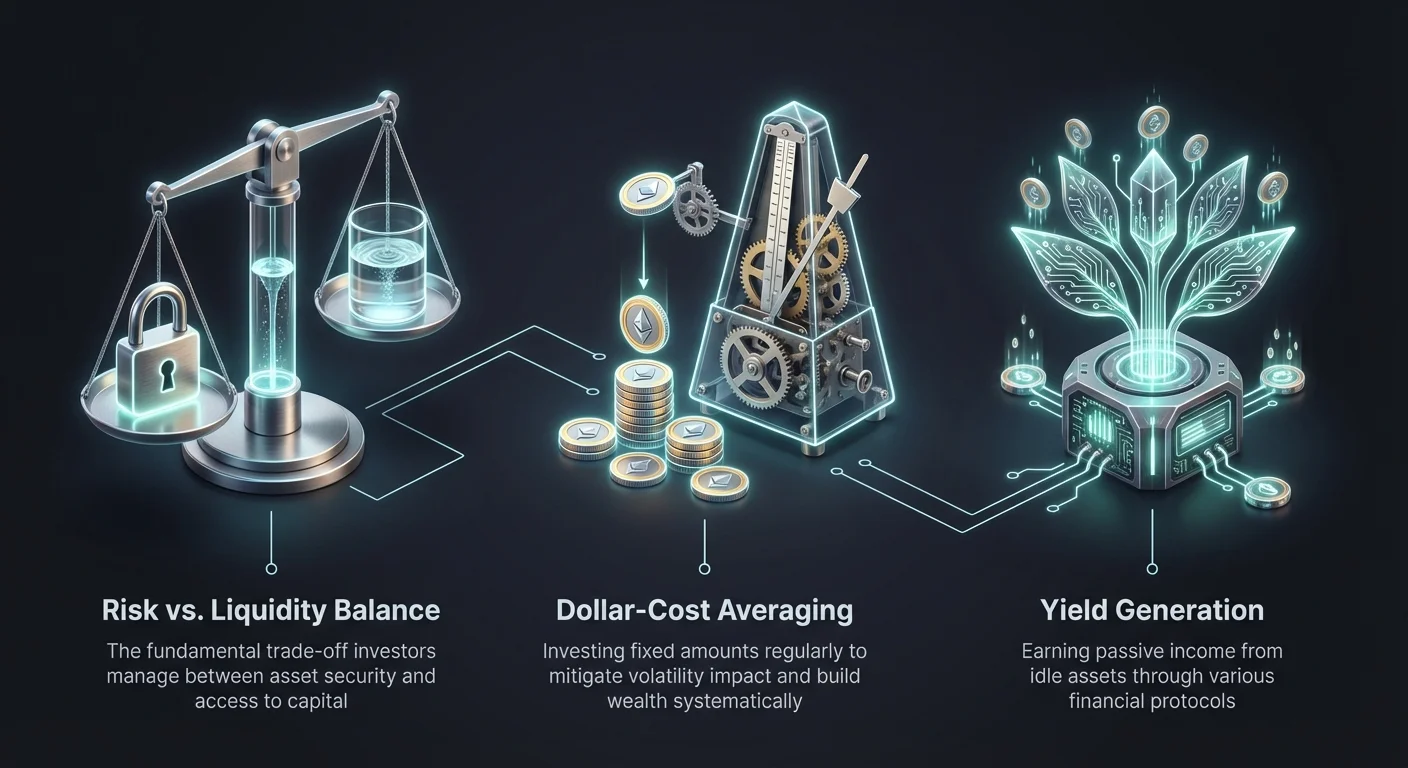

Designing a robust investment strategy in the cryptocurrency ecosystem requires a fundamental understanding of two opposing forces: risk and liquidity. Passive income strategies are not merely about selecting an asset with a high yield. They involve constructing a framework where capital remains accessible when needed while mitigating the inherent volatility of the digital asset market. The "Risk vs. Liquidity Matrix" serves as a mental model for investors to categorize various tools, such as savings accounts, lending protocols, and dollar-cost averaging (DCA) strategies.

By placing different financial instruments on this matrix, investors can balance their desire for yield against their need for capital preservation and access. A savings account might offer high liquidity but lower comparative yields, whereas locking assets in a lending protocol might increase yield at the cost of liquidity. Understanding where each strategy falls on this spectrum is the first step toward building a resilient portfolio that generates consistent returns regardless of broader market conditions.

This framework moves beyond simple "buy and hold" tactics. It incorporates automated accumulation strategies and sophisticated financial products like tokenized stocks. The goal is to remove emotional decision-making from the equation. By analyzing the mechanics of these tools, investors can deploy capital efficiently. This ensures that every satoshi or wei in a portfolio is either generating a return or providing necessary strategic flexibility.

The Foundation of Accumulation: Dollar-Cost Averaging

Dollar-cost averaging (DCA) serves as the bedrock for many passive income portfolios, primarily functioning as a risk management tool. It involves investing a fixed amount of money at regular intervals, regardless of the asset's price at that specific moment. This strategy is designed to bypass the complexity and stress of timing the market. Instead of trying to predict peaks and troughs, the investor commits to a schedule.

The primary advantage of this approach is the reduction of volatility impact. When prices are high, the fixed investment amount purchases fewer units of the asset. Conversely, when prices drop, that same amount purchases more units. Over time, this lowers the average cost per unit compared to a lump-sum purchase executed at a market peak. This smoothing effect is crucial in the crypto market, where double-digit percentage swings can occur within a single trading day.

Discipline is the second pillar of DCA. It enforces a regular investment habit, similar to paying rent or a mortgage. By treating investment as a recurring non-negotiable expense, investors build wealth systematically. This removes the emotional hesitation that often strikes during market downturns, which is paradoxically the best time to accumulate.

Analyzing Market Scenarios

To understand the efficacy of DCA, one must look at historical performance during different market phases. Consider a "buying the top" scenario where an investor enters the market at a price peak. Data shows that a lump-sum purchase at a historical all-time high can result in significant unrealized losses for extended periods if the market corrects immediately after.

In contrast, a DCA strategy initiated at the same peak would continue to acquire assets as the price falls. This lowers the break-even point significantly. If the market eventually recovers, the DCA investor often sees profit much earlier than the lump-sum investor, who must wait for the price to reclaim the absolute peak.

The strategy also offers protection during "catching the bottom" attempts. Predicting the absolute floor of a bear market is statistically improbable for most traders. A lump-sum buyer might enter too early, suffering further drops, or too late, missing the initial recovery. DCA captures the average price throughout the bottoming formation, ensuring exposure without requiring perfect timing.

The Cost of Flexibility

While DCA reduces risk, it does come with trade-offs. The most notable is the concept of "cash drag." In a market that is trending strictly upward with no significant corrections, DCA will statistically underperform a lump-sum investment. This is because the lump-sum investor deploys all capital at the lowest starting price, while the DCA investor buys at progressively higher prices.

However, crypto markets rarely move in a straight line. The volatility that characterizes digital assets makes the cash drag of DCA a reasonable insurance premium against downside risk. Another factor is transaction costs. Frequent small purchases can incur more trading fees than a single large transaction. Investors must select platforms with low fee structures to ensure these costs do not erode the benefits of the strategy.

Automated Investment Protocols

Modern exchanges have evolved to support this strategy through Auto DCA features. These tools allow users to automate the entire process, linking a funding source to a recurring buy order. The investor defines the interval—daily, weekly, or monthly—and the specific asset. The system then executes trades without manual intervention.

Automation serves two purposes. First, it eliminates the manual effort of placing orders, ensuring the schedule is never missed due to forgetfulness or inconvenience. Second, and more importantly, it removes the psychological barrier of buying during a crash. When headlines are negative and prices are red, human nature urges investors to flee. An automated system has no such bias and continues to accumulate cheap assets according to the plan.

The Savings Tier: Maximizing Idle Assets

Once assets are accumulated, the next phase in the passive income framework is generating yield on those holdings. Crypto savings accounts represent the high-liquidity, lower-risk quadrant of the matrix. These accounts function similarly to traditional bank savings accounts but typically offer significantly higher interest rates. Users deposit their digital assets, and the platform pays interest over time.

The mechanism behind these yields often involves the platform lending the pooled assets to institutional borrowers or other users. In exchange for providing liquidity to the platform, the depositor receives a share of the revenue generated. This transforms idle assets, which would otherwise sit stagnant in a wallet, into productive capital that compounds over time.

Flexible vs. Fixed Savings

Platforms generally offer two distinct types of savings products: flexible and fixed-term. Flexible savings accounts prioritize liquidity. They allow investors to deposit and withdraw funds at any time without penalty. This is ideal for capital that might be needed on short notice or for funds waiting to be deployed into other opportunities. The trade-off is that interest rates for flexible accounts are usually lower.

Fixed-term accounts require the investor to lock their assets for a predetermined period, such as 30, 60, or 90 days. In return for sacrificing liquidity, the platform offers a higher Annual Percentage Yield (APY). This option suits long-term holders who have no intention of selling in the near future. By committing to a lock-up, they maximize the passive income generated from their stack.

Calculating Returns

Understanding how returns are calculated is vital for comparison. Most platforms use APY, which accounts for the effect of compound interest. Compounding occurs when the interest earned is reinvested to earn its own interest. Over long periods, high APY rates can significantly accelerate portfolio growth compared to simple interest calculations (APR).

Investors should also note the payout currency. Interest is typically paid in the same asset that is deposited. If you deposit Bitcoin, you earn Bitcoin. This means the dollar value of the earnings will fluctuate with the market price of the asset. Some platforms may offer the option to earn interest in a platform-specific token, which might offer higher rates but comes with the added risk of that token's volatility.

Crypto Lending and Liquidity Management

Moving further along the risk/yield spectrum, we encounter crypto lending platforms. These services allow users to act as lenders, providing their assets to borrowers in exchange for interest payments. This sector has grown to include both centralized and decentralized options, each with unique risk profiles.

In a lending scenario, the investor supplies liquidity to a pool. Borrowers, who are often traders looking for leverage or institutions seeking working capital, access this pool. To secure the loan, borrowers must provide collateral. This over-collateralization protects the lender; if the borrower defaults or the value of their collateral drops too low, the system liquidates the collateral to repay the lender.

The Loan-to-Value (LTV) Ratio

The Loan-to-Value (LTV) ratio is a critical metric in this ecosystem. It represents the percentage of the collateral's value that is borrowed. For example, if a borrower deposits $10,000 worth of Bitcoin and takes out a $5,000 loan, the LTV is 50%.

From the perspective of the passive income investor (the lender), a lower LTV offered to borrowers generally implies a safer lending environment. It means there is a larger buffer of collateral to absorb market price drops before a liquidation event is triggered. Platforms that allow very high LTV ratios carry more risk, as a flash crash could potentially devalue the collateral faster than it can be liquidated, leading to bad debt.

Borrowing as a Strategy

While this article focuses on income, the borrowing side of these platforms plays a role in the liquidity matrix. Investors holding appreciating assets may not want to sell them to access cash, as selling triggers capital gains tax and results in the loss of future upside. By taking a crypto-backed loan, they can access liquidity for real-world expenses while retaining ownership of their digital assets.

This strategy introduces liquidation risk. If the price of the collateral asset drops significantly, the borrower may face a margin call. They must then deposit more collateral or repay part of the loan to lower the LTV. If they fail to do so, the platform sells their assets. Therefore, using lending platforms for liquidity requires careful monitoring of market conditions and conservative LTV management.

Tokenized Stocks: The Hybrid Frontier

Tokenized stocks represent a convergence of traditional equity markets and blockchain technology. These are digital tokens that track the price performance of publicly traded companies. For the passive income investor, they offer a way to diversify exposure beyond the crypto market while remaining within the digital asset ecosystem.

These tokens allow for fractional ownership. In traditional markets, a single share of a high-performing company might cost hundreds or thousands of dollars, creating a barrier to entry. Tokenized stocks allow investors to purchase a fraction of a share, potentially with as little as a few dollars. This enables precise portfolio allocation and diversification, even with smaller capital amounts.

24/7 Liquidity Access

One of the defining features of crypto markets is that they never sleep. Traditional stock markets operate with limited trading hours, weekends off, and holiday closures. Tokenized stocks, trading on crypto exchanges, are available 24/7. This provides superior liquidity options for investors who may need to react to global news events that occur outside of standard New York trading hours.

This continuous liquidity alters the risk profile of the asset. Investors are not trapped in positions over the weekend waiting for the Monday bell. They can enter or exit positions at any time. However, it is important to verify how the underlying asset is custodied. Reliable tokenized stock platforms hold the actual shares in a regulated brokerage account to back the value of the digital tokens 1:1.

Comparison of Asset Attributes

| Feature | Traditional Stocks | Tokenized Stocks |

|---|---|---|

| Trading Hours | Fixed (e.g., 9:30-4:00) | 24/7 |

| Settlement | T+2 Days | Near Instant |

| Ownership | Whole Shares | Fractional Shares |

Evaluating Platform Risk

Every passive income strategy relies on a platform, whether it is an exchange, a lending protocol, or a savings wallet. The risk associated with the platform itself—counterparty risk—is a major variable in the matrix. If the platform fails, acts maliciously, or suffers a security breach, the yield generated becomes irrelevant as the principal capital is lost.

Security features are the primary filter for platform selection. Investors must look for exchanges that utilize cold storage for the majority of user funds. Cold storage involves keeping private keys offline, disconnected from the internet, making them immune to remote hacking attempts. Furthermore, two-factor authentication (2FA) should be mandatory for all withdrawals and sensitive account changes.

Regulatory and Operational Health

The regulatory status of a platform provides insight into its long-term stability. Platforms that comply with local laws and have clear operational guidelines are less likely to face sudden shutdowns or asset freezes by authorities. Transparency regarding reserves is also crucial. Proof of Reserves (PoR) audits allow users to verify that the exchange actually holds the assets it claims to owe its customers.

Insurance is another differentiator. Some platforms maintain insurance funds to cover potential losses from hacks or technical failures. While this does not usually cover user error (like losing a password), it adds a layer of protection against systemic platform failures. Investors should read the terms of service to understand exactly what is covered and what is excluded.

Impact of Fees on Net Yield

Passive income is a game of margins. High fees can quickly erode the returns from staking, lending, or savings accounts. When engaging in DCA, trading fees are incurred with every purchase. Even a small percentage fee adds up over dozens or hundreds of transactions. Investors should seek platforms with tiered fee structures or low costs for recurring buys.

In the lending and savings sector, withdrawal fees can be a hidden trap. A platform might offer a high APY, but if it charges a significant flat fee to withdraw funds, it may negate months of interest earnings, especially for smaller balances. It is essential to calculate the "round trip" cost of the investment: the fee to deposit, the fee to buy/swap, and the fee to withdraw.

Fee Structures to Monitor

| Fee Type | Impact | Mitigation Strategy |

|---|---|---|

| Trading/Swap | Reduces acquisition amount | Use limit orders; hold exchange tokens |

| Withdrawal | Reduces final liquidity | Batch withdrawals; check network fees |

| Management | Lowers APY directly | Compare net APY across platforms |

Liquidity Considerations and Lock-ups

Liquidity refers to the ease with which an asset can be converted into cash without affecting its market price. In the context of passive income strategies, liquidity also refers to the accessibility of funds. A strategy with high returns often demands low liquidity (lock-ups), while high liquidity strategies typically offer lower returns.

Investors must assess their personal liquidity needs before committing to a strategy. Money needed for near-term expenses or an emergency fund should not be placed in fixed-term savings accounts or volatile lending protocols. Flexible savings accounts or holding stablecoins offer the best profile for this capital, ensuring it is available instantly if required.

Conversely, funds allocated for long-term wealth generation (5+ years) can tolerate lower liquidity. For these funds, locking assets to secure a higher yield is a rational strategic decision. The risk of not being able to sell during a market spike is outweighed by the guaranteed higher interest accumulation over the long horizon.

Tax Implications of Passive Crypto Income

The generation of passive income in cryptocurrency triggers tax events in many jurisdictions. Unlike simply holding an asset where tax is deferred until sale, earning interest is often treated as income at the time of receipt. This means every interest payment—whether daily, weekly, or monthly—may be a taxable event based on the fair market value of the asset at that moment.

Keeping detailed records is non-negotiable. Investors need to track the date, amount, and value of every interest payment. Many platforms provide exportable transaction histories to assist with this. However, the complexity increases with high-frequency payouts. Using crypto tax software can automate the aggregation of this data.

Additionally, disposing of the earned assets later (selling the interest earned) triggers capital gains or losses. This creates a dual-taxation structure: income tax on the initial receipt and capital gains tax on any subsequent appreciation. Investors must budget for these liabilities to avoid being forced to liquidate long-term holdings to pay tax bills.

Diversification: The Risk Killer

No single asset or platform should hold 100% of an investor's portfolio. Diversification is the most effective method for mitigating idiosyncratic risk. This applies to both the assets held and the platforms used. Spreading capital across Bitcoin, Ethereum, stablecoins, and tokenized stocks reduces the impact if one specific asset collapses.

Platform diversification is equally important. If an investor uses savings accounts, spreading funds across two or three reputable exchanges ensures that a technical failure or freeze on one platform does not paralyze the entire portfolio. While this increases management overhead, it is a critical safety valve for preserving wealth.

Stablecoins vs. Volatile Assets

A balanced passive income portfolio often includes a mix of stablecoins and volatile assets. Stablecoins (like USDC or USDT) are pegged to fiat currency. Yields on stablecoins are often higher than traditional bank rates and do not suffer from price volatility. This provides a steady, predictable income stream that can be used to pay living expenses or reinvest.

Volatile assets (BTC, ETH) offer lower predictable yields but come with the potential for capital appreciation. The passive income from these assets acts as a bonus on top of the price growth. A strategic mix allows the investor to enjoy the safety of stablecoins while maintaining exposure to the upside potential of the broader crypto market.

Conclusion

The Risk vs. Liquidity Matrix provides a structured approach to navigating the complex world of crypto passive income. By plotting strategies based on these two axes, investors can build a portfolio that aligns with their financial goals and risk tolerance. Dollar-cost averaging offers a high-liquidity, risk-managed entry point. Savings accounts provide a flexible, lower-yield safety net. Lending and fixed-term options offer higher returns in exchange for reduced liquidity.

Successful implementation requires more than just selecting the highest APY. It demands rigorous platform vetting, an understanding of collateral mechanics, and disciplined fee management. Investors must remain vigilant regarding regulatory changes and tax obligations, ensuring that their passive income streams do not become administrative burdens.

Ultimately, the goal is to construct a system where technology and financial protocols work for the investor. By automating accumulation and strategically deploying capital into yield-bearing instruments, one can weather market volatility. This approach transforms a portfolio from a stagnant collection of coins into a dynamic engine for wealth preservation and growth.

The most effective strategy is the one you can stick to consistently, regardless of market noise.