Witamy w konkurencyjnym świecie arbitrażu kryptowalutowego. Chociaż podstawowa koncepcja—kupowanie aktywa tanio na jednej platformie i natychmiastowe sprzedawanie go drożej na innej—brzmi zwodniczo prosto, osiągnięcie stałego zysku wymaga czegoś więcej niż tylko dostrzeżenia różnicy w cenie. Na dzisiejszych hiperwydajnych rynkach kryptowalut sukces zależy wyłącznie od szybkości i solidnej infrastruktury.

Ten przewodnik wykracza poza proste definicje botów arbitrażowych. Skupimy się na wymaganiach technicznych, przeszkodach logistycznych i zapotrzebowaniu infrastrukturalnym niezbędnym do angażowania się w realizację międzygiełdową o niskim opóźnieniu. Jest to różnica między dostrzeżeniem zyskownej okazji a posiadaniem zdolności technologicznych do wykonania transakcji, zanim zrobi to ktoś inny does. Dla poważnych inwestorów detalicznych, dążących do działania w tej konkurencyjnej niszy, zrozumienie ograniczeń API, zarządzanie opóźnieniem serwera i strategiczna alokacja kapitału to prawdziwe umiejętności wymagane do osiągnięcia sukcesu.

Zrozumienie Arbitrażu Kryptowalutowego: Co Staramy Się Osiągnąć?

Arbitraż to akt jednoczesnego zakupu i sprzedaży aktywa na różnych rynkach w celu osiągnięcia zysku z tymczasowej różnicy w cenie. W wysoce rozdrobnionym krajobrazie kryptowalut, gdzie tysiące aktywów jest przedmiotem obrotu na dziesiątkach różnych giełd na całym świecie (takich jak Coinbase, Kraken, Bitget, etc.), te rozbieżności cenowe pojawiają się nieustannie. Wyzwaniem jest jednak zrealizowanie transakcji, zanim rynek sam się skoryguje, co często dzieje się w ciągu milisekund.

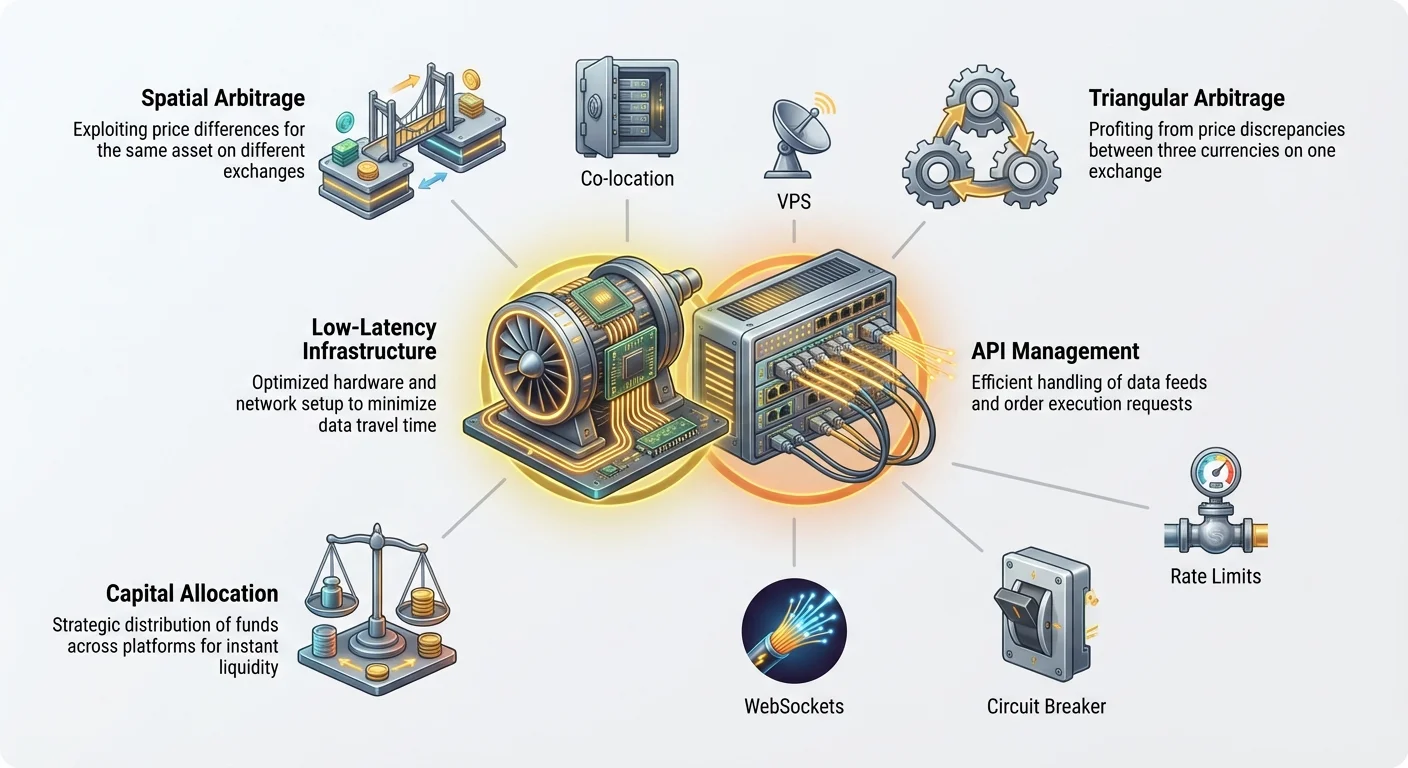

Arbitraż Przestrzenny (Międzygiełdowy)

Arbitraż przestrzenny, znany również jako arbitraż międzygiełdowy, jest najbardziej powszechną i najprostszą formą koncepcyjną. Polega na identyfikacji tego samego aktywa (e.g., Bitcoin, or BTC) notowanego po nieco innej cenie na dwóch odrębnych giełdach.

Przykład użycia: Załóżmy, że BTC jest notowany po $60,000 na Exchange A (główna platforma globalna) i jednocześnie po $60,015 na Exchange B (mniejsza platforma regionalna). Okazją do arbitrażu przestrzennego jest różnica $15.

- System natychmiast wysyła zlecenie kupna 1 BTC na Exchange A po $60,000.

- System natychmiast wysyła zlecenie sprzedaży 1 BTC na Exchange B po $60,015.

Zysk brutto wynosi $15 (minus opłaty transakcyjne i koszty transferu sieciowego). Ponieważ ta różnica w cenie jest natychmiast widoczna dla wszystkich zautomatyzowanych systemów, okno czasowe na realizację jest niezwykle krótkie—często ułamki sekundy. Wymaga to infrastruktury o niskim opóźnieniu.

Arbitraż Trójkątny

Arbitraż trójkątny jest bardziej złożony, ponieważ wykorzystuje niespójności cenowe między trzema różnymi parami walutowymi na tej samej giełdzie. Zamiast przenosić aktywa między platformami, bot wykonuje szybki łańcuch trzech transakcji, które wracają do aktywa początkowego.

Przykład użycia (użycie USD jako waluty początkowej):

- Transakcja 1: Użyj USD, aby kupić BTC (e.g., $100,000 kupuje 1 BTC).

- Transakcja 2: Użyj the BTC, aby kupić ETH (e.g., 1 BTC kupuje 15 ETH).

- Transakcja 3: Użyj the ETH, aby sprzedać z powrotem za USD (e.g., 15 ETH sprzedaje się za $100,100 USD).

If the initial cost was $100,000 and the final return is $100,100, the profit is $100. Cała ta pętla musi zostać ukończona natychmiast, aby uchwycić krótką nieefektywność, zanim wewnętrzne mechanizmy giełdy skorygują ceny. Ponieważ wszystkie trzy transakcje odbywają się na tej samej giełdzie, strategia ta jest mniej zależna od zewnętrznej szybkości sieci, ale w dużym stopniu zależy od API i głębokości księgi zleceń używanej pojedynczej giełdy.

Dlaczego Szybkość Jest Jedyną Przewagą

W każdym scenariuszu arbitrażu istnienie zysku jest ulotne. Gdy tylko pojawi się różnica w cenie, dwie siły natychmiast działają, aby ją wyeliminować:

- Inne boty: Wysoce zoptymalizowane, profesjonalne systemy transakcyjne nieustannie skanują te same rynki. Działają na szybszej infrastrukturze i realizują zlecenia szybciej niż przeciętny inwestor detaliczny.

- Efektywność Rynku: Presja kupna na tańszej giełdzie i presja sprzedaży na droższej giełdzie szybko sprowadzają ceny z powrotem do zgodności.

W momencie, gdy identyfikujesz okazję na $15, profesjonalne systemy prawdopodobnie już ją wykryły i zaczęły zamykać. Jeśli twój czas realizacji wynosi 100 milliseconds, a ich 50 milliseconds, spóźnisz się, potencjalnie nie wykonując transakcji po cenie docelowej lub, co gorsza, ponosząc stratę z powodu poślizgu (realizacji po gorszej cenie niż przewidywano). Dlatego optymalizacja infrastruktury nie jest opcjonalna—jest warunkiem wstępnym rentowności.

Główne Wyzwanie: Radzenie Sobie z Opóźnieniem (Latency)

Latency, simply defined, is delay. W kontekście handlu jest to czas potrzebny na przesłanie informacji z serwera giełdy do twojego systemu transakcyjnego oraz czas potrzebny na powrót twojego zlecenia transakcyjnego do giełdy. Minimalizacja tej zwłoki jest najważniejszym czynnikiem w arbitrażu o niskim opóźnieniu.

Definiowanie Opóźnienia w Handlu

Głównie martwimy się trzema rodzajami opóźnień:

- Opóźnienie Danych (Data Latency): Czas potrzebny na opuszczenie giełdy przez aktualizację ceny (nowa transakcja lub zmiana księgi zleceń) i dotarcie do twojego komputera. Jeśli cena giełdowa wynosi $60,015, ale otrzymasz tę aktualizację 50 milliseconds za późno, okazja może już minąć.

- Opóźnienie Sieciowe (Network Latency): Fizyczny czas potrzebny na podróż danych przez kable internetowe (z twojego routera, przez twojego dostawcę usług internetowych i przez kontynenty do centrum danych giełdy).

- Opóźnienie Realizacji (Execution Latency): Czas, jaki zajmuje twojemu systemowi transakcyjnemu przetworzenie przychodzących danych, obliczenie zysku arbitrażowego, skonstruowanie zleceń kupna/sprzedaży i odesłanie ich z powrotem do giełdy w celu realizacji.

W przypadku arbitrażu przestrzennego, opóźnienie sieciowe między dwiema odległymi geograficznie giełdami jest często największą przeszkodą. Na przykład, jeśli jedna giełda jest hostowana w New York i druga w Singapore, fizyczny czas podróży danych może łatwo przekroczyć 150-200 milliseconds, co czyni arbitraż o niskim opóźnieniu prawie niemożliwym bez dedykowanej infrastruktury sieciowej.

Kolokacja i Bliskość Serwera (Ideały)

Absolutnym standardem dla handlu o niskim opóźnieniu jest co-location. Oznacza to umieszczenie serwerów handlowych w tym samym fizycznym centrum danych, w którym znajdują się serwery giełdy.

Dlaczego kolokacja ma znaczenie: Jeśli twój serwer znajduje się w tym samym budynku co serwer giełdy, sygnał podróżuje zaledwie kilka stóp zamiast setek lub tysięcy mil. Redukuje to opóźnienie sieciowe z tens of milliseconds (ms) do single-digit or sub-millisecond speeds.

Podczas gdy major exchanges often reserve co-location opportunities for large institutional clients, the retail trader must replicate this advantage as closely as possible using cloud computing infrastructure.

Optymalizacja Sieci dla Inwestorów Detalicznych

Since full co-location is generally out of reach for beginners, retail arbitrage traders must utilize Wirtualne Serwery Prywatne (VPS) strategically placed near the exchange data centers.

Najlepsze Praktyki Wyboru VPS:

- Targetowanie Geograficzne: Zidentyfikuj fizyczne lokalizacje serwerów docelowych giełd. If Exchange A is known to use an AWS data center in Virginia and Exchange B uses a Google Cloud center in London, you need to purchase high-performance VPS instances in both locations.

- Dedykowane Zasoby: Avoid cheap, shared hosting. Low-latency systems require dedicated CPU cores and guaranteed bandwidth. Shared resources can introduce "jitter"—inconsistent processing delays—which is fatal to arbitrage profitability.

- Minimalna Liczba Przeskoków: Use networking tools (like

pingortraceroute) to check the path data takes from your VPS to the exchange’s API endpoint. Fewer hops (fewer routers and intermediary services) equate to lower latency. Choose VPS providers known for high-quality network backbones. - Wybór Systemu Operacyjnego: Linux distributions (like Ubuntu or Debian) are standard for trading bots due to their low operating system overhead compared to Windows, which can add unnecessary processing delay (latency) to the execution module.

Praktyczna Wskazówka: Even if you are operating from your home computer, you must connect to the VPS instances directly. The bot must run 24/7 on the VPS, not on your laptop, ensuring continuous, high-speed connection directly to the exchanges.

Budowanie Kręgosłupa Komunikacyjnego: Zarządzanie API

After ensuring minimal physical distance (latency), the next critical step is establishing the fastest and most reliable communication pathway to the exchanges. This is done entirely through Interfejsów Programowania Aplikacji (APIs). The API acts as the digital waiter that takes your orders (trades) and brings you the menu (price data).

Zrozumienie Kanałów REST a WebSocket

Exchanges typically offer two primary methods for interacting with their systems, and understanding the difference is crucial for low-latency trading:

1. REST (Representational State Transfer)

- Jak to działa: This is a traditional request-response model, similar to loading a webpage. You send a specific request (e.g., "What is the current BTC price?") and the exchange sends a static reply.

- Przypadek użycia: Ideal for checking account balances, initiating deposits/withdrawals, or sending single, non-time-critical orders.

- Problem z opóźnieniem: Each REST request requires initiating a new connection and waiting for the full response. This added overhead makes it too slow for real-time price monitoring needed for arbitrage.

2. WebSocket Feeds

- Jak to działa: This establishes a persistent, open connection between your server and the exchange server. Instead of you constantly asking for updates, the exchange przekazuje real-time price changes (order book updates, completed trades) to your system instantly.

- Przypadek użycia: Essential for arbitrage. WebSockets provide the lowest data latency, delivering price feeds as they happen.

- Najlepsza Praktyka: Your data aggregation engine (the scanner) must use WebSockets to monitor the order books of all target exchanges simultaneously.

Obsługa Limitów Żądań API (Rate Limits)

Every exchange imposes rate limits—a cap on how many requests (API calls) your system can send within a specific time window (e.g., 60 requests per second). These limits are designed to prevent malicious denial-of-service (DDoS) attacks and ensure fair access for all users.

Niebezpieczeństwo Limitów Żądań: If your bot hits the rate limit, the exchange will temporarily blacklist your IP address or throttle your connection, meaning you cannot send or receive price updates or execution orders. This is devastating for an arbitrage strategy where every second counts. If you are halfway through an execution and get rate-limited, the market will move against you, resulting in a guaranteed loss.

Strategie Łagodzenia:

- Priorytetyzacja i Kolejkowanie: Do not spam the API. Implement a sophisticated queuing system that only sends essential requests (primarily execution orders). Price monitoring should rely almost exclusively on the non-rate-limited WebSocket stream.

- Przetwarzanie Równoległe (Ostrożnie): While arbitrage requires simultaneous actions on multiple exchanges, be careful not to create too many concurrent threads to a single exchange's API, which can be mistaken for a DDoS attack.

- Monitorowanie Nagłówków: Exchanges send back HTTP headers that explicitly state how many requests you have remaining before hitting the limit. Your infrastructure must constantly read these headers and dynamically slow down or pause non-critical tasks if the limit is approached.

Bezpieczeństwo Kluczy API i Najlepsze Praktyki

Your API keys grant your bot full control over your exchange accounts, including the ability to trade and, sometimes, withdraw funds. Securing these keys is paramount.

- Zasada Najmniejszych Uprawnień: When generating API keys on the exchange (e.g., Coinbase or Kraken), only enable the necessary permissions: reading account data and trading. Nigdy nie włączaj uprawnień do wypłat unless absolutely required for your specific strategy, as this significantly mitigates risk if your bot or server is compromised.

- Bezpieczne Przechowywanie: API keys should nigdy be stored in plain text or hardcoded directly into the bot's source code. Use secure environment variables, encrypted key vaults, or dedicated key management services.

- Dedykowane Klucze: Use unique API keys for each exchange and for each strategy. If one key is compromised, you can revoke it without affecting your access to other platforms.

- Biała Lista IP: If the exchange allows it, configure your API keys so they can wyłącznie be used from the static IP addresses of your chosen VPS instances. If a hacker steals the key, they still won't be able to use it unless they are also operating from your approved server location.

Projekt Infrastruktury: Komponenty Systemu Arbitrażowego

Moving from a simple script to a production-grade arbitrage system requires architecting three distinct, yet interconnected, functional components.

1. Mechanizm Agregacji Danych (Skaner)

This component is responsible for gathering and normalizing real-time market data from all connected exchanges. It is the eyes and ears of the system.

- Funkcja: Connects via WebSockets to Exchange A, Exchange B, Exchange C, etc., simultaneously pulling order book data (bids and asks), completed trade history, and account balances.

- Normalizacja: Different exchanges structure their data differently. The Scanner must instantly translate all incoming price feeds into a standardized format (e.g., always use a five-decimal-place price, always use the symbol BTC/USD) so the Decision Engine can compare them fairly.

- Monitorowanie Opóźnienia: The Scanner should also measure its own data latency—the time elapsed between an exchange publishing a price change and the moment the change is processed by the Scanner. High latency here indicates a network or VPS issue that needs attention.

2. Mechanizm Decyzyjny (Mózg)

This component takes the normalized data from the Scanner and runs proprietary logic to identify and confirm profitable arbitrage opportunities.

- Wykonanie Logiki: This engine constantly runs complex calculations, comparing prices across exchanges (spatial arbitrage) or across three pairs on one exchange (triangular arbitrage).

- Próg Zysku: It determines if the gross profit margin (the price difference) exceeds the necessary Próg Rentowności. This threshold must include all known costs: trading fees, potential withdrawal fees, and a buffer for slippage. If the profit is $15 but the fees are $16, the opportunity is discarded instantly.

- Sprawdzenie Równoczesności: For cross-exchange arbitrage, the Decision Engine must confirm that adequate liquidity (enough volume in the order book) exists on both the buying exchange and the selling exchange to fill the required order size instantly.

3. Moduł Wykonawczy (Ręce)

Once the Decision Engine confirms a viable opportunity above the profit threshold, the Execution Module takes over. This component is designed for speed and reliability.

- Jednoczesne Składanie Zleceń: The Execution Module must fire the buy order on Exchange A and the sell order on Exchange B as close to simultaneously as possible (a process known as "atomic execution" in the high-frequency world).

- Wybór Typu Zlecenia: For arbitrage, market orders are typically used because speed is prioritized over price certainty. However, using limit orders slightly outside the market price can sometimes reduce fees if execution speed isn't absolutely critical. Most low-latency systems default to market orders for guaranteed, rapid filling.

- Zabezpieczenia i Obsługa Błędów: This is arguably the most complex part. If the buy order fills but the sell order fails (due to latency, rate limit, or market movement), the system is left holding the asset and exposed to market risk. The Execution Module must have immediate protocols to cancel the remaining order and potentially execute a risk-mitigating trade to exit the position quickly and minimize losses.

Wyzwanie Logistyczne: Alokacja Kapitału

Even with the fastest infrastructure and the most secure APIs, an arbitrage system is useless if the capital is not positioned correctly. The core difficulty of spatial arbitrage is that you need funds ready to execute trades instantly on wszystkich target exchanges.

Równoważenie Środków Pomiędzy Wieloma Giełdami

Arbitrage requires capital to be idle, waiting for an opportunity. You need funds on the "low" side to buy and funds on the "high" side to sell.

Dylemat Kapitału Międzygiełdowego: Suppose you target BTC/USD arbitrage between Coinbase and Kraken. You must have:

- USD available on Coinbase to buy BTC.

- BTC available on Kraken to sell for USD.

If an opportunity reverses (Kraken becomes the cheaper source), you immediately need:

- BTC available on Coinbase to sell.

- USD available on Kraken to buy.

This means you must maintain a balanced inventory of both fiat/stablecoins (like USD or USDT) and the target cryptocurrency (like BTC or ETH) across all participating exchanges.

Rozwiązanie: Zautomatyzowane Równoważenie Kapitału

A mature arbitrage system includes a sub-module dedicated to capital rebalancing. After a profitable sequence, the net result is an uneven distribution of assets (e.g., more USD on Kraken, less BTC on Coinbase).

- Ręczne Równoważenie: If the profit margin allows, the system must initiate cryptocurrency transfers (BTC, ETH, or sometimes stablecoins) between the exchanges to restore the balanced inventory, preparing for the next trade.

- Preferencja Stablecoinów: Transfers using high-speed, low-fee stablecoins (e.g., USDC or USDT on low-fee networks like Solana or Polygon, if supported by the exchanges) are often preferred for rebalancing, as they minimize volatility risk during the transfer time.

Zarządzanie Opłatami Transakcyjnymi i Wypłatami

While the gross profit of an arbitrage trade might look appealing, fees can quickly erode the margin. A $15 gross profit quickly disappears if trading fees are $5 (buy) + $5 (sell), leaving only $5.

- Opłaty Transakcyjne: Many exchanges tier their fees based on trading volume. A serious arbitrage setup should aim for high-volume tiers ("Maker-Taker" fees) to minimize cost per trade. Your Decision Engine must incorporate your specific exchange fee structure into its profit calculations.

- Opłaty za Wypłatę: When rebalancing capital, withdrawal and network fees (gas fees) are incurred. Since these fees can be substantial (especially for Ethereum-based tokens), rebalancing must only occur when the accumulated profit significantly outweighs the cost of the transfer. This often means running many small trades to build up enough profit before spending it on a rebalancing transfer.

Znaczenie Płynności

Liquidity refers to how easily an asset can be bought or sold without affecting its price. For arbitrage, high liquidity is non-negotiable.

If you attempt to execute a trade on a low-liquidity exchange, your large market order may instantly "eat up" all the available volume at the advertised price, forcing the remainder of your order to execute at worse prices (slippage).

- Ryzyko: This slippage eliminates the arbitrage profit and can even cause a net loss.

- Łagodzenie: The Decision Engine must always check the depth of the order book (the volume available at the current price levels) on both sides of the trade. If the available volume is less than your intended trade size, the opportunity should be ignored, regardless of the observed price difference. Focus arbitrage efforts only on high-volume, top-tier centralized exchanges (CEXs) where depth is reliably present.

Bezpieczeństwo i Łagodzenie Ryzyka

Operating automated systems that have direct control over significant capital across multiple centralized platforms introduces severe security risks. A single vulnerability can lead to catastrophic loss.

Bezpieczne Kodowanie i Praktyki Środowiskowe

Security must be built into the infrastructure from day one.

- Izolacja: The production environment (the VPS hosting the live trading system) should be completely isolated from your development or personal machines.

- Konfiguracja Zapory: Configure the VPS firewall (e.g.,

ufwon Linux) to explicitly allow only outgoing connections to the whitelisted exchange API domains, and incoming connections only from your secure management IP (e.g., your home office IP). Block all other unnecessary ports. - Regularne Audyty: Use external libraries and frameworks (like Python’s CCXT library) that are well-tested for connecting to exchange APIs, rather than trying to build API connectors from scratch. Regularly update all system dependencies to patch known vulnerabilities.

- Logowanie: Implement detailed, non-sensitive logging. Record every decision made by the system (why a trade was executed, why it was rejected, latency metrics) but nigdy nie loguj kluczy API, sekretów ani poufnych danych uwierzytelniających.

Wdrażanie Zabezpieczeń Awaryjnych i Wyłączników Obwodu (Circuit Breakers)

Automated systems can, and eventually will, encounter unforeseen errors, bugs, or extreme market conditions. A responsible system must have mechanisms to prevent runaway losses.

1. Wyłącznik Obwodu (Circuit Breaker)

The circuit breaker is the ultimate safety net. It is a piece of code that, when specific conditions are met, immediately halts all trading activity, cancels open orders, and alerts the operator.

Wyzwalacze dla Wyłącznika Obwodu:

- Maksymalna Dzienna Strata: If the system’s running P&L (Profit and Loss) exceeds a preset daily limit (e.g., losing more than 2% of total capital), the system shuts down.

- Nadmierne Błędy: If the system receives a high volume of unhandled API errors (e.g., rate limit errors or execution failures) within a short time frame, indicating a systemic issue.

- Utrata Łączności: If the system loses connection to one or more critical WebSockets for more than 60 seconds.

2. Limity Pozycji

Always impose strict limits on the maximum size of a single trade and the maximum net exposure (total asset value held) at any given time. This ensures that even a catastrophic error only affects a portion of the capital, not the entire portfolio.

Ochrona Kluczy API i Danych Uwierzytelniających

As discussed briefly in the API section, key management is paramount. Consider using encrypted volumes or specialized secrets management tools (like HashiCorp Vault) to ensure that even if the underlying VPS is breached, the attacker cannot immediately gain access to the raw credentials needed to steal funds or execute malicious trades.

Najlepsza Praktyka: Use two-factor authentication (2FA) wherever possible, even for read-only access to your exchange accounts, and ensure the 2FA method is not tied to the server running the bot.

Podsumowanie: Wyścig z Zerowym Zyskiem

Dążenie do arbitrażu o niskim opóźnieniu to ciągła walka o marginalne przewagi. Chociaż koncepcja kupowania tanio i sprzedawania drogo jest intuicyjna, realizacja wymaga głębokiego zaangażowania w infrastrukturę technologiczną i rygorystyczną logistykę.

Dla początkującego sukces w tej niszy nie wynika ze znalezienia "magic bot." Wynika on z opanowania optymalizacji opóźnień, sumiennego zarządzania interakcjami API w celu uniknięcia limitów żądań i strategicznej alokacji kapitału na wielu giełdach w celu zapewnienia natychmiastowej płynności.

W miarę dojrzewania globalnych rynków kryptowalut i coraz częstszego wchodzenia w tę przestrzeń profesjonalnych firm handlowych wysokiej częstotliwości, okno zyskowności arbitrażu kurczy się. Wyścig z zerowym zyskiem oznacza, że optymalizacja infrastruktury jest jedynym zrównoważonym sposobem na utrzymanie przewagi. Koncentrując się na połączeniach o niskim opóźnieniu, bezpiecznym zarządzaniu API i solidnej obsłudze błędów, poważni inwestorzy detaliczni mogą zbudować fundament niezbędny do konkurowania, even if only on the smaller, faster-moving, cross-exchange opportunities that still exist today.