Iedomājieties, ka jums pieder bagātība, kuru nevar atņemt, iesaldēt vai bloķēt neviena valdība, banka vai centralizēta iestāde. Gadsimtiem ilgi mūsu finanšu dzīve ir balstījusies uz uzticamām trešajām pusēm (TTP)—bankām, kas glabā mūsu ietaupījumus, maksājumu procesoriem, kas apstiprina mūsu darījumus, un valdībām, kas nodrošina sistēmas noteikumus. Lai gan šī struktūra piedāvā ērtības, tā prasa augstu cenu: absolūtas kontroles pār saviem finanšu resursiem zaudēšanu.

Ciparu aktīvu parādīšanās, īpaši Bitcoin, ieviesa radikālu konceptu: pašsuverenitāti. Šis termins apzīmē stāvokli, kurā ir pilnīga kontrole un galīga vara pār savām finansēm bez vajadzības pēc ārēju subjektu atļaujas. Šo revolūciju padara iespējamas divas galvenās tehniskās funkcijas: nekonfiscējamība un cenzūras pretestība.

Šis ceļvedis izpēta, ko šie jēdzieni nozīmē praktiski, pārejot aiz tehniskajām definīcijām, lai izpētītu, kā nekonfiscējamā nauda piedāvā kritisku izmantojamību ne tikai investoriem, bet arī humanitārajām organizācijām, politiskajiem disidentiem un ikvienam, kas meklē īstu finanšu brīvību arvien vairāk uzraudzītā digitālajā pasaulē. Pašsuverenitātes izpratne ir pirmais izšķirošais solis ceļā, lai kļūtu par savu pašu banku.

I. The Technical Core: Defining Censorship Resistance

To understand why Bitcoin is considered "unseizable," we must first define its primary defense mechanism: censorship resistance. In simple terms, a system is censorship resistant if no single entity can stop a legitimate transaction from being processed or confirmed.

In traditional finance, if you try to send money to a person or country deemed hostile by your bank or government, the transaction will be intercepted and stopped. The bank acts as a central gatekeeper, exercising censorship based on political or regulatory demands.

Bitcoin, however, operates differently. It is built on a distributed network of computers (nodes) that all agree on the rules of the network. These rules are mathematical and applied equally to everyone, meaning political or social biases cannot be enforced to block a payment.

Centralized Gatekeepers vs. Decentralized Networks

In the fiat world, money flows through central banks and commercial banks. These entities have the legal and technical authority to pause, reverse, or freeze accounts. If the U.S. government, for example, issues a sanction against an individual, major financial institutions worldwide are obligated to comply by freezing any associated assets. The institution acts as the point of centralization, making it highly vulnerable to pressure.

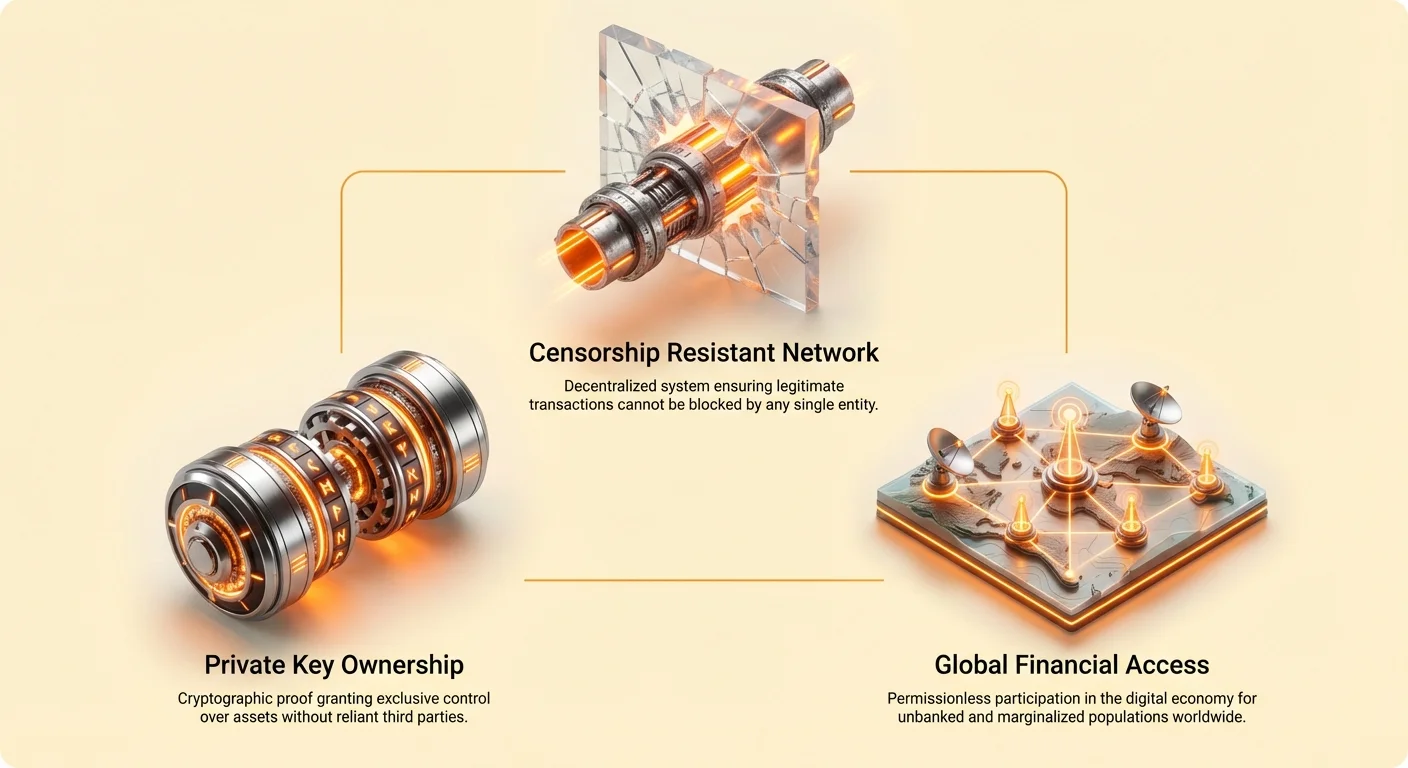

Bitcoin’s network has no central headquarters. Transactions are broadcast to thousands of independent computers (nodes) across the globe. For a transaction to be confirmed and added to the blockchain (the public ledger), it must only adhere to the established rules of the Bitcoin protocol (e.g., the sender must prove ownership via their private key). As long as the transaction is mathematically valid, the decentralized consensus mechanism ensures it is processed. There is no single "off switch" or central administrator capable of blocking the transfer.

Defining "Invalid" vs. "Censored"

It is important to clarify that censorship resistance does not mean "anything goes." The Bitcoin network strictly rejects invalid transactions. An invalid transaction might be one where the sender tries to spend coins they do not own, or one that breaks the cryptographic signing rules.

However, the network is designed to resist censorship—the denial of service based on the identity, location, or purpose of the sender or receiver. Nodes and miners operate based on objective cryptographic proof, not subjective human judgment. If you prove ownership of the funds, the network processes the transaction, regardless of who you are trying to pay.

The Prohibitive Cost of Denial

The ultimate defense against censorship is the sheer cost of attack. To successfully censor transactions on the Bitcoin network, an entity would need to control more than 51% of the total computing power (hash rate) securing the network. Gaining and maintaining control over the majority of global mining resources is practically impossible, requiring billions of dollars in hardware, electricity, and coordination. This economic reality ensures that the network is protected from unilateral hostile takeover by governments or mega-corporations, guaranteeing its neutrality.

II. Fiat kontrasts: Kāpēc aktīvi šodien ir konfiscējami

Lai novērtētu nekonfiscējamās naudas vērtību, vispirms jāatzīst ievainojamība, kas raksturīga tradicionālajām finansēm. Visas modernas banku un maksājumu sistēmas ir balstītas uz implícētu uzticības ietvaru, kur finanšu starpnieki darbojas kā jūsu aktīvu glabātāji un jūsu finanšu atļauju šķīrēji.

Uzticēšanās trešajām pusēm (TTP) ievainojamība

Kad noguldāt naudu bankā, jūs juridiski nododat šo līdzekļu glabāšanu iestādei. Banka sola atgriezt līdzekļus pēc pieprasījuma, bet starlaik tā saglabā tehnisko un juridisko kontroli. Šīs attiecības bieži apkopo frāze: "Nav jūsu atslēgas, nav jūsu monētas." Kad banka vai birža glabā jūsu aktīvus, tie ir tie, kas posedē privātās atslēgas uz šīs finanšu iestādes glabātiem līdzekļiem, dodot tiem galīgo teikšanu.

Šī sistēma darbojas labi, kad uzticība tiek uzturēta, bet tā rada dziļas ievainojamības situācijās, kad:

- Politiskā nestabilitāte: Valdības var ieviest kapitāla kontroles, neļaujot pilsoņiem izņemt vai pārvietot savu naudu ārpus valsts.

- Juridiskas strīdības: Tiesa var izdot aresta rīkojumus, juridiski piespiežot bankas nodot aktīvus, lai apmierinātu parādu vai spriedumu.

- Iestādes neveiksme: Ja banka vai birža sabrūk, jūsu piekļuve līdzekļiem var tikt aizkavēta vai ierobežota, pat sistēmās ar iemaksu apdrošināšanu.

Aktīvu iesaldēšanas un finanšu izslēgšanas gadījumu izpēte

Teorētiskais konfiskācijas risks ir realizējies atkārtoti modernajā laikmetā, radot skaidrus lietošanas gadījumus nekonfiscējamai naudai:

1. Politiskie protesti un finanšu de-platformēšana

Politisko protestu laikā dažādās attīstītās valstīs pēdējos gados valdības izmantoja banku regulas, lai iesaldētu protestu dalībnieku vai ziedotāju līdzekļus. Izdotas tiesas pavēles finanšu iestādēm, varas iestādes spēja liegt protestētājiem piekļuvi viņu ietaupījumiem, efektīvi apturot viņu spēju maksāt par degvielu, ēdienu vai juridisko aizstāvību. Tas demonstrēja, ka finanšu brīvība ir nosacīta, atkarīga no politiskās pakļaušanās.

2. Kapitāla kontroles un ekonomiskais sabrukums

Valstīs, kas piedzīvo hiperinflāciju vai smagu ekonomisko nestabilitāti (piemēram, Libānā, Argentīnā vai Kiprā), valdības ir ierobežojušas pilsoņu spēju izņemt vai pārsūtīt ārvalstu valūtu, ieslēdzot viņu ietaupījumus deprecijējošā vietējā sistēmā. Vidējam pilsonim bankas kontā redzamā nauda ir tikai ieraksts datubāzē, ko kontrolē pati valdība, kas rada ekonomisko grūtību.

3. Šķērsošanas robežu ierobežojumi un humanitārie pudeles kakli

Lielu naudas summu pārvietošana, pat likumīgiem mērķiem kā labdarība vai biznesa investīcijas, prasa precīzu regulatīvo atbilstību. Pretnaudas atmazgāšanas (AML) un Pazīsti savu klientu (KYC) regulas, lai gan svarīgas tiesībsargāšanai, bieži rezultējas likumīgu līdzekļu aizkavēšanā, atzīmēšanā vai pilnīgā bloķēšanā, šķērsojot starptautiskās robežas, radot milzīgu birokrātisku slogu palīdzības organizācijām.

III. Self-Sovereignty in Practice: The Unseizable Wallet

Bitcoin flips the script on financial control. It moves the authority from the institution (the bank) to the individual (the private key holder). True financial self-sovereignty is achieved when the user alone holds the means to access and spend their funds.

Private Keys as Absolute Ownership

The key to unseizable money lies in cryptography. When you own Bitcoin, you do not physically possess a digital coin; you possess a private key. This key is a secret, long string of letters and numbers (often represented by a 12 or 24-word seed phrase) that acts as the cryptographic proof of ownership.

If you maintain sole custody of this private key, no one—not your government, your bank, or the network's developers—can move your Bitcoin. They can see the balance associated with your public address on the blockchain, but they cannot authorize a transaction. This simple technological fact creates absolute financial sovereignty.

Analogy: If bank money is like a title deed stored in a government registry, self-sovereign money is like a safe deposit box key that only you possess, where the location of the safe is known to everyone, but the contents are impenetrable without your specific key.

The Critical Role of Self-Custody

For an asset to be truly unseizable, it must be held in self-custody—meaning you, and only you, control the private keys.

If you purchase Bitcoin and leave it on a centralized cryptocurrency exchange (CEX) like Coinbase or Binance, the asset is not self-sovereign. The exchange holds the private keys, making it a trusted third party. Just like a bank, the exchange must comply with legal orders, freezing or seizing the assets if mandated by a court.

True self-sovereignty demands that you move your assets into a dedicated, non-custodial wallet (often a hardware wallet or a robust software wallet). In this environment, the digital asset is effectively immune to institutional seizure, providing the user with unprecedented control.

Plausible Deniability and Portable Wealth

Self-sovereignty offers practical utility in situations of extreme distress, such as fleeing political persecution or conflict. A significant amount of wealth—potentially millions of dollars worth of Bitcoin—can be secured by memorizing a 12- or 24-word seed phrase.

This creates plausible deniability for wealth storage. Unlike gold, diamonds, or physical cash, which can be searched for, confiscated, or taxed at the border, a seed phrase is intangible. A person can cross any international boundary, carrying only their knowledge, and later regenerate their entire life savings using a new wallet and an internet connection anywhere in the world. This portability is a foundational aspect of self-sovereign money.

IV. Globālā izmantojamība: Kam vajadzīga cenzūras pretestība?

Lai gan finanšu pašsuverenitāte piedāvā spēcīgas priekšrocības ikvienam, tās visdziļākā izmantojamība realizējas tiem, kas vēsturiski ir izslēgti vai apspisti no centralizētām sistēmām. Cenzūras pretestība nav tikai investora funkcija; tā ir kritisks instruments cilvēktiesībām, ekonomiskajai stabilitātei un brīvībai.

Atbalsts disidentiem un politiskajai opozīcijai

Autoritāros režīmos viena no pirmajām taktikām, lai apspiestu nesaskaņas, ir finanšu atslēgšana. Valdības var ātri identificēt, lokalizēt un iesaldēt opozīcijas līderu, NVO vai aktīvistu grupu līdzekļus, aizrījot viņu spēju organizēties, komunicēt vai maksāt algas.

Bitcoin piedāvā glābšanas līniju. Disidenti var pieņemt ziedojumus no starptautiskiem atbalstītājiem bez bankas konta, starpnieka vai oficiālas atļaujas vajadzības. Šie līdzekļi var tikt uzglabāti ārpus valsts jurisdikcijas un iztērēti peer-to-peer, apietot diktatora kontroli pār finanšu sistēmu. Šī finanšu izturība stiprina pozīcijas tiem, kas cīnās par demokrātiju un cilvēktiesībām.

Humanitārā palīdzība konfliktu zonās

Humanitārās organizācijas bieži saskaras ar milzīgiem izaicinājumiem, darbojoties konfliktu zonās vai nestabilas pārvaldības apgabalos. Bankas var atteikties apstrādāt darījumus uz noteiktām reģioniem sankciju riska dēļ vai vietējās valdības var konfiscēt palīdzības līdzekļus caur korupciju vai tiešu sagrābšanu.

Izmantojot cenzūras pretestīgu aktīvu, organizācijas var:

- Nodrošināt tiešu piegādi: Līdzekļus var nosūtīt tieši indivīdiem vai vietējiem kopienu līderiem, izmantojot vienkāršus mobilos maciņus, apietot centralizētus finanšu šaurinājumus.

- Samazināt birokrātiju: Pārskaitījumi tiek apstrādāti neatkarīgi no laika joslām, politiskajām robežām vai banku darba laikiem, paātrinot ārkārtas palīdzības izvietošanu.

- Saglabāt vērtību: Apgabalos, kur vietējā valūta sabrūk, palīdzības saņemšana relatīvi stabilā digitālā aktīvā nodrošina labāku ilgtermiņa drošību saņēmējiem.

Finanšu iekļaušana nebanknotajiem

Apmēram 1,7 miljardi pieaugušo visā pasaulē ir nebanknoti, t.i., tiem nav piekļuves formālām finanšu pakalpojumiem. Bieži tas ir tāpēc, ka tiem nav valdības izsniegtas identifikācijas, viņi dzīvo attālinātās vietās vai nevar izpildīt minimālā atlikuma prasības.

Pašsuverēnie kripto tīkli piedāvā tūlītēju finanšu iekļaušanu. Jebkurš ar viedtālruni var lejupielādēt neuzglabājošu maciņu un piedalīties globālajā ekonomikā. Nav vajadzīga atļauja, kredīta pārbaude vai valdības ID, lai izveidotu Bitcoin maciņu. Šī piekļuve ļauj agrāk finanšu ziņā neredzamiem indivīdiem ietaupīt, veikt darījumus un saņemt pārskaitījumus, dodot viņiem taustāmu daļu savā ekonomiskajā nākotnē.

V. Responsibility and Risk: Becoming Your Own Bank

The concept of self-sovereignty is synonymous with extreme responsibility. When you eliminate the intermediary (the bank), you gain ultimate control, but you also assume all the associated risks that the bank traditionally managed. For a beginner, this transition requires a fundamental shift in mindset.

Your Private Key Is Your Bank Vault

In the fiat world, if you forget your password, the bank can verify your identity and reset your account access. If you get defrauded, the bank or payment processor might be able to reverse the transaction or insure your losses.

In the world of self-sovereign money, there is no customer service line, no government insurance, and no reversal button.

- If you lose your private key (seed phrase), your funds are permanently lost. They cannot be recovered by anyone, as no central database holds a copy.

- If your private key is stolen, your funds are permanently stolen. Once a thief spends your Bitcoin, the transaction is immutable (cannot be reversed).

This immutability is the trade-off for unseizability. The features that make the money impossible for a government to seize also make it impossible for you to recover if you mismanage the key.

Security Best Practices for Self-Custody

Achieving and maintaining self-sovereignty requires rigorous adherence to security protocols:

1. Prioritize Physical Security of the Seed Phrase

The 12 or 24 words of your recovery seed phrase are the physical representation of your private key.

- Do not store it digitally (no screenshots, cloud storage, or plain text files on a computer). Digital copies are highly vulnerable to hacking.

- Write it down on specialized paper or etch it into metal. Metal backups are recommended for long-term storage as they are resistant to fire and water damage.

- Store the physical backup in a secure, hidden location (e.g., a safe or bank vault).

2. Utilize Hardware Wallets

For beginners and those holding non-trivial amounts of money, a hardware wallet (like Trezor or Ledger) is the gold standard for self-custody. A hardware wallet keeps your private key isolated offline, ensuring it never touches an internet-connected device. Even if your computer is infected with malware, the key remains protected inside the device, requiring physical confirmation (pressing a button) for any transaction.

3. Practice Test Transactions

Before moving a significant amount of wealth, practice the entire process: move a very small amount of Bitcoin into your new self-custody wallet, then wipe the wallet software (or reset the hardware device), and practice restoring the funds using only your seed phrase. Only once you have successfully demonstrated that you can restore your funds should you move larger sums.

The Double-Edged Sword of Immutability

The unseizable nature of self-sovereign money means that transaction finality is absolute. Once a Bitcoin transaction is confirmed on the blockchain, it is immutable—it is recorded forever and cannot be changed or reversed.

While this immutability provides censorship resistance, it also means mistakes are permanent. If you accidentally send funds to the wrong address, or if you fall for a scam and send money voluntarily, there is no recourse. This requires users to be meticulous, double-checking addresses and amounts before broadcasting any transaction. This high standard of care is the price of total self-sovereignty.

Secinājums: Finanšu brīvības atgūšana

Pašsuverenitāte, kas realizēta caur nekonfiscējamās naudas un cenzūras pretestības tehniskajām īpašībām, pārstāv fundamentālāko pārmaiņu finansēs pēdējos desmitgadēs. Tā pārvieto varu prom no centralizētām iestādēm—kas darbojas, balstoties uz mainīgiem politiskajiem vējiem un birokrātiskajām prasībām—un novieto to tieši indivīda rokās.

Šī pārmaiņa nodrošina praktisku izmantojamību: tā aizsargā disidentus no finansējuma atslēgšanas, piedāvā humanitārajām organizācijām uzticamu ceļu palīdzībai un piešķir miljardiem nebanknoto indivīdu piekļuvi globālajai digitālajai ekonomikai pirmo reizi.

Tomēr pašsuverenitāte nav pasīvs stāvoklis; tā ir aktīva prakse. Kļūšana par savu pašu banku nozīmē pilnas atbildības pieņemšanu par drošību un uzglabāšanu. Tiem, kas gatavi uzņemties šo atbildību un apgūt nepieciešamos drošības soļus, atlīdzība ir īsta, bez nosacījumiem finanšu brīvība—spēcīgs instruments pašnoteikšanai jaunajā digitālajā ekonomikā.