Bitcoin emerged in 2009 following the release of a whitepaper by the pseudonymous Satoshi Nakamoto. This invention introduced a decentralized digital currency that operates without the oversight of governments or financial institutions. In the years since its inception, the asset has sparked an intense debate regarding its fundamental nature and classification within the broader financial landscape. Investors, economists, and technologists continue to argue whether it represents a modern form of digital gold or a speculative risk asset.

The core of this debate centers on the asset's utility and price behavior. On one side, proponents argue that its fixed supply and decentralized structure make it an ideal store of value, similar to precious metals but adapted for the digital age. They view it as a hedge against monetary inflation and a tool for preserving purchasing power over long time horizons. This perspective focuses on the structural similarities between the digital asset and historical monies like gold.

Conversely, skeptics and market analysts often classify it as a risk asset. They point to its historical price volatility and its tendency to correlate with speculative technology stocks during periods of economic uncertainty. From this viewpoint, the asset behaves more like a high-growth tech investment than a stable safe haven. Understanding this duality requires a deep dive into the mechanical properties, economic incentives, and market dynamics that drive the network.

Defining a Store of Value in the Digital Age

To determine whether Bitcoin qualifies as a store of value, one must first understand what that term implies. Broadly speaking, a store of value is any object or asset that retains its purchasing power into the future and can be readily exchanged. The primary requirement is that the asset should be worth the same or more over time relative to goods and services. It acts as a mechanism for transferring wealth from the present to the future without significant loss.

Essential Characteristics of Value Preservation

For an asset to function effectively as a store of value, it must possess specific attributes. It needs a reasonably long lifespan; perishable items like food cannot serve this purpose. It requires liquidity, which is a measure of how easily the asset can be exchanged for other things. If an asset cannot be sold or traded without extreme difficulty or delay, its utility as a value store diminishes significantly. Real estate, for instance, is a strong store of value but suffers from low liquidity compared to other assets.

Scarcity is perhaps the most critical constraint. An asset that is easily produced or abundant often loses value as supply outstrips demand. Air is vital for survival, yet its abundance makes it worthless as a monetary store. Historically, precious metals like gold and silver fulfilled this role because they are rare relative to other natural minerals. They require significant effort and resources to extract, refining their status as a verifiable store of wealth.

The Challenge of Digital Durability

In the physical world, durability is straightforward. Gold does not rust or decay. In the digital realm, durability takes on a different meaning. A digital store of value must be resistant to data loss, hacking, and systemic failure. Bitcoin relies on a globally distributed network of independently operated computers, known as nodes, to track ownership. This decentralized architecture ensures that the ledger remains intact even if significant portions of the network go offline.

The durability of this digital asset is tied to the internet itself. Just as the internet is resilient because of its distributed nature, the Bitcoin network maintains a permanent, unalterable record of transactions. This digital durability effectively mimics the physical durability of precious metals, ensuring that the units of account cannot be destroyed or lost to history as long as the network persists.

The Case for Digital Gold

The "digital gold" narrative is the strongest argument for Bitcoin’s status as a store of value. This comparison is not merely symbolic; it is rooted in shared functional characteristics. Both assets possess rarity, durability, and divisibility. However, proponents argue that the digital version improves upon the monetary properties of its physical counterpart in several key ways, particularly regarding portability and verification.

Portability and Verification

Gold is heavy, expensive to secure, and difficult to transport in large quantities. Moving millions of dollars in physical gold across international borders requires logistics, security teams, and immense cost. In contrast, Bitcoin is highly portable. Any amount of value, from a few cents to billions of dollars, can be transmitted anywhere in the world in minutes. The user needs only access to their private keys or a wallet application to move immense wealth.

Verification is another area where the digital asset excels. Verifying the purity and authenticity of a gold bar requires professional assaying tools and expertise. Transacting with fake gold is a known risk in physical markets. With Bitcoin, verification is intrinsic to the protocol. The network itself validates every coin and transaction. It is effectively impossible to transact with a counterfeit unit, as the decentralized nodes would reject the invalid data immediately.

Comparing Monetary Properties

The following table outlines how Bitcoin compares to gold and fiat currency across various monetary attributes:

| Attribute | Bitcoin | Gold | Fiat Currency |

|---|---|---|---|

| Scarcity | Fixed (21M cap) | High | Unlimited (printable) |

| Portability | High (Digital) | Low (Physical) | High (Digital/Physical) |

| Divisibility | High (8 decimals) | Moderate | High |

| Verifiability | Instant/Easy | Difficult/Slow | Easy |

| Censorship Resistance | High | Moderate | Low |

This comparison highlights why many investors view the digital asset as a superior evolution of the store-of-value concept. By combining the scarcity of gold with the transactional ease of fiat, it attempts to bridge the gap between a savings technology and a medium of exchange.

Volatility and the Risk Asset Argument

Despite the theoretical alignment with gold, the market reality often paints a different picture. Critics argue that an asset cannot be a true store of value if its price fluctuates wildly in the short term. Volatility creates uncertainty for those looking to preserve wealth over weeks or months, rather than years. If a saver puts money into an asset and it loses half its value in a month, it has failed as a short-term store of value.

Historical Drawdowns

Bitcoin has a history of extreme price cycles. In 2014, the asset lost approximately 58% of its value. In 2018, it suffered a drawdown of roughly 73%. More recently, from its peak in November 2021 to the lows of November 2022, the price plummeted by over 75%. These massive contractions are characteristic of speculative risk assets rather than stable defensive plays. For risk-averse individuals, this level of volatility disqualifies it as a reliable place to park capital needed for near-term expenses.

The counter-argument is that volatility is a natural symptom of a new asset class undergoing price discovery. When an asset grows from zero to a trillion-dollar market capitalization, the path is rarely linear. Proponents suggest that as the market cap grows and adoption widens, the volatility will dampen, eventually allowing it to behave more like a traditional stable asset. However, until that maturation occurs, the risk label remains valid.

Correlation with Tech Stocks

In recent years, the asset has shown a high correlation with the Nasdaq 100 and other growth-oriented equity indices. During periods of macroeconomic tightening, such as when central banks raise interest rates, both tech stocks and digital assets tend to sell off together. This suggests that many institutional investors treat crypto exposure as part of their "risk-on" portfolio allocation.

If the asset were truly a non-correlated store of value like gold, it should theoretically hold steady or rise when risk assets fall. The fact that it often moves in lockstep with speculative equities fuels the argument that it is currently a risk asset. Market sentiment, liquidity conditions, and global economic forecasts impact its price just as they do for early-stage technology companies.

Scarcity: The 21 Million Cap

Scarcity is the bedrock of the store-of-value thesis. When things are not rare, they generally hold less value over time. If an item used as money is easily produced, it leads to a reduction in purchasing power. The creators of Bitcoin addressed this by hard-coding a strict supply cap. There will only ever be 21 million units created. This makes the asset rare compared to historical forms of money like seashells, salt, or even modern fiat currencies.

Programmatic Inflation Control

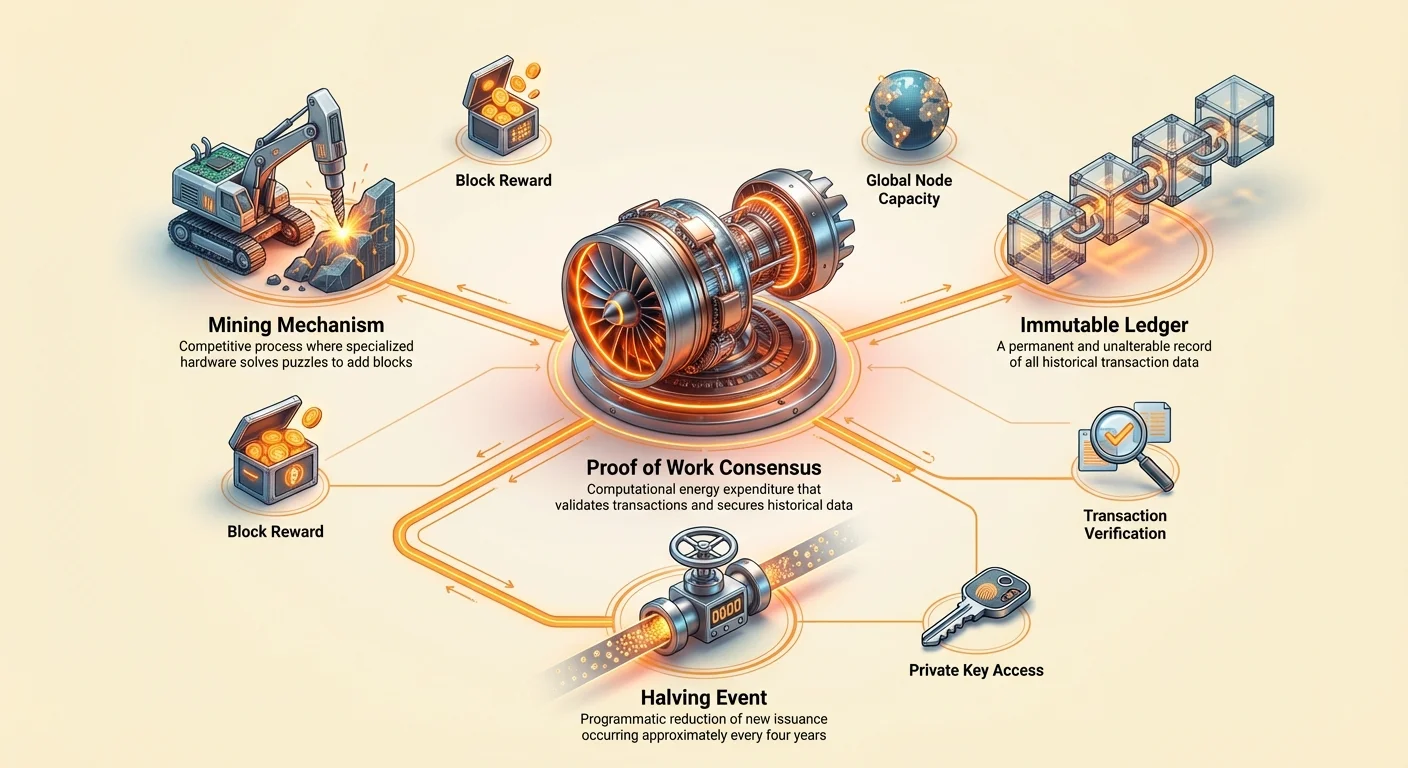

The creation of new units occurs programmatically and is predictable. Unlike central banks, which can decide to print money at any time based on policy decisions, the issuance of new coins is governed by math. Approximately every four years, an event known as the "Bitcoin Halving" occurs, cutting the daily issuance of new coins in half. This disinflationary schedule ensures that the supply expands at a decreasing rate until it eventually hits the hard cap.

This fixed supply creates a stark contrast with fiat currencies. The US dollar, for example, has an unlimited potential supply. Governments and central banks increase the money supply to manage economic stability, fund debts, or stimulate growth. While this flexibility has policy advantages, it inevitably dilutes the value of existing currency units held by savers. Bitcoin’s rigid monetary policy is designed to prevent this dilution completely.

Divisibility and Availability

While the total supply is capped, the asset is highly divisible. One unit can be divided into 100 million smaller pieces known as "sats." This divisibility ensures that the world will never effectively "run out" of the currency. Even if the value of a single whole coin becomes astronomically high, users can transact in tiny fractions. This feature mirrors the divisibility of gold but with much greater precision, as digital fractions are easier to manage than physical flakes or dust.

Censorship Resistance and Sovereignty

A unique aspect of this digital asset’s value proposition is its resistance to censorship. In the traditional financial system, third parties like banks, governments, and payment processors stand between a user and their funds. These intermediaries have the power to block transactions, freeze accounts, or confiscate assets. Financial censorship is the suppression of financial activities, and it is a tool often used by regimes to control dissent or enforce policy.

The Three Pillars of Resistance

Censorship resistance in the crypto ecosystem rests on three pillars: the freedom to transact, freedom from confiscation, and transaction immutability. Because the network is decentralized, no single entity can prevent a user from sending or receiving value. As long as a user holds their private keys in a self-custodial wallet, the funds cannot be frozen by a bank manager or government official.

This property makes the asset a form of "sovereign money." It empowers individuals to act as their own bank. For people living under authoritarian regimes or in countries with unstable banking systems, this feature is not merely theoretical; it is a lifeline. The ability to transport wealth across borders without permission or physical confiscation risk adds a layer of utility that traditional assets lack.

Immutability of the Ledger

Once a transaction is confirmed on the blockchain, it cannot be reversed. This prevents charge-backs and ensures that the history of the ledger remains pristine. In traditional finance, transactions can often be altered or reversed by the centralized ledger keeper. The immutability of the blockchain provides a level of finality and trust that is mathematically guaranteed rather than institutionally promised. This assurance is a critical component of its value as a reliable settlement layer for global value.

Decentralization: Removing the Middleman

The traditional banking model relies on a trusted third party to maintain the ledger. When a person receives a salary or pays rent, they trust the bank to record these deposits and withdrawals accurately. While this system works for many, it introduces counterparty risk. Banks can make mistakes, become insolvent, or be used as instruments of political control.

The Role of Nodes

Bitcoin replaces the trusted third party with a decentralized network of "nodes." Nodes are computers run by volunteers and participants all over the world. Each node maintains a full copy of the blockchain and verifies every transaction against the network's rules. Anyone can run a node without asking for permission. This redundancy ensures that no single entity controls the truth. The ledger is distributed, making it extremely difficult to hack or manipulate.

To shut down the network, an attacker would effectively need to shut down the global internet. This robustness contributes to the asset's status as a safe haven. It is not dependent on the solvency of a corporation or the stability of a specific government. It exists as a neutral protocol, similar to TCP/IP for the internet, operating continuously without downtime since its early days.

Consensus and Proof of Work

The network arrives at an agreement on the state of the ledger through a mechanism called Proof of Work (PoW). Participants known as miners expend energy to solve complex mathematical problems. This process validates transactions and secures the network against attacks. The requirement to spend real-world resources (energy and hardware) makes it prohibitively expensive for bad actors to rewrite the blockchain's history.

Mining is also the distribution mechanism for new coins. It ensures that issuance is decentralized and competitive, rather than decided by a central authority. This connection between digital value and physical energy expenditure is often cited as the "anchor" that grounds the asset's value in the physical world, much like the effort required to mine gold grounds its value.

Bitcoin vs. Fiat: The Inflation Hedge

Fiat money is government-issued currency that is not backed by a physical commodity. Its value is derived from government decree and public trust. While fiat is excellent for daily transactions due to its stability and acceptance, it is generally a poor store of value over long periods. Inflation erodes the purchasing power of fiat currency. As governments print more money, each unit buys less.

Understanding Inflation

Inflation is often described as a hidden tax on savers. If a person keeps cash under a mattress for twenty years, the nominal amount remains the same, but the real value—what that cash can buy—decreases significantly. History is replete with examples of hyperinflation where currencies collapsed entirely due to excessive printing and economic mismanagement.

Proponents view the digital asset as a hedge against this debasement. Because the supply is mathematically capped, it cannot be inflated away. In a world where central banks have aggressively expanded money supplies to combat economic crises, the appeal of a deflationary asset grows. Investors looking to protect their wealth from the erosion of fiat purchasing power often turn to hard assets like real estate, gold, and increasingly, digital currency.

Coexistence of Systems

The future financial landscape may likely see a coexistence of fiat and digital assets. Fiat remains superior for short-term spending and tax payments, while capped digital assets serve as long-term savings vehicles. The "Gresham's Law" concept in economics suggests that "bad money drives out good." In this context, people may choose to spend their depreciating fiat currency (bad money) while hoarding their appreciating digital assets (good money).

Privacy and Fungibility

A common misconception is that Bitcoin is anonymous. In reality, it is pseudonymous. Transactions are recorded publicly on the blockchain, visible to anyone. While the user's real name is not directly on the ledger, their identity is represented by an alphanumeric address. If that address can be linked to a real-world identity—perhaps through a centralized exchange that requires ID verification—then the user's entire financial history becomes traceable.

The Traceability Dilemma

Blockchain analysis firms specialize in tracking the flow of funds across the network. They can identify patterns and link addresses to specific individuals or entities. This transparency is a double-edged sword. It helps law enforcement track illicit funds, debunking the myth that crypto is primarily for criminals. However, it also degrades the privacy of law-abiding citizens who may not want their financial habits exposed to the world.

True cash is fungible and private; one dollar bill is indistinguishable from another, and handing it to someone leaves no digital footprint. Bitcoin does not fully replicate this level of privacy by default. However, privacy-enhancing tools and techniques, such as using new addresses for every transaction or utilizing "coin join" services, can improve anonymity.

Fungibility Risks

Because the history of every coin is trackable, there is a risk to fungibility. If a specific coin is associated with a hack or illegal activity, exchanges or merchants might refuse to accept it. This "taint" could theoretically make some coins worth less than others, breaking the core money principle where one unit must equal another unit. Upgrades to the protocol and second-layer technologies like the Lightning Network aim to address these privacy and fungibility concerns over time.

Environmental Considerations

The environmental impact of the network is a contentious topic in the valuation debate. Critics argue that the Proof of Work mechanism consumes vast amounts of electricity, comparable to the usage of entire countries. They posit that an asset requiring such high energy expenditure is unsustainable and ethically flawed. This "dirty" image can deter environmentally conscious investors and institutions, potentially limiting the asset's growth as a universally accepted store of value.

Energy Composition and Nuance

Supporters counter that high energy usage is the necessary cost for the most secure, decentralized network in history. They also point out that electricity consumption is not equivalent to carbon emissions. A significant portion of mining occurs using renewable energy sources like hydro, wind, and solar, often utilizing excess power that would otherwise go to waste.

Miners are geographically mobile and seek out the cheapest electricity available. This often leads them to stranded energy assets, such as remote hydroelectric dams or flared natural gas fields. By monetizing waste energy, the network can act as a subsidy for renewable energy infrastructure. Furthermore, proponents argue that the traditional banking system and gold mining industry also consume massive resources, though their environmental costs are less transparently tracked than an on-chain network.

Comparison to Ethereum and Altcoins

It is important to distinguish Bitcoin from other cryptocurrencies, particularly Ethereum. While Bitcoin is designed primarily as digital money and a store of value, Ethereum is a platform for decentralized applications (DApps) and smart contracts. Ethereum’s native token, Ether, acts more like "digital oil" fueling a global computer, whereas Bitcoin acts as "digital gold."

Different Purposes, Different Economics

Ethereum has a different monetary policy. It does not have a hard cap of 21 million units. Its supply dynamic is more complex, involving issuance for validators and the burning of transaction fees. While Ethereum has shifted to a Proof of Stake consensus mechanism to reduce energy consumption and increase scalability, this move introduces different trade-offs regarding centralization and security.

Investors often hold both, but for different reasons. Bitcoin is held for stability, security, and scarcity. Ethereum is held for its utility in the decentralized finance (DeFi) and NFT ecosystems. The distinct value propositions mean they are not necessarily direct competitors but rather complementary assets in a diversified digital portfolio. The "store of value" debate is largely unique to Bitcoin due to its specific architectural focus on immutability and fixed supply.

Conclusion

The classification of Bitcoin as either a store of value or a risk asset is not a binary choice but rather a reflection of its current stage of evolution. It possesses the structural properties of a store of value—scarcity, durability, and censorship resistance—that arguably surpass those of gold. However, its market behavior currently exhibits the volatility and correlation associated with risk assets. This contradiction is typical of a nascent money that is still undergoing the process of monetization and price discovery on a global scale.

For investors, the asset represents a unique paradox. It serves as a potential hedge against long-term monetary debasement while simultaneously carrying significant short-term speculative risk. Its decentralized nature offers protection against institutional failure and political overreach, a utility that becomes increasingly valuable in times of crisis. As the market matures and adoption deepens, the volatility is expected to subside, potentially allowing the fundamental store-of-value properties to shine through more clearly.

Ultimately, the debate will be settled by the market's usage over the coming decades. If the public and private enterprises continue to accumulate the asset as a reserve, its status as digital gold will solidify. Until then, it remains a hybrid asset class, offering the technological promise of sovereign savings wrapped in the volatile price action of early-stage innovation.

Bitcoin combines the scarcity of gold with the speed of the internet to create a new digital asset class.