Welcome to the world of crypto trading. If you are just starting out, fees might seem like a small annoyance—a few dollars here and there when you buy Bitcoin or Ethereum. However, as you transition from a casual investor to a serious, high-volume trader, fees stop being an annoyance and become the single most critical factor determining your profitability.

For advanced traders, particularly those utilizing strategies like high-frequency trading or complex derivative instruments, even a tiny difference in a fee percentage can result in tens of thousands of dollars in annual profit or loss. Navigating this landscape requires moving beyond simple percentages and understanding how exchanges incentivize behavior, offer volume discounts, and even provide fee rebates to institutional players.

This guide provides a comprehensive breakdown of crypto exchange fee structures, starting with the basics and moving quickly into the advanced strategies used by professional traders to achieve market maker status—the pinnacle of cost efficiency in digital asset trading.

The Foundational Cost of Trading: Taker vs. Maker Fees

The first step in understanding advanced fee structures is grasping the fundamental difference between Taker and Maker fees. This distinction is central to how almost every major centralized exchange (CEX) manages liquidity and charges its clients.

Defining the Order Book and Liquidity

To understand Taker and Maker fees, we must first understand the Order Book. The order book is the live, public list of all outstanding buy (bid) and sell (ask) orders for a specific asset pair (like BTC/USD).

Liquidity refers to how easily an asset can be bought or sold without significantly impacting its price. An exchange with high liquidity means there are many resting orders, allowing large trades to be executed instantly at stable prices. Exchanges highly prioritize attracting liquidity because it makes the platform more attractive and reliable for all users.

Taker Fees: The Cost of Immediate Execution

A Taker is a trader who executes an order immediately against existing orders already resting on the order book. When you place a "market order"—an instruction to buy or sell immediately at the best available price—you are taking liquidity out of the market.

Why Takers Pay More: The exchange charges Takers a higher fee because they are consuming the available liquidity, which the exchange must constantly strive to replenish.

- Example: You see BTC trading at $60,000. You place a market order to buy 1 BTC instantly. Your order executes against someone else’s pre-placed sell order. You are the Taker, and you pay the Taker fee (often ranging from 0.05% to 0.10%).

Maker Fees: The Reward for Providing Liquidity

A Maker is a trader who places a limit order that is not immediately matched. Instead, the order "rests" on the order book, waiting for a matching counterparty. By placing this resting order, the Maker is providing liquidity, making it easier for future traders (Takers) to execute their trades.

Why Makers Pay Less (or Get Paid): Exchanges want more resting limit orders to deepen their order book. To incentivize this behavior, they charge Makers significantly lower fees, and in advanced tiers, they may even offer a rebate (a negative fee).

- Example: BTC is trading at $60,000. You place a limit order to sell 1 BTC at $60,500. This order doesn't execute instantly; it joins the order book. If another trader later executes a market buy order against your resting sell order, you are the Maker, and you pay the lower Maker fee (often ranging from 0.01% to 0.05% for retail users).

For the high-frequency trader, the primary goal is to structure every possible transaction as a Maker trade to minimize execution costs.

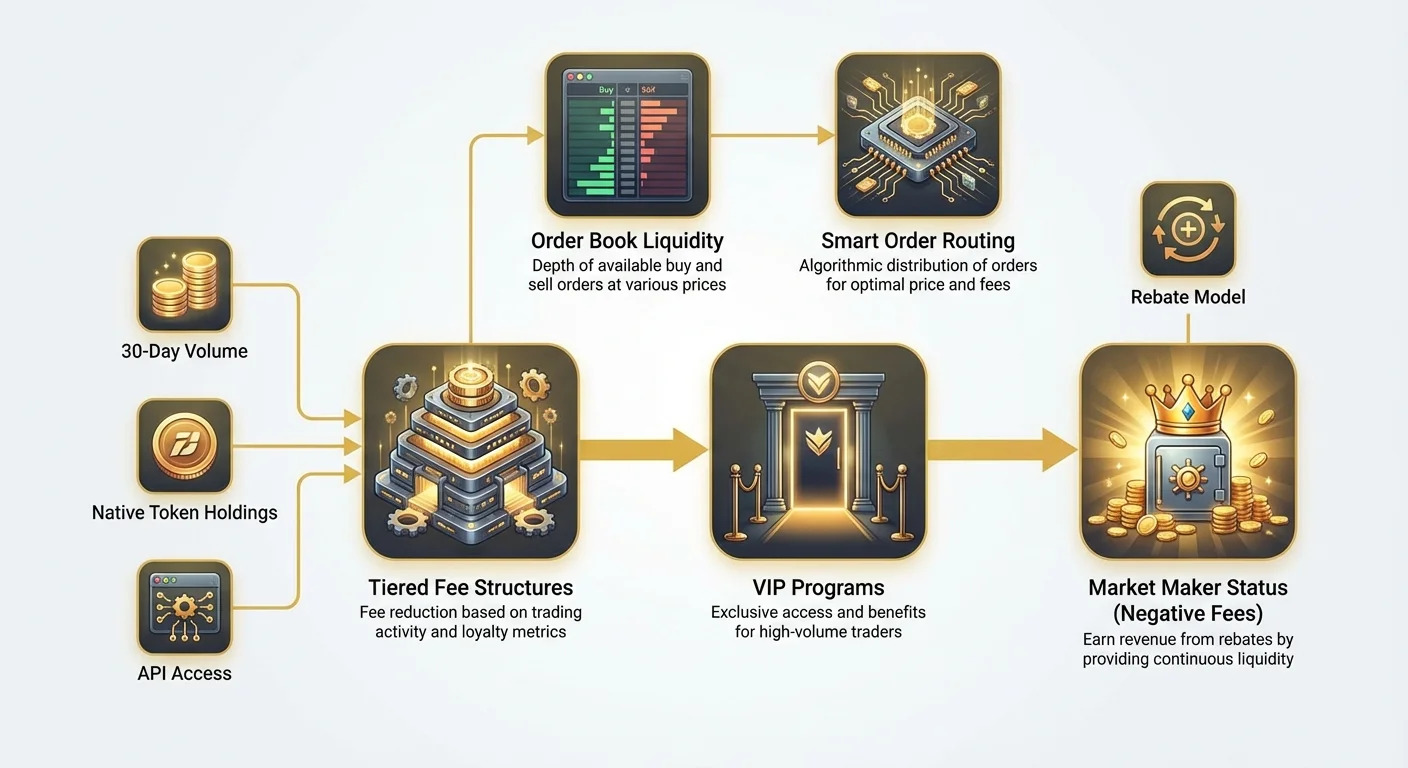

Scaling Costs: Understanding Tiered Fee Structures

While retail traders usually operate on a single, flat fee schedule, high-volume traders interact with complex, tiered fee structures that dramatically reduce their costs based on monthly activity.

Volume and Token Holdings: The Two Main Drivers of Tiered Fees

Tiered fee structures are designed to reward loyalty and high activity. Exchanges define tiers based on two primary metrics:

- 30-Day Trading Volume: This is the most common metric. Exchanges calculate the total value of trades executed by the user (usually in USD or a specific asset) over the preceding 30 days. As volume increases, the user moves up the VIP tiers, and both their Taker and Maker fees decrease.

- Native Token Holdings: Many exchanges incentivize holding their proprietary exchange token (e.g., BNB for Binance, FTT for FTX before its collapse, etc.). Holding a minimum balance of these tokens often grants an immediate reduction in fees, regardless of trading volume, or unlocks access to higher VIP tiers sooner.

For example, a low-volume retail user might start at "Tier 0" with Taker/Maker fees of 0.10%/0.10%. A trader executing $10 million in trades per month might reach "Tier 5" with Taker/Maker fees of 0.03%/0.01%.

VIP Programs and Institutional Accounts

Above the standard retail tiers, exchanges typically maintain exclusive VIP Programs or offer specific Institutional Accounts. These programs are tailored for entities like hedge funds, proprietary trading desks, and large-scale liquidity providers.

Accessing these tiers often requires substantial commitments:

- High Volume Thresholds: Trading volumes may need to exceed $100 million or even $1 billion per month.

- API Quality: Institutional accounts often get dedicated API access points, ensuring lower latency (faster execution times) compared to standard retail accounts, which is critical for high-frequency strategies.

- Dedicated Support: They receive dedicated account managers to handle settlement, regulatory, and technical issues instantly.

The primary benefit of these top-tier programs is not just lower fees, but access to fee rebates, which moves us closer to the concept of Market Maker status.

Calculating the Effective Trading Cost

When analyzing a tiered structure, professional traders do not look at the advertised fee. They calculate the Effective Trading Cost (ETC).

The ETC accounts for the combination of fees paid and any rebates or discounts received. Since a successful high-frequency strategy aims to execute most trades as Maker trades, the ETC heavily weights the Maker fee (or rebate).

Formula for ETC (Simplified):

Where $V$ is the percentage volume traded as Taker or Maker, and $F$ is the respective fee rate.

If a high-frequency firm can maintain 95% of its volume as Maker volume, even if the Taker fee is high (say 0.05%), the overall effective cost remains extremely low, especially if the Maker fee is negative (a rebate).

The Ultimate Cost Advantage: Achieving Market Maker Status

For professional trading firms, the ultimate goal is not simply reducing fees but reversing them entirely—moving into a net positive revenue stream derived from trading volume. This is achieved through the Market Maker (MM) Status.

What is a Market Maker?

A Market Maker is a specialized firm or individual that simultaneously places both buy (bid) and sell (ask) limit orders for an asset, aiming to profit from the small spread (the difference between the highest bid and lowest ask price).

The Role: Market makers are crucial for exchange health. They ensure that there is always someone ready to buy and someone ready to sell, thereby guaranteeing deep liquidity and minimizing price slippage for everyone else.

The Market Maker Rebate Model (Negative Fees)

Because exchanges rely so heavily on market makers to provide stability, they don't just waive the Maker fees—they offer a rebate. A rebate is essentially a negative fee: the exchange pays the market maker a small percentage of the trade value for every transaction that executes against their resting limit order.

| Tier Example | Taker Fee | Maker Fee | Impact |

|---|---|---|---|

| Retail Trader | 0.10% | 0.08% | Pays exchange $0.80 per $1,000 trade. |

| VIP Trader | 0.04% | 0.00% | Pays $0.40 (Taker) or $0 (Maker). |

| Market Maker (MM1) | 0.02% | -0.005% | Exchange pays MM $0.05 per $1,000 trade. |

The Market Maker status effectively transforms trading from a cost center (paying fees) into a revenue center (earning rebates), allowing them to operate at volumes and speeds that retail traders cannot compete with.

Requirements and Obligations for Market Maker Programs

Gaining MM status is not automatic; it requires formal application and meeting strict technical and operational criteria:

- Minimum Volume Commitment: Exchanges demand proof of ability to maintain a guaranteed minimum 30-day trading volume, often in the hundreds of millions or billions of dollars.

- High-Frequency Trading Capability: MMs must demonstrate the ability to update quotes and execute trades rapidly (high update rate and low latency). This typically involves dedicated API connection testing.

- Quote Reliability (Uptime): Exchanges require MMs to maintain continuous liquidity and uptime, meaning their algorithms must run 24/7/365, reacting instantly to market shifts.

- Spread Constraints: Some exchanges require MMs to keep their bids and asks within a very tight percentage of the mid-price (the average of the best bid and best ask). This ensures the liquidity provided is truly useful and competitive.

These sophisticated requirements highlight why MM status is almost exclusively reserved for dedicated institutional trading firms that invest heavily in infrastructure, co-location, and algorithmic development.

Practical Example: How Rebates Power High-Frequency Trading

Consider a high-frequency trading (HFT) firm targeting a spread of $10 on a Bitcoin trade.

- They place a bid (buy) at $59,995 and an ask (sell) at $60,005.

- A retail Taker executes against the bid, buying 1 BTC. The HFT firm makes $5 from the trade execution and simultaneously receives a $3 rebate (based on a negative 0.005% Maker fee).

- The HFT firm’s profit is $8 per BTC, derived primarily from the rebate structure.

Because the firm is earning money simply by having their orders filled, they can afford to quote much tighter spreads than a retail trader who has to pay a fee, further cementing their dominance in liquidity provision.

Dissecting Zero-Fee and Promotional Exchanges

In recent years, many exchanges have popularized the concept of "zero-fee trading" or offered highly aggressive promotional fee schedules. While these seem appealing, especially to beginners, understanding their business model reveals the true costs.

The Myth of Truly Free Trading

No business operates truly for free. If an exchange advertises zero fees, they are almost certainly making revenue elsewhere. This is often referred to as monetization through different verticals.

Common sources of revenue for "zero-fee" platforms include:

- Spreads: The exchange intentionally widens the difference between the buy and sell prices (the spread). While you pay "no fee," you execute the trade at a slightly worse price than the market average, meaning the exchange captures the difference.

- Derivatives Trading Fees: While spot trading (buying and selling the underlying asset) might be free, the exchange charges fees on highly profitable products like futures, options, and perpetual contracts.

- Interest/Lending: The exchange uses client deposits for lending or interest-generating activities.

- Premium Services: Fees for margin trading, dedicated APIs, or advanced analytics.

For high-volume traders, a seemingly "zero-fee" exchange might actually be far more expensive than a low-fee, high-rebate exchange due to hidden costs embedded in execution quality or the spread.

Spot vs. Derivatives Fees

It is critical to distinguish between fees for spot trading and fees for derivatives trading.

- Spot Trading: Generally, fees are higher, especially for Takers, because the exchange must manage custody and settlement of the actual assets.

- Derivatives Trading (Futures, Perpetuals, Options): Fees are often dramatically lower, particularly for large-scale traders, because derivatives are based purely on contracts and involve significantly more leverage and volume potential.

The source articles highlight the popularity of perpetual futures and leverage. The immense volume generated by trading these instruments makes them highly profitable for exchanges, allowing them to offer very competitive (often negative) Maker fees to institutional players to encourage constant liquidity in these markets. If you are aiming for Market Maker status, your focus will overwhelmingly be on high-volume derivatives markets.

Analyzing Cost in the Context of Leverage and Futures

When using leverage, small fees become exponentially more expensive relative to your invested capital.

Imagine a trader using 10x leverage on a $10,000 position:

- The fee is calculated on the full $10,000 notional value, even though the trader only put up $1,000 of collateral.

- A 0.10% Taker fee costs the trader $10.

- If the trader makes 100 such leveraged trades a day, the accumulated fees become substantial very quickly.

This magnification effect is why advanced traders using leverage strategies simply cannot afford standard retail fees. Achieving VIP or Market Maker status is not just a benefit—it’s a prerequisite for the viability of the strategy itself. By lowering the Taker fee to 0.02% or earning a Maker rebate of -0.005%, the cost burden on high-frequency, leveraged trading is manageable, or even profitable.

Advanced Strategies for Minimizing Trading Costs

Professional trading requires proactive management of fee structures. It's not enough to simply check the fee schedule once; fees must be factored into every automated decision.

Smart Order Routing and Fee Optimization

Sophisticated trading algorithms utilize Smart Order Routing (SOR) to achieve the best possible execution price and fee structure across multiple exchanges.

Instead of sending an entire order to a single exchange, an SOR system will:

- Liquidity Sweep: Check the current order books across all accessible exchanges (e.g., Coinbase, Kraken, Binance, proprietary platforms).

- Fee Calculation: Determine the effective cost (including Taker/Maker status) for executing different parts of the order on different venues.

- Optimal Allocation: Slice the main order into smaller sub-orders, sending them to the exchanges that offer the lowest ETC or the highest rebate.

For instance, if Exchange A offers a better rebate for a Maker trade, the SOR will send a limit order there. If a high-volume Taker execution is necessary, the SOR might prioritize Exchange B, which offers the lowest Taker fee due to the trader’s current VIP tier status on that specific platform.

The Importance of Venue Selection (CEX vs. DEX)

Choosing the right trading venue is crucial for fee optimization.

| Venue Type | Fee Structure Focus | Cost Optimization Model |

|---|---|---|

| Centralized Exchanges (CEX) | Taker/Maker Fees, Tiered Rebates | Volume and Infrastructure. Rewards HFT firms with large capital and dedicated API connections. |

| Decentralized Exchanges (DEX) | Gas Fees (Network Cost), Protocol Fees | Efficient Smart Contract Interaction. Rewards users who batch transactions or utilize Layer 2 scaling solutions to minimize gas costs. |

While CEXs are the primary focus for achieving Market Maker status and negative fees, high-frequency traders also dedicate resources to minimizing DEX transaction costs (gas fees), which, if not managed, can often dwarf the percentage-based fees of a centralized platform.

Actionable Tip: Periodic Fee Audit

Even if you are a retail or mid-level trader, performing a quarterly fee audit can save significant capital:

- Analyze Your Behavior: Review your last 90 days of trades. Calculate the percentage split between Taker and Maker orders. If your Maker volume is low, adjust your strategy to use more limit orders.

- Check Tier Requirements: Compare your 30-day volume against the next higher fee tier on your primary exchange. If you are close, a few strategic, large trades might unlock a lower fee, paying for themselves over time.

- Evaluate Token Holdings: If your exchange offers fee reductions for holding their native token, calculate whether the potential fee savings outweigh the risk and cost of buying and holding the required token amount.

Conclusion

Fee structures are the hidden engine of modern cryptocurrency trading. For the retail investor, they represent a minor transactional cost. For the professional, high-volume, or institutional trader, they represent a strategic asset.

By mastering the distinction between Taker and Maker dynamics, understanding how tiered systems reward volume, and ultimately, striving to achieve Market Maker status and its associated fee rebates, advanced traders transform cost management into a fundamental source of competitive advantage. In the high-stakes, low-margin world of automated trading, knowing exactly what you pay—or what you are paid—is the key to long-term profitability.