The cryptocurrency market operates on a schedule that differs significantly from traditional finance. Unlike stock markets that close in the evenings and on weekends, digital asset markets function twenty-four hours a day, seven days a week. This continuous operation creates a unique environment where speed and execution methods define profitability.

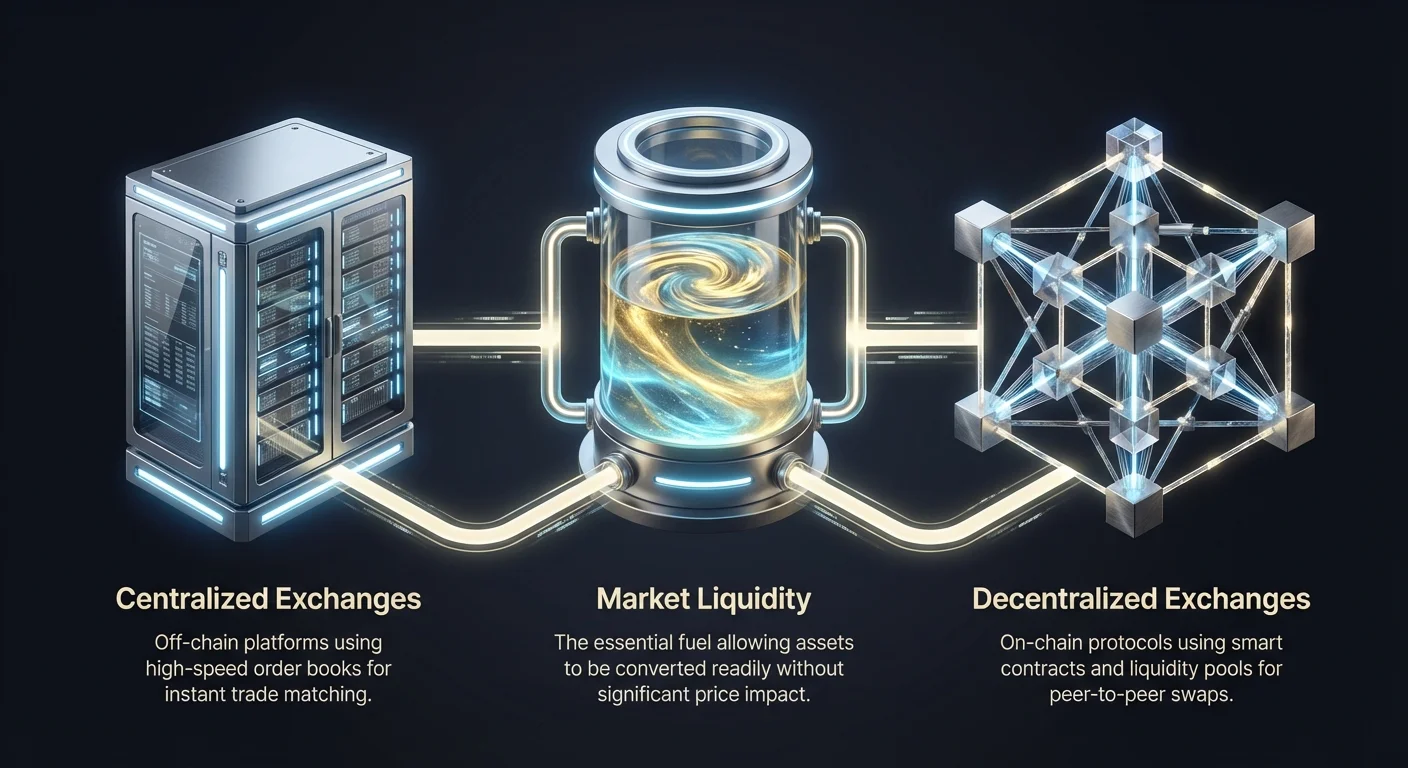

In this fast-paced ecosystem, the mechanism of exchange plays a critical role. When a user decides to trade Bitcoin for another asset, the transaction does not happen in a vacuum. It relies on a complex infrastructure of liquidity, order books, or algorithmic pools to determine the price and execute the swap. Understanding the difference between centralized and decentralized execution is vital for any participant.

The speed at which a trade settles depends heavily on the type of platform used. Centralized exchanges act as intermediaries, matching buyers and sellers off-chain to ensure near-instant execution. In contrast, decentralized platforms rely on blockchain confirmation, introducing variables such as block times and network congestion.

The Mechanics of Centralized Speed

Centralized exchanges (CEXs) function similarly to traditional stock brokerage platforms. They are businesses that facilitate transactions between two parties by maintaining a central order book. When a user deposits funds, the exchange takes custody of those assets. This custodial arrangement allows the platform to execute trades internally without waiting for blockchain confirmations for every single action.

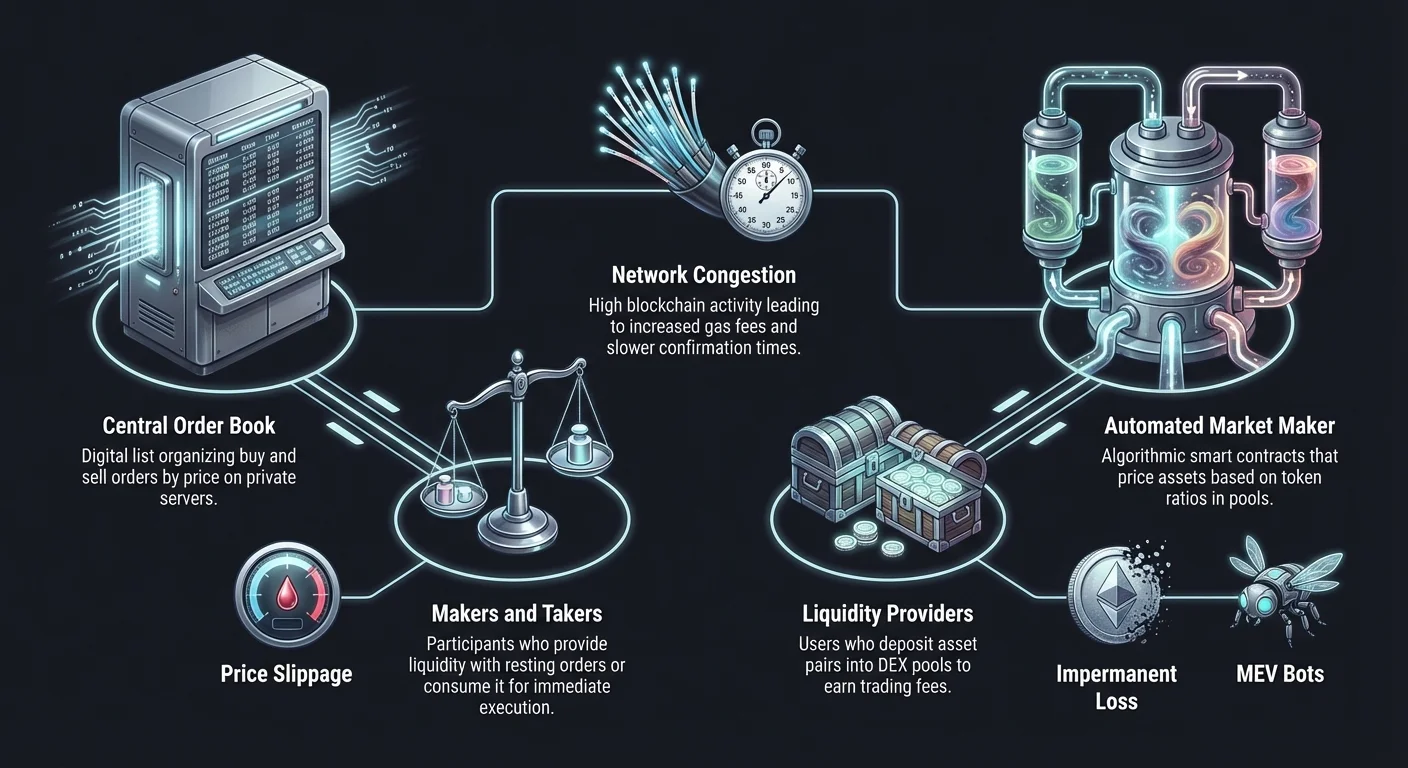

The primary engine of a CEX is the order book. This digital list records all buy and sell orders for a specific asset pair. It organizes these orders by price and size, creating a real-time map of market demand. When a trader submits a request, the exchange's matching engine scans the order book to find a corresponding offer. Because this happens on the exchange's private servers rather than the public blockchain, the process is exceptionally fast.

Makers and Takers

Market participants on these platforms are categorized into two distinct groups: makers and takers. This distinction is fundamental to understanding how liquidity is generated and consumed. Makers are traders who place orders that do not execute immediately. For example, a maker might place a limit order to buy Bitcoin at a price lower than the current market rate.

These orders sit on the order book, adding depth to the market. By waiting for the price to come to them, makers provide liquidity that others can use. Because they contribute to the health of the marketplace, exchanges often reward makers with lower trading fees.

Takers, on the other hand, are those who demand immediate execution. They look at the order book and accept the existing prices to fill their orders instantly. When a user places a market order, they are acting as a taker. They remove liquidity from the book by "taking" the available offers. Consequently, takers usually pay higher fees for the convenience of speed.

Order Types and Execution

To navigate these markets effectively, traders utilize specific order types that dictate how and when a trade occurs. The most common form is the market order. This instruction tells the exchange to buy or sell a specific amount of cryptocurrency immediately at the best available price. Market orders prioritize speed over price certainty.

In a highly liquid market, a market order will likely execute close to the last traded price. However, in fast-moving or thin markets, the final price might differ from the expectation. This discrepancy is known as slippage.

Alternatively, a limit order allows a trader to set a specific price ceiling or floor. A limit buy order indicates the maximum price a user is willing to pay. If the market never drops to that level, the trade will simply not execute. This prioritizes price precision over speed.

| Order Type | Priority | Risk Profile | Execution Speed |

|---|---|---|---|

| Market Order | Speed | Price Slippage | Immediate |

| Limit Order | Price | Non-execution | Delayed/Conditional |

| Stop-Loss | Protection | Trigger Variance | Conditional |

Decentralized Execution and On-Chain Latency

Decentralized exchanges (DEXs) offer a fundamentally different approach to market execution. Unlike their centralized counterparts, DEXs operate without a trusted intermediary. They facilitate peer-to-peer transactions directly on the blockchain using smart contracts. This structure removes the need for users to deposit funds into a custodial account, granting them full control over their private keys.

However, this decentralization introduces different latency factors. On a DEX, every trade is a transaction that must be validated by the blockchain network. This means execution speed is tied to the block time of the underlying network. On some networks, this might take seconds, while on others, it could take minutes.

The Automated Market Maker

Early decentralized exchanges attempted to mimic the order book model used by CEXs. This approach often failed because updating an order book on-chain was slow and computationally expensive. The solution that revolutionized decentralized trading was the Automated Market Maker (AMM).

AMMs replace the traditional order book with liquidity pools. A liquidity pool is a smart contract that holds reserves of two or more tokens. Instead of matching a buyer with a specific seller, the AMM allows users to trade against the pool itself. The price of the assets in the pool is determined algorithmically based on the ratio of the tokens held in the contract.

The most common formula used is $x * y = k$. In this equation, $x$ and $y$ represent the quantities of the two tokens in the pool, and $k$ is a constant value. When a trader buys one token from the pool, they increase the supply of the other token in the pool. The formula automatically adjusts the price to maintain the constant balance.

Network Congestion and Gas

Because DEX interactions occur on-chain, they require the payment of network fees, known as gas. These fees pay for the computational work required to process the smart contract. During periods of high network activity, gas prices can spike significantly.

This creates a dynamic where the cost of execution fluctuates alongside the speed. Users can often pay higher gas fees to prioritize their transactions, pushing them to the front of the block. Conversely, setting a low gas fee might result in a transaction remaining stuck in the backlog (mempool) for an extended period.

Furthermore, the public nature of these transactions creates visibility risks. Advanced trading bots monitor the mempool for large pending trades. If a bot detects a significant buy order, it can attempt to "front-run" the trade. The bot places its own buy order with a slightly higher gas fee to get processed first, driving up the price before the original user's trade executes.

Understanding Liquidity Dynamics

Liquidity is the lifeblood of any financial market, determining how easily an asset can be converted into cash or another asset. In the context of crypto speed and execution, liquidity dictates the stability of prices during a trade. A highly liquid market can absorb large orders without significant price changes.

There are two primary types of liquidity: financial liquidity and market liquidity. Financial liquidity refers to the general ease of converting an asset to cash. Major cryptocurrencies like Bitcoin and Ethereum are considered highly liquid. They can be sold for cash or stablecoins almost instantly on major platforms.

Market liquidity refers to the health of a specific trading pair on a specific exchange. For instance, the Bitcoin-USDT pair might have massive liquidity on a major exchange, allowing for multimillion-dollar trades with minimal impact. However, a niche altcoin pair on a small decentralized exchange might suffer from poor liquidity.

The Impact of Low Liquidity

When liquidity is low, execution suffers. If a trader attempts to sell a large amount of an illiquid asset, there may not be enough buyers at the current price to absorb the order. The order essentially "eats through" the order book or unbalances the liquidity pool.

This results in significant slippage. The final execution price ends up being much lower than the market price at the start of the trade. In AMMs, this is exacerbated by the pricing algorithm. A large trade shifts the ratio of tokens in the pool drastically, causing the price to slide against the trader exponentially as the order size increases relative to the pool size.

During market downturns, liquidity becomes even more critical. When volatility spikes, market participants often rush to exit positions simultaneously. This flight to safety can cause liquidity to dry up rapidly. As buyers vanish, the gap between buy and sell orders widens, causing extreme price fluctuations and making real-time execution difficult or costly.

Liquidity Pools and Providers

To solve liquidity issues in DeFi, AMMs incentivize users to become liquidity providers (LPs). LPs deposit equal values of two assets into a pool. In return, they receive a portion of the trading fees generated by that pool. This system effectively crowdsources market depth.

However, providing liquidity comes with risks, notably impermanent loss. This phenomenon occurs when the price of the deposited assets changes compared to when they were deposited. Because the AMM always sells the appreciating asset and buys the depreciating one to maintain ratios, the LP may end up with less value than if they had simply held the assets in a wallet.

Real-Time Trading Strategies

For traders operating in these real-time markets, strategy is as important as infrastructure. Day trading involves making frequent trades within a single day to capitalize on short-term price movements. This style of trading requires intense focus and rapid execution capabilities.

Day traders often rely on technical analysis to identify trends and entry points. They monitor charts and indicators to predict price movements. However, analysis is useless without the ability to execute orders swiftly. This is why many day traders prefer centralized exchanges for their high throughput and advanced order types.

Managing Volatility

Volatility is a double-edged sword. It provides the price swings necessary for profit, but it also increases the risk of rapid loss. Effective risk management is essential for survival in real-time markets. This includes position sizing—allocating only a small percentage of capital to a single trade—and the strict use of stop-loss orders.

A stop-loss is a defensive instruction. It tells the exchange to automatically sell an asset if its price drops to a certain level. This limits potential losses during sudden market crashes. In the volatile crypto environment, where double-digit percentage moves can happen in minutes, automated protection is often safer than manual execution.

The Role of Aggregators

In the decentralized sector, traders use tools called aggregators to improve execution. A DEX aggregator connects to multiple liquidity pools and exchanges simultaneously. When a user wants to make a trade, the aggregator scans all available sources to find the best price.

Aggregators can also split a single large order across multiple DEXs. By breaking the trade into smaller chunks, the aggregator minimizes the impact on any single liquidity pool. This reduces slippage and ensures the user gets a better overall rate than if they had traded on a single platform.

| Feature | Single DEX | DEX Aggregator |

|---|---|---|

| Liquidity Source | Single Protocol | Multiple Protocols |

| Price Discovery | Isolated | Global/Market-wide |

| Slippage | Variable/High | Optimized/Lower |

| Convenience | Direct Interaction | Automated Routing |

Risks in Algorithmic Execution

While AMMs and smart contracts have democratized market making, they introduce specific risks related to their algorithmic nature. One such risk is the reliance on arbitrageurs. AMMs do not automatically know the "real" global market price of an asset. They only know the ratio of assets in their own pool.

If the price of Ethereum rises on a centralized exchange, the price on the AMM will lag behind until a trader executes a swap. Arbitrageurs exploit this difference. They buy the underpriced asset on the AMM and sell it on the centralized exchange for a profit. This trading activity creates price alignment. Without these actors, the AMM price would remain disconnected from the broader market.

Smart Contract Vulnerabilities

Real-time execution on DEXs is also subject to smart contract risk. These platforms act as autonomous software programs. If there is a bug or exploit in the code, the funds locked in the liquidity pools can be drained. Unlike a centralized exchange where a company might have insurance or a recovery plan, DeFi losses are often irreversible.

Scams also proliferate in the permissionless environment of DEXs. Because anyone can list a token and create a liquidity pool, malicious actors can create fake tokens. They might provide initial liquidity to lure traders, only to pull the liquidity later in a "rug pull," leaving traders with worthless tokens that cannot be sold.

Front-Running and MEV

As mentioned earlier, the transparency of the blockchain allows for predatory behaviors like front-running. This is often referred to as Miner Extractable Value (MEV) or Maximal Extractable Value. sophisticated bots scan the network for profitable transactions waiting to be confirmed.

If a bot sees a large trade that will increase a token's price, it can insert its own transaction beforehand. The victim of this attack ends up buying at a higher price, while the bot immediately sells for a profit. This "sandwich attack" extracts value directly from the user's trade execution, acting as a hidden tax on speed and volume in decentralized systems.

Infrastructure for the Active Trader

To participate effectively in real-time crypto markets, a trader's setup extends beyond the exchange itself. The primary tool is the wallet. For frequent trading, users often utilize "hot wallets," which are connected to the internet. These can be mobile apps, desktop software, or browser extensions.

Hot wallets offer convenience and speed, allowing for quick connection to DEXs and dApps (decentralized applications). However, they are more vulnerable to online threats than "cold wallets" or hardware wallets, which keep private keys offline. Many traders use a hybrid approach: keeping long-term holdings in cold storage while moving a smaller "trading stack" to a hot wallet or exchange account for active execution.

Connectivity and Interface

The user interface (UX) of a trading platform significantly impacts execution speed. A cluttered or confusing interface can lead to errors, such as entering the wrong price or mistaking a buy order for a sell order. Top-tier exchanges invest heavily in designing intuitive dashboards that display order books, charts, and trade history clearly.

For decentralized trading, the connection between the wallet and the web interface is crucial. Protocol bridges like WalletConnect allow secure interaction between mobile wallets and desktop dApps. A stable internet connection and a responsive device are non-negotiable requirements for anyone attempting to trade volatility in real-time.

Conclusion

The speed of crypto is not defined by a single metric but by the interplay of various technological and economic factors. Centralized exchanges offer the familiarity and velocity of traditional matching engines, utilizing high-speed servers to connect makers and takers instantly. This model favors high-frequency strategies and provides deep liquidity for major assets, though it requires trust in a central custodian.

Decentralized exchanges have introduced a novel paradigm where code replaces the middleman. Through Automated Market Makers and liquidity pools, they enable continuous, permissionless trading. While variables like network congestion and block times can introduce latency, innovations like aggregators and arbitrage incentives work to maintain market efficiency.

Ultimately, successful market execution requires navigating the trade-offs between speed, security, and cost. Whether utilizing the instant order books of a CEX or the algorithmic pricing of a DEX, understanding the underlying mechanics is essential. Liquidity remains the constant fuel for both systems, ensuring that digital value can move freely and rapidly across the ecosystem.

True market speed comes from understanding the mechanism behind the trade.