Digital currencies have transformed the financial landscape, but their inherent volatility often creates a barrier to entry for everyday transactions. Bitcoin and Ethereum serve as revolutionary assets, yet their price fluctuations make them difficult to use for paying rent or buying groceries. This specific challenge led to the creation and rapid adoption of stablecoins. These unique digital assets function as a bridge between the traditional fiat economy and the decentralized web.

Stablecoins offer the speed and security of blockchain technology without the wild value swings associated with standard cryptocurrencies. By pegging their market value to external assets like the US dollar or gold, they provide a reliable medium of exchange. This stability allows traders to hedge against market downturns without exiting the crypto ecosystem entirely. It also enables seamless cross-border payments that settle in minutes rather than days.

The importance of stablecoins extends far beyond simple trading utility. They have become the fundamental plumbing for the entire Decentralized Finance (DeFi) sector. From earning yield in liquidity pools to serving as collateral for loans, these tokens drive billions of dollars in daily economic activity. Understanding how they work, the risks they carry, and their impact on the broader market is essential for any modern participant in the digital economy.

The Fundamentals of Stablecoin Architecture

Defining the Asset Class

Stablecoins are a specific category of cryptocurrency designed to maintain a stable value relative to a target price. While Bitcoin serves as a store of value and medium of exchange with a floating price, stablecoins prioritize price consistency. They are not typically "coins" in the strictest technical sense but are usually "tokens" built on top of existing blockchains.

For instance, popular stablecoins often exist as ERC-20 tokens on the Ethereum network or SPL tokens on Solana. This distinction is important because it means they inherit the security and transaction speed of the host blockchain. They do not run on their own proprietary chains but rely on smart contracts to manage their supply and issuance. This architecture allows them to be easily integrated into various decentralized applications (dApps) and wallets.

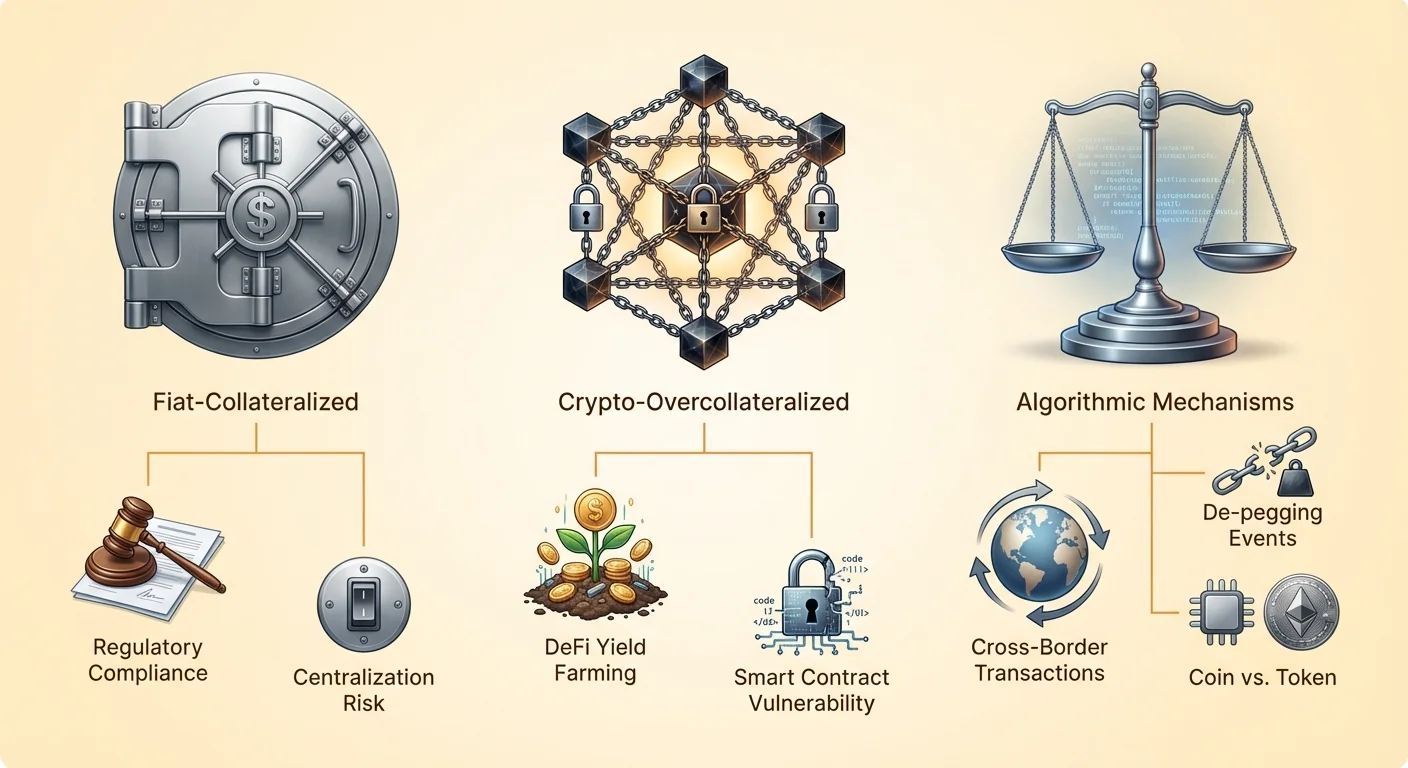

The Coin vs Token Distinction

To fully grasp stablecoins, one must understand the difference between a coin and a token. A coin, like Bitcoin or Litecoin, runs on its own independent blockchain. Its primary role is often to pay for network fees and secure the ledger. Tokens, conversely, are assets created on top of those networks.

Stablecoins fall firmly into the token category. They utilize the infrastructure of major chains like Ethereum or BNB Smart Chain to operate. This allows developers to focus on the mechanism of stability rather than building a new blockchain from scratch. It also means that sending a stablecoin usually requires a small amount of the native coin (like ETH) to pay for the transaction "gas" fees.

Core Use Cases

The primary utility of stablecoins is to provide a safe harbor during periods of market volatility. Traders often swap volatile assets into stablecoins to "lock in" profits without converting back to fiat currency, which can be slow and costly. Beyond trading, they are increasingly used for everyday payments and remittances.

In the DeFi ecosystem, stablecoins are indispensable. They serve as the base currency for most trading pairs on decentralized exchanges (DEXs). Users deposit them into liquidity pools to earn yield, or use them as collateral to borrow other assets. Their predictable value makes them ideal for financial contracts that require a steady unit of account over time.

Mechanisms of Stability

Fiat-Collateralized Models

The most common and widely understood method for maintaining a peg is fiat collateralization. In this model, a central issuer holds reserves of traditional currency, such as the US dollar, in a bank account. For every unit of the stablecoin issued on the blockchain, there is a corresponding unit of fiat currency held in reserve.

Tokens like USDC and USDT operate on this principle. Users trust that the issuer has the funds to back every token in circulation. When a user wants to redeem their tokens, the issuer destroys the digital token and sends the equivalent fiat currency to the user's bank account. This model is simple and capital efficient but relies heavily on trust in the central entity managing the reserves.

Crypto-Collateralized Systems

To remove the reliance on centralized banks, some stablecoins use other cryptocurrencies as collateral. Since the collateral itself is volatile (like ETH or BTC), these systems must be "over-collateralized." This means that to mint $100 worth of a stablecoin, a user might need to lock up $150 or $200 worth of cryptocurrency.

If the value of the collateral drops below a certain threshold, the smart contract automatically sells the collateral to pay back the debt and maintain the peg. This decentralized approach aligns with the ethos of crypto but requires complex management of collateral ratios. It enables the creation of stable assets without touching the traditional banking system.

Algorithmic and Hybrid Approaches

Algorithmic stablecoins attempt to maintain their peg through software logic rather than physical collateral. The protocol expands or contracts the supply of the token based on market demand. If the price goes above $1.00, the system mints more tokens to lower the price. If it drops below $1.00, it incentivizes users to burn tokens to reduce supply.

These models are highly experimental and carry significant risk, as seen in historical market events. However, innovation continues in this space. New projects, such as the Freedom Dollar (fUSD) on the Zano network, are exploring hybrid models that combine privacy features with stability mechanisms. These typically involve complex incentives to ensure the token tracks its target asset without centralized control.

Regulatory Risks and Compliance

The Security Classification Debate

As stablecoins have grown into a multi-billion dollar market, they have attracted intense scrutiny from regulators worldwide. The primary risk facing issuers is the potential classification of stablecoins as securities rather than currencies. If a stablecoin is deemed a security, it faces strict oversight regarding issuance, trading, and reporting.

This classification could fundamentally change how stablecoins are traded. Exchanges might be forced to delist tokens that do not comply with securities laws. This uncertainty creates a layer of risk for holders, as regulatory actions can lead to sudden liquidity crunches or limitations on redeeming the tokens for fiat currency.

Centralization and Censorship

Most major stablecoins are centralized. The companies behind them have the power to freeze addresses and blacklist funds at the request of law enforcement. While this compliance helps prevent illicit activity, it contradicts the censorship-resistant nature of cryptocurrencies like Bitcoin.

This "regulatory exposure" is a critical trade-off. Users gain the stability of the dollar but lose the absolute control over their funds found in decentralized assets. Regulators are increasingly demanding that issuers implement strict Know Your Customer (KYC) and Anti-Money Laundering (AML) protocols, pushing these assets closer to traditional banking products.

The 2025 Landscape

Looking forward, the regulatory environment is expected to become more defined. Governments are actively drafting frameworks to govern stablecoin issuers. This likely means that only highly regulated, transparent entities will be allowed to issue dollar-pegged tokens.

We may see a bifurcated market: fully compliant, bank-integrated stablecoins for institutional use, and decentralized, crypto-backed stablecoins for DeFi and privacy-focused applications. Projects like World Liberty Financial are entering the space, signaling that political and financial figures are taking a direct interest in shaping how these assets are governed and adopted.

The Role in Decentralized Finance (DeFi)

Fueling Liquidity Pools

Stablecoins are the lifeblood of decentralized exchanges (DEXs). In systems like the Verse DEX, liquidity pools allow users to trade between assets without an intermediary. Stablecoins are almost always one half of these trading pairs (e.g., ETH/USDC).

By providing stablecoins to these pools, users facilitate smoother trading for the entire market. Without stable pairs, traders would be forced to trade volatile assets against other volatile assets, making price discovery difficult. Stablecoins provide a common denominator that stabilizes the entire DeFi ecosystem.

Yield Farming and Lending

One of the most popular activities in DeFi is yield farming. Users lend their stablecoins to protocols or liquidity pools in exchange for interest or reward tokens. Because the principal asset is stable, the risk of "impermanent loss" is often lower compared to volatile pairings.

Lending platforms also rely heavily on stablecoins. Borrowers often want to take out loans in stable currency to pay real-world expenses, while using their Bitcoin or Ethereum as collateral. This allows them to access liquidity without selling their long-term investment holdings.

Cross-Chain Interoperability

Stablecoins are increasingly becoming the standard for moving value across different blockchains. Through bridges and wrapping protocols, a user can move USDC from Ethereum to Solana or Avalanche. This interoperability is crucial for a connected crypto economy.

However, this also introduces bridge risk. If the smart contracts governing the bridge are exploited, the stablecoins on the destination chain can lose their backing. Despite this, the demand for cross-chain stablecoin transfer continues to drive innovation in interoperability protocols.

Market Impact and Economic Utility

Remittances and Cross-Border Payments

Traditional international money transfers are slow and laden with fees. Stablecoins have emerged as a superior alternative for remittances. Networks like Stellar (XLM) and Tron (TRX) specifically target this use case, offering near-instant settlement at a fraction of the cost of a wire transfer.

Workers in foreign countries can receive stablecoins and exchange them for local currency locally, bypassing expensive banking intermediaries. This utility provides real-world economic freedom to millions of unbanked or underbanked individuals, fulfilling one of the original promises of cryptocurrency.

Inflation Hedge

In countries with hyperinflation, local fiat currencies lose value rapidly. Citizens in these regions often turn to stablecoins as a way to preserve their purchasing power. Unlike Bitcoin, which can also drop in value, a US dollar-pegged stablecoin offers the relative stability of the world's reserve currency.

This "dollarization" of local economies through crypto rails is a growing trend. It allows individuals to access the stability of the US dollar without needing a US bank account. This phenomenon highlights the global demand for stable, censorship-resistant stores of value.

Institutional Adoption

Institutions are beginning to use stablecoins for settlement and treasury management. The immediate finality of blockchain transactions appeals to corporate treasurers tired of the multi-day settlement times of the traditional banking system.

Projects involving major financial figures and traditional payment processors are validating the technology. As regulatory clarity improves, we can expect more corporations to hold stablecoins on their balance sheets or use them for supply chain payments.

Identifying and Managing Risks

While stablecoins offer safety from volatility, they introduce their own set of risks. The most prominent is "de-pegging." This occurs when a stablecoin loses its 1:1 value with its target asset. This can happen due to a loss of confidence in the reserves, a technical failure, or a liquidity crisis.

Smart contract risk is another major concern. Since stablecoins are programmable tokens, they are governed by code. Bugs or vulnerabilities in the smart contract can be exploited by hackers to mint infinite tokens or prevent users from redeeming them.

Counterparty risk is inherent in centralized stablecoins. You are trusting the issuer to keep the money safe and to honor redemptions. If the issuer goes bankrupt or is shut down by regulators, the tokens could become worthless.

Comparison of Stablecoin Types

| Feature | Fiat-Collateralized | Crypto-Collateralized |

|---|---|---|

| Backing | Cash & Equivalents | Cryptocurrencies |

| Centralization | High (Central Issuer) | Low (DAO/Smart Contract) |

| Capital Efficiency | High (1:1) | Low (Over-collateralized) |

Privacy and Advanced Features

The Need for Privacy

Most public blockchains are transparent, meaning anyone can view the transaction history of a stablecoin address. This lack of privacy acts as a deterrent for businesses that do not want to reveal their suppliers or payroll information to competitors.

This has led to the development of privacy-focused stablecoins and networks. Projects like Zano are pioneering "Confidential Assets," which allow for the issuance of tokens that hide transaction amounts and sender/receiver details.

Private Stablecoins

The Freedom Dollar (fUSD) is an example of this innovation. It combines the stability of a pegged asset with the privacy features of a secure blockchain. Unlike standard ERC-20 tokens, where every transfer is visible, privacy stablecoins ensure that financial data remains confidential.

This sector faces significant regulatory hurdles, as governments are wary of untraceable digital cash. However, for users prioritizing personal sovereignty and data protection, these assets represent the next frontier of stablecoin technology.

Storing and Securing Stablecoins

Custodial vs Self-Custodial Wallets

Choosing how to store stablecoins is a critical decision. Custodial wallets (like those on centralized exchanges) hold the keys on your behalf. This is convenient but introduces third-party risk. If the exchange fails, you may lose your funds.

Self-custodial wallets, such as the Bitcoin.com Wallet, give the user full control over their private keys. This protects users from exchange insolvencies but places the responsibility of security entirely on the individual.

Security Best Practices

When holding stablecoins in a self-custody wallet, backing up the recovery phrase is paramount. This phrase is the only way to recover funds if a device is lost or damaged. Users should never share this phrase with anyone.

For large amounts, using a hardware wallet or a multisig (shared) wallet adds an extra layer of security. These methods ensure that a single compromised device cannot lead to the loss of funds.

Conclusion

Stablecoins have evolved from a simple trading tool into a foundational pillar of the global crypto economy. They solve the critical issue of volatility, making blockchain technology usable for payments, savings, and complex financial contracts. By bridging the gap between traditional fiat currency and decentralized networks, they offer the best of both worlds: stability and efficiency.

However, this convenience comes with distinct risks. Users must navigate regulatory uncertainty, the potential for technical failures, and the centralization of major issuers. Whether using fiat-backed giants like USDC or exploring decentralized alternatives, understanding the underlying mechanism of the asset is vital.

As the market matures towards 2025 and beyond, we will likely see increased regulation and innovation working in parallel. The distinction between coins and tokens will remain technically relevant, but for the end user, the focus will shift to utility and safety. Stablecoins are not just a temporary parking spot for capital; they are building a new, more efficient global financial infrastructure.

Stablecoins provide the essential stability needed to unlock the full potential of the decentralized digital economy.