The digital economy has shifted from simple value transfer to a complex, programmable ecosystem. At the foundation of this shift lies a collection of technologies often referred to as the decentralized stack. This architecture does not rely on a single server or authority. Instead, it operates through a distributed network of computers that validate and record transactions. This structure fundamentally changes how financial products are built, accessed, and maintained.

In the traditional world, financial services are siloed. Banks, insurance companies, and exchanges operate on closed systems that do not talk to each other. The decentralized stack flips this model. It creates an open environment where applications can interact seamlessly. This interoperability allows for the creation of entirely new financial instruments that were previously impossible.

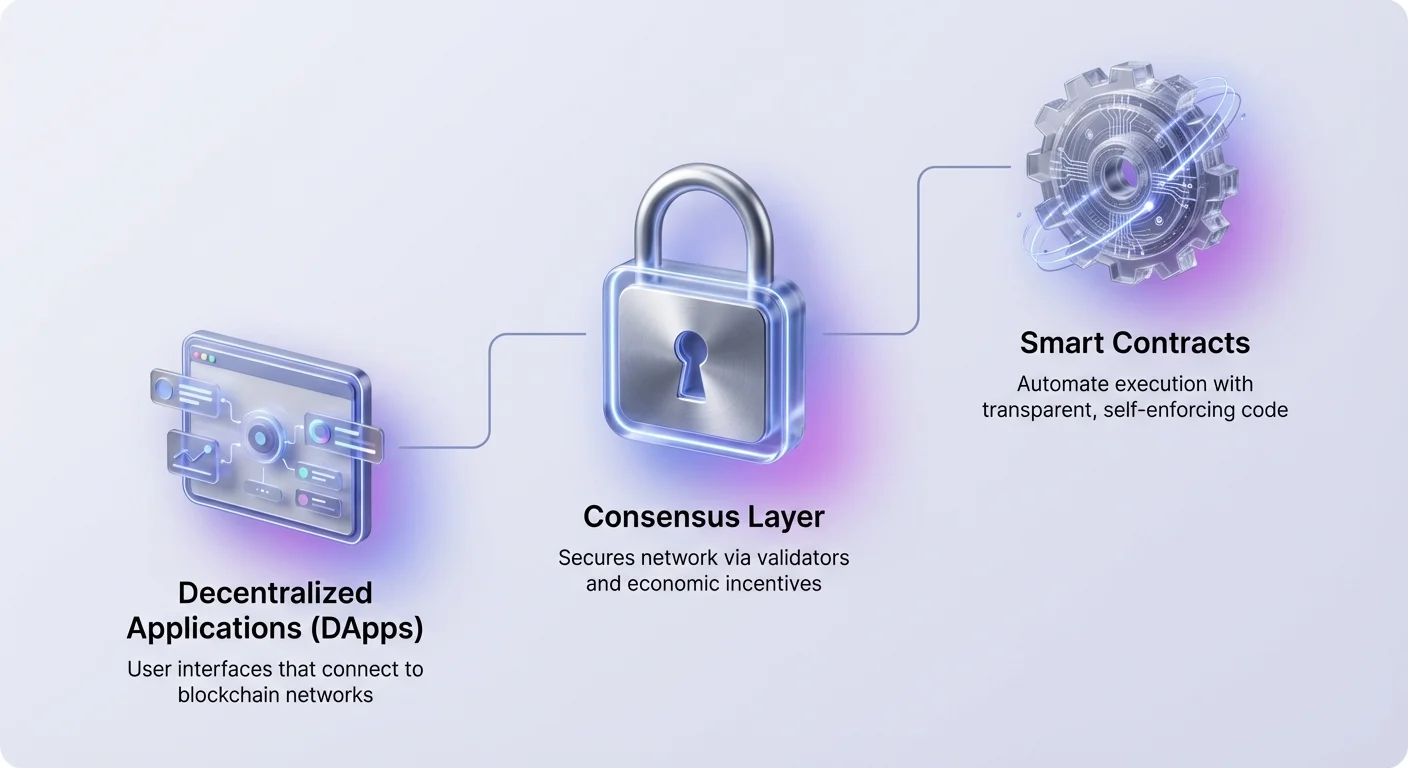

The stack is composed of several distinct layers. At the bottom, consensus mechanisms secure the network. Above that, smart contracts provide the logic for automation. On top, decentralized applications offer user interfaces for interaction. Understanding how these layers function is essential for navigating the modern crypto landscape.

The Foundation of Automation: Smart Contracts

The engine driving the decentralized stack is the smart contract. These are self-executing programs stored on a blockchain that run when predetermined conditions are met. Unlike traditional contracts that require lawyers or notaries to enforce, smart contracts enforce themselves through code. They automate the execution of an agreement so that all participants can be certain of the outcome immediately.

Because these contracts exist on a decentralized network, they are transparent and immutable. Once deployed, the code cannot be altered by a single party. This creates a deterministic environment where users do not need to trust a central authority. They only need to trust the logic of the code itself. This shift reduces counterparty risk and eliminates the need for intermediaries in many financial transactions.

However, the immutability of smart contracts is a double-edged sword. While it prevents tampering, it also means that errors in the code are permanent until a new contract is deployed. This makes the development process critical. Developers must ensure that the logic is sound and free of vulnerabilities before money flows into the system.

The Interface Layer: Decentralized Applications

Users interact with the blockchain primarily through Decentralized Applications, or DApps. A DApp functions similarly to a standard web application but connects to a blockchain network instead of a centralized database. The frontend looks familiar, but the backend logic runs on a distributed network. This architecture ensures that no single entity can shut down the application or censor user access.

To use a DApp, individuals connect a digital wallet rather than creating a username and password. This wallet acts as a passport across the ecosystem. It holds the user's private keys and assets, allowing them to sign transactions and interact with smart contracts directly. This model grants users full custody of their data and funds.

DApps span a wide range of categories. While financial applications are currently the most prominent, the technology supports gaming, social media, and identity management. In every case, the DApp serves as the bridge between the complex code of the blockchain and the end-user. It simplifies the experience while retaining the benefits of decentralization.

Financial Primitives and DeFi Protocols

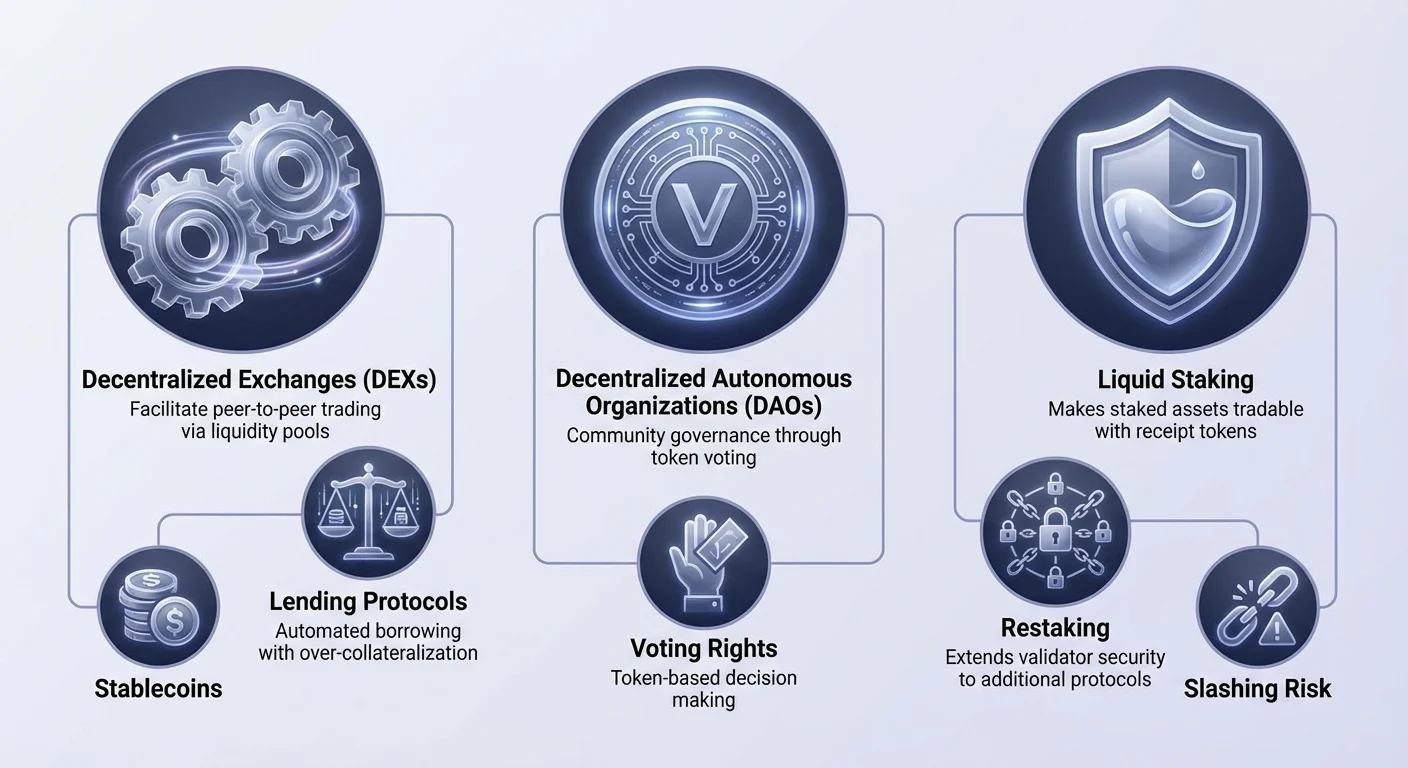

Decentralized Finance, or DeFi, represents the most mature implementation of DApps and smart contracts. It rebuilds traditional financial instruments on open rails. The ecosystem relies on modular "money legos" that can be combined to create complex financial strategies.

Decentralized Exchanges and Liquidity

A core pillar of DeFi is the Decentralized Exchange (DEX). Unlike centralized counterparts, DEXs do not take custody of user funds. Instead, they facilitate peer-to-peer trading through smart contracts. Many DEXs utilize a model known as an Automated Market Maker (AMM).

In an AMM system, traditional order books are replaced by liquidity pools. Users deposit pairs of assets into these pools to facilitate trading for others. In return, these liquidity providers earn a portion of the trading fees. This mechanism crowdsources liquidity, allowing anyone to become a market maker and earn yield on their idle assets.

Automated Lending and Borrowing

Lending protocols have revolutionized access to credit. In traditional finance, obtaining a loan requires credit checks and banking history. In DeFi, the process is permissionless and automated. Users deposit crypto assets into a smart contract to earn interest, while borrowers draw funds against collateral.

To manage risk without a human loan officer, these protocols typically require over-collateralization. For example, a borrower might need to deposit $200 worth of Ethereum to borrow $100 worth of stablecoins. If the value of the collateral drops below a specific threshold, the smart contract automatically liquidates the asset to repay the loan. This ensures the solvency of the lending pool.

Stablecoins and Derivatives

Volatility is a constant in the crypto market. Stablecoins address this by pegging their value to a stable asset, usually the US dollar. They serve as a critical bridge, allowing users to remain in the crypto ecosystem without being exposed to massive price swings. They are the primary medium of exchange within DeFi protocols.

Derivatives and prediction markets extend the utility of the stack further. Users can trade perpetual futures or speculate on real-world events without intermediaries. These markets operate 24/7 and offer global access, removing the geographic restrictions often found in traditional derivatives trading.

Governance Through DAOs

The decentralized stack requires a new method of organization. Decentralized Autonomous Organizations (DAOs) fill this role. A DAO is an entity represented by rules encoded as a computer program that is transparent, controlled by the organization members, and not influenced by a central government.

| Feature | Traditional Corporation | DAO |

|---|---|---|

| Management | Hierarchical | Flat / Distributed |

| Decision Making | Board of Directors | Token Holder Voting |

| Transparency | Private | Public on Blockchain |

In a DAO, governance rights are often tokenized. Holders of the project's native token can vote on proposals, such as protocol upgrades or treasury allocations. The smart contracts then execute the result of the vote automatically.

This structure allows for global coordination without complex legal filings. It aligns the incentives of the community with the success of the protocol. However, it also introduces challenges regarding voter apathy and the concentration of voting power among large holders.

Network Consensus and Staking

Beneath the application layer lies the consensus mechanism. This is the system that secures the network and validates transactions. While early blockchains used energy-intensive mining, modern networks largely rely on Proof of Stake (PoS).

The Evolution of Consensus

Proof of Stake replaces computational work with financial commitment. Validators lock up, or "stake," a certain amount of the network's native cryptocurrency. This stake acts as a security deposit. If a validator acts maliciously or fails to maintain their node, a portion of their stake can be slashed, meaning it is destroyed or confiscated.

This economic model aligns the security of the network with the value of the asset. The more value that is staked, the more expensive it becomes for an attacker to compromise the chain. In return for securing the network, validators receive staking rewards, similar to interest payments.

Validator Responsibilities

Validators are responsible for proposing new blocks and checking the work of others. For most users, running a dedicated validator node is too technical. Consequently, many participate through delegation.

Delegation allows a user to assign their voting weight to a professional validator while retaining the economic benefits of staking. This lowers the barrier to entry, allowing anyone with the native token to contribute to network security and earn passive rewards.

Optimizing Capital Efficiency with Liquid Staking

A significant limitation of traditional staking is illiquidity. When assets are staked, they are locked in a smart contract and cannot be used for trading or collateral. This creates a conflict for users who want to support the network but also want to utilize their capital in DeFi.

Liquid staking resolves this inefficiency. When a user stakes through a liquid staking protocol, they receive a receipt token in return. This token represents their claim on the staked asset plus any accrued rewards. For instance, staking Ethereum might yield a token that tracks the value of that Ether.

These liquid staking tokens (LSTs) are freely tradable. They can be used as collateral in lending protocols or traded on DEXs. This allows the same capital to be productive in two places at once. The asset secures the underlying blockchain while the receipt token generates yield or provides liquidity in the DeFi ecosystem.

Expanding Security Horizons: Restaking

The concept of restaking represents the next evolution in blockchain security efficiency. It allows the trust established on one network to be extended to others. Traditionally, every new decentralized service, such as an oracle or a bridge, needed to bootstrap its own set of validators and economic trust. This is expensive and often leads to fragmented security.

The Mechanics of Shared Security

Restaking enables validators to reuse their staked capital to secure additional protocols. By opting into new slashing conditions, a validator can commit their existing stake to secure multiple services simultaneously. This aggregates security, allowing smaller protocols to inherit the robust security guarantees of a major blockchain like Ethereum.

There are two primary methods for this. Native restaking involves a validator pointing their withdrawal credentials to the restaking smart contracts. They run additional software to validate the new services. Liquid restaking, on the other hand, involves depositing LSTs into a restaking protocol, which then manages the delegation to operators.

Risks of Rehypothecation

While restaking increases capital efficiency and reward potential, it introduces compounded risks. The most prominent is the risk of slashing. Since the same capital is securing multiple networks, a technical failure or malicious act could result in penalties across all of them.

Furthermore, restaking adds layers of complexity to the ecosystem. It creates a web of dependencies where a failure in one protocol could ripple through to others. There are also concerns regarding centralization, as validators who take on more risk to offer higher yields might attract the majority of the capital, weakening the decentralized nature of the base layer.

Navigating Risks in the Decentralized Stack

The decentralized stack offers immense power, but it transfers the burden of security to the user. Without banks to reverse transactions, mistakes are often irreversible. Understanding the specific risks associated with DApps and smart contracts is vital for asset preservation.

Technical Vulnerabilities

Code is written by humans, and human error is inevitable. Smart contracts can contain bugs that hackers exploit to drain funds. Even protocols that have been audited by security firms are not immune. An audit reduces risk but does not eliminate it.

Users must be wary of "rug pulls," where developers abandon a project and steal the funds. This often happens in new, unverified projects offering unrealistically high yields. In these scenarios, the code may allow the creators to mint infinite tokens or drain the liquidity pools, leaving investors with worthless assets.

Operational Security

Phishing is a pervasive threat in the Web3 space. Attackers create fake websites that mimic legitimate DApps. If a user connects their wallet to a malicious interface, they may inadvertently sign a transaction giving the attacker permission to spend their funds.

Verifying the URL is the first line of defense. Additionally, users should check for lock icons in the browser and rely on bookmarks for frequently used services. The open nature of the stack means anyone can deploy a contract, so due diligence is the responsibility of the individual.

Conclusion

The decentralized stack represents a fundamental re-architecture of digital value. By layering DApps and smart contracts over robust consensus mechanisms, it enables a financial system that is open, transparent, and automated. From the foundational security of staking to the capital efficiency of restaking, each layer builds upon the last to create a cohesive ecosystem.

While the innovation provides new opportunities for yield and participation, it demands a higher level of technical literacy. The removal of intermediaries empowers users but also removes the safety nets found in traditional finance. As the technology matures, the distinction between these layers may blur, but the core principles of self-custody and verifiable code will remain central.

The decentralized stack empowers you to be your own bank, provided you verify every interaction.