The world of Decentralized Finance (DeFi) has revolutionized how individuals manage and grow their capital. Moving beyond simply holding cryptocurrencies, DeFi offers accessible mechanisms for generating passive income—money earned without active trading or management. This shift is profound, allowing anyone with internet access to essentially become their own bank.

However, the sheer variety of income methods—staking, yield farming, and lending—can be overwhelming for beginners. While these terms often get lumped together, they represent vastly different risk profiles, liquidity constraints, and expected returns. Choosing the wrong strategy based on high reported Annual Percentage Yields (APYs) alone can lead to significant loss.

This guide moves past defining these terms and focuses on the crucial next step: strategic decision-making. We provide a side-by-side framework comparing the core mechanics of staking, yield farming, and lending, helping you choose the strategy that aligns best with your capital requirements, risk tolerance, and investment timeline.

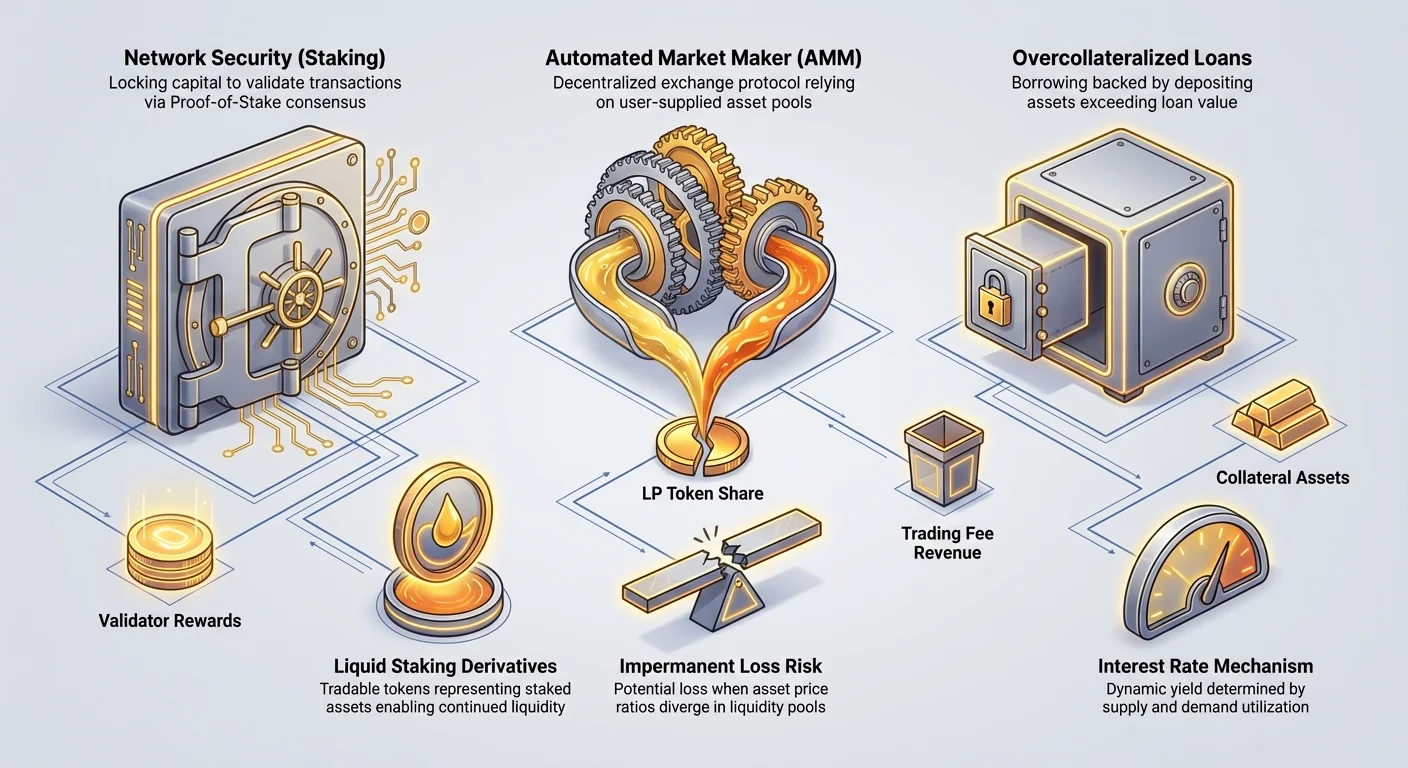

Foundational Pillar 1: Staking (The Security Model)

Staking is often considered the most accessible and foundational method of generating passive income in DeFi. It is fundamentally tied to the security and operation of a blockchain network.

How Staking Works: Proof-of-Stake Simplified

Staking exists on blockchains that utilize a consensus mechanism called Proof-of-Stake (PoS). Unlike Bitcoin's Proof-of-Work (PoW), which relies on energy-intensive computing power to validate transactions, PoS relies on economic commitment.

When you stake your tokens, you are locking them up as collateral to help secure the network. Validators (nodes running the software) use this staked collateral to confirm new transaction blocks honestly. In return for securing the network and validating transactions, the protocol rewards stakers with newly minted tokens or transaction fees.

Think of staking as depositing money into a special high-interest savings account (the blockchain) where your funds are used to guarantee the integrity of the bank’s operations.

Types of Staking: Direct, Pooled, and Liquid

The entry barrier and liquidity profile of staking depend heavily on how you stake:

1. Direct Staking (Running a Node)

This involves running your own validator node. It requires a significant capital minimum (e.g., 32 ETH for Ethereum) and advanced technical knowledge. The risks involve "slashing"—penalties applied if your node goes offline or attempts malicious actions.

2. Pooled Staking (Delegation)

This is the most common path for beginners. You delegate (assign) your tokens to a professional validator who manages the node on your behalf. You earn rewards minus a small commission fee (typically 10-20%) paid to the validator. Your funds are not technically held by the validator, only entrusted to their node for security purposes.

3. Liquid Staking (LSTs)

Standard staking often requires your funds to be locked up for a period, making them illiquid. Liquid Staking Tokens (LSTs) solve this. When you stake your crypto through a liquid staking protocol (like Lido or Rocket Pool), the protocol stakes the funds on the blockchain, but in return, it immediately issues you a derivative token (e.g., stETH, rETH).

The Strategic Advantage of LSTs: This derivative token represents your staked asset plus earned rewards. Crucially, the LST is liquid and tradable. This means you can immediately use the LST in other DeFi protocols (like lending or farming) while still earning staking rewards from the underlying asset—effectively doubling your capital utility.

Key Strategic Metrics: Liquidity and Lock-up

The primary strategic drawback of traditional direct or pooled staking is the lock-up period and liquidity constraint.

- Lock-up: Depending on the blockchain, withdrawal periods can range from a few days to several weeks after you decide to unstake.

- Yield Source: Rewards come directly from the network, providing highly predictable and generally stable APYs (usually 3% to 8%, depending on the chain and participation rate).

- Risk Profile: Low to moderate. The primary risks are smart contract failure in the pooling mechanism or potential slashing penalties (if you run your own node or choose a poor validator).

Foundational Pillar 2: Yield Farming (The Liquidity Model)

Yield farming is a high-octane strategy focused on maximizing returns by actively moving assets between various protocols, leveraging liquidity pools, and often harvesting multiple forms of yield simultaneously.

How Yield Farming Works: Supplying Assets to Liquidity Pools

Yield farming centers around providing liquidity to decentralized exchanges (DEXs) like Uniswap or PancakeSwap. DEXs rely on Automated Market Makers (AMMs) and Liquidity Pools (LPs) to facilitate trading without centralized intermediaries.

When you "farm," you become a Liquidity Provider (LP). You deposit a pair of tokens (e.g., ETH and USDC) into a pool. In exchange, you receive LP tokens representing your share of the pool.

The core sources of income in yield farming are:

- Trading Fees: Every time a user trades using the pool you provided liquidity to, you earn a proportional share of the transaction fee (typically 0.25% to 0.30% of the trade).

- Farming Rewards: Many protocols incentivize LPs by distributing their native governance token (often called a 'farm token') as an additional reward layer, boosting the total APY significantly.

The Primary Risk: Understanding Impermanent Loss

While yield farming often promises very high APYs (sometimes exceeding 50% or 100% in new pools), these figures are necessary to offset the inherent structural risk: Impermanent Loss (IL).

Impermanent Loss occurs when the price ratio of the two assets in your liquidity pool changes after you deposit them. The AMM mechanism automatically rebalances the pool to maintain a 50/50 value split. In essence, the protocol forces you to sell the asset that goes up in price and buy the asset that goes down.

If you withdraw your assets, you will own fewer units of the higher-performing asset and more units of the lower-performing asset than if you had simply held the two assets in your personal wallet.

Example: You deposit 1 ETH and 1,000 USDC. Later, ETH doubles to 2,000 USDC. When you withdraw, the pool has rebalanced, and you might only receive 0.75 ETH and 1,500 USDC. The total dollar value of the assets you withdrew will be less than the dollar value of the same 1 ETH and 1,000 USDC held outside the pool. This loss is "impermanent" only if the token prices return to their initial ratio; otherwise, the loss is realized upon withdrawal.

Strategic Considerations for Yield Farming

- Liquidity: High. LP tokens can often be redeemed immediately (unpooled), though network congestion and high gas fees might delay the process.

- Yield Source: Highly variable. Rewards rely on trading volume (fees) and the price stability of the governance token rewards. High APYs can drop instantly if rewards are reduced or if the farm token crashes in value.

- Risk Profile: High. IL is the primary danger, compounded by volatility risk and smart contract risk.

Actionable Tip: To mitigate IL, many strategic farmers focus on stablecoin pairs (e.g., USDC/DAI), where the price ratio is almost guaranteed to remain 1:1, offering much lower but highly stable yields.

Foundational Pillar 3: DeFi Lending (The Credit Model)

DeFi lending is the closest analogue to traditional banking, where users can borrow and lend digital assets through automated, decentralized money markets.

How Lending Works: Supplying Funds to Money Markets

In DeFi lending protocols (such as Aave or Compound), you act as the supplier (lender). You deposit assets (e.g., ETH, USDC) into a collective pool. Borrowers then take loans from this pool, but they must provide excess collateral (usually 120% to 150% of the loan value) to secure the debt.

If the value of the borrower's collateral drops too low (risking under-collateralization), the protocol automatically liquidates the collateral to protect the lenders' principal.

Your passive income comes from the interest paid by the borrowers.

Risk Profile: Counterparty Risk and Smart Contract Failure

DeFi lending eliminates traditional bank counterparty risk (the risk the bank fails), but it introduces two new, distinct risks:

- Smart Contract Risk: If there is a bug or vulnerability in the lending protocol's code, all funds in the pool could potentially be drained or frozen. This risk is managed by using well-audited and time-tested protocols.

- Liquidation and Oracle Risk: While liquidation mechanisms are robust, if extreme market volatility causes collateral prices to crash faster than the system can liquidate, the pool could become under-collateralized. Additionally, the system relies on external price feeds (oracles); if an oracle is manipulated, the system can be exploited.

Strategic Advantage: Flexibility and Stable APYs

Lending is prized for its simplicity and relatively low risk compared to yield farming:

- Predictable Income: Interest rates are determined by supply and demand within the protocol, offering APYs that are generally much steadier than farming rewards.

- Maximum Liquidity: Funds are rarely locked up. You can typically withdraw your deposited assets immediately, provided there is enough liquidity in the pool (which is nearly always the case for major assets like ETH and stablecoins).

- Strategy: Lending is ideal for capital that needs to remain highly liquid but should still generate yield. It’s the closest DeFi equivalent to a traditional bond or high-yield savings account.

Comparative Framework: Choosing Your Strategy

Choosing the right strategy requires analyzing the trade-offs across four key dimensions: Risk, Return, Liquidity, and Complexity.

| Feature | Staking (PoS/LSTs) | DeFi Lending (Money Markets) | Yield Farming (LP Pools) |

|---|---|---|---|

| Primary Goal | Secure the Network | Provide Credit (Interest) | Provide Liquidity (Trading Fees) |

| Typical APY | Low (3% – 8%) | Moderate (4% – 12%) | High (15% – 100%+) |

| Primary Risk | Slashing, Smart Contract, Lock-up | Smart Contract, Liquidation Risk | Impermanent Loss (IL) |

| Liquidity Profile | Low (Traditional Staking) / High (LSTs) | Very High (Instant withdrawal) | Moderate (Requires unpooling) |

| Capital Lock-up | Weeks/Months (Traditional) / None (LSTs) | None | None (But withdrawal realizes IL) |

| Entry Barrier | Low (Delegation/LSTs) | Very Low (Simple deposit) | Moderate (Requires understanding IL) |

Risk-Adjusted Returns: Low Risk vs. High APY

The core strategic choice is where you position yourself on the risk-reward spectrum:

1. Low Risk, Low APY (The Foundation): Staking and Stablecoin Lending

If capital preservation is your priority, these are the safest choices. Staking rewards are tied to network inflation, making them reliable. Lending stablecoins (like USDC or USDT) provides predictable interest payments with almost zero volatility risk and zero Impermanent Loss risk. This is the optimal foundation for any beginner DeFi portfolio.

2. Moderate Risk, Moderate APY: Variable Asset Lending

Lending more volatile assets like ETH or major altcoins carries higher yields than stablecoins (due to higher demand for borrowing these assets), but the value of your principal fluctuates with the market.

3. High Risk, High APY (The Accelerator): Volatile Yield Farming

High APY figures in farming are often misleading because they are frequently denominated in the farm's native governance token, which can be highly inflationary or volatile. These strategies are suitable only for experienced investors who understand how to calculate and hedge against Impermanent Loss and are comfortable with extreme volatility in total returns.

Capital Requirements and Entry Barriers

The minimum technical knowledge and capital needed vary significantly:

| Strategy | Capital Minimum | Technical Barrier |

|---|---|---|

| Staking (Delegated) | Low (often $10 minimum) | Very Low (Use an exchange or pool UI) |

| DeFi Lending | Very Low (often $1 minimum) | Low (Simple deposit/withdrawal on major apps) |

| Yield Farming | Moderate (Need sufficient capital to offset high gas fees) | Moderate (Requires knowledge of IL, token pairing, and contract interaction) |

For beginners, starting with a simple staking mechanism (via an exchange or a dedicated LST protocol) or depositing stablecoins into a reputable lending pool is the easiest entry point. Yield farming requires a much deeper understanding of smart contract interaction, gas cost dynamics, and risk calculation.

Liquidity and Lock-up Comparison

Liquidity refers to how quickly you can convert your investment back into cash or use it elsewhere. This is the crucial strategic variable for anyone who might need access to their funds unexpectedly.

- Traditional Staking: High liquidity risk. The funds are locked and may take weeks to retrieve. This is capital best reserved for long-term conviction (5+ years).

- DeFi Lending: Minimal liquidity risk. Since lending protocols use dynamic interest rates, they don't lock funds, allowing instant withdrawal (assuming the pool isn't temporarily depleted—a rare occurrence on major platforms).

- Yield Farming: Moderate liquidity risk. While funds are not officially locked, you must interact with the protocol twice (approve, deposit) and twice again to withdraw (unpool, redeem). This means you are constantly exposed to network congestion and high transaction (gas) costs, which can render small positions unprofitable.

Advanced Strategy Concepts (Integrating the Pillars)

As you move beyond the basics, DeFi offers powerful ways to combine these strategies, allowing you to increase both capital efficiency and total yield.

Enhancing Staking Liquidity: Leveraging Liquid Staking Tokens (LSTs)

LSTs are the key bridging technology between the Staking model and the Lending/Farming models. By using an LST, you unlock your staked capital for use in other protocols, a process sometimes called "Lego stacking."

Strategic Use Case (Staking + Lending):

- Stake ETH via a Liquid Staking provider (e.g., receive stETH).

- Deposit the stETH into a DeFi lending market (Aave).

- Earn ETH staking yield (Source 1).

- Earn interest from lending stETH (Source 2).

This strategy efficiently generates two layers of yield on the same underlying asset, radically improving capital utilization. However, it significantly increases the overall risk profile because you are now exposed to smart contract risk from two or more separate protocols.

The Rise of Restaking: Doubling Down on Security and Yield

Restaking is a highly advanced concept that builds directly upon Liquid Staking. In restaking, you take your LST (the derivative token representing your staked ETH) and redeploy it to secure additional decentralized networks or services (called Actively Validated Services, or AVSs).

How it Works Strategically: You are promising to uphold the security and honesty requirements of the core Ethereum chain and several peripheral AVSs using the same capital. This allows those smaller services to bootstrap their security without needing to issue their own tokens and validators.

- Benefit: Restaking offers substantial, layered yields (Source 3, Source 4, etc.) from securing multiple services.

- Risk: The slashing risk is also layered. If you fail to perform honestly on an AVS, you risk losing your underlying staked ETH. This is a high-reward, high-consequence strategy suitable only for advanced users who fully grasp the underlying technical risks.

Portfolio Allocation: Combining Strategies for Diversification

A well-structured DeFi portfolio should utilize all three pillars to achieve diversification across risk vectors and yield sources. This moves the strategic focus from "where do I get the highest APY?" to "how do I protect my core capital while optimizing yield?"

A strategic allocation might look like this for a moderate-risk investor:

- Safety Bucket (50%): Stablecoin lending on major, audited protocols (USDC, DAI). This provides highly liquid, foundational yield.

- Growth Bucket (35%): Liquid Staking of major assets (ETH, SOL). This provides core network yield and maintains capital efficiency for future opportunities.

- High-Risk Bucket (15%): Volatile yield farming, typically in high-fee pairs (or new protocol liquidity mining). This capital is expendable and allocated only for high-potential returns.

Best Practices and Risk Management for Beginners

Passive income in DeFi is not risk-free. Before deploying capital, focus on minimizing preventable errors.

Rule #1: Smart Contract Audit Diligence

Every DeFi interaction involves smart contracts—the immutable code that governs transactions. If this code contains a bug, your funds are at risk.

- Practice: Always prioritize established protocols (Aave, Compound, Lido) that have been running for years and have undergone numerous third-party security audits. New protocols offering exceptionally high APYs are exponentially riskier. Check the protocol’s documentation for audit reports and TVL (Total Value Locked) as a proxy for trust and usage.

Rule #2: Understanding Gas Fees and Net Profit

Transaction fees (gas) are required to execute any action on a blockchain, especially Ethereum. Gas costs can sometimes exceed the potential profit of a small DeFi position.

- Strategic Tip: Before entering a yield farm, calculate your potential net profit after accounting for all transaction costs (deposit, claim rewards, withdrawal). Strategies that require constant interaction (like harvesting small reward tokens daily) can easily be wiped out by high gas costs. For smaller accounts, focus on low-interaction strategies like simple lending or delegated staking on chains with lower transaction fees.

Rule #3: Start with Stablecoins

If you are a beginner, your biggest risk is asset volatility, not smart contract failure. By using stablecoins (cryptocurrencies pegged 1:1 to the US Dollar), you eliminate volatility risk and allow yourself to focus solely on mastering the mechanics of the DeFi protocol.

- Lending Start: Start by lending USDC on a platform like Aave. You learn how to deposit, track your yield, and withdraw, all while knowing that $100 deposited will still be worth $100 (plus interest) when you retrieve it.

Rule #4: Know Your Exit Strategy

Passive income often involves accumulating reward tokens (like CRV, UNI, or the farm's native token). These tokens often have fluctuating value. Strategic investors define two conditions before they enter a position:

- When to Claim Rewards: Do you claim rewards weekly, monthly, or when gas is low?

- When to Exit the Position: What specific change (e.g., APY drops below 5%, the price of the asset pair changes significantly, or the overall market turns bearish) triggers a full withdrawal?

Conclusion

The journey into DeFi passive income is a spectrum, moving from the stable, reliable yields of staking and lending toward the complexity and high risk of active yield farming. For the strategic beginner, the initial focus should be on building a resilient foundation using staking (leveraged by LSTs for liquidity) and stablecoin lending for predictable cash flow.

Only after mastering these foundational pillars and fully internalizing the risks associated with Impermanent Loss should an investor venture into the higher-risk, higher-reward territories of volatile yield farming or restaking. By adopting a comparative, risk-aware framework, you can transform from a passive holder of crypto assets into a highly strategic DeFi investor.