The cryptocurrency market has evolved significantly from simple spot trading to a complex financial ecosystem dominated by crypto derivatives explained. Among these financial instruments, perpetual futures contracts have emerged as the primary vehicle for price speculation and hedging. Unlike traditional futures contracts that have a specific expiration date, perpetual futures allow traders to hold positions indefinitely. This flexibility has made them the most liquid instrument in the crypto space, far surpassing spot volume on major exchanges.

Derivatives are financial contracts between two or more parties that derive their value from an underlying asset. In the context of cryptocurrency, the underlying asset is typically a digital currency like Bitcoin or Ethereum. Traders use these instruments to speculate on future price movements without necessarily owning the asset itself. This distinction is crucial for understanding market mechanics, as it introduces layers of leverage and settlement that do not exist in spot markets.

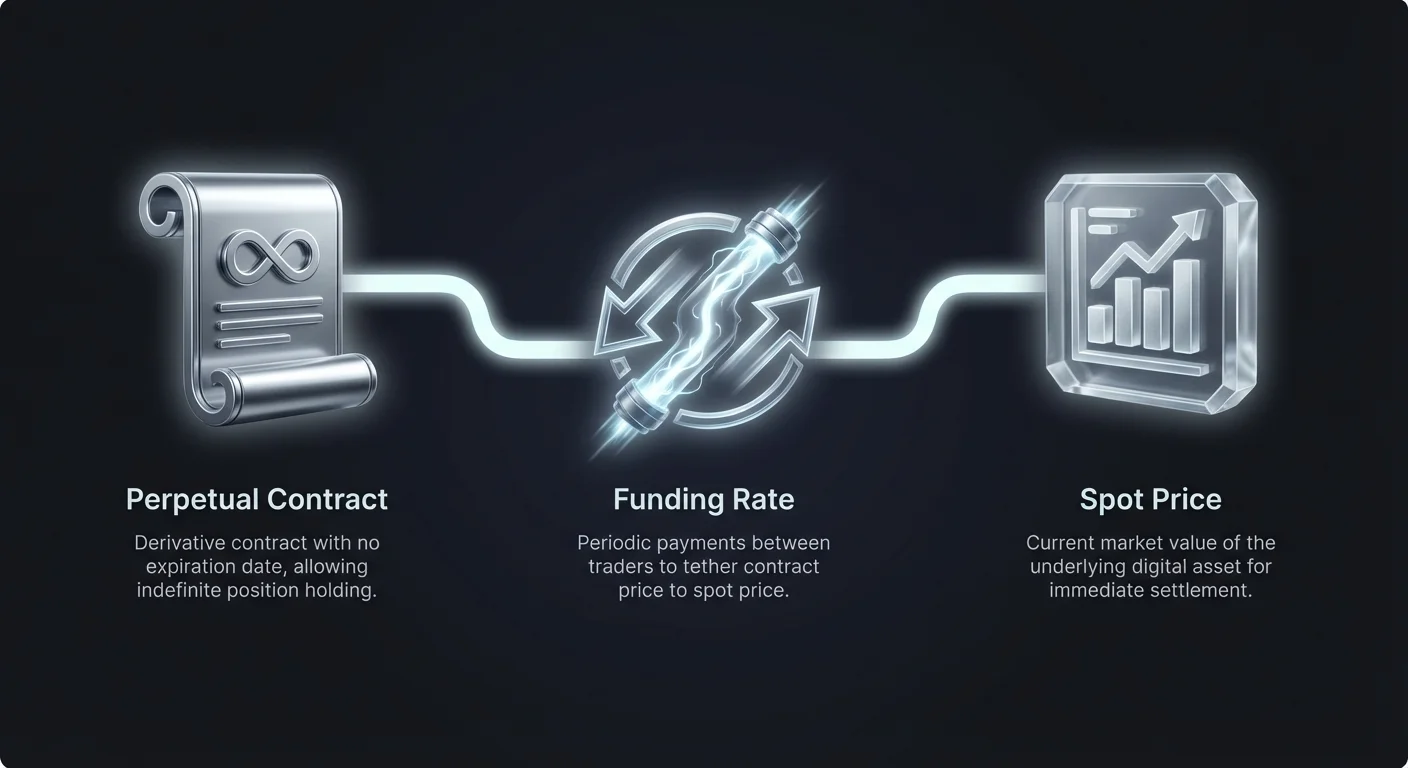

The popularity of perpetual contracts stems from their ability to mimic the spot market while offering the capital efficiency of futures. In a traditional futures contract, the price of the contract eventually converges with the spot price as the expiration date approaches. Perpetual contracts lack this expiration date, requiring a different mechanism to ensure the contract price remains tethered to the underlying spot price.

This mechanism is known as the funding rate. It acts as a periodic payment between traders holding long positions and those holding short positions. By adjusting incentives based on market demand, the funding rate prevents the perpetual price from deviating too far from the index price. Understanding this mechanism is essential for any trader looking to navigate the derivatives market effectively.

The Architecture of Perpetual Contracts

A perpetual futures contract, often referred to as a "perp," is a unique derivative product found primarily in cryptocurrency markets. It allows traders to gain exposure to an asset's price movements without the constraints of a settlement date. When you buy a traditional futures contract, you are agreeing to buy the asset at a specific price on a specific date. If you hold a perpetual contract, you are agreeing to buy or sell the asset at an undetermined point in the future, maintaining the position as long as you meet margin requirements.

The primary utility of this architecture is the consolidation of liquidity. In traditional markets, liquidity is fragmented across various expiry dates—March futures, June futures, September futures, and so on. Perpetual contracts concentrate all that trading activity into a single instrument. This results in deeper order books, tighter spreads, and more efficient price discovery. For high-frequency traders and institutions, this liquidity depth is a critical factor in executing large orders without significant slippage.

Because there is no settlement date, the contract essentially rolls over continuously. This creates a trading experience that feels very similar to spot trading but with the added functionality of leverage and shorting. However, simply removing the expiry date would theoretically allow the contract price to decouple completely from the spot price. If the majority of the market is bullish, the price of the perpetual contract could trade significantly higher than the actual asset.

To solve this, exchanges use a system of price anchors. The "Index Price" represents the average spot price of the asset across major exchanges. The "Mark Price" is a calculation used to value positions and determine liquidations, designed to prevent manipulation. Finally, the funding rate mechanism forces convergence between the contract price and the underlying asset price.

Funding Rate Dynamics

The funding rate is the equilibrium mechanism of the perpetual futures market. It ensures that the price of the derivative aligns with the price of the underlying spot asset. Without it, supply and demand imbalances would cause permanent price divergence.

Positive Funding Rates

When the funding rate is positive, the price of the perpetual contract is trading higher than the spot price. This typically indicates bullish sentiment, where more traders are opening long positions than short positions. In this scenario, traders holding long positions must pay the funding fee to traders holding short positions. This payment incentivizes traders to close long positions or open short positions, driving the contract price down toward the spot price.

Negative Funding Rates

Conversely, a negative funding rate occurs when the perpetual contract price falls below the spot price. This signals bearish sentiment, with selling pressure outweighing buying pressure. When the rate is negative, traders holding short positions pay fees to those holding long positions. This incentivizes buying activity (closing shorts or opening longs), which pushes the contract price back up to align with the market average.

Calculating Funding Costs and Yields

The calculation of funding rates occurs at specific intervals, typically every eight hours on most major exchanges. This periodic settlement means that holding a position during the funding timestamp will result in either a debit or credit to the trader's account balance. The magnitude of the rate depends on the "premium index," which measures the gap between the perpetual price and the spot price, combined with an interest rate component.

For a trader, understanding the annualized impact of these rates is vital for profitability. A funding rate of 0.01% per eight-hour interval might seem negligible at first glance. However, this translates to approximately 10.95% per year. During periods of extreme volatility or strong market trends, funding rates can spike significantly higher. It is not uncommon to see rates reach 0.1% or even higher per interval during a massive bull run.

If a trader is holding a leveraged long position during a strong rally, the cost of maintaining that position can erode potential profits. For example, if you hold a position size of $100,000 and the funding rate is 0.1%, you would pay $100 every eight hours. Over a week, this amounts to $2,100 in fees alone, regardless of whether the asset price moves in your favor.

Conversely, this mechanism creates yield-generation opportunities. A trader taking the contrarian side of the market earns these fees. If the market is heavily long and paying high funding, a short seller receives that cash flow directly into their margin balance. This dynamic creates a predictable income stream that is distinct from the price appreciation of the asset itself.

It is important to note that funding fees are exchanged directly between users. The exchange itself does not collect these fees. This peer-to-peer transfer is designed strictly to balance the order book and maintain market health. Traders must monitor the predicted funding rate, which is usually displayed on the trading interface, to decide whether to hold a position through the settlement timestamp.

Arbitrage Opportunities

Arbitrage in the perpetual futures market involves exploiting price inefficiencies between the spot price and the futures price, or between funding rates across different platforms. These strategies are often considered market-neutral, as they seek to profit from the mechanics of the market rather than the direction of the asset.

Cash and Carry Trade

The most common arbitrage strategy is the "cash and carry" trade. When funding rates are positive, a trader can buy the underlying asset in the spot market and simultaneously open a short position of equal value in the perpetual market. Since the short position receives funding payments from longs, the trader earns the funding rate as profit. Because the long spot position and short futures position cancel each other out, the trader is hedged against price movements.

Funding Rate Arbitrage

Another form of arbitrage involves capitalizing on the difference in funding rates between two different exchanges. If Exchange A has a funding rate of 0.05% and Exchange B has a funding rate of 0.01%, a trader can open a short position on Exchange A (to receive the high rate) and a long position on Exchange B (paying the low rate). The net difference represents a profit, assuming transaction fees do not consume the margin.

Leverage and Margin Mechanics

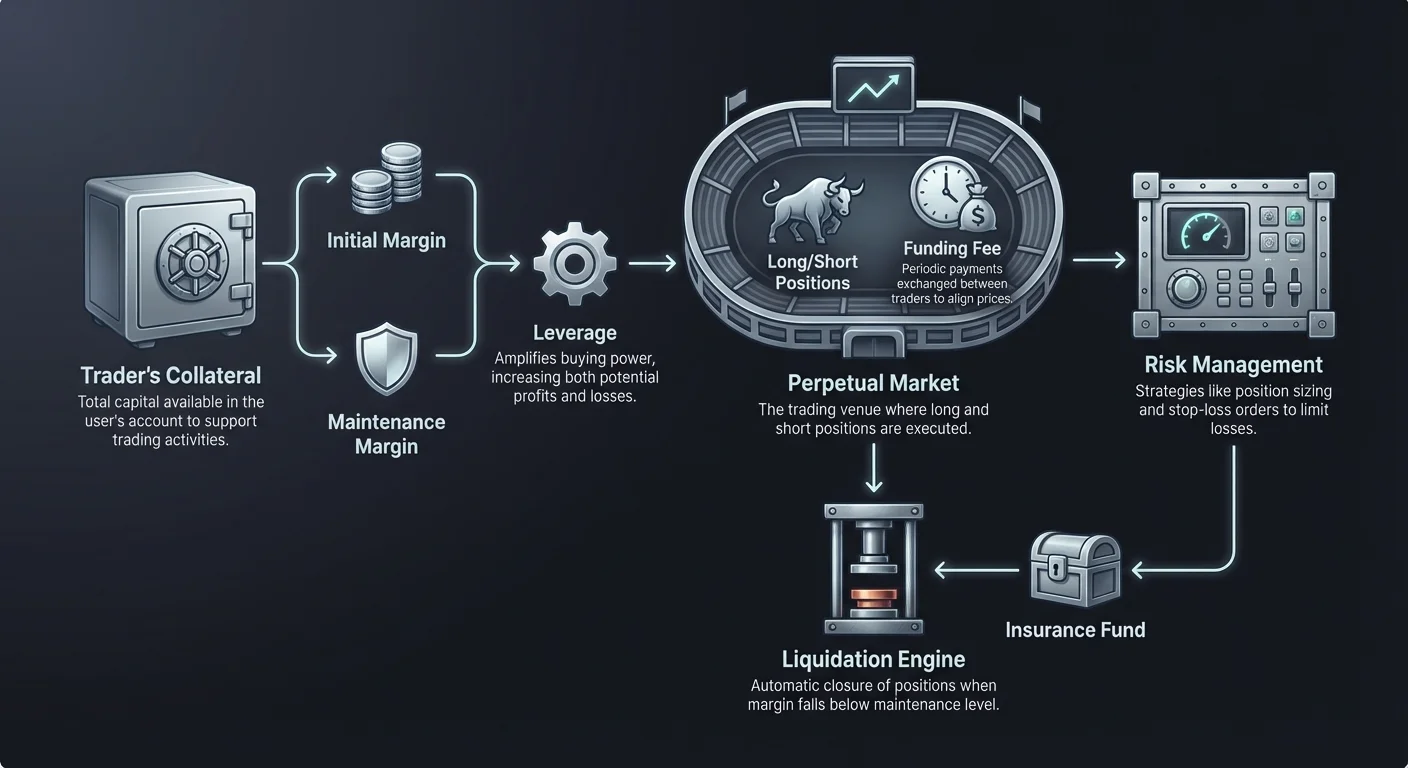

Leverage is a double-edged sword that defines the derivatives landscape. It allows traders to control a position size that is significantly larger than their actual account capital. For instance, using 10x leverage allows a trader with $1,000 to open a position worth $10,000. The borrowed funds are provided by the exchange or liquidity pool, enabling capital efficiency but introducing substantial risk.

The concept of margin is central to leveraged trading. "Initial Margin" is the amount of collateral required to open the position. In the example above, the $1,000 is the initial margin. "Maintenance Margin" is the minimum amount of equity that must remain in the account to keep the position open. If the market moves against the trader and their equity falls below this maintenance level, the position is liquidated.

There are two primary modes of margin management: Cross Margin and Isolated Margin. Cross Margin uses the entire balance of the trading account as collateral for all open positions. This helps prevent liquidation of a single position by utilizing profit or excess capital from other trades. However, it puts the entire account balance at risk. If one position goes drastically wrong, it can drain the capital reserved for other trades, leading to a total account wipeout.

Isolated Margin allocates a specific amount of collateral to a single position. If that position fails, the loss is limited to the funds allocated to that specific trade. The rest of the account balance remains untouched. This is generally recommended for traders managing specific risks or testing speculative strategies.

Leverage amplifies both gains and losses mathematically. A 5% move in the underlying asset price becomes a 50% move in equity when using 10x leverage. While this can lead to rapid wealth accumulation, it makes the portfolio extremely sensitive to volatility. A mere 10% drop in asset price would result in a 100% loss of the initial margin, triggering liquidation.

Liquidation Protocols

Liquidation is the forced closure of a trader's position by the exchange. This occurs when the trader's margin balance falls below the required maintenance margin. Liquidation is a safety mechanism designed to protect the exchange and other traders from insolvency.

The Liquidation Engine

When a liquidation price is triggered, the exchange's liquidation engine takes over the position. It attempts to close the position at the best available market price. Because this forced selling (or buying, in the case of a short) adds pressure to the order book, it can exacerbate price movements. In volatile markets, this can lead to "liquidation cascades," where one liquidation triggers price movement that triggers further liquidations.

Insurance Funds

To manage the risk of slippage during liquidation, exchanges maintain insurance funds. If a position is closed at a price worse than the bankruptcy price (where the trader's equity is zero), the insurance fund covers the deficit. This prevents the winning side of a trade from facing "clawbacks" or socialized losses. Traders should prefer exchanges with robust insurance funds to ensure system stability.

Long and Short Strategies

The ability to take both long and short positions is a defining feature of perpetual futures. In spot trading, a participant can typically only profit if the asset value increases. To profit from a decline, they would have to sell their assets and buy them back later. Perpetual futures simplify this by allowing traders to sell contracts they do not own, effectively betting on a price decline.

Going long involves buying a contract with the expectation that the price will rise. This is similar to buying spot, but with the added dimension of funding rates. If a trader is long, they must be aware that in a bullish market, they will likely pay funding fees. This cost of carry must be factored into the trade's expected return. Long strategies are often used for speculation during uptrends or for leveraging a high-conviction bullish thesis.

Shorting is the act of selling a contract to profit from a price drop. This is essential for market efficiency, as it allows bearish sentiment to be expressed in the price discovery process. Shorting is also a vital tool for hedging. A trader who holds a large portfolio of Bitcoin in cold storage might not want to sell their assets during a temporary downturn for tax or security reasons. Instead, they can open a short position in the perpetual market.

If the price of Bitcoin drops, the value of the cold storage holdings decreases, but the short position in the futures market generates a profit. These two movements offset each other, effectively locking in the portfolio's dollar value. This strategy, known as a "short hedge," allows investors to remain market-neutral without liquidating their long-term holdings.

Shorting carries unique risks, primarily because asset prices theoretically have no ceiling. A long position can only go to zero, capping the loss at 100%. A short position, however, faces unlimited loss potential if the asset price skyrockets. This asymmetry requires strict risk management, particularly when leverage is involved. Short squeezes occur when rising prices force short sellers to buy back their positions to close them, adding more buying pressure and driving the price even higher.

Platform Ecosystems

The landscape of derivatives trading is divided between centralized exchanges (CEX) and decentralized exchanges (DEX). Centralized platforms currently dominate the market volume. They offer high-speed matching engines, deep liquidity, and advanced order types. User interfaces on centralized exchanges are typically polished and responsive, catering to the needs of active day traders and institutional desks.

However, centralized exchanges introduce counterparty risk. Traders must deposit funds into the exchange's custody. As history has shown, mismanagement of funds or security breaches can lead to loss of user capital. Additionally, centralized entities are subject to regulatory pressures that can result in account freezes or jurisdictional restrictions.

Decentralized derivatives platforms are growing in sophistication. Protocols like dYdX and others utilize smart contracts to facilitate perpetual trading without taking custody of user funds. Trades are executed on-chain or via Layer 2 scaling solutions to reduce gas fees and latency. The primary advantage of a DEX is self-custody; the trader retains control of their assets until the trade is executed.

Liquidity on decentralized platforms has historically been lower than on centralized counterparts, but this gap is narrowing. Automated Market Makers (AMMs) and order book models in DeFi are evolving to support the high throughput required for leverage trading. For traders prioritizing privacy and security over raw speed, decentralized options provide a viable alternative.

When choosing a platform, traders must consider the "maker" and "taker" fee model. Takers are traders who execute orders immediately at the market price, removing liquidity from the order book. Makers place limit orders that sit in the order book, providing liquidity. Exchanges often charge higher fees to takers and offer rebates or lower fees to makers to incentivize liquidity provision.

Fee Structures and Economics

Fees are a critical component of any trading strategy, particularly for high-frequency trading or arbitrage. In the perpetual futures market, there are two main types of fees: trading fees and funding fees. Trading fees are paid to the exchange for executing the order, while funding fees are peer-to-peer payments exchanged between traders.

Trading Fees

Exchanges typically employ a tiered fee structure based on 30-day trading volume. The base tier might charge a taker fee of 0.05% and a maker fee of 0.02%. While these percentages seem small, leverage amplifies their impact. If a trader uses 10x leverage, a 0.05% fee on the position size is equivalent to 0.5% of the initial margin. Opening and closing a position would therefore cost 1% of the trader's equity, significantly raising the breakeven point.

Maker vs Taker

To minimize costs, advanced traders use limit orders to act as market makers. By providing liquidity, they often qualify for fee reductions or even rebates, where the exchange pays the trader for the order. This is crucial for arbitrage strategies where profit margins are thin. A "taker" strategy in arbitrage can often eat up the entire spread, rendering the trade unprofitable.

| Fee Type | Payer | Receiver | Purpose |

|---|---|---|---|

| Taker Fee | Trader executing market order | Exchange | Revenue for service |

| Maker Fee | Trader placing limit order | Exchange | Revenue (often discounted) |

| Funding Fee | Long or Short Traders | Counterparty Traders | Price alignment |

Managing Risk in Derivatives

Trading perpetual futures involves significant risk, primarily due to the presence of leverage and volatility. Effective risk management is not optional; it is a requirement for survival. The first line of defense is position sizing. Traders should never allocate their entire capital to a single trade. By using only a small percentage of their portfolio for initial margin, they can withstand market noise without facing liquidation.

Stop-loss orders are essential tools for automating risk control. A stop-loss is an instruction to close the position if the price reaches a certain level. This prevents emotional decision-making during market crashes. Trailing stops are particularly useful in trend-following strategies, as they adjust the exit price upward as the asset price rises, locking in profits while leaving room for further growth.

Traders must also be aware of "slippage." In fast-moving markets, a stop-loss order might not execute at the exact trigger price if there is insufficient liquidity. This is why trading on platforms with deep liquidity is important. Using limit orders for exits can guarantee a price, but carries the risk that the order might not fill if the price moves too quickly, leaving the position open to further losses.

Another risk factor is the "liquidation wick." Occasionally, the price on a specific exchange may momentarily spike or crash due to a large market order clearing out the order book. If this price movement touches a trader's liquidation price, the position is closed, even if the market immediately recovers. Using the "Mark Price" for liquidation triggers rather than the "Last Price" helps mitigate this, as the Mark Price is usually an aggregate of multiple exchanges and is less susceptible to single-exchange anomalies.

Diversification across different assets and strategies can also reduce risk. Instead of betting solely on the direction of Bitcoin, a trader might engage in basis trading or funding rate arbitrage, which are market-neutral. Combining directional trades with yield-generating strategies creates a more robust portfolio that is less dependent on lucky market timing.

Conclusion

Perpetual futures have fundamentally altered the cryptocurrency landscape by providing a capital-efficient tool for speculation and risk management. Through the innovative mechanism of funding rates, these instruments maintain a peg to spot prices without the need for expiration dates. This structure consolidates liquidity and offers traders continuous exposure to the market.

For sophisticated market participants, perpetuals open the door to complex strategies like cash-and-carry arbitrage and delta-neutral farming. However, the inclusion of high leverage and the risk of liquidation demands a disciplined approach. Success in this arena requires a deep understanding of the underlying mechanics, strict adherence to risk management protocols, and a clear strategy for navigating fees and volatility.

Master funding rates and leverage mechanics to transform market volatility into calculated financial opportunity.