The world of crypto trading is relentless. While manual traders rely on clicking buttons and reading charts, true speed and efficiency in day trading are achieved through automation. Moving from manual execution to an algorithmic system is the natural progression for any serious day trader seeking optimal pricing and minimal execution delay.

This transition is often misunderstood. Many believe high-frequency trading (HFT) is only for large financial institutions. However, the fundamental tools used for automated speed—Application Programming Interfaces (APIs) and simple execution algorithms—are now readily available to individual retail traders on major crypto exchanges. By leveraging these tools, you can ensure your orders are executed not just quickly, but intelligently, minimizing market impact and maximizing profitability potential.

This guide provides a comprehensive, beginner-friendly framework for understanding, setting up, and managing the technical backbone required for high-frequency day trading automation. We will move beyond simply running a pre-built trading bot and focus on the technical details necessary to build a truly efficient, speed-focused execution engine.

The Foundation: Understanding Trading Automation and Speed

Before setting up any code, it is vital to understand the difference between standard trading bots and speed-focused automated execution, as well as the fundamental role that latency plays in successful high-frequency strategies.

Manual vs. Algorithmic Trading: Why Automate?

When you place a manual trade, you face two primary enemies: emotional bias and execution delay (latency).

- Eliminating Emotion: Automated systems execute based purely on predefined logic. They don't panic during flash crashes or get greedy during parabolic rises. This disciplined approach is crucial for consistency.

- Achieving Speed: Even the fastest human reaction time is orders of magnitude slower than a computer. In fast-moving markets, milliseconds matter. Algorithmic systems can monitor dozens of data points and react instantaneously, submitting or canceling orders faster than you can blink.

- Managing Market Impact: If you try to buy a very large amount of a low-liquidity crypto all at once, your single order will drive the price up against you, a phenomenon called slippage. Automation allows you to slice that large order into many smaller pieces, strategically released to the market over time, minimizing this impact.

Defining High-Frequency Trading (HFT) vs. Algorithmic Trading (AT)

The term "algorithmic trading" is an umbrella term for any trading strategy executed by a computer program. This includes simple grid bots, long-term trend-following systems, and even execution algorithms like VWAP (which we discuss later).

High-Frequency Trading (HFT) is a specific subset of AT defined by its emphasis on extremely low latency (sub-millisecond execution) and rapid turnover of trades. HFT strategies typically involve holding assets for only seconds or minutes.

For the retail trader, achieving true institutional-level HFT is challenging and expensive (requiring co-location). However, the principles of minimizing latency and automating execution through APIs are accessible and essential for advanced day trading. We are aiming for high-speed algorithmic execution, utilizing HFT principles to gain a competitive edge over manual traders.

The Role of Execution Speed (Latency)

Latency is simply the time delay between an event occurring (e.g., a new order appearing on the exchange) and your system successfully processing that event and taking action (e.g., submitting your own order).

In high-speed trading, latency dictates profitability. If your competitor sees a profitable opportunity and places their order 100 milliseconds faster than you, they will secure the trade, and you will miss the optimal entry price, or worse, face adverse slippage.

Understanding and minimizing the latency introduced by three main factors is the core technical challenge of automation:

- Network Latency: The time it takes for data to travel over the internet (distance between your server and the exchange).

- API Latency: The speed at which the exchange's systems process your request.

- Code Latency: The time your own program takes to receive data, analyze it, and generate an order.

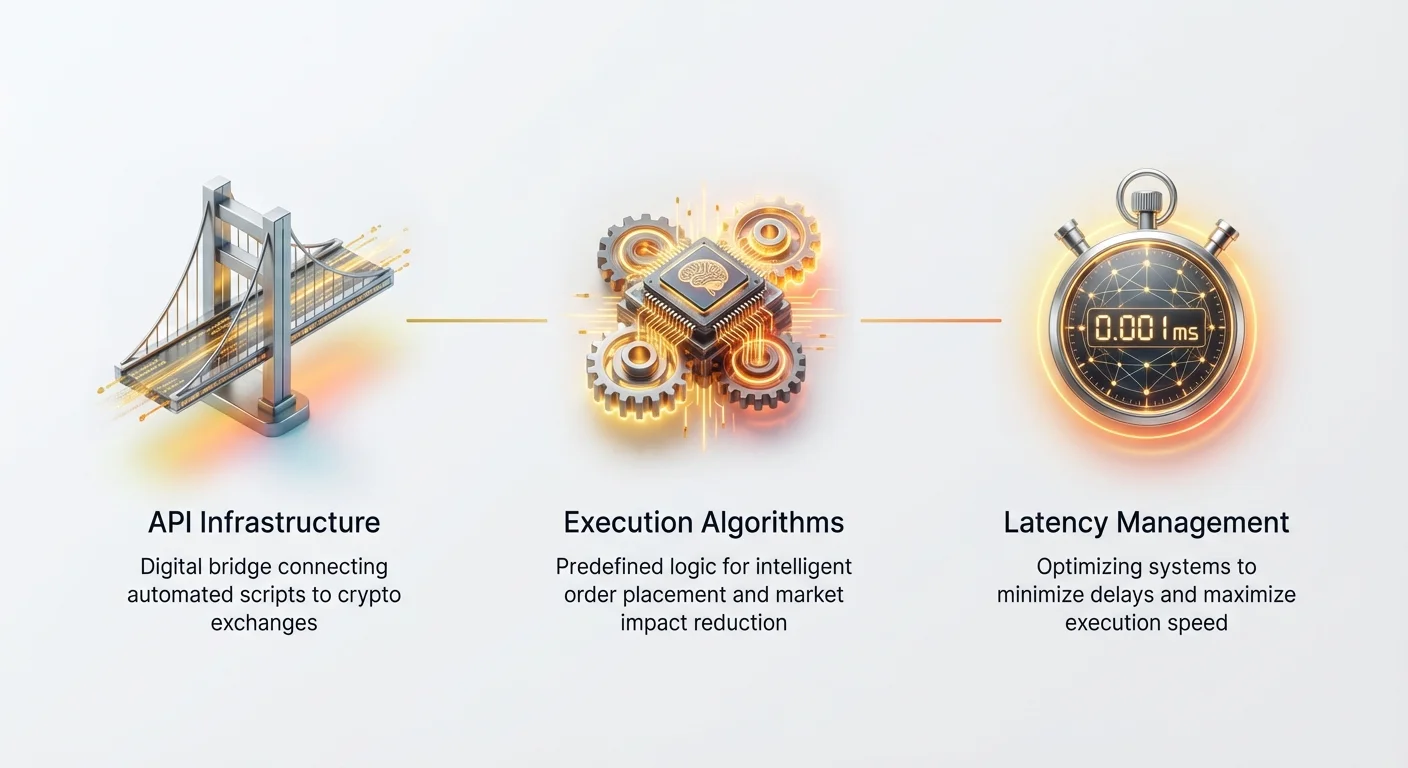

Choosing the Right API Infrastructure

The Application Programming Interface (API) is the digital bridge between your automated trading script and the crypto exchange’s order book. Choosing and configuring this infrastructure correctly is the most important technical step.

REST vs. WebSocket APIs: The Need for Speed

Exchanges typically offer two primary types of APIs for interacting with their systems:

1. REST APIs (Representational State Transfer)

REST APIs operate on a request/response cycle.

- How it works: Your program sends a request (e.g., "What is my current balance?" or "Place a Market Buy order"), and the exchange sends a one-time response.

- Use Cases: Placing orders, managing accounts, fetching historical data (candles).

- Speed Limitation: For every piece of information you need, you must initiate a brand-new connection and wait for the response. This creates unnecessary latency for real-time data needs.

2. WebSocket APIs

WebSockets establish a persistent, two-way communication channel between your server and the exchange.

- How it works: Once connected, the exchange streams real-time data to you automatically without you having to ask for it repeatedly. This is a constant flow of information.

- Use Cases: Receiving real-time market data (ticker prices, order book updates, trade executions) and receiving personalized user updates (fills, cancellations).

- Speed Advantage: WebSockets are essential for high-frequency strategies. They drastically reduce network overhead, allowing your algorithm to receive critical pricing information immediately—often in sub-millisecond timeframes—which is crucial for timely execution.

Actionable Tip: Any strategy relying on instant market reactions (e.g., executing based on the current highest bid) must utilize WebSocket feeds for data ingestion. Use REST only for slower administrative tasks like checking P&L or fetching historical data.

Essential API Functions for Automation

Regardless of the exchange you choose, your automation system must master a few core API functions:

- Authentication: Securely signing your requests using your private API key and secret key. This proves to the exchange that you are who you say you are and grants access to your trading account.

- Data Retrieval (Market Data): Fetching the essential information required to make decisions:

- Tick Data: The raw stream of every trade executed.

- Order Book Depth: The volume of buy (bids) and sell (asks) orders currently at various price levels.

- User Data: Your current open orders and account balance.

- Order Placement and Management: The ability to submit, modify, and cancel orders instantly. The speed of the

cancelOrderfunction is arguably as important asplaceOrder, especially in HFT, where market conditions change rapidly.

Selecting a Reliable Exchange Partner

Not all crypto exchanges are created equal when it comes to automation infrastructure. When selecting a platform for high-frequency work, evaluate these criteria:

- API Stability and Uptime: The exchange’s API must be robust. Frequent downtime or connection issues will lead to missed trades and potential errors.

- Rate Limits: Exchanges impose limits on how many API calls you can make per second (rate limits). High-frequency systems require generous limits. Look for exchanges that offer higher tiers for active traders or market makers.

- Liquidity and Volume: Execution is useless if there’s no one to trade with. You need deep liquidity (high trading volume) to ensure your large orders can be executed without causing excessive slippage. Popular derivative markets (like perpetual futures) often offer the deepest liquidity for automation.

- Clear Documentation: Comprehensive and well-maintained API documentation is non-negotiable for developers.

Developing Basic Execution Algorithms

Execution algorithms (Algos) are designed to handle the intelligent placement of large orders, ensuring they are filled at the best possible price while minimizing disruption to the market. For beginners in automation, mastering the Time-Weighted Average Price (TWAP) and Volume-Weighted Average Price (VWAP) algorithms provides a strong foundation.

What is an Execution Algorithm?

An execution algorithm is a predefined set of instructions that determines how a large trade is broken down and submitted to the market. Its purpose is not to decide when to trade (that’s the strategy), but how to execute a trade once the strategic decision has been made.

If your strategy determines you should buy 50 BTC right now, the execution algo takes over and manages the submission of those 50 BTC into the market in a controlled manner.

Time-Weighted Average Price (TWAP) Strategy Explained

TWAP is the simplest and most common execution algorithm. It aims to distribute a large order evenly over a specified period of time. The goal is to achieve an execution price close to the average price of the asset during that time window.

How TWAP Works:

- Define Total Quantity: E.g., Buy 100 ETH.

- Define Time Window: E.g., Execute over 60 minutes.

- Calculate Slice Size: 100 ETH / 60 minutes = 1.66 ETH per minute.

- Execution: The algorithm submits small market or limit orders (1.66 ETH) at regular, one-minute intervals until the total quantity is filled.

Use Case: TWAP is highly effective in markets with low or stable volatility when your primary concern is preventing market impact. By slowly feeding orders into the book, you disguise your true intention (buying 100 ETH), preventing other traders from front-running you or adjusting prices adversely.

Implementation Tip: A robust TWAP algorithm must handle two failure modes:

- Unfilled Orders: If a slice doesn't fill completely, the algorithm must decide whether to resubmit the remainder immediately or wait for the next scheduled interval.

- Market Changes: If the price moves significantly during the execution window, the algorithm may need parameters that allow it to pause or accelerate execution.

Volume-Weighted Average Price (VWAP) Strategy Explained

VWAP is a more sophisticated execution algorithm that aims to execute an order at a price close to the market's true Volume-Weighted Average Price for a given period. Unlike TWAP, which distributes orders based on time, VWAP distributes orders based on the expected distribution of trading volume.

How VWAP Works:

- Analyze Historical Volume: The algorithm first looks at historical trading data for the chosen asset (e.g., Bitcoin) to determine what percentage of the total daily volume typically occurs during specific time blocks (e.g., 9:00 AM to 10:00 AM might see 15% of the total volume).

- Define Target: E.g., Buy 100 BTC between 9:00 AM and 5:00 PM.

- Real-Time Execution: The algorithm monitors current market volume in real time. If 15% of the day’s volume occurs between 9:00 AM and 10:00 AM, the VWAP algorithm will attempt to execute 15% (15 BTC) of the 100 BTC order during that hour. It constantly adjusts the pace of execution to match the actual market volume flow.

Use Case: VWAP is ideal when you want to minimize your market footprint by blending in with natural market activity. If the market is quiet, the algorithm slows down; if volume spikes, it accelerates execution to fill more of your order during periods of deep liquidity.

VWAP Challenge: VWAP requires continuous monitoring of real-time volume data, meaning it is more complex to program and requires reliable, low-latency WebSocket connections to be effective.

Latency Management and Optimizing Execution Speed

In automated trading, speed is paramount. Latency management involves aggressively identifying and eliminating time delays throughout your system, from your server’s physical location to the efficiency of your code.

The Enemy: Network Delay and Data Processing

Network latency is primarily determined by distance. Since internet data travels through fiber optic cables at near the speed of light, the closer your trading server is physically to the exchange’s server, the faster your connection will be.

A retail server running from a home computer across the country might have 50-100ms (milliseconds) of network latency to a major exchange. An optimized setup aiming for speed needs to drive that number down to under 5ms, or ideally, 1ms.

Beyond network delay, consider data processing delay. This is the time your own computer spends:

- Receiving data packets (e.g., a new order book update).

- Parsing the data (turning raw text into usable numbers).

- Running the decision logic (if price > X, then buy).

- Formatting and encrypting the outgoing order.

Every line of inefficient code adds delay. In HFT, developers focus obsessively on minimizing memory allocation and garbage collection because those operations can introduce critical, measurable delays.

Co-location and Proximity Hosting (The Ultimate Speed Boost)

For traders pursuing the absolute fastest execution (sub-1ms), proximity hosting or co-location is the standard solution.

- Co-location (Institutional Level): This involves renting space inside the same data center, or even the same rack, where the exchange hosts its servers. This eliminates almost all external network travel, reducing latency to physical cable length (measured in microseconds). This is very expensive and generally unnecessary for retail traders unless they have significant capital and are pursuing pure arbitrage strategies.

- Proximity Hosting (Retail Level): This involves renting a Virtual Private Server (VPS) that is geographically located as close as possible to the exchange’s data center (e.g., hosting your server in the same major city or availability zone). This is a practical compromise that dramatically lowers network latency for retail traders, usually offering latency in the 2ms to 10ms range.

Actionable Tip: If you plan to trade frequently, abandon your home internet connection. Invest in a dedicated, high-performance VPS service located near the exchange’s physical data centers. Many exchanges publish their recommended server locations.

Techniques for Reducing Local Latency (Code Optimization)

While hardware and location matter, efficient code is essential for minimizing local latency:

- Use Efficient Programming Languages: While Python is excellent for rapid prototyping and general algorithmic trading due to its ease of use and libraries, languages like C++ or Rust often provide significantly faster execution times for pure, speed-critical HFT logic because they manage memory more directly. For most retail automation, Python remains adequate, but understanding its limitations is important.

- Optimize Data Structures: Use data structures (like dictionaries or hash maps) that allow for extremely fast lookup times when managing orders and market data. Avoid inefficient loops or slow list searches.

- Parallel Processing (Multithreading): Your program should ideally not halt trading execution while waiting for market data. Use separate threads or asynchronous programming (common in Python with

asyncio) to ensure:- Thread 1: Manages the WebSocket connection and incoming data.

- Thread 2: Executes the trading logic and order submission.

- Thread 3: Manages monitoring and logging. This ensures that data is processed and orders are submitted without waiting for slow I/O (input/output) operations.

Security Best Practices for Automated Trading

An automated trading system represents a direct, continuous link to your exchange account and funds. Because your system operates 24/7 without direct human oversight, security and contingency planning are critically important.

API Key Management and Permissions

Your API keys are the master controls to your account. Treating them like passwords is insufficient—they must be guarded with extreme vigilance.

- Principle of Least Privilege: When generating API keys on your exchange, assign them the minimum necessary permissions. If your bot only needs to trade spot BTC, do not grant it permission to withdraw funds, manage derivatives, or access your wallet history. If the key is compromised, the damage is strictly limited to trading activity.

- Environmental Variables (Best Practice): Never hard-code your API keys (the actual text strings) directly into your script. If you accidentally share your code or upload it to a public repository like GitHub, your keys are exposed. Instead, load keys dynamically from secure environment variables on your trading server. This keeps the sensitive credentials separate from the code logic.

- IP Whitelisting: If your exchange supports it, restrict API key access to only a single, known IP address—that of your dedicated trading VPS. If someone manages to steal your keys but tries to use them from a different location, the exchange will automatically reject the request.

Implementing Fail-Safes and Kill Switches

Even the most robust algorithm can encounter unforeseen market conditions or technical bugs. A runaway bot can execute hundreds of bad trades in minutes. A mandatory component of any automated system is a contingency plan.

1. The Global Kill Switch

This is an emergency function that immediately cancels all open orders and shuts down the trading logic loop.

- Mechanism: Implement a simple external trigger, such as checking a specific file or database flag. If the flag is set (e.g.,

kill_switch = True), the bot executes the emergency shutdown procedure. - Access: This switch should be easily accessible from your mobile phone or a secure web interface, allowing you to stop the bot instantly even if you are away from your main computer.

2. Risk Limits (Circuit Breakers)

Programmatic limits must be integrated directly into your bot’s decision-making logic:

- Daily Loss Limit: If the bot’s Profit and Loss (P&L) crosses a specific threshold (e.g., -5% in 24 hours), all trading must stop immediately, and an alert must be sent.

- Max Exposure Limit: Limit the maximum capital the bot can commit at any given moment (e.g., never hold more than 5 BTC).

- Maximum Open Order Count: If the bot submits more than a reasonable number of orders in a short time, it may indicate a technical loop error, triggering a shutdown.

Protecting Your Code and Infrastructure

Your trading strategy is your intellectual property. Protect the physical and virtual location where your code runs.

- VPN and Server Hardening: Always connect to your VPS using a secure SSH client and ensure your server software is routinely updated. Disable unnecessary ports and services that could present security vulnerabilities.

- Encrypted Storage: If you must store historical trade data or log files, ensure they are encrypted, especially if they contain any information about your account or trade secrets.

- Redundancy and Logging: Ensure continuous, detailed logging of all API interactions (requests and responses). If a trade goes wrong, you must have a clean log to diagnose whether the error originated in your code, the network, or the exchange’s API.

Getting Started: Tools and Practical Steps

Moving from theory to practice requires selecting the right tools and following a clear, step-by-step process to establish your first automated connection.

Recommended Programming Languages (Python Focus)

For most new traders entering the automation space, Python is the recommended choice.

Why Python?

- Readability: Python’s structure is clean and easy to read, reducing the chance of subtle errors creeping into the logic.

- Extensive Libraries: Python offers ready-made libraries (e.g.,

requests,pandas, and specialized libraries likeccxtwhich unify interactions across multiple exchanges) that handle complex tasks like API authentication, data manipulation, and historical backtesting. - Asynchronous Capabilities: Modern Python (

asyncio) is well-suited for managing the simultaneous demands of monitoring WebSockets and submitting orders without blocking the execution loop—a crucial feature for low-latency systems.

While other languages like Java, C#, or Go are used for institutional-level HFT, Python provides the fastest ramp-up time for developing and testing execution algorithms like TWAP and VWAP.

Step-by-Step API Connection Checklist

Follow this checklist to establish your foundational automated connection:

Phase 1: Preparation

- Exchange Selection: Choose an exchange known for stable APIs and high liquidity (as discussed previously).

- API Key Generation: Generate a new API key pair. Only grant necessary permissions (e.g., "Read Market Data" and "Trade"). Do not grant withdrawal access.

- Setup VPS: Rent a proximity-hosted VPS and configure its firewall to allow only essential ports (SSH, and outgoing connections for trading).

- IP Whitelisting: Whitelist the VPS IP address on your exchange’s API key settings.

Phase 2: Initial Connection

- Install Python Environment: Install Python and necessary libraries (e.g.,

requestsfor REST,websocket-clientfor WebSockets). - Secure Key Storage: Store your API key and secret key as environment variables on the VPS.

- Test REST Connection: Write a simple script to use the REST API to fetch a static piece of information, like your current account balance, ensuring authentication is successful.

- Test WebSocket Connection: Write a script to connect via WebSocket and print the real-time stream of the BTC/USD ticker price. This confirms low-latency data ingestion.

Phase 3: Order Execution Test

- Place a Small Order: Using the REST API, submit a tiny limit order (e.g., $1 worth of Bitcoin) to confirm the order submission function works. Immediately cancel the order.

- Implement the Kill Switch: Verify your emergency kill switch mechanism functions correctly, instantly halting the script and canceling any open orders.

The Importance of Paper Trading (Simulation)

Never deploy a new algorithmic strategy—especially one focused on high-speed execution—to a live account immediately.

Paper Trading (or simulation) involves executing your algorithm against real-time market data without risking real capital. Most major crypto exchanges offer test environments or "paper trading" accounts that mirror the live API structure.

Benefits of Simulation:

- Validate Logic: Ensure your TWAP or VWAP logic calculates slice sizes and execution frequency correctly.

- Test Failure Modes: Stress-test the algorithm by simulating market drops or network disconnections to ensure your fail-safes and cancellation logic work properly.

- Assess Latency Impact: Even in a simulated environment, monitor the time delay between receiving market data and submitting the simulated order. This helps confirm whether your VPS setup and code optimization are effective.

Only after a strategy has run successfully for several weeks in a paper trading environment and you have complete confidence in its technical stability should you transition to using a small amount of live capital.

Conclusion

The shift from manual day trading to high-frequency automation marks a crucial evolution in a trader’s journey. It moves the focus from predicting market movements to optimizing the precision and speed of execution.

By mastering the technical infrastructure—specifically, relying on fast WebSocket APIs, implementing foundational execution algorithms like TWAP and VWAP, and aggressively managing latency through proximity hosting and code optimization—you gain a measurable edge over the vast majority of retail traders.

Remember that while speed is critical, security is non-negotiable. A disciplined approach to API key management, coupled with robust kill switches and circuit breakers, ensures that your automated system operates efficiently and responsibly. Automated trading is a continuous learning process; start small, test rigorously, and maintain an unwavering focus on minimizing every millisecond of latency.