Converting digital assets into fiat currency is a fundamental skill for any cryptocurrency participant. While the entry points into the crypto ecosystem are often streamlined, the process of exiting—or "off-ramping"—can present unique challenges regarding liquidity, fees, and asset flow optimization.

Off-ramping refers to the mechanism of selling cryptocurrency in exchange for government-issued currency, such as the US Dollar, Euro, or Yen. This process requires an interface that connects the blockchain network with the traditional banking system. Unlike digital-to-digital trades, which occur seamlessly on the blockchain, off-ramping involves regulatory compliance and banking infrastructure.

Investors must navigate various platforms to find the most efficient route for their specific needs. Factors such as transaction speed, privacy requirements, and the volume of assets being sold play a critical role in determining the best strategy.

The Centralized Exchange Ecosystem

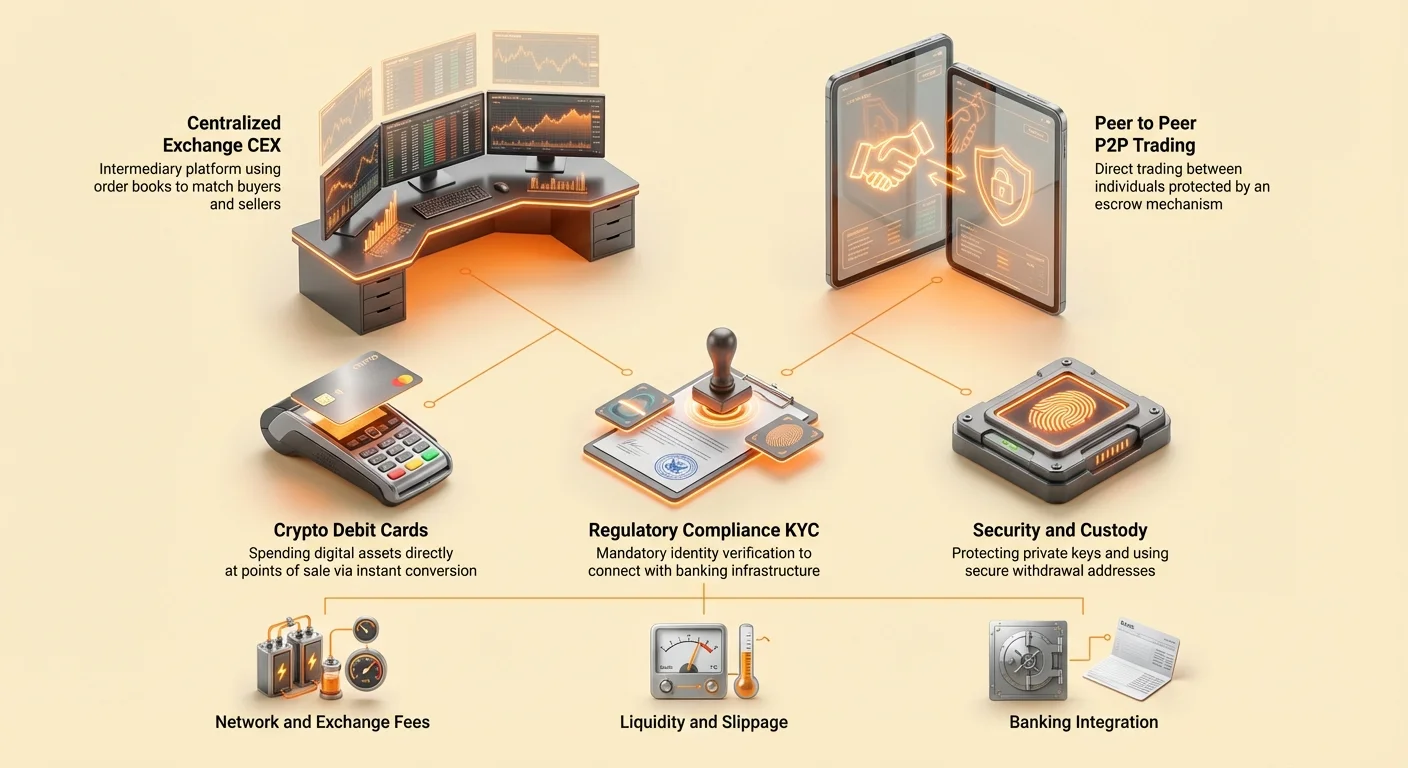

Centralized exchanges (CEXs) represent the most common venue for converting cryptocurrency into fiat. These platforms operate as intermediaries, facilitating trades between buyers and sellers while maintaining custody of the assets during the transaction.

Order Books and Market Depth

The core functionality of a centralized exchange revolves around the order book. This digital ledger records all buy and sell interest for a specific asset at various price points. When a user initiates a sale, the exchange matches their request with a corresponding buy order from another user.

Market depth refers to the volume of orders available at different price levels. An exchange with deep liquidity can handle large sell orders without causing significant price slippage. Slippage occurs when there are not enough buyers at the current market price to fulfill a large order, forcing the seller to accept progressively lower prices to complete the transaction.

Makers and Takers

Participants in this ecosystem are categorized as either makers or takers. Makers are traders who place limit orders that do not execute immediately. By doing so, they add liquidity to the order book, effectively "making" the market.

Takers are traders who accept existing orders from the book, usually through market orders that execute instantly. Because takers remove liquidity from the platform, they often pay higher fees than makers. Understanding this dynamic is crucial for optimizing the costs associated with selling large positions.

Banked versus Partially Banked Platforms

Not all centralized exchanges offer the same level of integration with the traditional financial system. Fully banked exchanges allow users to deposit and withdraw fiat currency directly to a bank account. These platforms act as comprehensive bridges between the crypto and fiat worlds.

Partially banked exchanges might allow users to purchase crypto using credit cards or payment apps but may restrict withdrawals to crypto-only transfers. When selecting an off-ramp, it is essential to verify that the platform supports fiat withdrawals to your specific region and banking institution.

Navigating Peer-to-Peer Trading

Peer-to-Peer (P2P) trading offers a decentralized alternative to the automated matching engines of centralized exchanges. These platforms allow individuals to trade directly with one another, negotiating terms and payment methods without a central authority processing the transaction.

The Escrow Mechanism

Trust is the primary challenge in direct trading. To solve this, P2P platforms utilize escrow services. When a trade is initiated, the seller's cryptocurrency is locked in a secure digital vault controlled by the platform.

The buyer then proceeds to send the agreed-upon fiat payment directly to the seller. This payment can take many forms, including bank transfers, digital wallet payments, or even cash in person. Once the seller confirms receipt of the funds, the platform releases the cryptocurrency from escrow to the buyer. This system protects both parties from fraud.

Privacy and Flexibility

One of the distinct advantages of P2P trading is the flexibility of payment methods. While centralized exchanges are often limited to wire transfers or card payments, P2P marketplaces can support hundreds of local payment options. This is particularly valuable in regions where banking access is limited or restricted.

Privacy is another consideration. While many P2P platforms now require identity verification, the direct nature of the payment means that the transaction details on bank statements often appear as transfers to individuals rather than to known cryptocurrency exchanges.

Risk Management in P2P

Despite the protections offered by escrow, P2P trading carries inherent risks. Users must be vigilant against social engineering scams or fraudulent payment proofs. Most platforms implement a reputation system, displaying a user's trade history and feedback rating.

Engaging only with traders who have established high reputation scores significantly reduces the risk of encountering bad actors. Additionally, all communication and trade details should remain within the platform to ensure that dispute resolution services can be utilized if necessary.

| Feature | Centralized Exchange (CEX) | Peer-to-Peer (P2P) |

|---|---|---|

| Speed | Instant execution | Depends on counterparty |

| Price | Determined by market | Negotiated between users |

| Privacy | Lower (Strict KYC) | Higher (Varies by platform) |

Bridging with Crypto Debit Cards

For many users, the goal of off-ramping is not to hold cash in a bank account but to purchase goods and services. Crypto debit cards effectively skip the withdrawal step by allowing digital assets to be spent directly at points of sale.

Real-Time Conversion

These cards function similarly to prepaid debit cards but are funded with cryptocurrency. When a purchase is made, the card provider instantly converts the necessary amount of crypto into fiat currency to pay the merchant.

This process, often called "auto-conversion," allows users to keep their wealth in digital assets until the exact moment of expenditure. This eliminates the need to plan sales in advance or wait for bank transfers to clear.

Virtual versus Physical Cards

Providers typically offer both virtual and physical card options. Virtual cards are issued almost instantly and are designed for online commerce. They exist only as data within a mobile app or wallet.

Physical cards allow for in-person transactions at brick-and-mortar stores and can often be used to withdraw cash from standard ATMs. This feature essentially turns any ATM into a crypto off-ramp, providing immediate access to physical cash without going through a bank.

Fee Structures

Convenience often comes at a cost. Crypto debit cards may carry specific fees that differ from standard exchanges. Users should be aware of conversion fees charged at the point of sale.

Additionally, there may be issuance fees for physical cards or monthly maintenance fees. However, many providers offset these costs by offering rewards programs, such as cashback paid in cryptocurrency, which can enhance the overall value proposition.

The Mechanics of Stablecoins

Stablecoins provide a strategic middle ground for traders who wish to exit volatile positions without immediately converting to fiat currency. These digital assets are pegged to the value of a stable asset, most commonly the US Dollar.

Escaping Volatility

Cryptocurrency markets operate 24/7 and can experience rapid price fluctuations. Selling volatile assets like Bitcoin or Ethereum into a stablecoin allows a trader to "lock in" the value of their portfolio.

This is particularly useful during times of market uncertainty. Once the value is secured in a stablecoin, the trader can decide whether to re-enter the market later or proceed with a fiat withdrawal at their convenience. This separation of trading decisions from banking logistics reduces emotional pressure.

DeFi Integration

Stablecoins also grant access to Decentralized Finance (DeFi) protocols. Instead of sitting idle, funds held in stablecoins can be deployed into lending pools or yield farming strategies.

This capability allows capital to remain productive even when it is not invested in volatile assets. When the user is finally ready to cash out to a bank account, the stablecoins can be moved to a centralized exchange and sold for fiat currency.

Understanding the Fee Landscape

Every off-ramp method incurs costs. Minimizing these fees requires an understanding of the different types of charges applied at various stages of the transaction.

Network Fees Explained

Network fees are paid to the miners or validators who secure the blockchain. These fees are required whenever crypto is moved from a personal wallet to an exchange.

The cost is determined by the demand for block space at the time of the transaction, not the value of the transfer. During periods of high network congestion, these fees can rise significantly. Users can often customize these fees in their wallet settings, choosing to pay less in exchange for slower confirmation times.

Exchange and Withdrawal Costs

Exchange services charge fees to facilitate the trade from crypto to fiat. These are typically calculated as a percentage of the transaction value. Withdrawal fees are then charged to move the fiat currency from the exchange to a bank account.

It is important to check the fee schedule of any platform before trading. Some exchanges may offer low trading fees but charge high rates for fiat withdrawals, or vice versa.

The Maker-Taker Model

On centralized exchanges, the fee you pay often depends on whether you are a maker or a taker. Makers, who provide liquidity by placing limit orders, are often rewarded with lower fees.

Takers, who remove liquidity by executing market orders, generally pay higher rates. For large off-ramp transactions, using limit orders to act as a maker can result in significant savings compared to an instant market sell.

Security and Custody Considerations

The safety of funds during the off-ramp process is paramount. Understanding the difference between custodial and non-custodial storage is the first step in securing assets.

The Risks of Centralization

When funds are deposited onto a centralized exchange, the user effectively hands over control of those assets to the platform. The user no longer possesses the private keys.

History has shown that exchanges can be vulnerable to hacks, mismanagement, or insolvency. Therefore, it is a best practice to only keep funds on an exchange for the short duration required to execute a trade and withdraw the fiat. Long-term storage should be avoided on these platforms.

Self-Custody Best Practices

Self-custody wallets give the user complete control over their private keys. Assets held in these wallets are immune to exchange failures. When preparing to off-ramp, funds should be moved from cold storage (offline hardware wallets) or self-custody apps directly to the exchange only when necessary.

Maintaining strict hygiene regarding private keys and recovery phrases ensures that the assets remain secure until the moment they are sold.

Protecting Your Data

Security extends beyond the assets themselves to personal information. When using regulated exchanges, users must submit sensitive identity documents.

It is crucial to use unique, strong passwords for exchange accounts and to enable Two-Factor Authentication (2FA). Hardware keys or authenticator apps are superior to SMS-based 2FA, which can be vulnerable to SIM-swapping attacks.

Regulatory Compliance and Identity

The interface between crypto and fiat is heavily regulated. To operate legally, exchanges must comply with financial laws designed to prevent illicit activity.

Know Your Customer (KYC)

Know Your Customer (KYC) regulations require exchanges to verify the identity of their users. This process typically involves submitting a government-issued ID, a selfie, and proof of address.

While this process removes anonymity, it adds a layer of legitimacy and security to the platform. It enables the exchange to offer connections to the traditional banking system, which is necessary for fiat withdrawals.

Anti-Money Laundering (AML)

Anti-Money Laundering (AML) protocols are used to monitor transactions for suspicious activity. Exchanges may flag deposits coming from known illicit addresses, such as those associated with darknet markets or theft.

Users should be aware that their transaction history on the blockchain is public. Sending funds from a reputable source helps ensure a smooth off-ramp experience without triggering AML freezes.

Tiered Verification

Many exchanges employ a tiered verification system. Lower levels of verification may allow for crypto-to-crypto trading but restrict fiat withdrawals.

Higher tiers, which require more extensive documentation, unlock higher daily or monthly withdrawal limits. Users planning to off-ramp large amounts should complete the necessary verification steps in advance to avoid delays.

Alternative Off-Ramp Methods

Beyond standard exchanges and P2P markets, there are niche methods for converting crypto to cash that suit specific user needs.

Bitcoin ATMs

Bitcoin ATMs (BTMs) are physical kiosks that allow users to buy or sell cryptocurrency for cash. To sell, the user sends crypto to a specific address provided by the machine. Once the transaction is confirmed on the blockchain, the machine dispenses cash.

BTMs offer high speed and convenience, often with less stringent verification requirements for small amounts. However, they typically charge significantly higher fees than online exchanges, sometimes exceeding 10% of the transaction value.

Over-the-Counter (OTC) Desks

For high-net-worth individuals or institutions moving very large sums, standard exchanges may not be suitable due to liquidity constraints. OTC desks facilitate large trades privately.

In an OTC trade, the buyer and seller negotiate a price directly, and the trade is settled off the open order book. This prevents large sell orders from crashing the market price and ensures the seller receives a predictable rate.

Direct Brokerage Services

Brokerage platforms act as simplified intermediaries. Unlike exchanges with complex charts and order books, brokerages offer a simple "sell" button. The broker quotes a price, and if the user accepts, the broker executes the trade.

While user-friendly and ideal for beginners, brokerages often include a "spread" in the price, meaning the user gets slightly less than the market rate. This spread acts as the broker's fee.

Transaction Safety Protocols

Executing a transaction to off-ramp funds requires attention to detail. Crypto transactions are irreversible; if funds are sent to the wrong address, they are likely lost forever.

Address Verification

When depositing crypto to an exchange to sell, users must ensure they are sending to the correct address. Malware exists that can swap clipboard data, pasting a hacker's address instead of the intended destination.

Always double-check the first four and last four characters of the address before confirming the send. Many platforms also offer address whitelisting, allowing users to pre-approve specific withdrawal addresses for added security.

Test Transactions

For large transfers, it is advisable to send a small test amount first. Once the test transaction arrives safely and is confirmed by the exchange, the remaining balance can be sent.

This incurs a second network fee but provides invaluable peace of mind. It confirms that the network is functioning correctly and that the destination address is valid and under the user's control.

Network Selection

Many assets, particularly stablecoins, exist on multiple blockchains (e.g., Ethereum, Solana, Tron). When depositing to an exchange, it is critical to select the correct network.

Sending a token via the wrong network (e.g., sending an ERC-20 token to a TRC-20 address) can result in the permanent loss of funds. Exchanges will explicitly state which networks they support for deposits.

Liquidity Explained

Liquidity is a measure of how easily an asset can be converted into cash without affecting its price. It is a vital concept for anyone looking to sell cryptocurrency.

Financial Liquidity vs. Market Liquidity

In the broader financial sense, cash is the most liquid asset because it is universally accepted. Real estate is illiquid because finding a buyer takes time.

In the context of crypto markets, liquidity refers to the volume of active buy and sell orders. Bitcoin is highly liquid, meaning millions of dollars can be sold instantly with minimal price impact. Smaller "altcoins" may be illiquid, making it difficult to exit a position quickly.

Managing Slippage

When trading illiquid assets, slippage becomes a major risk. If a user tries to sell a large amount of a low-volume coin, they may exhaust the available buy orders at the current price.

To complete the order, the exchange matches the remaining sell volume with buy orders at lower and lower prices. To avoid this, traders should break large orders into smaller chunks or use limit orders to specify the minimum price they are willing to accept.

Tax Implications of Selling

It is important to recognize that selling cryptocurrency for fiat is a taxable event in many jurisdictions. When crypto is converted to cash, any profit realized from the sale is typically subject to capital gains tax.

Using stablecoins or purchasing goods with a crypto debit card does not necessarily exempt the user from tax obligations. Most tax authorities view spending crypto as a sale of the asset at its fair market value at the time of the transaction.

Record-keeping is essential. Users should maintain detailed logs of their cost basis (the original value of the asset when acquired) and the sale price. Many exchanges provide transaction history exports that can be used to calculate tax liabilities accurately.

Conclusion

Mastering the art of off-ramping is as critical as learning to invest. The transition from digital assets to fiat currency involves balancing convenience, cost, and security. Centralized exchanges offer deep liquidity and banking integration, making them the standard choice for most users. However, they require trust and compliance with strict identity regulations.

For those prioritizing privacy or operating in regions with limited banking access, Peer-to-Peer platforms and Bitcoin ATMs serve as vital alternatives. Meanwhile, crypto debit cards and stablecoins provide flexibility, allowing users to spend or shield their wealth without immediately exiting the crypto ecosystem. Regardless of the method chosen, safeguarding private keys and verifying transaction details remain the foundation of a safe financial strategy.

The safest off-ramp strategy combines rigorous security practices with a clear understanding of fees and liquidity.