The financial landscape is undergoing a radical transformation driven by the digitization of value. For centuries, traditional money has served as a medium of exchange and a store of value, but the emergence of blockchain technology has introduced new competitors to the global stage. At the forefront of this shift is the tension between decentralized cryptocurrencies, such as Bitcoin, and pegged digital assets designed to maintain a stable value. This evolution has created a dynamic ecosystem where volatility competes with stability, and decentralized governance challenges centralized control.

Understanding this battle for digital value requires a deep dive into the mechanics of how these assets function. It is not merely a question of which currency is superior, but rather how different types of digital assets serve distinct purposes within the economy. From the pioneering days of Bitcoin to the complex utility of modern tokens, the market has expanded into a diverse array of financial instruments.

The rapid growth of this sector has led to the creation of stablecoins, which aim to combine the speed and security of cryptocurrency with the price stability of fiat currency. These assets solve one of the primary hurdles facing early crypto adoption: volatility. By pegging their value to external assets like the US dollar, stablecoins have become a critical bridge between the traditional financial world and the burgeoning decentralized economy.

However, this bridge is not without its complexities. As these technologies mature, they face increasing scrutiny regarding regulation, security, and their role in the broader financial system. The distinction between a decentralized coin and a token running on another network becomes vital for investors and users navigating this space. To truly grasp the stakes of this battle for digital value, one must first understand the foundational elements that power these digital economies.

The Architecture of Digital Value

The terminology used in the cryptocurrency space can often be confusing for newcomers. Words like "coin," "token," and "altcoin" are frequently used interchangeably, yet they represent fundamentally different technologies and use cases. Understanding these distinctions is essential for evaluating the potential and risks of any digital asset. At the most basic level, the industry divides assets based on their relationship to the underlying blockchain infrastructure.

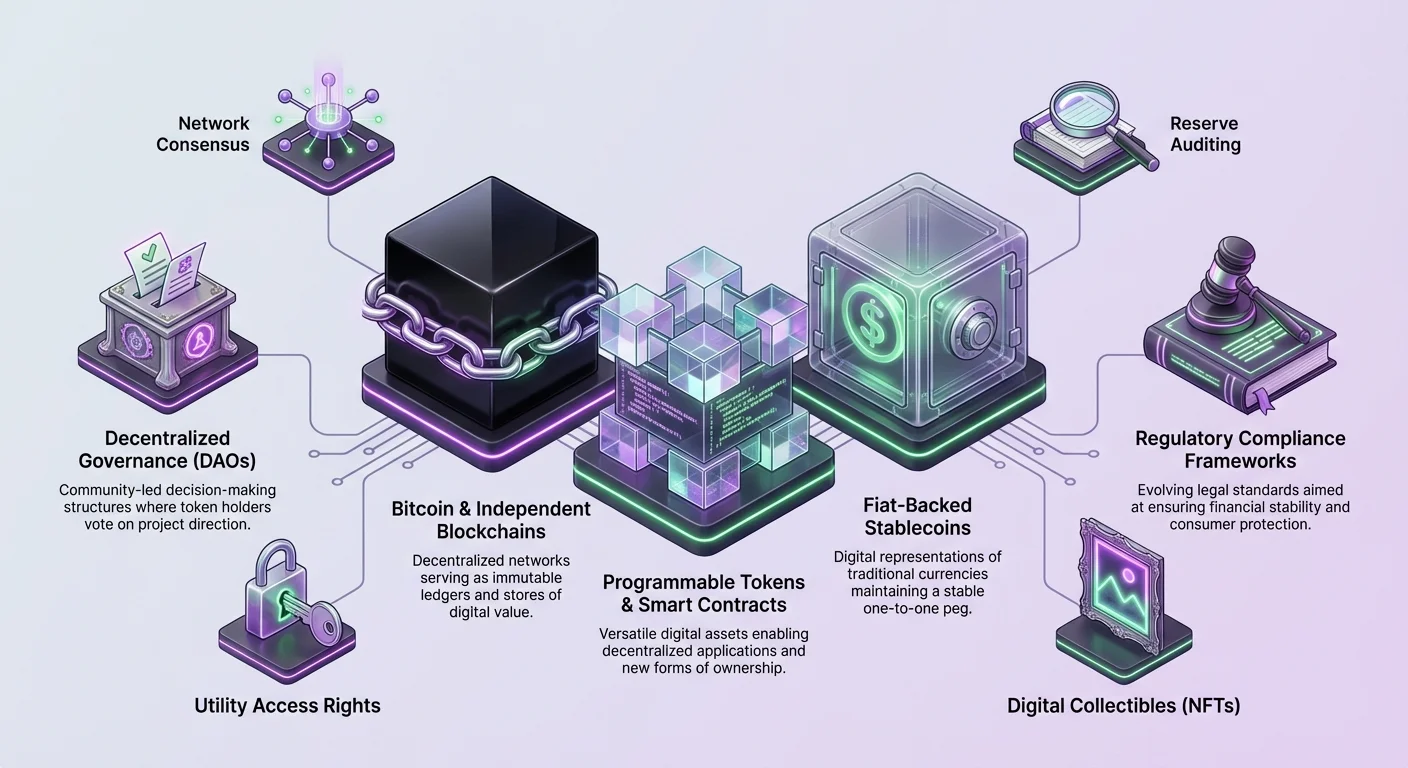

Coins: The Native Assets

A coin is a cryptocurrency that operates on its own independent blockchain. Bitcoin is the prime example of this. Launched in 2009, it pioneered the concept of decentralized digital currency and established the first secure, immutable ledger. Coins act as the foundational currency for their specific networks. They are used to pay transaction fees, secure the network through mining or validation, and serve as a base unit of account within that ecosystem.

Because coins exist at the protocol level, they are deeply tied to the health and security of their respective networks. For instance, Ether (ETH) is the native coin of the Ethereum blockchain, and SOL is the native coin of the Solana network. These assets are generated by the consensus rules of the protocol itself, rather than by external applications. Their primary role is to incentivize the participants who maintain the network's integrity, such as miners or validators.

The independence of a coin means that it does not rely on another blockchain’s infrastructure to function. This autonomy provides a high level of security, as the asset is protected by its own consensus mechanism. However, this also means that creating a new coin requires building a new blockchain from scratch, a process that demands significant technical resources and community adoption to succeed.

Tokens: The Application Layer

In contrast to coins, tokens are digital assets built on top of existing blockchains. They leverage the security and technological framework of the host network rather than establishing their own. This allows developers to create new assets quickly and efficiently without the need to bootstrap a new decentralized network of validators.

Tokens are typically created using smart contracts, which are self-executing pieces of code that define the rules and behaviors of the asset. For example, the Ethereum blockchain hosts thousands of different tokens that adhere to specific standards, such as ERC-20. These tokens can represent anything from a currency to a vote in a governance system, or even ownership of a unique digital item.

The flexibility of tokens has unleashed a wave of innovation in the crypto space. Projects can launch utility tokens that grant access to specific services, or governance tokens that allow holders to vote on project decisions. Because they live on established chains like Ethereum or Solana, tokens benefit from the robust security and decentralization of the underlying layer while offering specialized functionality that native coins may not provide.

The Blurring Lines of Classification

While the technical distinction between coins and tokens is clear, the lines can sometimes blur in practice. Some assets start as tokens on one chain and eventually migrate to their own blockchain, effectively becoming coins. A notable example is BNB, which launched as a token on the Ethereum network before moving to its own dedicated chain.

Furthermore, the rise of Layer 2 networks has introduced new complexities. These networks operate on top of main blockchains to improve speed and reduce costs, issuing their own assets that function independently but rely on the main chain for final settlement. This evolution highlights the fluid nature of the crypto ecosystem, where technical definitions must adapt to rapid technological advancements.

The Rise of Stablecoins

As the cryptocurrency market expanded, the extreme volatility of assets like Bitcoin became a barrier to their use as everyday money. While Bitcoin proved to be an excellent store of value and a speculative investment, its price swings made it difficult to use for pricing goods or paying salaries. This challenge led to the development of stablecoins, a class of cryptocurrencies designed specifically to maintain a steady value.

Mechanisms of Stability

Stablecoins aim to hold a consistent value, most commonly pegged 1:1 to the US dollar. This peg provides a familiar unit of account for users while retaining the benefits of blockchain technology, such as 24/7 availability and rapid transaction settlement. To achieve this stability, these assets employ various mechanisms to ensure their value does not deviate from their target.

The most common type of stablecoin is backed by reserves of fiat currency or equivalent assets. In this model, a central issuer holds physical dollars or liquid assets in a bank account to back every digital token issued on the blockchain. This allows users to redeem their tokens for fiat currency, theoretically guaranteeing the value. Other mechanisms include crypto-collateralized stablecoins, which use over-collateralized positions of other cryptocurrencies to maintain their peg, and algorithmic stablecoins, which use code to adjust supply and demand dynamically. Comparing Collateralization Models.

The Utility of Pegged Value

The primary advantage of stablecoins is their ability to facilitate everyday transactions without the risk of price depreciation during the transfer. This makes them ideal for remittances, allowing individuals to send money across borders efficiently and cost-effectively without the high fees and slow processing times associated with traditional banking.

Beyond payments, stablecoins have become the lifeblood of the Decentralized Finance (DeFi) ecosystem. In DeFi, users can lend, borrow, and trade assets without intermediaries. Stablecoins provide a stable medium of exchange within these protocols, allowing traders to move in and out of volatile positions without leaving the crypto ecosystem. They act as a safe harbor during periods of market turbulence, preserving capital while keeping funds ready for future opportunities.

Risks and Centralization

Despite their utility, stablecoins introduce risks that are distinct from decentralized cryptocurrencies like Bitcoin. Many prominent stablecoins are issued by centralized entities, which reintroduces the concept of custodial risk. Users must trust the issuer to manage the reserves responsibly and to honor redemptions. This centralization is a point of contention in a broader industry focused on decentralization.

Furthermore, stablecoins face increasing regulatory scrutiny. Governments and financial regulators are closely monitoring these assets to ensure they comply with laws regarding money laundering and reserve transparency. The potential for regulatory changes creates uncertainty, as new rules could impact how these assets are issued and used. Additionally, there is always the technical risk that a stablecoin could lose its peg, decoupling from its target value and causing financial losses for holders.

The Tokenization of Everything

The technology that underpins stablecoins—smart contracts on a blockchain—has opened the door to a much broader application: tokenization. A token is not just a form of currency; it is a programmable container for value. This capability allows for the representation of virtually any asset or right on a decentralized ledger, fundamentally changing how ownership and access are managed in the digital age.

Utility and Access

Utility tokens are among the most common types of digital assets. They function like digital coupons or keys, granting the holder access to a specific product or service within a blockchain ecosystem. For example, a decentralized cloud storage network might require users to pay in a specific native token to store their data.

These tokens drive the internal economies of decentralized applications (dApps). They incentivize users to participate in the network, whether by providing resources, curating content, or validating transactions. The value of a utility token is inextricably linked to the demand for the underlying service it unlocks. As the platform grows and more users seek access, the demand for the token increases.

Governance and Community Control

Another significant innovation is the governance token. These assets empower holders to participate in the decision-making processes of a project. Unlike traditional corporate structures where decisions are made by a board of directors, decentralized protocols often allow token holders to propose and vote on changes to the software or the management of the community treasury.

Governance tokens represent a shift toward decentralized autonomous organizations (DAOs). In a DAO, the rules of the organization are encoded in smart contracts, and governance tokens act as voting shares. This model democratizes control, allowing the community of users and investors to steer the direction of the project. It aligns the incentives of the developers with the users, as both parties have a stake in the platform's success.

Security Tokens and Real-World Assets

Security tokens represent a bridge between traditional finance and blockchain technology. These tokens are digital representations of ownership in real-world assets, such as shares in a company, real estate, or commodities. Unlike utility tokens, security tokens are designed to be investments and are subject to strict regulatory requirements.

By tokenizing securities, issuers can offer fractional ownership, allowing investors to buy small portions of high-value assets like commercial property or fine art. This increases market liquidity and makes investment opportunities more accessible to a broader audience. Furthermore, security tokens can automate compliance through smart contracts, ensuring that trading restrictions and dividend distributions are executed programmatically.

Non-Fungible Tokens (NFTs)

While most tokens are fungible, meaning they are identical and interchangeable, Non-Fungible Tokens (NFTs) represent unique items. Each NFT has a distinct digital signature that verifies its authenticity and ownership history. This technology has revolutionized the digital art and collectibles market by providing a way to prove ownership of digital files.

NFTs are not limited to art; they can represent virtual real estate, gaming items, or even identity credentials. In the context of the battle for digital value, NFTs demonstrate that value is not solely derived from currency or utility but also from scarcity, provenance, and cultural significance. They expand the definition of what can be owned and traded on a blockchain.

Bitcoin vs. Stablecoins: The Value Proposition

Comparing Bitcoin to stablecoins illuminates the two distinct philosophies dominating the crypto market. Bitcoin functions as a store of value and a hedge against inflation, often referred to as "digital gold." Its value is derived from its fixed supply of 21 million coins and the security of its decentralized network. It is designed to be censorship-resistant and independent of any central authority.

Stablecoins, on the other hand, function as a medium of exchange and a unit of account. They are the "digital dollar." Their value is derived from the trust in the issuer and the reserves backing the asset. While Bitcoin offers the potential for significant price appreciation, it also carries high volatility. Stablecoins offer zero price appreciation potential but provide the stability necessary for day-to-day commerce.

| Feature | Bitcoin | Stablecoins |

|---|---|---|

| Primary Purpose | Store of value, long-term investment | Medium of exchange, payment settlement |

| Supply Mechanism | Fixed algorithmically (21M cap) | Variable based on demand/reserves |

| Issuer | Decentralized network (No issuer) | Centralized entity or protocol |

The investment considerations for these two asset classes are vastly different. Investors hold Bitcoin with the expectation that its scarcity will drive up its purchasing power over time. It is a bet on the future adoption of a decentralized monetary standard. Conversely, holding stablecoins is a defensive strategy used to preserve capital or to facilitate active trading. They yield no profit from holding unless deposited into a lending protocol to earn interest.

The choice between the two often depends on the user's risk tolerance and goals. A long-term investor might favor Bitcoin for its growth potential, accepting the short-term volatility. A merchant or a trader might prefer stablecoins for their predictability and ease of use in transactions. Both assets play complementary roles in the ecosystem, catering to different needs within the digital economy.

The Regulatory Landscape and Future Outlook

The battle for pegged digital value is not just technological; it is increasingly political. As stablecoins and tokens grow in popularity, they have caught the attention of regulators worldwide. Governments are grappling with how to integrate these digital assets into existing legal frameworks without stifling innovation.

The Push for Regulation

Regulatory bodies are concerned about consumer protection, financial stability, and the potential for illicit use of cryptocurrencies. The lack of clear rules has historically created uncertainty, but guidelines are now becoming more defined. For stablecoins, the focus is heavily on reserve auditing and redemption guarantees. Regulators want to ensure that for every digital dollar issued, there is a real dollar available to back it.

This regulatory pressure is driving the market toward more transparent and compliant solutions. It is likely that the future landscape will be dominated by stablecoins that fully adhere to government standards. This may lead to a consolidation of the market, where only the most compliant and well-capitalized issuers survive.

Centralization vs. Decentralization

The increased involvement of regulators highlights the tension between centralization and decentralization. While Bitcoin remains highly resistant to control due to its decentralized architecture, stablecoins and many tokens have central points of failure. Issuers can freeze funds or blacklist addresses to comply with legal orders.

This reality challenges the original ethos of cryptocurrency, which sought to create unstoppable money. However, for many users, the convenience and legal safety of regulated stablecoins outweigh the ideological compromise. This dichotomy suggests a future where decentralized assets like Bitcoin coexist alongside regulated, centralized digital currencies, each serving different segments of the market.

Innovation and Adoption

Looking ahead, the future of altcoins and tokens depends on continued technological advancement and adoption. Innovations in scalability, such as the Lightning Network for Bitcoin and various Layer 2 solutions for Ethereum, are addressing the limitations of early blockchain networks. These improvements make digital assets faster and cheaper to use, paving the way for mass adoption.

Real-world use cases are also expanding. From supply chain tracking to decentralized voting systems, the utility of tokens is moving beyond speculation. As traditional institutions continue to explore blockchain technology, we can expect to see more hybrid models that blend the efficiency of distributed ledgers with the safeguards of traditional finance.

Conclusion

The landscape of digital value is vast and multifaceted, defined by the interplay between native coins, versatile tokens, and the stabilizing force of pegged assets. Bitcoin remains the unshakeable anchor of the industry, offering a decentralized alternative to traditional money and a hedge against inflation. Its fixed supply and autonomous nature secure its position as a digital store of value.

In parallel, stablecoins have carved out a critical niche by solving the problem of volatility, enabling seamless payments and fueling the decentralized finance sector. They serve as the pragmatic bridge for users entering the crypto space, prioritizing utility and stability over speculative growth. Meanwhile, the explosion of utility and governance tokens demonstrates that blockchain technology is about more than just money; it is about redefining ownership, access, and community governance.

As the industry matures, the friction between decentralized ideals and regulatory realities will continue to shape the market. Whether through the adoption of strictly regulated stablecoins or the continued resilience of decentralized coins, the ecosystem is evolving toward a more sophisticated and integrated financial future.

The future of finance lies in choosing the right digital tool for the specific economic task at hand.