The landscape of digital asset acquisition has evolved significantly since the inception of blockchain technology. While the underlying networks operate globally on decentralized protocols, the access points for individuals often depend on local infrastructure and banking regulations. Investors and users must navigate a variety of platforms to find the most efficient route for buying, selling, and trading cryptocurrencies. These pathways range from centralized corporate entities to direct peer-to-peer interactions that bypass traditional financial intermediaries.

Understanding the distinctions between these access points is crucial for anyone looking to participate in the digital economy. Each method offers a different balance of convenience, privacy, fee structures, and control over assets. For some, a regulated exchange connected to a local bank account offers the smoothest experience. For others, particularly in regions with limited banking infrastructure, peer-to-peer marketplaces provide essential liquidity.

The choice of platform impacts not only the cost of acquisition but also the security of funds. Users must weigh the benefits of high liquidity and customer support against the risks of third-party custody. Simultaneously, the rise of decentralized protocols has introduced automated ways to swap assets without any human intermediary. By comprehending these diverse mechanisms, participants can tailor their approach to suit their specific financial needs and geographical constraints.

The Role of Centralized Platforms

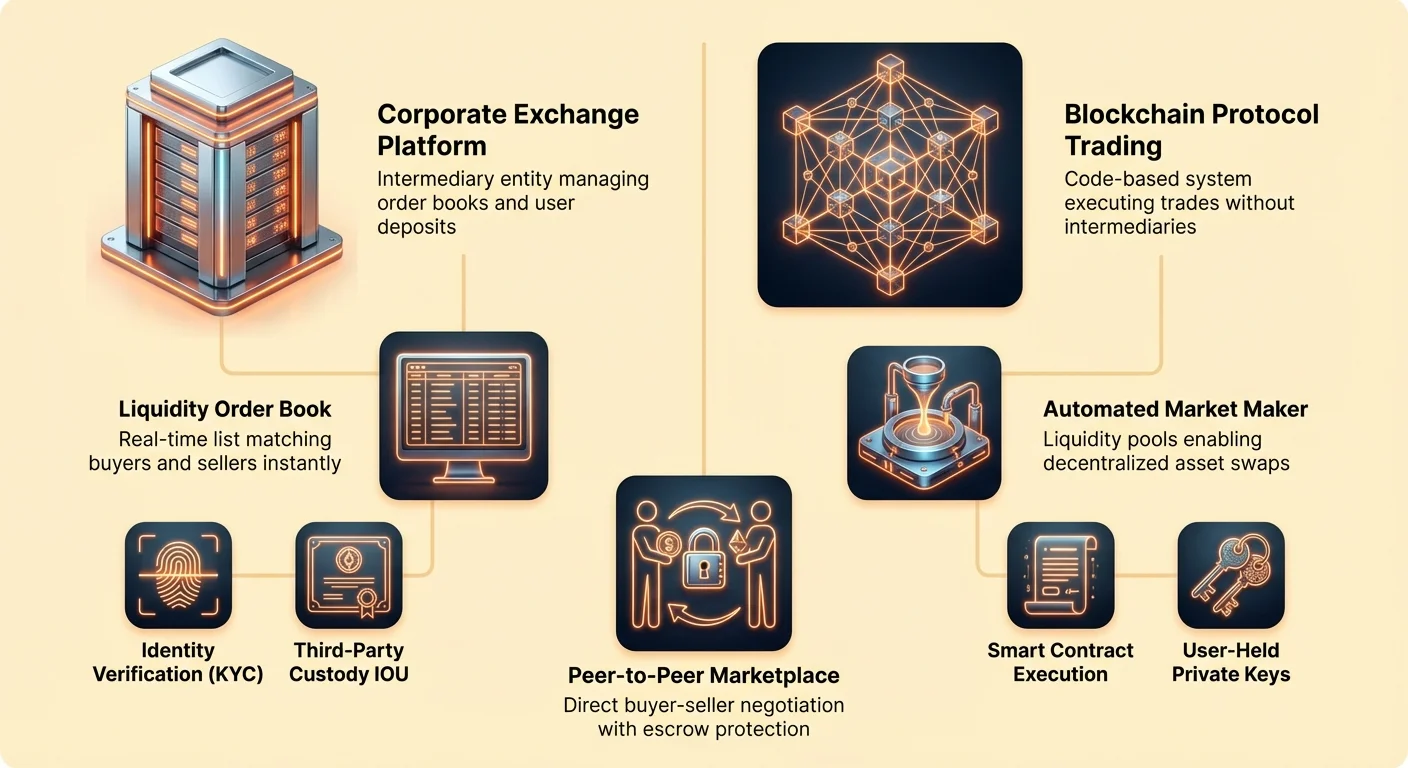

Centralized exchanges (CEXs) represent the most common entry point for new market participants. These platforms function as intermediaries, matching buyers with sellers within a closed system. They operate similarly to traditional stock brokerages or banks. The exchange maintains an order book, which is a real-time list of buy and sell orders for various assets. When a user places a request to buy Bitcoin, the exchange’s engine finds a corresponding seller to complete the transaction.

This model offers high liquidity, meaning users can typically buy or sell large amounts of an asset without causing significant price shifts. Because the platform aggregates orders from thousands or millions of users, trades execute almost instantly at predictable market rates. These entities often provide fiat on-ramps, allowing users to deposit government-issued currency via bank transfers or credit cards.

However, this convenience comes with a trade-off regarding control. When funds are deposited onto a centralized platform, the user effectively hands over custody to the company. The user does not hold the private keys to those assets. Instead, they hold an IOU from the exchange. This structure requires users to trust that the platform remains solvent and secure against external threats, highlighting the spectrum of custody risks.

Decentralized Exchange Protocols

In contrast to the corporate structure of centralized platforms, decentralized exchanges (DEXs) operate without a central authority. These platforms run on code, utilizing smart contracts to facilitate trading directly between users. There is no company ensuring the trade happens; rather, the blockchain protocol itself executes the transaction. This aligns with the core ethos of cryptocurrency, promoting disintermediation and user sovereignty.

DEXs do not take custody of user funds. Instead, users connect their personal digital wallets directly to the protocol. When a trade occurs, assets move from the user's wallet to the smart contract and back, ensuring the user retains control of their private keys throughout the process. This model eliminates the risk of an exchange freezing accounts or blocking withdrawals, as the protocol operates permissionlessly.

Liquidity on these platforms is often sourced from users themselves. Through a mechanism known as an Automated Market Maker (AMM), individuals deposit pairs of assets into liquidity pools. Traders then swap against these pools rather than matching with a specific counterparty. While this innovation has solved early liquidity issues for DEXs, it introduces different fee structures and technical complexities compared to centralized alternatives.

Peer-to-Peer Trading Dynamics

Peer-to-peer (P2P) exchanges offer a distinct alternative by connecting buyers and sellers directly. Unlike a standard exchange that uses an order book to match anonymous orders, P2P platforms function more like a marketplace or classifieds listing. Users post offers stating the amount of cryptocurrency they wish to buy or sell and the specific terms of the deal.

This method provides exceptional flexibility regarding payment methods. Since the trade happens between two individuals, they can agree to settle the fiat portion of the transaction using almost any medium. This includes bank transfers, cash in person, digital payment apps, or even gift cards. This flexibility makes P2P trading vital in regions where banking support for crypto is restricted or nonexistent.

To mitigate the risk of one party failing to honor the deal, P2P platforms utilize escrow services. When a trade is initiated, the seller’s cryptocurrency is temporarily locked in a secure account held by the platform. The assets are only released to the buyer once the seller confirms receipt of the payment. This system allows strangers to trade with a higher degree of confidence, reducing the potential for fraud.

The Mechanics of Market Liquidity

Liquidity is a fundamental concept that dictates the efficiency of any exchange. It refers to the ease with which an asset can be converted into cash or another asset without affecting its price. In a highly liquid market, there are many participants ready to buy and sell. This results in tight spreads, which is the difference between the highest price a buyer is willing to pay and the lowest price a seller is willing to accept.

Bitcoin typically commands the highest liquidity among cryptocurrencies due to its massive network of participants and trading volume. However, liquidity varies significantly across different platforms. A large centralized exchange may have billions of dollars in daily volume, ensuring that a user buying $1,000 worth of Bitcoin gets the global market price. Conversely, a small P2P marketplace may have fewer sellers, leading to price disparities or premiums.

Market participants are categorized into two roles: makers and takers. Makers are those who place limit orders that do not fill immediately. They add liquidity to the order book by stating a specific price they are willing to wait for. Takers are those who accept existing orders on the book, usually via market orders. Takers remove liquidity from the exchange. Consequently, many platforms incentivize makers with lower trading fees while charging takers slightly higher rates.

Financial Bridges and Payment Cards

While exchanges facilitate the acquisition of digital assets, spending them in the traditional economy often requires a bridge. Bitcoin debit cards and crypto-linked payment cards serve this purpose. These financial tools allow users to spend their cryptocurrency holdings at any merchant that accepts major credit card networks like Visa or Mastercard. They effectively translate digital assets into fiat currency at the point of sale.

These cards function in two primary ways. Some operate as prepaid cards where the user must manually convert crypto to fiat and load the balance onto the card before use. Others offer auto-conversion features. In the auto-convert model, the user keeps their balance in cryptocurrency. When a purchase is made, the exact amount needed is instantly sold for fiat to settle the transaction with the merchant.

This integration provides utility for digital assets beyond speculative trading. It allows for the seamless purchase of everyday items, from groceries to fuel, using blockchain-based wealth. However, users must remain aware of the tax implications. In many jurisdictions, every swipe of a crypto card that results in a sale of assets is considered a taxable event, potentially complicating financial reporting.

| Feature | Prepaid Crypto Card | Auto-Convert Card |

|---|---|---|

| Funding | Manual load required | Linked to crypto wallet |

| Conversion | Occurs before purchase | Occurs at point of sale |

| Flexibility | Fixed fiat balance | Spend crypto directly |

Transaction Fees and Network Costs

Every interaction with a blockchain network incurs a cost. These network fees are separate from the trading fees charged by exchanges. Network fees are paid to the miners or validators who process transactions and secure the blockchain. They serve as an incentive for these participants to include a user's transaction in the next block of data added to the chain.

The cost of these fees is determined by supply and demand for block space. When a network is congested with many users trying to transact simultaneously, fees rise as users bid against each other to get their transactions processed quickly. Conversely, during periods of low activity, fees can be negligible. This dynamic is particularly visible on networks like Ethereum, where gas fees can fluctuate wildly based on network usage.

Users often have the ability to customize these fees in self-custodial wallets. By opting to pay a higher fee, a user can prioritize their transaction for faster confirmation. If speed is not a priority, setting a lower fee can save money, though it risks the transaction taking longer to confirm. Centralized exchanges, however, often charge a flat withdrawal fee that averages out these network costs, providing less flexibility but more predictability.

Understanding Addresses and Transfers

Sending and receiving digital assets requires precise knowledge of public addresses. A crypto address acts similarly to a bank account number or an email address for the blockchain. It is a string of alphanumeric characters derived from the user's public key. Because blockchain transactions are irreversible, accuracy when inputting this address is paramount. Sending funds to the wrong string of characters usually results in permanent loss.

To simplify this process, modern wallets and exchanges utilize QR codes. Scanning a recipient's QR code eliminates the risk of typographical errors associated with manual entry. Additionally, shareable links are emerging as a user-friendly alternative for specific assets. These allow a sender to generate a URL that, when clicked by the recipient, facilitates the transfer without the sender needing to know the recipient's complex alphanumeric address beforehand.

When moving funds from an exchange to a personal wallet, users engage in a withdrawal process. This moves the asset from the exchange's omnibus wallet (where they hold funds for many users) to the user's specific address. This on-chain transaction incurs network fees and is subject to the security protocols of the exchange, which may include confirmation delays or identity verification steps.

Identity Verification Standards

Regulated exchanges are bound by strict compliance laws designed to prevent financial crimes. Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations require these platforms to verify the identity of their users. This process typically involves submitting government-issued identification, such as a passport or driver’s license, and sometimes proof of address.

This verification creates a digital footprint linking a user's real-world identity to their on-chain activity. For many investors, this is an acceptable trade-off for the security and legal protections offered by regulated entities. It ensures that the exchange operates within the law and can offer recourse in certain dispute scenarios.

However, this requirement creates barriers for the unbanked or those lacking formal documentation. It also raises privacy concerns for individuals who prefer to keep their financial activities discreet. P2P platforms and DEXs often offer alternative routes that may require less stringent verification, though they place more responsibility on the user to ensure the legitimacy of their counterparties and the security of their own data.

The Philosophy of Custody

The concept of custody is central to the ethos of cryptocurrency. "Not your keys, not your coins" is a prevalent maxim that highlights the risks of leaving assets on centralized platforms. When funds are stored on an exchange, the user relies on that third party's security measures. If the exchange is hacked, goes bankrupt, or faces regulatory seizure, the user's funds may be lost or frozen.

Self-custody involves holding assets in a private wallet where the user controls the private keys. This grants the user absolute sovereignty over their funds. Transactions cannot be censored, and accounts cannot be frozen by any external authority. However, this freedom comes with absolute responsibility. If a user loses their private keys or recovery phrase, there is no customer support line to restore access; the funds are lost forever.

Wallets come in various forms to suit different needs. Hardware wallets, or cold storage, act as physical vaults that keep private keys offline, offering the highest security against remote hacks. Software wallets, or hot wallets, reside on mobile devices or desktops, providing convenience for frequent trading and spending but requiring vigilant digital hygiene to prevent unauthorized access.

Global Versus Local Trading Nuances

The cryptocurrency market operates 24 hours a day, 7 days a week, ignoring national borders. However, the experience of acquiring assets varies locally. In some regions, users can easily link a bank account to a major exchange and buy assets instantly. In other areas, banking restrictions prevent direct transfers to crypto companies.

This discrepancy drives the popularity of local and P2P exchanges. These platforms adapt to the specific payment habits of a region. For example, in areas where cash is dominant, P2P trades facilitated by local agents or in-person meetups provide the primary on-ramp. In regions with robust mobile money ecosystems, trades are often settled via SMS-based payment networks.

Bitcoin ATMs also bridge this gap physically. These kiosks allow users to insert cash and receive Bitcoin directly to a digital wallet. While they often charge higher fees compared to online exchanges, they offer immediate access without the need for bank accounts or lengthy registration processes. This physical infrastructure is crucial for bringing digital assets to the unbanked population.

Navigating Volatility and Stablecoins

Cryptocurrencies are known for their price volatility. Values can swing dramatically within short periods, presenting both opportunities and risks for traders. To manage this volatility, many users utilize stablecoins. These are digital assets pegged to the value of a stable fiat currency, typically the US Dollar.

Stablecoins allow traders to exit a volatile position without leaving the cryptocurrency ecosystem. Instead of selling Bitcoin for fiat and withdrawing it to a bank—a process that can take days and incur fees—a trader can swap Bitcoin for a stablecoin like USDT or USDC in seconds. This preserves the capital in a digital format, ready to be deployed again when market conditions change.

This mechanism is particularly useful on DEXs, where fiat withdrawals are not possible. Stablecoins serve as the quote currency for most trading pairs, allowing decentralized traders to measure profit and loss in stable terms. They also facilitate efficient transfer of value between exchanges, as moving a stablecoin is often faster and cheaper than moving fiat currency through the banking system.

Advanced Trading Mechanisms

Beyond simple buying and selling, the crypto ecosystem offers sophisticated trading instruments. Futures and options markets allow traders to speculate on the future price of assets without owning the underlying coins. These derivatives can be used to hedge against risk or to amplify potential returns through leverage.

Leverage allows a trader to control a large position with a relatively small amount of capital. For instance, with 10x leverage, a trader can open a position worth $10,000 using only $1,000 of their own funds. While this magnifies profits if the market moves favorably, it also magnifies losses. If the market moves against the position, the trader risks liquidation, where the exchange automatically closes the trade and seizes the collateral to cover the loss. Understanding these risks requires knowledge of leverage trading mechanics.

Automated trading strategies have also become accessible to retail investors. Copy trading allows users to automatically mirror the buy and sell orders of experienced traders. Algorithmic bots can execute trades based on predefined criteria, such as price movements or technical indicators, operating tirelessly day and night. These tools can help remove emotional decision-making from the trading process.

Swapping and Cross-Chain Operations

Swapping refers to the direct exchange of one cryptocurrency for another. In the early days, this often required moving through Bitcoin or Ethereum as a base pair. Today, modern platforms allow for direct swaps between a vast array of assets. This capability is essential for portfolio diversification and accessing new projects.

Cross-chain swaps address the issue of interoperability. Different blockchains, like Bitcoin and Solana, operate on incompatible protocols. They cannot speak to each other directly. Bridges and specialized exchanges allow users to move value across these distinct networks. This might involve "wrapping" an asset, where a token representing Bitcoin is issued on the Ethereum network, allowing it to be used in Ethereum-based applications.

The efficiency of a swap depends on the liquidity available for that specific pair. On a centralized exchange, the matching engine handles this instantly. On a DEX, the trade interacts with a liquidity pool. If the pool is small relative to the trade size, the user may experience slippage, receiving slightly less of the target asset than expected due to the price impact of their own order.

Security Best Practices

Regardless of the platform used, security is the paramount concern for any crypto user. The irreversible nature of blockchain transactions makes the industry a target for scammers and hackers. Protecting assets requires a proactive approach to digital hygiene.

Two-factor authentication (2FA) is a mandatory layer of defense for any exchange account. This ensures that even if a password is compromised, an attacker cannot access the account without a secondary code, usually generated by an app on the user's mobile device. SMS-based 2FA is considered less secure than app-based authenticators due to the risk of SIM swapping attacks.

Phishing remains a common threat. Malicious actors create fake websites or social media profiles that mimic legitimate exchanges to trick users into revealing their login credentials or private keys. Users should always verify the URL of the platform they are visiting and never share their recovery phrase with anyone, under any circumstances. No legitimate support agent will ever ask for a private key.

The Future of Access

The infrastructure for acquiring and trading digital assets continues to mature. The lines between traditional finance and the crypto economy are blurring. Banks are beginning to offer crypto custody services, while crypto platforms are issuing debit cards and offering interest-bearing accounts.

Simultaneously, decentralized technology is becoming more user-friendly. Wallet interfaces are improving, abstracting away the complex alphanumeric addresses and network settings that confuse beginners. Layer-2 solutions are reducing transaction costs, making it economically viable to use Ethereum and Bitcoin for smaller, everyday transfers.

As these technologies converge, the friction involved in finding global access is reducing. The goal is a seamless financial layer where moving value across the world is as easy as sending an email, regardless of whether the user prefers a regulated bank-like experience or a private, sovereign peer-to-peer interaction.

Conclusion

Navigating the world of cryptocurrency acquisition and sales requires a nuanced understanding of the available tools. From the high-speed order books of centralized exchanges to the private, direct negotiations of peer-to-peer marketplaces, each method serves a distinct purpose. Centralized platforms offer speed, liquidity, and ease of use, making them ideal for beginners and high-volume traders. Conversely, decentralized and P2P options provide essential privacy, autonomy, and access in regions underserved by traditional banking.

Ultimately, the choice of platform dictates the user's level of control and security. Bridges like crypto debit cards and stablecoins further enhance utility, allowing digital assets to function within the traditional economy. By mastering these diverse access points and adhering to strict security practices, individuals can effectively participate in the global digital asset market.

Choose the exchange method that aligns with your need for control, privacy, and convenience.