Decentralized finance represents a significant shift in how individuals interact with economic systems. Rather than relying on centralized intermediaries like banks or brokerages, this new ecosystem utilizes technology to offer financial products directly to users. At the center of this transformation is the concept of value stability in assets. While cryptocurrencies are known for price volatility, the financial applications built on blockchain networks often require steady assets to function effectively.

These stable assets serve as the primary medium of exchange and store of value within the digital economy. They allow users to lock in profits, facilitate seamless payments, and engage in complex financial strategies without immediate exposure to market fluctuations. By leveraging the transparency and automation of blockchain networks, developers have created systems where monetary stability is maintained through code rather than central bank policy. This technological foundation enables a global, permissionless economy accessible to anyone with an internet connection.

The Technological Foundation of Digital Stability

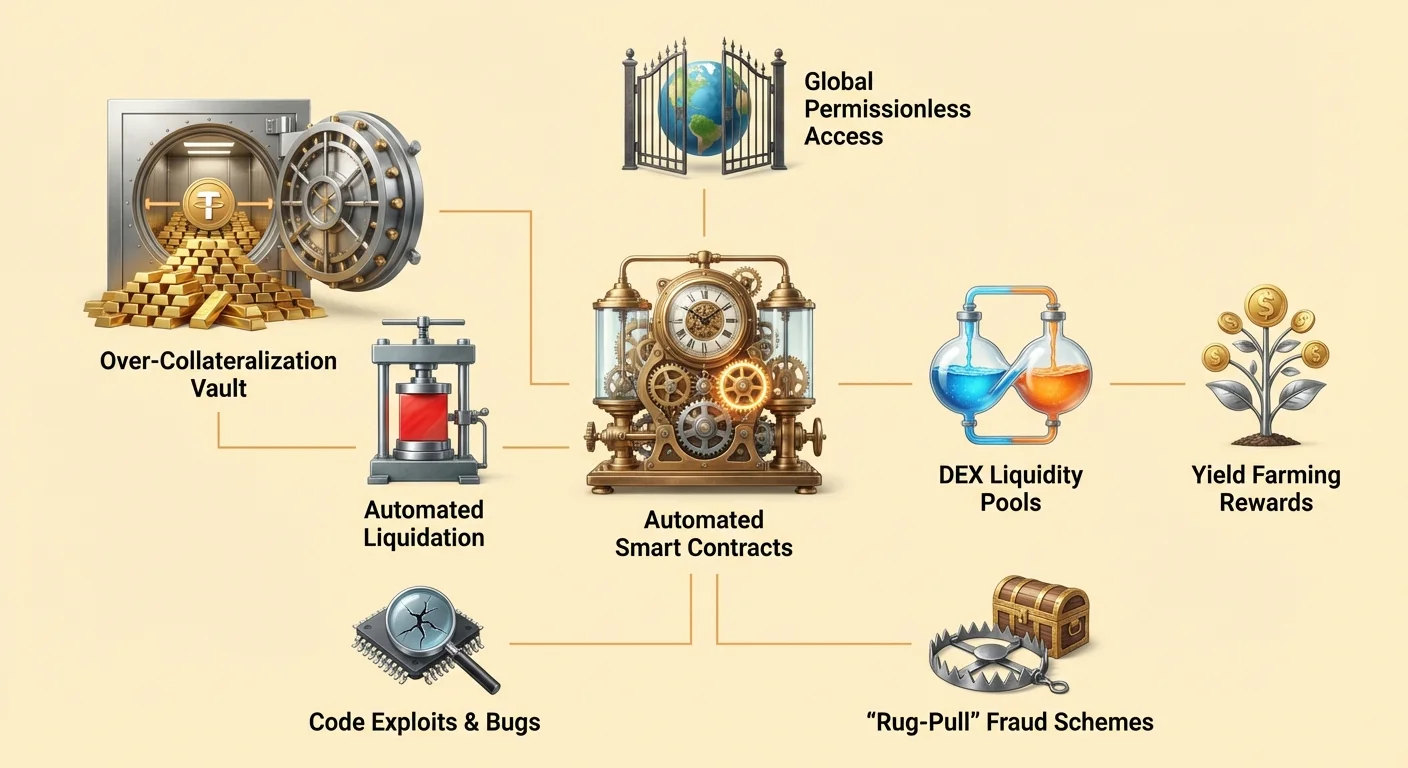

The infrastructure supporting stable monetary assets in the decentralized ecosystem relies heavily on smart contracts. These are computer programs stored on a blockchain that execute automatically when specific conditions are met. Unlike traditional software that runs on private servers, these contracts operate on public networks that are open for verification by any participant.

Automating Monetary Policy

Smart contracts act as self-executing agreements that define the rules of money within the system. In the context of decentralized finance, or DeFi, these contracts replace the manual processes typically handled by bank employees or lawyers. The code determines exactly how assets are issued, redeemed, and transferred based on pre-defined logic.

For example, a smart contract can be programmed to issue a specific amount of digital currency only when a user deposits a corresponding amount of collateral. This automation ensures that the issuance of money is not subject to human error or discretionary manipulation. The rules are immutable once deployed, providing a predictable framework for all market participants. This deterministic nature is crucial for maintaining trust in a system where there is no central authority to mediate disputes.

Trustless Execution

The concept of "trustless" systems is fundamental to how these digital assets operate. In this context, trustless does not mean the system is untrustworthy. Instead, it means that users do not need to place their faith in a third party to ensure the system works correctly. The validity of the network and the execution of contracts can be verified by anyone.

When a user interacts with a stability-focused protocol, they are interacting directly with the blockchain. There is no need to trust a bank manager to approve a loan or a clearinghouse to settle a trade. The network itself validates the transaction. This eliminates the counter-party risk associated with centralized service providers, who might default, freeze funds, or suffer from operational failures. The security and transparency provided by this model form the bedrock upon which complex financial applications are built.

Mechanics of Collateralized Lending

One of the most prominent methods for creating stability in DeFi is through smart contract-based lending. This process allows users to generate liquidity without selling their underlying crypto assets. It mirrors traditional secured loans but operates entirely through automated protocols.

Over-Collateralization Strategies

To secure a loan in the decentralized ecosystem, borrowers must provide collateral. Because the underlying assets, such as Ethereum, can be volatile, these protocols typically require over-collateralization. This means the value of the deposit must exceed the value of the loan by a specific margin.

Consider a scenario where a user wants to borrow US dollars against their Ethereum holdings. They might send 1 ETH to a smart contract. If the protocol requires a 2:1 collateralization ratio, the user can borrow up to 0.5 ETH worth of dollars. The smart contract holds the original ETH as security. This ensures that even if the market fluctuates, the loan remains backed by sufficient value. This mechanism allows the creation of stable value (the loan) backed by volatile assets, all managed without a credit check or human intervention.

Managing Volatility and Liquidation

The stability of the system relies on strict enforcement of these ratios. If the value of the collateral drops significantly, the system must act to protect the solvency of the protocol. Smart contracts are programmed to trigger liquidations automatically when collateral values breach a certain threshold.

If the price of the collateral falls below the required ratio, the borrower has two options. They can pay back the loan plus interest, or they can add more collateral to the smart contract to restore the safe level. If the borrower takes no action and the value continues to drop, the smart contract will liquidate the collateral. This usually involves selling the ETH to repay the debt. This harsh but necessary mechanism ensures that the system remains solvent and that the stable assets issued by the protocol retain their backing, regardless of market conditions.

Facilitating Decentralized Exchange

Stable assets play a critical role in decentralized exchanges (DEXs). These platforms allow users to trade digital assets directly with one another without handing custody over to a centralized service. For these markets to function efficiently, they require deep liquidity and reliable quote currencies.

The Role of Liquidity Pools

Decentralized exchanges operate differently from traditional order book markets. They rely on liquidity pools, which are smart contracts holding pairs of assets. Liquidity providers deposit their tokens into these pools to facilitate trading for others. In return, they earn a percentage of the trading fees generated by the protocol.

Stablecoins are essential to this process because they are often half of a trading pair. Traders frequently swap volatile assets for stable ones to hedge against market downturns. Without a reliable stable asset in these pools, traders would have to swap one volatile asset for another, making it difficult to realize gains or protect capital. The incentive structure for liquidity providers creates "crowd-sourced" market depth, driving efficiency and reducing slippage for traders.

Enhancing Market Efficiency

The presence of stable assets in DEXs improves the overall user experience. It allows for easier price discovery and provides a safe harbor during periods of high volatility. Because these exchanges are permissionless, anyone can participate in market making.

The automation of these exchanges also removes the need for a middleman to hold funds. The smart contracts move assets transparently according to the code's logic. This eliminates the risk of a centralized exchange freezing withdrawals or getting hacked. Users retain control of their funds right up until the moment the trade executes. This alignment of incentives—where providers earn fees and traders get efficient execution—is powered by the constant availability of stable pairs within the ecosystem.

Yield Generation and Financial Inclusion

The combination of stable assets and open lending protocols has democratized access to yield-generating strategies. In traditional finance, high-yield opportunities are often restricted to institutional investors or high-net-worth individuals. DeFi changes this dynamic by allowing anyone with a wallet address to participate.

Earning Interest on Deposits

Users can deposit their stable digital assets into lending protocols to earn interest. This is analogous to a savings account at a bank, but the mechanics are different. In DeFi, the capital is pooled with funds from other providers and lent out to borrowers. The interest paid by borrowers is distributed automatically to the lenders.

Because the system cuts out the overhead of traditional banks—such as branches, staff, and legal departments—the yields offered in DeFi can be higher than those found in traditional finance. Smart contracts automate the distribution of profits, ensuring that lenders receive their share according to the precise terms of the protocol. This efficiency potentially leads to a more equitable distribution of profit among participants.

Permissionless Global Access

One of the most powerful aspects of this ecosystem is its permissionless nature. Traditional financial infrastructure is often limited by geography, documentation requirements, and banking regulations. This excludes billions of people from accessing basic financial services.

In the decentralized economy, there are no gatekeepers. Anyone with an internet connection and a digital wallet can interact with these protocols. It does not matter where the user lives or what their credit history looks like. A user in a country with a collapsing local currency can access dollar-pegged stable assets through a DeFi protocol, effectively preserving their purchasing power. This global accessibility allows individuals to become their own banks, lending out money and earning interest regardless of their physical location.

| Feature | Traditional Finance | Decentralized Finance |

|---|---|---|

| Access | Permissioned (ID required) | Permissionless (Open to all) |

| Custody | Third-party (Bank) | Self-custody (User) |

| Transparency | Opaque | Publicly verifiable |

Navigating Risks in the Ecosystem

While the potential of decentralized finance is vast, it is not without risks. The very mechanisms that provide autonomy and efficiency also introduce unique challenges that users must navigate. Understanding these risks is essential for anyone participating in the space.

Smart Contract Vulnerabilities

The reliance on code means that software bugs are a significant threat. Smart contracts are deterministic, meaning they do exactly what they are programmed to do. If there is an error or a loophole in the code, it can be exploited. Hackers search for these vulnerabilities to drain funds from protocols.

Even though many projects are open source, which allows the community to audit the code, errors can still persist. A "poorly designed" application might contain weaknesses that result in the loss of user funds. Unlike a bank, where fraudulent transactions might be reversed, blockchain transactions are generally immutable. Once funds are stolen through a smart contract exploit, they are often unrecoverable. The phrase "code is law" cuts both ways; it ensures neutral execution but also enforces the consequences of programming mistakes.

The Threat of Malicious Actors

Beyond accidental bugs, there is the risk of deliberate fraud. The anonymity and lack of regulation in the space can attract malicious actors. Some developers may deploy "malicious dApps" designed specifically to steal user deposits.

A common tactic is the "rug-pull." In this scenario, insiders might create a project, attract capital by promising high yields, and then abandon the project, taking the funds with them. They might hold a majority of the project's tokens and sell them all at once, crashing the price. Another risk is phishing, where attackers create websites that look identical to legitimate services. If a user connects their wallet to a phishing site, they may inadvertently grant permission for the attacker to drain their assets.

| Risk Type | Description | Consequence |

|---|---|---|

| Bug/Exploit | Flaw in code logic | Loss of funds to hacker |

| Rug-pull | Malicious insider action | Token value collapse |

| Phishing | Fake website interface | Theft of wallet assets |

Governance and Community Control

Many protocols that issue or utilize stable assets are governed by decentralized organizations. This introduces a layer of community control that is absent in traditional finance. Governance tokens are often used to facilitate this process, giving stakeholders a voice in the future of the protocol.

Voting and Protocol Upgrades

Governance tokens grant holders the right to vote on proposals. these proposals can range from adjusting interest rate models and collateralization ratios to allocating treasury funds. This system aims to align the interests of the users with the long-term health of the protocol.

For instance, if a lending protocol needs to add a new type of collateral, the community would vote on the parameters. This ensures that changes are not made unilaterally by a small group of insiders. It fosters a sense of ownership and responsibility among the participants. Active community members are incentivized to contribute to the project's growth, as the success of the protocol often correlates with the value of the governance token.

Distribution and Airdrops

Projects often distribute these governance tokens through mechanisms like "airdrops." An airdrop involves sending free tokens to users who meet specific criteria, such as having used the platform or provided liquidity. This strategy serves multiple purposes: it rewards early adopters, decentralizes the ownership of the protocol, and encourages future engagement.

By distributing tokens to a wide base of active users, projects can bootstrap a community of motivated stakeholders. This is often seen as a way to "market" the project while simultaneously building a decentralized governance structure. However, users must be wary of speculative behavior surrounding these events. The ultimate goal is to create a sustainable ecosystem where the community actively manages the parameters that maintain the stability and security of the monetary assets.

The User Interface of Decentralized Money

For the average person, interacting with these complex technical systems requires a bridge. This is where Decentralized Applications, or dApps, come into play. A dApp provides a user-friendly interface that connects a person's digital wallet to the underlying smart contracts.

Connecting to the Blockchain

To use a stablecoin or lend assets, a user connects their wallet to a dApp. The wallet holds the user's private keys and signs transactions. The dApp serves as the front-end, displaying balances, interest rates, and transaction options. It translates the complex logic of the blockchain into buttons and forms that are familiar to web users.

This connection is "permissionless," meaning the dApp does not store user data or require a login account in the traditional sense. The user's wallet address acts as their identity. This setup ensures that users maintain full control over their assets at all times. They do not need to deposit funds into the dApp's bank account; instead, they authorize specific interactions with the smart contract directly from their own custody.

Verifiability and Transparency

One of the key advantages of using dApps is transparency. Because the backend runs on a public blockchain, the history of the application's operations is immutable and visible to everyone. Users can verify that a game is "provably fair" or that a lending protocol actually holds the collateral it claims to.

This contrasts sharply with traditional apps where the backend logic is hidden on private servers. In the decentralized world, users can inspect the contract address and see the code (if they have the technical skill) or rely on community audits. This transparency builds a different kind of trust—one based on verification rather than reputation. It forces protocols to operate honestly, as any deviation from the code would be immediately visible on the public ledger.

Conclusion

The emergence of stablecoins and the decentralized finance ecosystem represents a fundamental reimagining of monetary infrastructure. By utilizing smart contracts, these systems automate the complex processes of lending, borrowing, and exchange. They replace intermediaries with transparent code, allowing for a financial system that is open to anyone with a digital wallet. The ability to create stable value through over-collateralization provides the necessary foundation for a reliable digital economy, enabling users to hedge against volatility while accessing global financial services.

However, this innovation is not without its perils. The reliance on software introduces risks of bugs, exploits, and malicious behavior that are less prevalent in traditional banking. Users must navigate this landscape with caution, verifying sources and understanding the mechanics of the protocols they use. Despite these challenges, the trajectory of DeFi suggests a future where financial access is more equitable and efficient. As the technology matures and open-source communities continue to harden the security of these protocols, the role of stable, decentralized money is likely to grow, offering a robust alternative to legacy financial systems.

True financial ownership empowers you to be your own bank, but it requires vigilance, education, and careful risk management.