The cryptocurrency market has evolved significantly from its early days of peer-to-peer transfers and experimental forums. Today, investors face a sophisticated landscape of entry points into the digital asset economy. Two primary avenues have emerged as the dominant methods for acquiring and trading digital currencies.

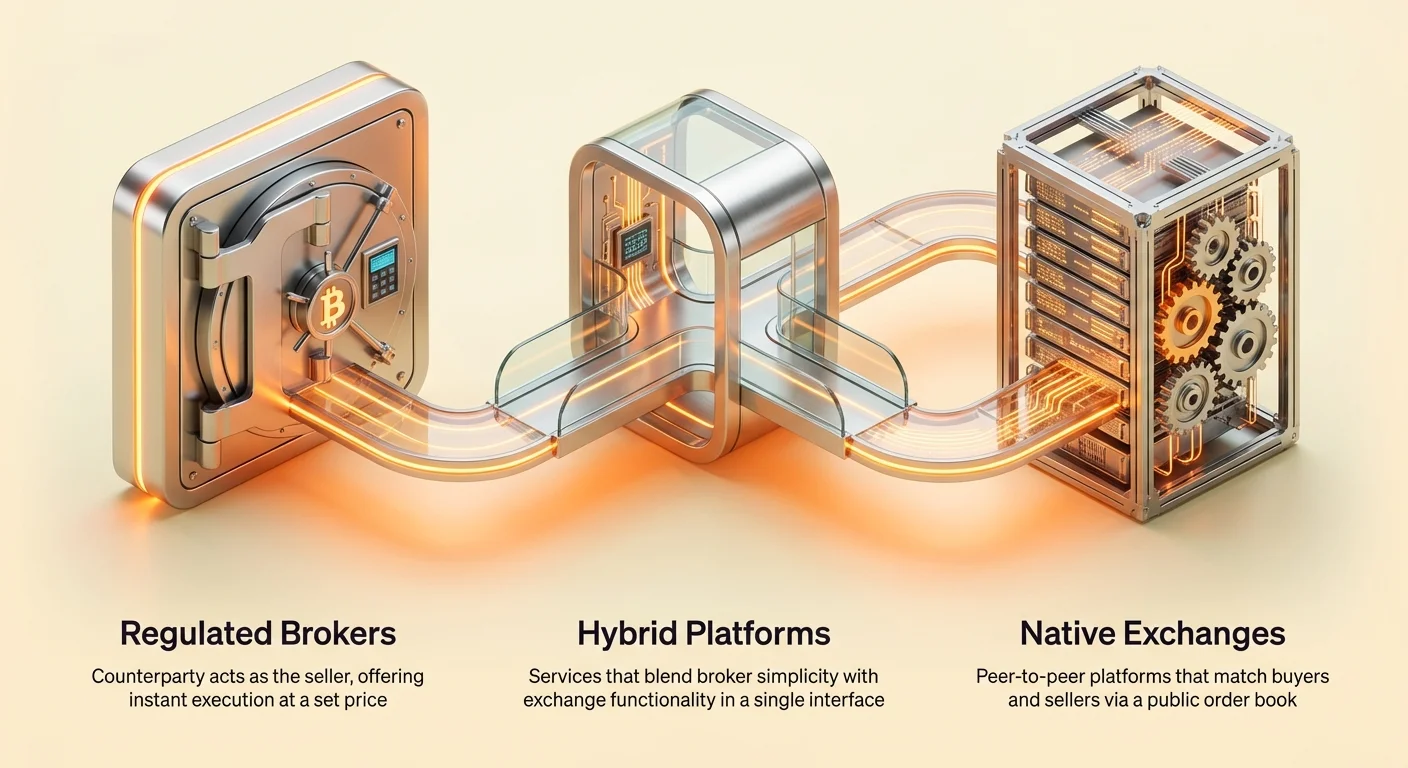

On one side stand native cryptocurrency exchanges. These platforms were built specifically for the blockchain era. They focus on direct market interaction and order book mechanics. On the other side are traditional brokers and regulated intermediaries. These entities often adapt traditional finance structures to the crypto world.

Understanding the distinction between these two models is vital. It impacts fees, security, asset ownership, and the overall trading experience. Newcomers often struggle to identify which model suits their investment goals. The choice depends heavily on whether one values convenience over control or low costs over simplicity.

This guide examines the operational differences, benefits, and risks associated with both native exchanges and regulated brokers. It explores how trade execution varies between them and what that means for your bottom line. By analyzing liquidity, custody, and compliance, investors can make informed decisions about where to park their capital.

Defining the Market Participants

The terminology in the crypto space can be fluid. However, distinct operational models separate brokers from exchanges. Recognizing these differences helps traders understand what happens behind the scenes when they click "buy."

Native Cryptocurrency Exchanges

Native exchanges are platforms designed to facilitate trading directly between users. In this model, the exchange acts as a matching engine. It connects buyers with sellers. When you place an order to buy Bitcoin, the exchange looks for a seller willing to part with Bitcoin at that price.

These platforms operate using an electronic order book. This is a public ledger of all buy and sell orders currently open in the market. The price of an asset on a native exchange is determined by supply and demand dynamics in real-time. The exchange itself does not set the price.

Users on native exchanges typically pay a fee for this service. This is known as a trading fee. The exchange takes a small percentage of the transaction value for facilitating the match. This model rewards liquidity and active participation.

Brokerage Platforms

Cryptocurrency brokers operate differently. Instead of matching you with another user, the broker acts as the counterparty to your trade. When you buy crypto from a broker, you are buying it directly from the broker's inventory.

In this scenario, the broker sets the price. They often source liquidity from multiple exchanges or large liquidity providers. They then offer a set price to the customer. This price typically includes a markup.

This model simplifies the process for the user. There is no need to worry about order books or market depth. You see a price, and you accept it. However, this convenience often comes with embedded costs that are less transparent than exchange fees.

Hybrid Models

The line between brokers and exchanges is becoming increasingly blurred. Many major platforms now offer both services. They provide a simple "convert" interface that functions like a broker. This is aimed at beginners who want instant execution.

Simultaneously, these platforms offer an "advanced trade" interface. This section provides access to the order book and functions as a traditional exchange. Users can choose which interface to use based on their expertise and needs.

Understanding which mode you are using is crucial. The fee structures and execution prices can differ significantly within the same app. Users must be aware of which service they are engaging with to manage costs effectively.

The Mechanics of Trade Execution

The way a trade is executed affects the final price you pay. It also determines the speed and reliability of the transaction. Brokers and exchanges handle this process in fundamentally different ways.

On a native exchange, execution depends on market liquidity. If you place a large market order, you might experience slippage. This happens when there are not enough sell orders at the current price to fill your order. The engine moves up the order book to higher prices to complete the trade.

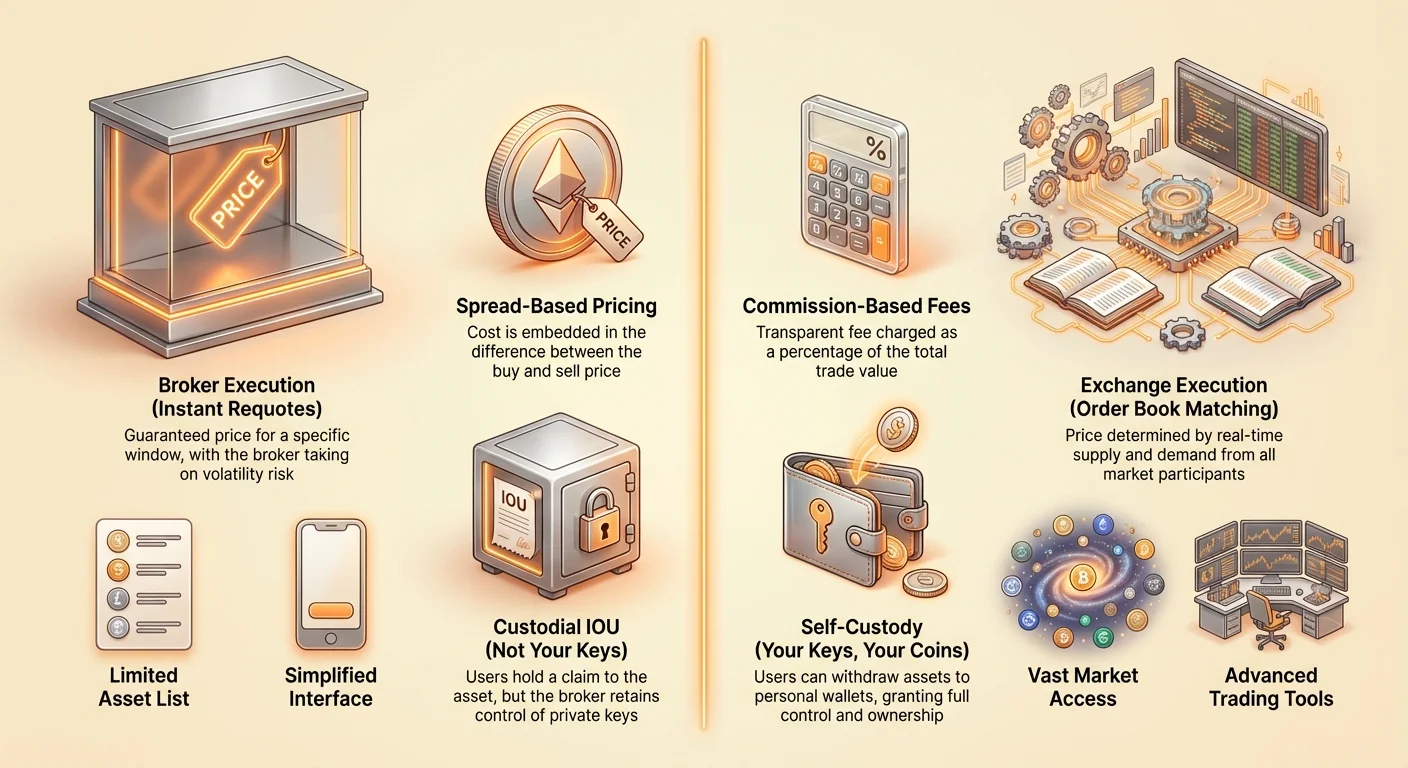

Brokers mitigate this complexity. They quote a guaranteed price for a specific window of time. This is known as a "requote" or instant execution model. The broker takes on the risk of price volatility during that window.

To compensate for this risk, brokers widen the spread. The spread is the difference between the buy and sell price. While you might get instant execution, you are likely paying a premium for that certainty.

Fee Structures and Cost Analysis

Cost is a primary consideration for any trader. The fee structures in the crypto market vary widely. They can be categorized generally into commission-based models and spread-based models.

Commission Models vs. Spreads

Native exchanges typically use a commission model. They charge a percentage of the total trade value. This fee is often split into "maker" and "taker" fees. Makers are traders who provide liquidity by placing limit orders that do not fill immediately. Takers are traders who remove liquidity by hitting existing orders.

Makers usually pay lower fees than takers. This incentivizes users to provide liquidity to the order book. Commissions on top exchanges can range from 0.1% to 0.6%. High-volume traders often receive significant discounts.

Brokers often advertise "zero fee" trading. This can be misleading. Instead of a transparent commission, they charge a spread. If the market price of Ethereum is $2,000, a broker might sell it to you for $2,050 and buy it back for $1,950.

The difference represents their profit. While there is no line item for a "transaction fee," the cost is embedded in the asset price. In many cases, the spread can exceed the cost of a standard exchange commission.

Hidden Costs and Non-Trading Fees

Beyond the trade itself, other costs accumulate. Withdrawal fees are common on native exchanges. These cover the network costs of sending crypto over the blockchain. Some exchanges add a surcharge on top of the network fee.

Brokers may not charge withdrawal fees if they do not allow crypto withdrawals. However, they might charge inactivity fees or overnight financing fees for leveraged positions. It is essential to read the fine print regarding account maintenance costs.

Deposit fees also vary. Funding an account via bank transfer is often free or cheap. Using a credit card or a payment processor like PayPal usually incurs a high percentage fee. This applies to both brokers and exchanges.

Custody and Asset Ownership

One of the most philosophical and practical differences between brokers and exchanges lies in the concept of custody. In the crypto ethos, "not your keys, not your coins" is a prevailing mantra.

Self-Custody Capability

Native exchanges generally allow users to withdraw their assets. You can buy Bitcoin on an exchange and send it to a personal hardware wallet. This gives you total control over your private keys. You become the sole custodian of your wealth.

This capability is essential for using crypto in the broader ecosystem. If you want to interact with decentralized finance (DeFi) protocols or pay for goods, you need to withdraw your funds. Exchanges facilitate this utility.

The "IOU" Model

Many traditional brokers operate on a closed-loop system. You can buy and sell exposure to the price of a cryptocurrency, but you cannot withdraw the actual asset. In this model, you hold an IOU (I Owe You) from the broker.

The broker holds the underlying asset (or a derivative contract) on your behalf. You profit if the price goes up, but you cannot use the crypto. You cannot send it to a friend or use it for payments.

This model is sufficient for pure speculation. If your only goal is to profit from price movements in fiat currency terms, a broker is adequate. However, it restricts the actual utility of the digital asset.

Regulated Custodians

Some brokers have started to evolve. They now partner with regulated custodians to hold the underlying assets. This adds a layer of security. The assets are segregated from the broker's operational funds.

Despite this, the user still relies on the broker for access. If the broker halts trading or faces technical issues, the user cannot move their funds. This centralization of control is a significant risk factor for those who value financial sovereignty.

Regulatory Compliance and Security

Safety is paramount when dealing with digital assets. Both exchanges and brokers have made strides in security, but they operate under different regulatory frameworks.

The KYC and AML Landscape

Regulated intermediaries must adhere to strict Know Your Customer (KYC) and Anti-Money Laundering (AML) laws. This means users must verify their identity. They must upload government IDs and sometimes proof of address.

Native exchanges, particularly centralized ones, have largely adopted these standards. It is rare to find a major exchange that allows significant trading without verification. This compliance helps prevent illicit activity.

However, some "anonymous" or decentralized exchanges still exist. These platforms prioritize privacy. They allow trading without ID verification. While this appeals to privacy advocates, it carries higher regulatory risk.

Insurance and Protections

Traditional brokers often carry government-backed insurance for fiat deposits. In the United States, for example, cash held in a brokerage account might be insured by the SIPC or FDIC up to a certain limit.

It is crucial to note that this insurance rarely extends to cryptocurrency holdings. Crypto assets are generally not considered legal tender or covered securities under these protection schemes.

Native exchanges rely on private insurance policies. Some hold a portion of their assets in cold storage (offline wallets) and insure that amount against theft. Others maintain an emergency fund to reimburse users in the event of a hack.

| Feature | Regulated Broker | Native Exchange |

|---|---|---|

| Asset Ownership | Often exposure/IOU | Actual Crypto/Withdrawable |

| Insurance | Fiat often insured | Private/Self-insured |

| Fee Structure | Spread-based | Commission-based |

Asset Variety and Market Access

The breadth of the market available to a trader differs significantly between platforms. The crypto market consists of thousands of tokens, but access to them is not uniform.

Listing Standards

Brokers tend to be conservative. They usually list only the largest and most established cryptocurrencies. You will find Bitcoin, Ethereum, and perhaps a dozen other "blue chip" assets. This curation protects beginners from highly volatile or scam tokens.

Native exchanges often have more aggressive listing policies. They may offer hundreds or even thousands of different trading pairs. This includes new projects, small-cap tokens, and niche sector assets.

For traders looking to find the "next big thing," native exchanges are the only viable option. Brokers generally wait until an asset has significant market cap and regulatory clarity before listing it.

Trading Pairs

Native exchanges offer crypto-to-crypto trading pairs. You can trade Ethereum directly for Solana or Bitcoin for Litecoin. This eliminates the need to go back to fiat currency between trades.

Brokers typically value everything in fiat currency (USD, EUR, etc.). To switch from one crypto to another, you must sell to cash and then buy the new asset. This triggers two taxable events and two spread costs.

Crypto-to-crypto pairs are more efficient for active traders. They allow for more complex portfolio management strategies without constantly moving in and out of government currencies.

User Interface and Experience

The complexity of cryptocurrency trading can be intimidating. Platforms design their interfaces to target specific demographics. This design philosophy creates distinct user experiences.

Simplicity for Beginners

Brokers prioritize simplicity. Their apps often resemble standard banking or stock trading apps. The buy button is prominent. Charts are simplified line graphs. Technical jargon is minimized.

This approach lowers the barrier to entry. A user can buy $50 of Bitcoin in seconds without understanding what a limit order is. It removes the "analysis paralysis" that can occur when looking at a complex trading screen.

However, this simplicity hides critical information. Users may not see the order book or recent trade history. They are trading somewhat blindly, relying on the broker's price feed.

Depth for Advanced Traders

Native exchanges offer "Pro" or "Advanced" interfaces. These screens are dense with data. They display candlestick charts, depth charts, real-time order books, and trade history.

They also offer advanced order types. Stop-loss orders protect against downside risk. Limit orders allow buying at a specific price. Trailing stops help lock in profits.

While the learning curve is steeper, these tools are essential for risk management. They give the trader granular control over their entry and exit points. Brokers rarely offer this level of precision.

Derivatives and Leverage

For sophisticated investors, spot trading (buying the actual asset) is just one part of the equation. Derivatives allow traders to speculate on price without owning the asset or to hedge their portfolios.

Futures and Perpetuals

Native exchanges dominate the market for crypto futures. Perpetual futures are a specific type of contract that has no expiry date. They allow traders to bet on the price rising (long) or falling (short).

These platforms often offer high leverage. Traders can control a position worth ten times their collateral or more. This amplifies both potential profits and losses. It is a high-risk environment suited for experienced participants.

Contract for Differences (CFDs)

Brokers, especially in Europe and Asia, frequently offer CFDs. These are contracts between the provider and the client. The client gains or loses the difference between the entry and exit price.

CFDs are similar to futures but are distinct instruments. They are often subject to different tax treatments and regulations. CFDs do not involve any blockchain interaction. They are purely synthetic financial products.

Using leverage on either platform requires caution. Liquidation mechanisms differ. Exchanges may automatically sell your position if the price moves against you. Brokers may issue margin calls, requiring you to deposit more funds immediately.

Privacy and Anonymity

The original vision of cryptocurrency emphasized privacy. However, the bridge between fiat currency and crypto has become highly surveilled. The level of privacy available depends on the platform type.

The Decline of Anonymity

Regulated brokers offer zero anonymity. They are fully integrated into the traditional banking system. Every transaction is recorded and tied to your social security or tax identification number. Reporting to tax authorities is often automatic.

Native centralized exchanges have followed suit. Due to global pressure, they enforce strict identity verification. Creating an account without an ID is becoming increasingly difficult on major platforms.

Niche Privacy Options

Some smaller exchanges still offer limited trading without full verification. These are often "crypto-to-crypto" only. They do not touch fiat currency, which allows them to bypass some banking regulations.

However, these platforms often struggle with liquidity. They may also face sudden shutdowns or domain seizures. For the average investor, the risk of using an unregulated, anonymous exchange often outweighs the privacy benefits.

Funding Methods and Accessibility

Moving money into the crypto ecosystem can be a friction point. Platforms vary in which funding rails they support.

Fiat On-Ramps

Brokers excel at fiat integration. Because they are often part of banking apps or stock brokerages, funding is seamless. Transfers from a linked bank account are instant.

Native exchanges have improved in this area. Many have partnered with payment processors to accept bank transfers and debit cards. However, banks sometimes flag or block transfers to known crypto exchanges due to perceived risk.

Alternative Payment Methods

Some platforms accept PayPal, Apple Pay, or Google Pay. These methods are convenient but often expensive. The payment processors charge high fees for the "chargeback risk" associated with crypto.

Brokers are more likely to support these consumer-friendly payment methods natively. Exchanges often use third-party integrators (like Simplex or Banxa) to process these payments, which adds another layer of fees.

Geographic Restrictions and Global Access

Crypto is global, but regulations are local. The availability of exchanges and brokers depends heavily on where you live.

The US Regulatory Environment

The United States has a fragmented regulatory landscape. Some states, like New York, have very strict rules (the BitLicense). Many global exchanges do not accept US customers because they do not want to comply with these regulations.

Brokers like Robinhood or PayPal are often the easiest option for US residents. They are fully licensed in all states. US-based exchanges like Coinbase or Kraken are also compliant but may restrict certain assets or features (like staking) based on state laws.

Global Availability

Outside the US, the options expand. International exchanges often offer more features, higher leverage, and a wider variety of assets. However, they may not offer accounts denominated in local currencies for smaller nations.

Investors must verify that a platform is legally allowed to operate in their country. Using a VPN to access a restricted exchange is risky. The exchange can freeze funds if they detect the deception.

Customer Support and Reliability

When money is on the line, support matters. The history of crypto is littered with stories of platforms going offline during periods of high volatility.

Support Channels

Brokers generally provide robust customer support. They often have phone lines and live chat with human agents. Their infrastructure is built on traditional finance standards, which prioritize client retention.

Native exchanges have historically struggled with support. During bull runs, ticket response times can stretch to weeks. Many rely on automated bots or FAQs. However, top-tier exchanges have invested heavily in improving this, now offering 24/7 live chat.

System Uptime

Both brokers and exchanges face outages. However, native exchanges are often targets of massive DDoS attacks. They also handle massive throughput during market crashes.

Brokers may halt trading artificially. If volatility is too high, they may "close the window" on requotes to protect themselves from losses. This can prevent users from buying the dip or selling the top.

The Convergence of Services

The industry is trending toward a middle ground. Native exchanges are obtaining banking licenses. Brokers are building wallet infrastructure.

Super-apps are emerging. These platforms combine the utility of a wallet, the depth of an exchange, and the simplicity of a broker. They offer savings accounts, loans, and debit cards backed by crypto.

This convergence benefits the consumer. It drives competition on fees and features. It also forces legacy platforms to upgrade their technology to match the speed of crypto-native companies.

Conclusion

Choosing between a regulated broker and a native exchange requires an honest assessment of your needs. Brokers offer a familiar, safe, and convenient entry point. They handle the security risks and simplify the tax reporting. For a passive investor looking to hold a small amount of Bitcoin, this is often the path of least resistance.

However, native exchanges unlock the full potential of the asset class. They provide ownership of keys, access to a vast array of projects, and the tools necessary for active trading. They demand more responsibility from the user but offer greater financial sovereignty in return.

The best platform is the one that balances your desire for control with your tolerance for technical complexity.