For many newcomers to the cryptocurrency space, trading begins with spot markets—buying Bitcoin (BTC) or Ethereum (ETH) directly, hoping the price goes up. However, the world of sophisticated financial management extends far beyond simple buying and selling. Once investors establish a foundational portfolio, they invariably encounter the need to protect their gains, limit potential losses, or generate income regardless of market direction. This is where options come in.

Crypto options are powerful derivative instruments that offer financial flexibility unmatched by standard spot trading or even basic futures contracts. Unlike speculative tools designed purely for leverage and high risk, options are fundamentally instruments of insurance and risk management. They allow investors to manage volatility, set precise price floors and ceilings for their assets, and hedge significant positions against adverse market moves.

This guide is structured to take absolute beginners through the essential mechanics of crypto options. We will start by defining the core concepts of calls and puts, move into practical, low-risk strategies like portfolio insurance, and culminate in an explanation of the underlying mathematical sensitivities—the Greeks—that govern how options are priced and behave. Our focus throughout will remain fixed on using options not for aggressive speculation, but as essential tools for responsible, advanced portfolio management.

The Foundation: What Are Crypto Options?

A crypto option contract is a derivative instrument—its value is derived from the value of an underlying asset, such as Bitcoin or Ethereum. Crucially, an option gives the holder the right, but not the obligation, to buy or sell the underlying asset at a predetermined price, on or before a specified date.

This concept of the "right, not the obligation" is what separates options from futures contracts. A futures contract obligates both the buyer and seller to transact on the expiry date, which introduces significant mandatory risk. Options offer flexibility; if the market moves against the holder, they can simply let the option expire worthless, losing only the initial cost.

Options vs. Spot Trading

When you engage in spot trading, you are immediately transacting ownership of the cryptocurrency. If you buy one BTC for $60,000, you spend $60,000 and own the asset, exposing you to all subsequent price volatility.

An option transaction, however, is a transaction involving risk transfer. Instead of buying the asset, you are buying a contract that controls the asset's potential future price.

Analogy: The Insurance Policy

Think of buying an option as buying car insurance. You pay a small fee (the premium) to the insurance company. If a major accident occurs (the market drops sharply), your policy (the option) guarantees that your losses are capped or that your asset can be protected at a certain value (the strike price). If no accident occurs, you only lose the small premium you paid, but you protected yourself against catastrophic risk.

Key Terminology

To understand options, you must first master four fundamental terms:

1. The Premium (Cost)

The premium is the price the buyer pays to the seller (writer) of the option contract. This is the up-front cost to acquire the right to exercise the option. If the option expires worthless, the buyer’s maximum loss is the premium paid, and the seller’s maximum gain is the premium collected.

2. The Strike Price (The Agreed Price)

The strike price (or exercise price) is the specific price at which the underlying asset can be bought or sold if the option is exercised. If BTC is trading at $65,000, and you buy an option with a $70,000 strike price, $70,000 is the guaranteed transaction price.

3. The Expiry Date (The Deadline)

Options have a limited lifespan. The expiry date is the final day on which the contract can be exercised. Crypto options are typically available for daily, weekly, monthly, or quarterly expiration periods. Once this date passes, the contract is dead.

4. Intrinsic Value and Time Value

- Intrinsic Value: This is the immediate profit you would realize if you exercised the option right now. An option only has intrinsic value if it is In the Money (ITM).

- Time Value: This is the portion of the premium that reflects the possibility that the option will move into the money before expiration. All options lose time value as they approach expiry, a concept known as Theta Decay.

Deciphering the Core Instruments: Calls and Puts

Options contracts are divided into two fundamental types: Call Options and Put Options. Each grants a different type of right and is used for different directional views or hedging needs.

Call Options: The Right to Buy

A Call Option grants the holder the right to buy the underlying asset at the specified strike price on or before the expiration date.

Who Buys Calls and Why?

Investors buy call options when they are bullish on the underlying asset. They believe the asset's price will rise significantly above the strike price before expiry.

Example Use Case (Speculative): BTC is currently trading at $60,000. You believe it will surge past $70,000 next month.

- You buy a call option with a strike price of $65,000, paying a $1,000 premium.

- If BTC rises to $75,000 by expiry, you can exercise your right to buy BTC for $65,000 (the strike price) and immediately sell it on the spot market for $75,000. Your profit is $10,000 minus the $1,000 premium paid, equaling $9,000.

- If BTC falls to $55,000, you simply let the option expire. You lose only the $1,000 premium.

Buying calls is a way to bet on an upward movement with defined, limited risk (the premium).

Put Options: The Right to Sell

A Put Option grants the holder the right to sell the underlying asset at the specified strike price on or before the expiration date.

Who Buys Puts and Why?

Investors buy put options when they are bearish or, more importantly, when they want to protect assets they already own from a downside move.

Example Use Case (Hedging/Protective): You own 1 ETH, currently worth $3,000, but you are nervous about a looming market crash.

- You buy a put option with a strike price of $2,800, paying a $100 premium.

- If ETH crashes to $2,000, you can exercise your right to sell your ETH for $2,800 (the strike price). The loss on your ETH holding is limited to $200 ($3,000 current price - $2,800 strike) plus the $100 premium.

- If ETH rises to $3,500, you let the put option expire worthless. You lose the $100 premium, but your ETH holding increased in value by $500, making the protection worthwhile.

Buying puts is the simplest and most effective way to hedge against downside risk, acting as portfolio insurance.

The Dynamics: Buyers vs. Sellers (Long vs. Short)

It takes two parties to create an option contract:

| Role | Position | Action | Risk Profile |

|---|---|---|---|

| Buyer (Long) | Long Call or Long Put | Pays the Premium | Risk is limited to the premium paid. Potential profit is unlimited (for Calls) or substantial (for Puts). |

| Seller (Short/Writer) | Short Call or Short Put | Receives the Premium | Profit is limited to the premium received. Risk is potentially unlimited (for Short Calls) or substantial (for Short Puts). |

Why Selling Options is Highly Advanced: While selling (or "writing") options guarantees you receive the premium upfront, it exposes the seller to potentially unlimited risk. If you sell a Call and the price skyrockets, you are obligated to sell the asset at a below-market price, forcing you to acquire it at a loss. Because of this unlimited downside exposure, selling options is generally reserved for highly experienced traders with strong risk collateral, and it is explicitly not recommended for beginners focused on simple hedging.

Options for Risk Management: Basic Hedging Strategies

The core strength of options lies in their ability to define risk precisely. By combining ownership of the underlying asset with specific option contracts, investors can implement effective hedging strategies that minimize volatility and maximize capital efficiency.

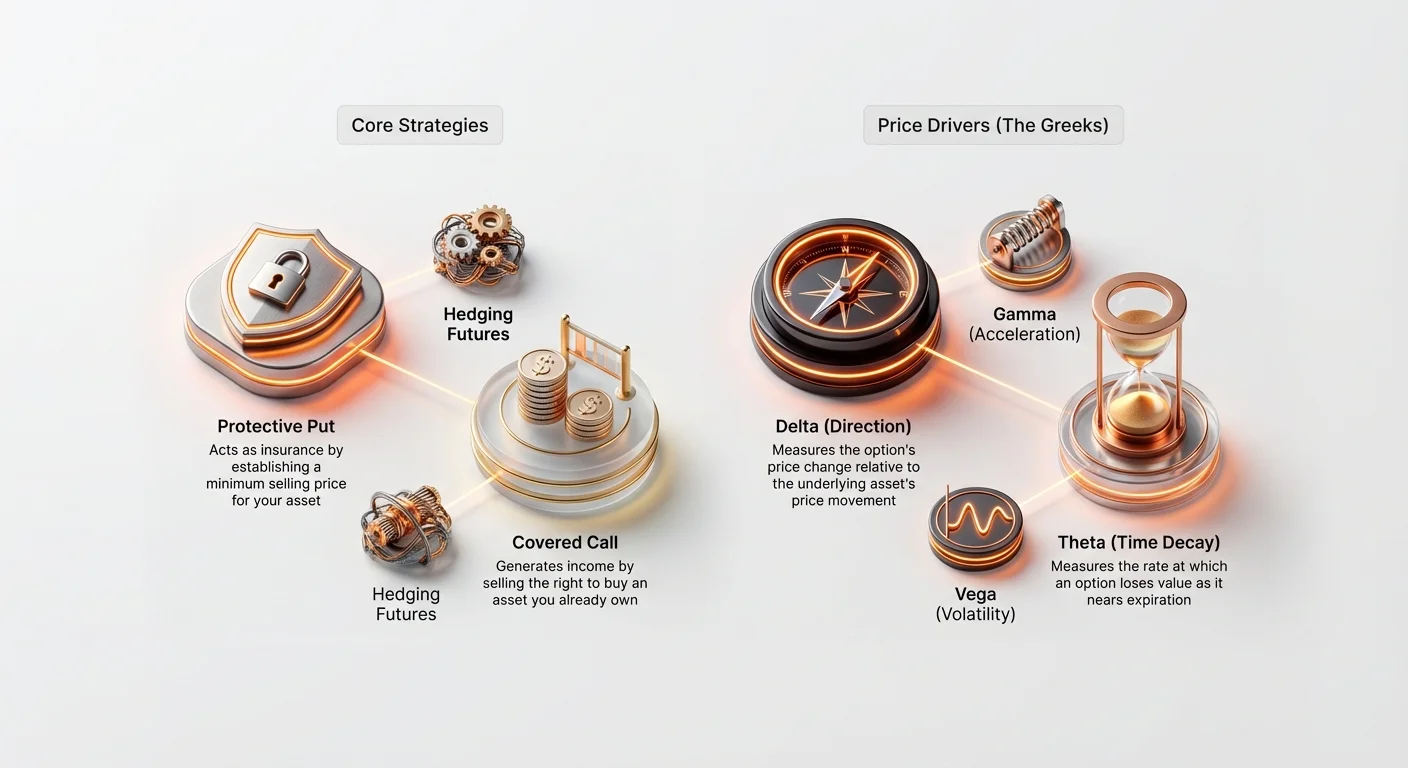

The Protective Put: Insuring Your Portfolio

The Protective Put is perhaps the most fundamental and essential hedging strategy for long-term investors. It involves buying a put option on an asset you already own (or "hold long").

How it Works: Creating a Price Floor

When you own an asset (like 1 BTC) and buy a put option (for 1 BTC) with a strike price slightly below the current market price, you establish a guaranteed minimum selling price for your asset. This is equivalent to setting an insurance deductible.

Example: Protecting a Bitcoin Holding

- Current Position: You hold 1 BTC, currently trading at $60,000.

- Strategy: Buy a 30-day Put option with a $55,000 strike price for a premium of $1,500.

| Scenario | BTC Price Movement (30 Days) | Action/Outcome | Net Profit/Loss |

|---|---|---|---|

| A. Market Crashes | BTC falls to $45,000. | Exercise the $55,000 Put, selling your BTC at $55,000. | Loss is capped at $5,000 (market drop) + $1,500 (premium) = $6,500. (Without the put, the loss would be $15,000). |

| B. Market Rises | BTC rises to $65,000. | Let the $55,000 Put expire worthless. | Gain $5,000 (asset appreciation) - $1,500 (premium) = $3,500. |

The key takeaway is that the Protective Put eliminates tail risk—the danger of catastrophic, sharp declines—while allowing the investor to fully benefit from any upward appreciation, minus the small cost of the premium.

The Covered Call: Generating Income on Holdings

The Covered Call strategy is an income-generating tool suitable for investors who hold an asset (like ETH or BTC) and are comfortable selling it if the price rises past a certain point, or if they believe the asset will trade sideways (in a range) for a period.

The strategy involves owning the underlying asset (the "cover") and selling (writing) a call option against it.

How it Works: Collecting Premium for Limited Upside

By selling the call, you collect the premium immediately. In return, you accept the obligation to sell the asset at the strike price if the buyer chooses to exercise the option.

Example: Selling Calls on Ethereum

- Current Position: You hold 10 ETH, currently trading at $3,000 per coin ($30,000 total).

- Strategy: Sell a 60-day Call option with a $3,300 strike price, collecting a premium of $100 per contract (or $1,000 total).

| Scenario | ETH Price Movement (60 Days) | Action/Outcome | Net Profit/Loss |

|---|---|---|---|

| A. Price Rises (Option Exercised) | ETH rises to $3,500. | The buyer exercises the call. You are obligated to sell your 10 ETH at $3,300. | You profit from the appreciation up to $3,300, plus the $1,000 premium. You miss out on appreciation above $3,300, but you secured a guaranteed sale price. |

| B. Price Falls or Stays Flat (Option Expires) | ETH falls to $2,900. | The option expires worthless. You keep your 10 ETH holdings. | You still keep the $1,000 premium received, generating income even though the underlying asset dropped slightly. |

The Covered Call is often used by large institutions to systematically generate yield on their long-term, high-capital holdings during periods of anticipated low volatility.

Understanding the Drivers of Option Price: The Greeks

To move beyond simply executing basic strategies, a sophisticated trader must understand the key factors that cause an option's premium to change in real-time. These factors are known as the Greeks—a set of mathematical measures that define an option's sensitivity to various market variables.

While the calculations behind the Greeks are complex (based on the Black-Scholes model), understanding their fundamental roles is essential for managing risk.

Delta (Δ): The Directional Sensitivity

Delta measures how much an option's price (premium) is expected to change for every $1 movement in the price of the underlying asset.

- Call Delta: Ranges from 0 to +1.0.

- Put Delta: Ranges from 0 to -1.0.

Interpretation: If a Call option has a Delta of 0.60, it means that if BTC rises by $1, the option premium will increase by $0.60.

- At-the-Money (ATM) options (where the strike price equals the current market price) typically have a Delta near 0.50 (for Calls) or -0.50 (for Puts).

- Deep In-the-Money (ITM) options (highly profitable) behave almost like the underlying asset itself, with a Delta approaching 1.0 or -1.0.

Hedging Use: Delta helps investors determine the directional exposure of their overall portfolio. If a portfolio has a net Delta of 20, it means the portfolio will gain $20 for every $1 rise in the underlying asset's price. Traders use options to balance their Delta (a process called Delta Hedging) to make their overall position neutral to small price changes.

Gamma (Γ): The Acceleration of Delta

Gamma measures the rate of change of Delta. In simpler terms, if Delta is the speed of the option premium change, Gamma is the acceleration or the gas pedal.

Interpretation: Gamma is highest for options that are At-the-Money. This means that as the underlying asset’s price moves toward or away from the strike price, the Delta changes very quickly, making the option premium highly sensitive to movement.

Practical Use: High Gamma indicates high risk. Traders with high Gamma must constantly monitor and rebalance their hedges because their directional exposure (Delta) changes rapidly with even small movements in the market.

Theta (Θ): The Impact of Time Decay

Theta measures how much an option’s premium loses value each day due purely to the passage of time. Theta is always negative for option buyers, reflecting the reality that time works against the buyer.

Interpretation: If an option has a Theta of -0.05, the option premium will lose $0.05 of value tomorrow, all else being equal.

Key Characteristic: Theta decay accelerates dramatically as the option approaches its expiration date. This is why a one-day-to-expiry option loses value much faster than an option with 90 days left.

Hedging Use: Investors must account for Theta when selecting options. For hedging large positions, purchasing options with a longer time horizon (e.g., three months) is often more cost-effective over the long run because they experience less daily Theta decay than short-term weekly options.

Vega (ν): The Volatility Magnet

Vega measures an option’s sensitivity to changes in the underlying asset's implied volatility (IV). Volatility is the market's expectation of how much the price will fluctuate in the future.

Interpretation: If an option has a Vega of 0.15, it means that if implied volatility increases by 1%, the option’s premium will increase by $0.15.

Key Relationship: Because options are fundamentally instruments that profit from movement (either up or down), volatility is their lifeblood. Higher implied volatility always leads to higher option premiums.

Hedging Use: Vega is critical for traders who use options to hedge against volatility itself. If you expect a major news event that could cause wild price swings, buying options (long Vega exposure) will increase the value of your hedge as market uncertainty increases, even if the price hasn't moved yet.

Volatility: The Heart of Option Pricing

While the price of the underlying asset is the obvious factor, volatility is the single greatest driver of an option's premium. Options are essentially bets on future uncertainty; the more uncertain the future, the more valuable the contract. This uncertainty is measured through volatility, which is generally categorized into two types: Implied and Realized.

Implied Volatility (IV): The Market’s Prediction

Implied Volatility (IV) is the market’s expectation of how volatile the underlying asset will be during the life of the option contract. It is not calculated from historical price movements; instead, it is derived by plugging the current market price of the option premium, along with the strike price, time to expiry, and current asset price, into an options pricing model.

IV is a Reflection of Demand and Fear:

- High IV: Indicates that the market anticipates significant price swings. When major events are upcoming (e.g., network upgrades, regulatory decisions), options demand spikes, driving up IV and premiums.

- Low IV: Suggests the market expects stability and little movement.

Importance for Hedgers: When buying insurance (Protective Puts), you want to buy them when IV is low, as the premium will be cheaper. If you wait until IV is high (i.e., fear has peaked), your insurance will be extremely expensive.

Realized Volatility (RV): The Actual Movement

Realized Volatility (RV), also known as Historical Volatility (HV), measures how much the asset actually has moved over a specific past period. It is a historical statistic calculated from price data.

The Relationship to Risk: A high RV means the asset has experienced large, sudden price swings in the past. While RV doesn't predict the future, it gives traders a benchmark for the asset’s natural movement range.

The IV/RV Relationship for Strategists

The difference between Implied Volatility and Realized Volatility forms a core aspect of advanced options trading strategy.

Scenario: IV > RV If the implied volatility (market expectation) is significantly higher than the realized volatility (historical movement), it suggests that options are overpriced. The market is pricing in a move that has not historically materialized. Advanced traders might look to sell options in this scenario (e.g., selling Covered Calls) to capitalize on the inflated premiums, assuming the volatility is unlikely to materialize.

Scenario: IV < RV If implied volatility is lower than realized volatility, it suggests that options are potentially underpriced. The market expects a calmer future than the asset has experienced in the recent past. This is an excellent time for hedgers to buy protective options, as the insurance is cheaper relative to the historical risk.

Actionable Tip: Strategic hedgers seek situations where the cost of insurance (IV) is low relative to the current level of risk (RV) to secure the best pricing for their protective puts.

Advanced Hedging Applications

Once you master the fundamentals of Calls, Puts, and the Greeks, options can be utilized in complex scenarios, particularly in conjunction with other derivatives like futures.

Using Options to Hedge Futures Positions

Futures and perpetual contracts allow traders to use high leverage, magnifying both potential profits and potential losses, including mandatory mandatory liquidation. Options provide a powerful tool to protect highly leveraged futures positions without reducing the leverage itself.

The Problem with Leveraged Long Futures

If you hold a 10x leveraged long BTC perpetual futures contract, a 10% drop in BTC price could lead to liquidation and total loss of collateral.

The Solution: Buying a Protective Put

By simultaneously holding the leveraged long futures contract and buying a Protective Put option, you can create a synthetic guaranteed price floor.

Example: Hedging a Leveraged Long

- Futures Position: Long 1 BTC futures contract at $60,000 (10x leverage). Liquidation price is near $54,000.

- Option Hedge: Buy a Put option with a strike price of $55,000.

- Outcome: If BTC drops sharply, the value of the Put option soars as it moves deep into the money. This profit from the Put contract can be used to offset the margin call losses on the futures position, effectively raising the liquidation price or covering the loss from the required margin top-up, preventing the leveraged position from being wiped out.

This combined strategy provides the high potential returns of leverage while ensuring a predetermined maximum loss, something impossible to achieve with stop-loss orders alone (which can fail during sudden market flash crashes).

Options for Range Trading (Straddles and Strangles)

While our focus is hedging, understanding strategies that capitalize on volatility is useful. Straddles and Strangles are two popular combinations used when a trader anticipates major movement, but is unsure of the direction.

- Long Straddle: Buy a Call and a Put option with the same strike price and same expiration date. This strategy pays off if the asset moves sharply up OR sharply down. It is a pure bet on volatility (long Vega).

- Long Strangle: Buy a Call above the market price and a Put below the market price (different strikes). This is cheaper than a straddle but requires an even larger price movement to be profitable.

These strategies are powerful hedges for situations involving binary risk—where an event could send the price wildly in either direction (e.g., waiting for a major central bank announcement or a lawsuit ruling).

Best Practices for Beginners in Crypto Options

Options are complex, and while they are excellent risk management tools, they require discipline and careful execution. Beginners should adhere to strict guidelines before entering the options market.

1. Start with Paper Trading and Demo Accounts

Never execute an options trade with real capital until you fully understand how Delta, Theta, and Vega affect the premium. Most major derivatives exchanges offer demo or "paper trading" accounts that use synthetic funds. Practice buying protective puts and covered calls, and watch how the premium changes daily due to time decay (Theta) and price movement (Delta).

2. Prioritize Protective Puts over Speculative Calls

For risk management purposes, begin by using options purely to protect existing long-term holdings (Protective Puts). This limits your exposure to the premium cost while giving you essential experience with contract expiration and exercise mechanics. Avoid buying naked Calls or Puts for speculation until you have significant experience.

3. Focus on Longer Expirations (Higher Theta Tolerance)

Short-term options (weekly) have dramatically higher Theta decay. This means your hedge loses value very quickly. While monthly or quarterly options cost more upfront, the time decay is spread out, making them much more forgiving for beginners who might not be checking the position hourly.

4. Never Sell (Write) Options

As covered earlier, selling or writing options (Short Calls or Short Puts) carries the risk of unlimited losses. This is the fastest way for a novice trader to experience catastrophic financial damage. Only advanced financial institutions or professionals with deep collateral should consider writing options.

5. Account for Transaction Costs

Crypto option markets may involve significant fees, including trading fees, settlement fees, and, sometimes, large collateral requirements. Ensure that the premium you are paying for your hedge is not so high that it erodes the potential profitability of your underlying position. Hedging is about risk reduction, not cost elimination.

Conclusion

Crypto options represent the financial backbone of sophisticated digital asset management. They move beyond simple directional bets, providing investors with the ability to define their exact risk exposure, cap their losses, and generate stable income from their existing holdings.

By mastering the difference between Calls and Puts, understanding how the Greeks drive price movement, and utilizing volatility analysis (IV vs. RV), novice investors can evolve into strategic market participants. Start with the Protective Put—treating the option premium as essential insurance for your portfolio—and gradually expand your knowledge. When used responsibly, options are not simply a complex trading vehicle, but an indispensable tool for long-term capital preservation in the volatile world of cryptocurrency.