navigacijom kroz trenja između centralizacije i decentralizacije te usvajanjem naprednih najboljih praksi, korisnici mogu osigurati svoje trajno, sigurno i usklađeno sudjelovanje u budućnosti financija.