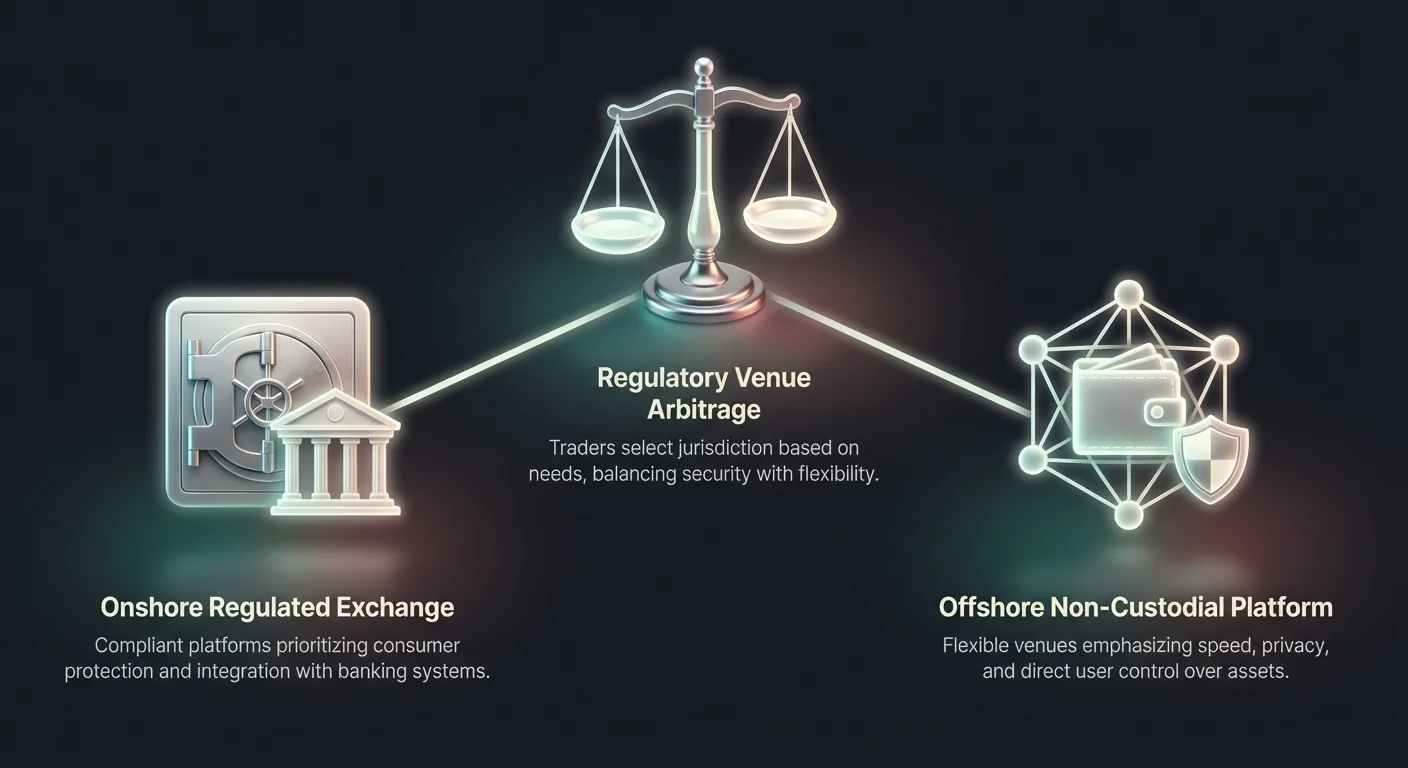

The concept of regulatory venue arbitrage has become a defining feature of the global cryptocurrency market. This phenomenon involves traders and entities selecting specific jurisdictions or platform types based on the regulatory environment that best suits their operational needs. In the digital asset space, this choice often splits between onshore, highly regulated exchanges and offshore or decentralized alternatives.

Understanding the distinctions between these two environments is critical for market participants. The regulatory framework governs every aspect of the trading experience, from account creation and identity verification to asset availability and tax reporting. Onshore platforms typically prioritize consumer protection and compliance with local laws, while offshore venues often emphasize speed, privacy, and broader market access.

This divergence creates a fragmented ecosystem where the user experience varies drastically depending on the platform's legal domicile. A trader in New York faces a completely different set of rules and available tools compared to a user accessing a global swap platform from a less regulated jurisdiction. Recognizing these differences allows participants to navigate the trade-offs between security, convenience, and functionality.

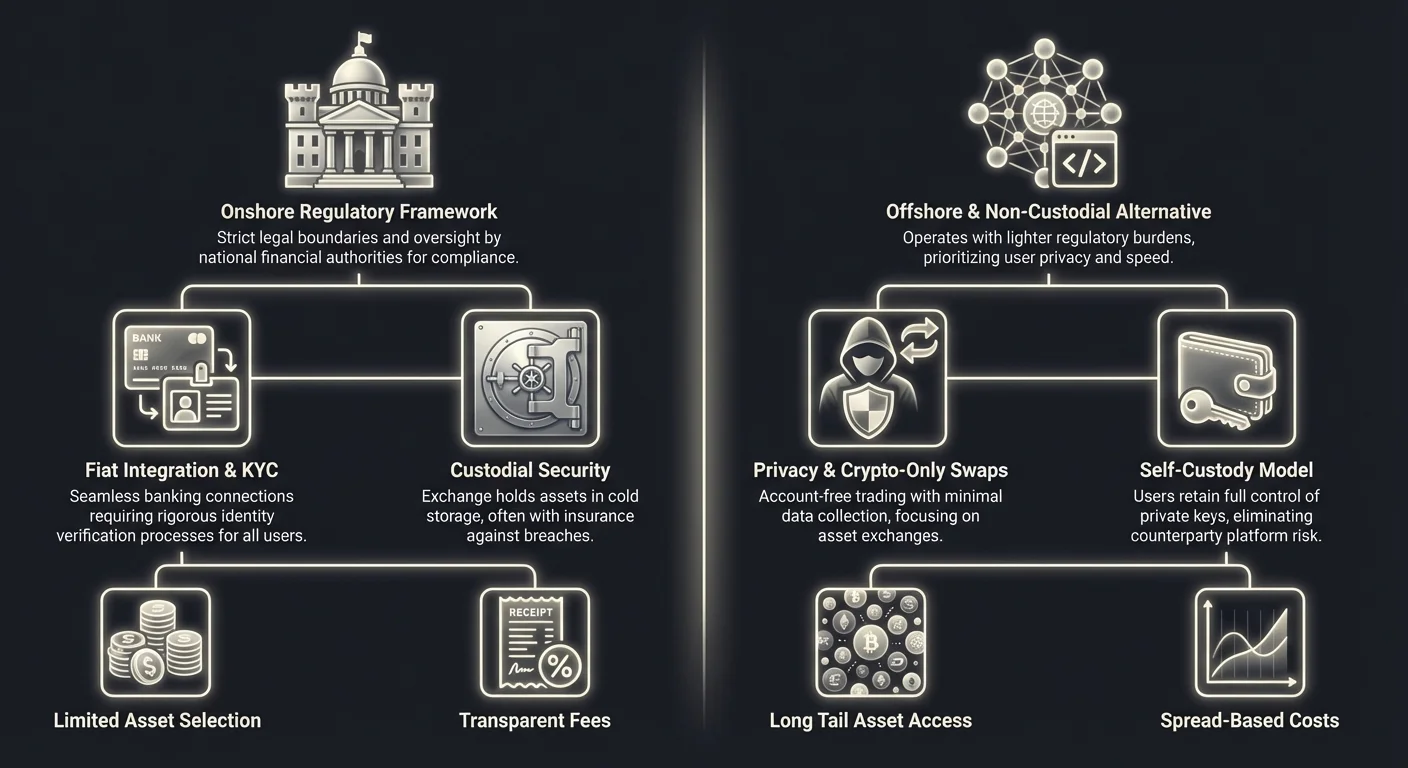

The Onshore Regulatory Framework

Onshore exchanges operate within strict legal boundaries set by national financial authorities. These platforms are designed to integrate seamlessly with the traditional banking system, offering fiat currency on-ramps and off-ramps. To maintain their licenses, they must adhere to rigorous standards regarding capital reserves, cybersecurity, and customer protection.

Strict Compliance and Oversight

The defining characteristic of onshore trading venues is their adherence to stringent regulatory requirements. In jurisdictions like the United States, Europe, and Australia, exchanges must register with financial intelligence units and banking regulators. For example, platforms operating in New York may be required to hold a specific license, such as the BitLicense, or operate as a limited purpose trust company.

These licenses mandate regular audits and transparent operational practices. Regulators often require exchanges to maintain a 1:1 reserve of customer assets, ensuring that funds are always available for withdrawal. This level of oversight provides a safety net for users, reducing the risk of insolvency or mismanagement that has plagued unregulated entities in the past.

Furthermore, onshore platforms are often subject to specific cybersecurity mandates. They frequently employ SOC 1 and SOC 2 certifications to demonstrate their commitment to data security and operational integrity. These certifications assure institutional clients and retail investors that the platform’s internal controls have been independently verified and meet industry standards.

Integration with Fiat Banking

One of the primary advantages of regulated onshore exchanges is their ability to process fiat currency transactions. Because these platforms comply with banking regulations, they can maintain direct relationships with traditional banks. This allows users to deposit and withdraw national currencies like the US Dollar, Euro, or Australian Dollar via wire transfers or automated clearing house systems.

This integration facilitates seamless settlement for large-scale transactions. For institutional investors and high-net-worth individuals, the ability to move millions of dollars in and out of the crypto market through compliant banking rails is essential. It eliminates the friction and legal uncertainty associated with using intermediaries or peer-to-peer networks to convert cash into digital assets.

However, this banking integration comes with limitations. Users are restricted to the payment methods and banking hours of the traditional financial system. Wire transfers may take days to settle, and banks may impose their own limits on transfers to crypto-related entities. Despite these delays, the legal clarity of these transactions is a significant draw for corporate treasuries and asset managers.

Limited Asset Selection

A notable trade-off for the security of onshore platforms is a restricted selection of tradable assets. Regulated exchanges must be extremely cautious about which cryptocurrencies they list. In many jurisdictions, listing a token that is later classified as an unregistered security can lead to severe legal penalties and enforcement actions.

Consequently, onshore exchanges typically support a curated list of established cryptocurrencies. Assets like Bitcoin and Ethereum are standard, along with a selection of major altcoins that have deemed to be sufficiently decentralized. Newer, more speculative tokens, or those with complex governance structures, are often excluded from these platforms until their regulatory status becomes clear.

This conservative approach limits the investment opportunities available to users of onshore exchanges. Traders looking for early access to small-cap tokens or experimental decentralized finance protocols often find the selection on regulated platforms insufficient. This limitation is a primary driver for users seeking alternative venues that operate outside these strict listing constraints.

The Offshore and Non-Custodial Alternative

In contrast to the walled gardens of regulated exchanges, the offshore and non-custodial sector offers a different value proposition. These platforms often operate in jurisdictions with lighter regulatory burdens or structure themselves as software providers rather than financial custodians. This flexibility allows them to offer features that are difficult or impossible to implement under strict onshore regimes.

Privacy and Minimal Data Collection

A major appeal of offshore and swap-based platforms is the preservation of user privacy. Many of these venues operate on a non-custodial basis, meaning they do not take possession of user funds. Instead, they facilitate the exchange of assets directly between user wallets or through liquidity pools. Because they do not hold funds, they often have reduced requirements for collecting personal data.

This "account-free" model contrasts sharply with the extensive data collection required by onshore entities. Users can often execute trades simply by connecting a digital wallet, without the need to upload government identification or proof of address. This aligns with the ethos of the broader cryptocurrency movement, which prioritizes financial autonomy and data minimization.

For traders concerned about data breaches or identity theft, the ability to trade without sharing sensitive personal information is a significant advantage. It also enables access for the unbanked or those living in regions with restrictive financial controls, providing a global gateway to the digital asset economy that is independent of local banking infrastructure.

Speed and Efficiency of Swaps

The operational model of offshore and non-custodial platforms prioritizes speed. Without the need for manual account approvals or bank transfer settlement times, trading can occur almost instantly. Automated swap platforms utilize smart contracts and liquidity aggregation to execute trades in seconds or minutes, depending on the blockchain network speed.

These platforms often feature "instant exchange" capabilities. A user sends one cryptocurrency to a provided address and receives the desired asset in return at a pre-agreed rate. This mechanism removes the complexity of order books, bid-ask spreads, and matching engines found on traditional centralized exchanges. It simplifies the user experience, making it accessible to novices who may be intimidated by professional trading interfaces.

Furthermore, the absence of fiat processing removes a major bottleneck. Since these platforms focus exclusively on crypto-to-crypto trades, they are not subject to banking hours or holiday closures. The market operates 24/7, and settlement is finalized as soon as the transaction is confirmed on the blockchain, offering a level of liquidity and access that traditional financial systems cannot match.

Access to the Long Tail of Assets

Without strict listing requirements, offshore and swap platforms can support a vast array of digital assets. It is not uncommon for these venues to list hundreds or even thousands of different tokens. This includes stablecoins, privacy coins, governance tokens, and emerging assets from various blockchain ecosystems like Solana, Polygon, and Avalanche.

This extensive selection allows traders to build highly diversified portfolios and access niche markets. Users can trade assets across different blockchains, often bridging the gap between incompatible networks. For example, a user might swap a Bitcoin-based asset directly for a token on the Ethereum network, a process that would be cumbersome on a strictly regulated exchange with limited pairs.

The ability to access the "long tail" of the crypto market attracts speculative traders and early adopters. These participants are willing to accept higher risks for the potential of higher returns found in unproven assets. This environment fosters innovation but also exposes users to lower-quality projects and higher volatility compared to the curated lists of onshore exchanges.

The Friction of Identity Verification (KYC)

The divide between onshore and offshore venues is most visible in their approach to Know Your Customer (KYC) protocols. KYC is the process by which a financial institution verifies the identity of its clients to prevent money laundering, fraud, and terrorism financing. In the crypto space, KYC is the gatekeeper that determines who can access specific platforms and services.

Tiered Verification Systems

Regulated onshore exchanges typically employ a tiered approach to identity verification. At the entry level, users might be able to trade small amounts after providing basic information. However, to access higher withdrawal limits or fiat currency deposits, users must undergo rigorous verification. This often involves uploading high-resolution photos of government ID documents, taking facial recognition selfies, and providing utility bills.

This process can be intrusive and time-consuming. Verification can take anywhere from a few minutes to several days, depending on the platform's efficiency and the clarity of the documents provided. For institutional clients, the process is even more exhaustive, requiring corporate formation documents, beneficiary ownership information, and compliance interviews.

While these measures create friction, they also build a layer of trust. Users know that the other participants on the platform have been vetted, reducing the likelihood of interacting with illicit actors. This sanitized environment is a prerequisite for many large investors and corporations who cannot legally transact on platforms that do not enforce strict anti-money laundering controls.

The "No-KYC" User Experience

Conversely, non-custodial swap platforms and offshore venues often market themselves on the absence of these barriers. By structuring their services as software tools rather than financial intermediaries, they argue that they are not subject to the same banking regulations. This allows for a frictionless onboarding experience where a user can start trading immediately upon visiting the site.

This model appeals to users who value speed and convenience over regulatory assurance. It is particularly useful for automated trading bots and algorithmic strategies that require instant execution without the risk of account freezes due to compliance flags. The lack of KYC also protects users from the risk of their personal data being hacked from a centralized server, a common occurrence in the digital age.

However, the "No-KYC" landscape is facing increasing pressure. Global regulators are working to close these loopholes, and many platforms are beginning to implement "geo-blocking" to prevent users from strict jurisdictions like the US from accessing their services. This creates a cat-and-mouse game where platforms and users constantly adapt to shifting regulatory boundaries.

Security Paradigms and Asset Custody

Security architectures differ fundamentally between onshore and offshore venues. The primary distinction lies in who holds the private keys to the digital assets. Onshore exchanges typically act as custodians, holding assets on behalf of the user, while offshore swap platforms often utilize a non-custodial model where the user retains full control.

Custodial Protections and Insurance

Onshore exchanges invest heavily in custodial security infrastructure. The vast majority of user funds are held in "cold storage," meaning the private keys are kept on offline devices that are air-gapped from the internet. This protects assets from remote hacking attempts. Only a small percentage of funds are kept in "hot wallets" to facilitate immediate withdrawals.

To further protect users, many regulated exchanges carry crime or theft insurance. While this insurance rarely covers individual account compromises due to weak passwords, it does protect against major platform breaches. Additionally, in some jurisdictions, fiat deposits held at the exchange may be eligible for pass-through deposit insurance, similar to a bank account.

These custodial protections offer peace of mind for users who do not wish to manage their own security. The exchange takes responsibility for the technical complexity of key management. If a user loses their password, there is a recovery process. This support system is critical for mass adoption among non-technical users.

Non-Custodial Autonomy

Offshore swap platforms and decentralized exchanges push security responsibility to the user. In a non-custodial trade, the assets move directly from the user's personal wallet to a smart contract or liquidity provider and back. The platform never legally owns the funds. This eliminates the risk of the exchange collapsing and taking user funds with it, a scenario known as counterparty risk.

This model adheres to the crypto maxim "not your keys, not your coins." It ensures that the user is immune to platform insolvency, bank runs, or regulatory seizures of exchange assets. However, it also means there is no customer support line to call if a user loses their private keys or sends funds to the wrong address.

The security of non-custodial trading relies entirely on the user's ability to secure their own wallet and the integrity of the smart contract code. While this removes the single point of failure of a centralized exchange, it introduces the risk of software bugs or "exploits" in the trading protocol. Users must trust the code rather than a company.

| Feature | Onshore / Regulated | Offshore / Non-Custodial |

|---|---|---|

| Asset Custody | Third-party custodian (Exchange) | Self-custody (User Wallet) |

| Identity Checks | Mandatory KYC/AML | Minimal or None |

| Security Model | Cold Storage & Insurance | Code Audits & User Responsibility |

Economic Incentives and Fee Structures

The regulatory venue also impacts the cost of trading. Compliance is expensive. Onshore exchanges must maintain large legal teams, pay licensing fees, and invest in sophisticated surveillance software to monitor for market manipulation. These costs are inevitably passed down to the user in the form of trading fees.

The Cost of Compliance

Regulated exchanges typically charge transparent fees per transaction, often based on a maker-taker model. Volume-based discounts are common, incentivizing high-frequency trading. While these fees can be competitive, they are rarely zero. The platform must generate sufficient revenue to cover its significant regulatory overhead and insurance premiums.

Additionally, moving fiat currency into and out of these platforms often incurs banking fees. Wire transfers, ACH processing, and credit card payments all involve third-party processors that charge for their services. These external costs add to the overall expense of using a compliant, fiat-connected venue.

However, the transparency of these fees is a benefit. Regulated entities are often required to clearly disclose their fee schedules and are prohibited from engaging in deceptive pricing practices. Users can calculate their exact costs before executing a trade, ensuring there are no surprises upon settlement.

Zero-Fee Models and Spreads

Offshore and swap platforms often utilize different economic models. Some market themselves as "zero-fee" exchanges, claiming to charge no commission on trades. While this is marketing gold, the reality is often more nuanced. These platforms typically monetize through the "spread"—the difference between the buying and selling price.

In a swap transaction, the rate offered to the user may be slightly worse than the raw market rate. This difference represents the platform's margin. While the user pays no explicit transaction fee, they pay an implicit cost in the form of price execution. This model simplifies the user experience but can sometimes result in higher effective costs for large trades compared to a transparent commission model.

Other offshore platforms incentivize market makers to provide liquidity by offering rebates rather than charging fees. This creates deep liquidity pools for specific assets. Without the burden of heavy compliance costs, these platforms can operate with thinner margins, potentially offering better net prices for specific crypto-to-crypto pairs, provided the user understands how to navigate the spread.

Institutional vs. Retail Market Segmentation

The choice between onshore and offshore venues effectively segments the market into two distinct groups: institutional capital and retail traders. This segmentation drives the development of different features and services tailored to the specific needs of each group.

The Institutional Mandate

Institutional investors, such as hedge funds, family offices, and corporate treasuries, have a fiduciary duty to protect client assets. This mandate effectively restricts them to onshore, regulated venues. They require qualified custodians, audited financial statements, and clear legal recourse in the event of a dispute.

Consequently, onshore exchanges have evolved to build "Prime Brokerage" services. These suites include features like smart order routing, which splits large orders across multiple liquidity venues to minimize price impact. They also offer advanced reporting tools compatible with traditional accounting software, facilitating tax compliance and portfolio management.

For these players, the priority is not the lowest possible fee or the widest selection of obscure tokens. The priority is legitimacy and stability. They are willing to pay a premium for a trading environment that guarantees their trades are legally recognized and their assets are ring-fenced from the platform’s operational funds.

The Retail Frontier

Retail traders, particularly those who are tech-savvy or live in regions with unstable currencies, often flock to offshore and swap platforms. These users prioritize utility and accessibility. They are often the first to explore new market sectors, such as yield farming or algorithmic stablecoins, which are rarely supported on regulated venues.

This demographic drives the innovation of user interfaces and trading mechanisms. Features like "copy trading," where users can automatically mimic the strategies of successful traders, and high-leverage futures trading originated in the offshore market. These tools offer retail users sophisticated ways to speculate that are often blocked by consumer protection laws in strict jurisdictions.

While retail traders are increasingly moving toward regulated options as the industry matures, a significant portion remains committed to the decentralized ethos. They view the friction of onshore regulations as a barrier to financial freedom and prefer the autonomy provided by non-custodial, permissionless platforms.

Conclusion

The divide between onshore and offshore crypto exchange licensing represents a fundamental choice between security and flexibility. Onshore venues offer a fortified environment integrated with the traditional financial system, providing legal recourse, insurance, and institutional-grade custody. This comes at the cost of privacy, asset selection, and onboarding speed. Conversely, offshore and swap platforms provide immediate access to the broader digital asset economy, prioritizing user autonomy and efficiency, but shifting the burden of security entirely to the individual.

As the industry evolves, the gap between these two worlds is beginning to narrow. Regulated entities are expanding their asset lists and improving user interfaces, while offshore platforms are increasingly adopting voluntary compliance measures to secure banking partnerships. However, distinct advantages remain in each sector. Investors must weigh their need for regulatory protection against their desire for operational agility. Ultimately, the "best" venue is not universal; it depends entirely on the user's risk tolerance, location, and specific trading objectives.

Traders must actively choose between the legal safety of onshore platforms and the operational freedom of offshore venues.