The financial landscape is currently undergoing a massive structural shift. This transformation is not merely about upgrading software or digitizing paper processes. It represents a fundamental divergence in how value is created, stored, and transferred. On one side stands Traditional Finance, or TradFi, a system built on centuries of established banking practices, intermediaries, and centralized authority. On the other side is Web3, a burgeoning ecosystem rooted in cryptography, decentralization, and peer-to-peer networks.

At the core of this comparison is the concept of the "opt-in" model versus the "by decree" model. Traditional fiat currency is money by government mandate. Citizens are compelled to use the currency of their nation, and their financial participation relies entirely on permissioned access granted by institutions. In contrast, cryptocurrency and Web3 assets are opt-in systems. They are controlled by the consensus of their users rather than a central bank.

This distinction creates two parallel worlds. One world relies on trusted third parties to maintain honesty and facilitate trade. The other relies on distributed infrastructure and code to verify ownership without a middleman. Understanding the friction between these two models requires looking at the bedrock of how they handle data, trust, and value.

The Architecture of Record Keeping

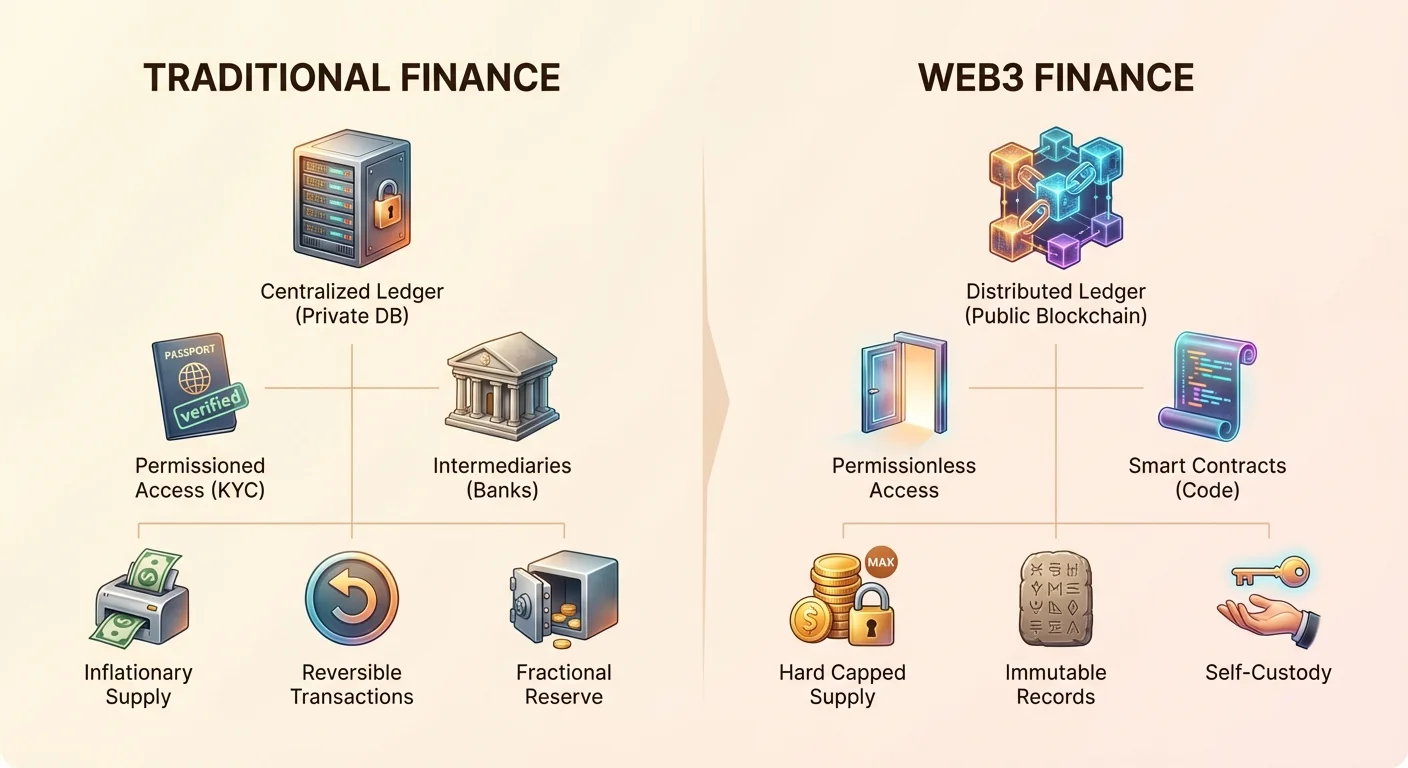

The primary difference between Web3 and TradFi lies in how they maintain the ledger. A ledger is simply the record of who owns what. In the traditional world, ledgers are private and centralized. Your bank maintains a database that says you have a specific amount of money. You cannot see this ledger directly; you can only see a representation of it through an app or statement. You trust the bank to keep this record accurate and secure.

Centralized Databases vs. Distributed Blockchains

In TradFi, the ledger is a single point of failure. If a bank’s server is hacked, corrupted, or physically destroyed, the record of funds can be compromised. To mitigate this, banks spend billions on cybersecurity and physical vaults. However, the control remains in the hands of a few executives and administrators. They have the power to alter the ledger, reverse transactions, or deny access to the data.

Web3 replaces this closed system with a blockchain. A blockchain is a digital record shared across a vast network of independent computers. No single entity owns the master copy. Instead, every participant in the network holds a copy of the ledger. When a transaction occurs, it must be verified by the network through a consensus mechanism. Once added to a block, the data is cryptographically linked to the previous block. This makes the history of transactions practically impossible to alter.

Immutability and Transparency

The result of this distributed architecture is immutability. In the context of Web3, this means that once a transaction is confirmed, it cannot be undone or tampered with. There is no administrator with a "delete" button. This feature builds trust mathematically rather than institutionally. In TradFi, a transaction can often be reversed days or weeks later due to disputes or administrative errors.

Transparency is the second major output of this architecture. Public blockchains allow anyone to audit the supply of the asset and the movement of funds. You do not need a subpoena or special permission to see transaction flows. While the identities of the users are often pseudonymous, the mechanics of the system are open for the world to verify. This contrasts sharply with the opaque nature of central banking reserves and commercial bank balance sheets.

The Evolution of Money

Money itself functions differently in these two environments. Throughout history, money has evolved from barter systems to commodity money like gold, and eventually to fiat currency. Fiat money is not backed by a physical commodity but by government decree and public trust. The value of fiat depends heavily on the stability of the issuing government and its monetary policy.

Inflation vs. Hard Capped Supply

One of the most significant points of friction between TradFi and Web3 is the management of supply. Fiat currencies are inflationary by design. Central banks have the authority to increase the money supply to manage economic crises or stimulate growth. While this provides flexibility, it also dilutes the purchasing power of existing holders over time. This phenomenon is often referred to as the "hidden tax" of inflation.

Crypto assets like Bitcoin were designed as a direct response to this. They often feature a hard cap on supply. For example, there will never be more than 21 million bitcoins. This scarcity is enforced by code, not policy. It mimics the properties of gold—rarity, durability, and divisibility—but adapts them for the digital age. This makes certain crypto assets function as a "store of value" that is immune to arbitrary supply expansion.

Unit of Account and Divisibility

Both systems struggle with different aspects of usability. Fiat currency excels as a unit of account because it is relatively stable day-to-day. Prices for goods and services are denominated in dollars or euros because the volatility is generally low. This makes fiat a reliable medium of exchange for daily coffee or rent payments.

Cryptocurrencies currently struggle with volatility, making them less ideal as a daily unit of account for small purchases. However, they offer superior divisibility. A single bitcoin can be divided into 100 million units called satoshis. This allows for micro-transactions that are often impossible in TradFi due to rounding errors or the high cost of processing small amounts.

Permission and Access

The traditional financial system operates on a permissioned basis. To open a bank account, you must prove who you are. This process, known as Know Your Customer (KYC), requires identity documents, proof of address, and often proof of income. While these regulations help preventing money laundering and terrorist financing, they also create massive barriers. Billions of adults worldwide remain unbanked because they lack the necessary paperwork or live in regions considered "high risk" by global banks.

The Permissionless Alternative

Web3 operates on a permissionless basis. The network does not care who you are, where you live, or what your credit score is. Creating a crypto wallet is a mathematical process, not a bureaucratic one. Anyone with an internet connection can download an app and generate a wallet address in seconds. There is no approval committee and no credit check.

This openness fundamentally changes who can participate in the global economy. A freelancer in a developing nation can receive payment from a client in New York without a bank intermediary. A refugee fleeing a war zone can carry their wealth in a digital wallet without fear of border guards seizing physical cash. The system is open to anyone who follows the protocol rules.

Identity and Privacy Trade-offs

The lack of gatekeepers introduces new responsibilities. In TradFi, if you lose your password, you can walk into a branch with your ID and regain access. The bank acts as a safety net for identity verification. In Web3, the user is solely responsible for their security. If you lose the private keys to your wallet, there is no customer service department to call. The funds are mathematically inaccessible.

Furthermore, privacy operates differently. In TradFi, the bank knows everything about your spending, but your neighbors do not. In Web3, your transactions are visible on the public ledger, but your identity is not necessarily attached to them. However, sophisticated analysis can often link wallet addresses to real-world identities, especially at the points where crypto is converted back to fiat.

Intermediaries vs. Smart Contracts

Efficiency in finance is often a function of how many hands the money must pass through. The traditional system is built on a stack of intermediaries. When you swipe a credit card, the transaction involves a merchant bank, a card network, an issuing bank, and a payment processor. Each step incurs a fee and adds time to the final settlement.

The Cost of Trust

These intermediaries exist to establish trust. The merchant needs to know the customer has the funds. The customer needs to know the merchant is legitimate. The banks act as the trusted brokers. This service is expensive. Cross-border payments, in particular, can take days to settle and cost significant percentages in fees. The "Correspondent Banking" system requires banks to hold accounts with each other globally, trapping liquidity and creating friction.

Automating Trust with Code

Web3 replaces these human and corporate intermediaries with smart contracts. A smart contract is code that automatically executes actions when certain conditions are met. For example, a decentralized exchange (DEX) allows users to trade assets directly with one another. The code ensures that the swap only happens if both parties provide the agreed-upon assets.

This creates "trustless" transactions. You do not need to trust the other trader; you only need to trust the code. Settlement on a blockchain is final once the block is confirmed. This can happen in minutes or seconds, regardless of whether it is a domestic or international transfer. The network operates 24/7, ignoring holidays and banking hours.

| Feature | Traditional Finance | Web3 Finance |

|---|---|---|

| Settlement | Days (T+2) | Minutes/Seconds |

| Operation | Banking Hours | 24/7/365 |

| Access | Permissioned (KYC) | Permissionless |

Custody and Ownership

The concept of ownership is perhaps the most philosophical difference between the two systems. In the traditional banking model, you do not technically own the money in your account. You have a claim on the bank. You are a creditor. The bank takes your deposit and lends it out to others to earn interest. This is known as fractional reserve banking.

Counterparty Risk and Bank Runs

Because banks lend out the majority of deposits, they do not have cash on hand to pay everyone at once. If confidence in the bank wavers, a "bank run" can occur. Depositors rush to withdraw their funds, and the bank collapses because it lacks liquidity. In these scenarios, governments often step in to insure deposits up to a certain limit, but amounts over that limit can be lost.

We have seen examples of this recently with the collapse of major regional banks. Furthermore, in times of extreme economic crisis, governments can impose capital controls, limiting how much of your own money you can withdraw or send abroad. Your access to your wealth is conditional on the solvency of the bank and the permission of the state.

Self-Custody and Sovereignty

Web3 introduces the capability for true self-custody of digital assets. If you hold your cryptocurrency in a non-custodial wallet, you possess the private keys. This is akin to holding digital cash. No bank is lending it out. No government can easily confiscate it without your key.

This eliminates counterparty risk. You do not need to worry if the blockchain is "solvent" because the blockchain does not lend out your funds. The asset sits at your address until you decide to move it. However, this total ownership means total liability. There is no fraud protection department to reverse a transaction if you send money to a scammer. You are your own bank, for better or worse.

Financial Products and Yield

The way users generate returns on their capital differs vastly between the two sectors. In TradFi, the primary vehicle for safe yield is the savings account or government bond. Historically, these yields have often been lower than the rate of inflation, meaning savers slowly lose purchasing power. The bank captures the majority of the profit generated from lending the customer's money.

The Rise of Decentralized Finance (DeFi)

DeFi opens up the "back end" of banking strategies to regular users. Through decentralized lending protocols, users can lend their assets directly to borrowers. The interest paid by borrowers goes to the lenders, with the protocol taking only a small fee for code maintenance. This creates a more efficient market where yields are typically higher, though risks are different.

Another mechanism is "yield farming" or liquidity provision. Users can deposit asset pairs into automated market makers (AMMs). By providing the liquidity that allows others to trade, they earn a portion of the trading fees. This turns passive capital into productive capital without the need for a financial manager.

Accessibility of Complex Instruments

In TradFi, high-yield products and complex derivatives are often restricted to "accredited investors"—wealthy individuals who meet specific income thresholds. This regulatory framework is intended to protect less sophisticated investors, but it also excludes them from the most lucrative opportunities.

DeFi platforms are agnostic to wealth. A user with $100 can access the same lending pools, trading strategies, and derivatives as a user with $10 million. While this democratizes access to wealth creation tools, it also exposes inexperienced users to high-risk mechanics they may not fully understand.

Censorship Resistance

Censorship resistance is the ability to transact freely without interference from a third party. In the traditional financial system, censorship is a feature, not a bug. Governments and banks use financial censorship to enforce laws, sanctions, and sometimes political agendas.

The Mechanism of Control

Financial censorship takes three main forms: freezing assets, blocking transactions, and confiscating funds. We have seen instances where payment processors block donations to political causes deemed controversial. Nations under sanctions lose access to the global banking network (SWIFT), affecting regular citizens alongside government officials. Even domestic legal disputes can result in frozen bank accounts before a trial concludes.

TradFi relies on a system of gatekeepers. If the gatekeeper decides you cannot enter, you are locked out of the economy. This power is consolidated in a few major institutions that act as de facto regulators of moral and political behavior through financial access.

Unstoppable Money

Web3 assets, particularly those like Bitcoin, are designed to be censorship-resistant. Because the network is decentralized, there is no CEO to call to block a transaction. Miners and validators are incentivized to process all valid transactions regardless of their origin or destination.

This property makes crypto a vital tool for human rights activists, journalists in authoritarian regimes, and individuals living under oppressive capital controls. It separates money from state. While governments can still target the "off-ramps" (where crypto is exchanged for fiat), they cannot easily stop the peer-to-peer transfer of value within the network itself.

Volatility vs. Stability

A common critique of Web3 is volatility. How can a currency replace the dollar if its value swings 10% in a day? TradFi offers stability in unit price (1 dollar always equals 1 dollar), although it suffers from the long-term instability of purchasing power degradation (inflation).

The Role of Stablecoins

To bridge this gap, the crypto industry developed stablecoins. These are tokens pegged to the value of a fiat currency, usually the US Dollar. They offer the speed and borderless nature of cryptocurrency with the price stability of fiat.

There are two main types: centralized and decentralized. Centralized stablecoins (like USDT and USDC) hold reserves of fiat in a bank to back their tokens. They act as a bridge, but they reintroduce counterparty risk—you must trust the issuer has the money. Decentralized stablecoins (like DAI) use over-collateralized crypto assets and smart contracts to maintain their peg.

Stablecoins have become the "killer app" for many users, allowing them to exit volatile markets without leaving the blockchain ecosystem. They also provide a lifeline for people in countries with hyperinflation, allowing them to hold digital dollars instead of a rapidly depreciating local currency.

Tokens and Governance

In TradFi, ownership in a project or company is represented by equity (stocks). Shareholders have rights to dividends and voting, but the voting process is often cumbersome and dominated by large institutional investors. Corporate governance is slow and opaque.

The Tokenization of Value

Web3 introduces tokens. A token can represent currency, but it can also represent utility, security, or governance rights. Utility tokens grant access to a service, similar to an arcade token or a software license. Security tokens are digital representations of traditional assets like real estate or company shares, subject to regulations.

Governance tokens allow holders to vote directly on changes to a protocol. This has given rise to Decentralized Autonomous Organizations (DAOs). In a DAO, decisions about treasury management, software upgrades, and fee structures are made by the community of token holders.

NFTs and Digital Uniqueness

Beyond fungible money, Web3 introduces Non-Fungible Tokens (NFTs). These represent unique assets. In TradFi, proving ownership of a unique digital item (like a piece of digital art or a game item) is difficult because digital files are easily copied. NFTs solve this by creating a unique, uncopyable certificate of ownership on the blockchain. This has implications for digital identity, intellectual property, and supply chain tracking, expanding the scope of finance to include all forms of value transfer.

Conclusion

The comparison between Web3 and Traditional Finance highlights a shift from institution-based trust to code-based truth. TradFi offers familiarity, consumer protections, and stability, but comes with the costs of exclusion, inflation, and centralization. It relies on a "walled garden" approach where safety is provided by gatekeepers.

Web3 offers an open wilderness. It provides transparency, immutability, and true ownership, but requires users to take full responsibility for their security. It removes the gatekeepers, allowing for a more inclusive and efficient global economy. As the technology matures, the friction between these systems will likely decrease, with Web3 infrastructure potentially becoming the backend that powers the future of all finance.

The future of money is shifting from trusted intermediaries to verifiable code.