The journey into cryptocurrency often begins with excitement over decentralized technology and explosive growth potential. However, as portfolios mature and trading volume increases, a crucial reality sets in: the tax implications. For many, tax reporting is viewed purely as a compliance chore—a necessary evil to track gains and report them accurately.

However, moving from basic compliance to strategic tax planning fundamentally changes your profitability. This is not about evading taxes; it is about legally and efficiently structuring your asset management and transactional flow to minimize liabilities. By strategically applying complex accounting methods like Specific Identification and proactively engaging in tax loss harvesting, you can significantly reduce the amount owed to tax authorities, preserving capital for future investment.

This guide moves beyond the simple act of calculating your total tax bill. We will explore the advanced methods and strategies employed by sophisticated crypto investors to optimize their financial outcomes throughout the year, ensuring that every transaction is viewed through the dual lens of market opportunity and tax efficiency. Mastering these concepts is the critical step toward building self-sovereignty in the digital economy, turning tax season from a stressful scramble into a strategic advantage.

The Foundation: Capital Gains and The Optimization Mindset

In most major jurisdictions, cryptocurrencies are treated as property, not currency. This fundamental classification means that every time you trade one crypto for another, exchange crypto for fiat currency, or use crypto to purchase goods or services, you are typically realizing a capital gain or loss. Understanding the mechanics of capital gains is the prerequisite for any optimization strategy.

The Cost Basis Imperative

Your cost basis is the total price you paid for an asset, including any fees or commissions required to acquire it. When you sell an asset, the taxable event is the difference between the sale price (the proceeds) and your cost basis.

- Gain: Proceeds > Cost Basis

- Loss: Proceeds < Cost Basis

If you buy 1 ETH for $2,000 and sell it later for $3,500, your realized gain is $1,500. This $1,500 is what the government taxes. The primary goal of tax optimization strategies is not to reduce the sale price, but to strategically manage which specific cost basis is matched against that sale price.

Short-Term Versus Long-Term Advantage

Tax minimization is profoundly affected by the holding period of your assets. Generally, tax authorities differentiate between assets held for less than one year (short-term) and those held for one year or more (long-term).

- Short-Term Gains: Often taxed at your ordinary income tax rate, which can be high (potentially 30% or more, depending on your income bracket).

- Long-Term Gains: Typically taxed at preferential, lower rates (in some countries, these rates are significantly reduced or even zero for certain income levels).

Strategic Tip: The most fundamental optimization strategy is patience. Holding assets beyond the one-year mark transforms highly taxed ordinary income into lower-taxed long-term capital gains, offering the most substantial tax saving potential for investors focused on accumulation.

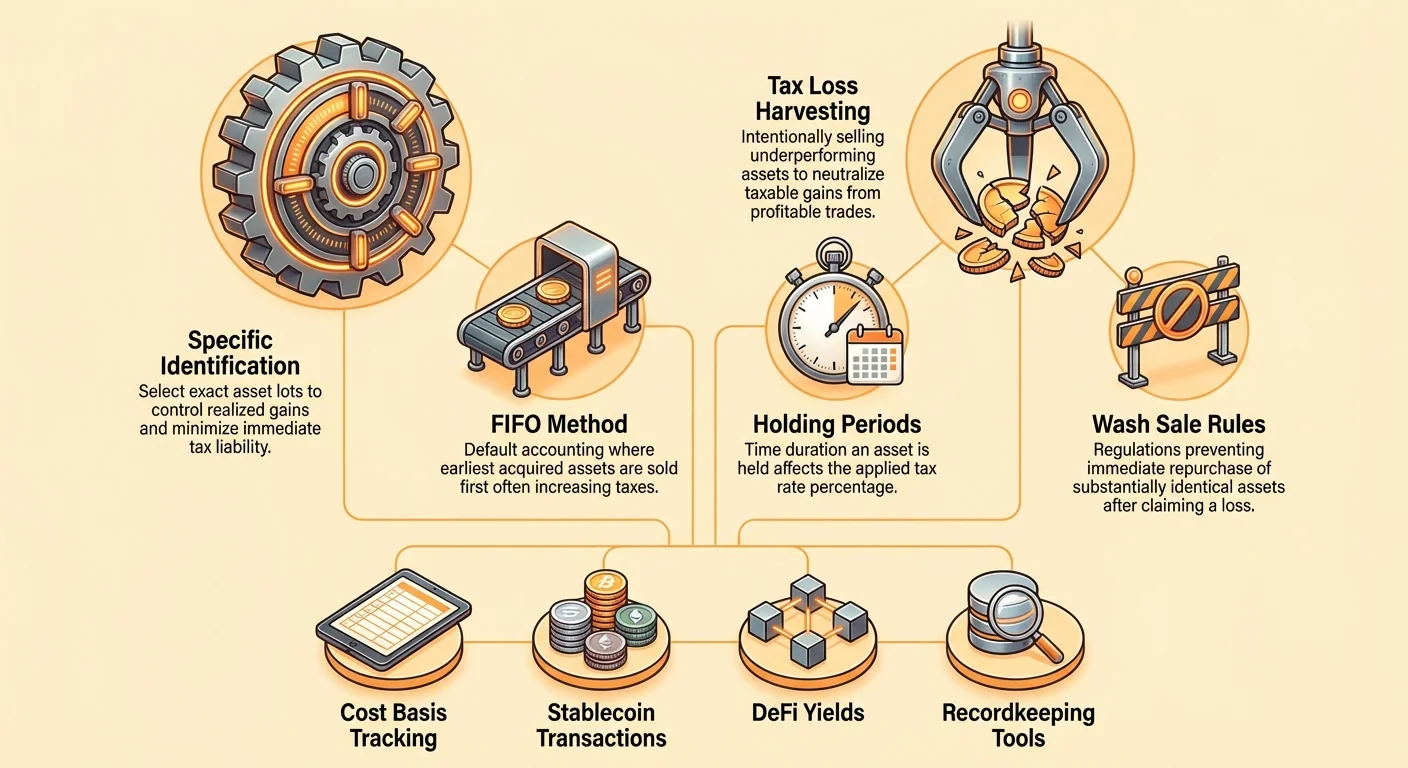

Inventory Accounting Methods: The Core of Optimization

When you buy a single cryptocurrency like Bitcoin or Ethereum multiple times over many years, you end up holding several distinct "lots," each purchased at a different price. When you decide to sell 1 ETH, how do you determine which specific $2,000-cost-basis lot gets matched with the sale? This is where inventory accounting methods come into play, and the method chosen can dramatically affect your realized tax liability.

FIFO (First-In, First-Out)

FIFO is the default method used by many tax jurisdictions and reporting software unless you specify otherwise. It operates on the simple principle that the very first unit you bought is the first unit you sell.

- How it works: When you sell 1 BTC, FIFO dictates that you match that sale against the oldest available BTC in your portfolio.

- Tax Implication (Rising Market): If the market has trended upward over time, the oldest coins will likely have the lowest cost basis. Matching a low cost basis against a high sale price results in the highest possible realized capital gain, meaning FIFO is generally the least tax-efficient method in a sustained bull market.

- When it's useful: FIFO is straightforward, easy to track, and may be preferred if you primarily want to ensure your older coins qualify for the preferential long-term capital gains rate.

LIFO (Last-In, First-Out)

LIFO assumes that the most recently acquired units are the first ones sold.

- How it works: When you sell an asset, LIFO matches that sale against the newest available lot in your portfolio.

- Tax Implication (Rising Market): If the market has been rising, your most recent purchases will have the highest cost basis. Matching a high cost basis against a sale price results in the lowest realized gain (or potentially a smaller loss), thus deferring tax.

- Regulatory Status: LIFO is generally not an accepted method for tax reporting in many major jurisdictions (including the USA, for tax purposes generally). This restriction is in place because it allows businesses to artificially depress taxable income during inflationary periods. Always verify the legality of LIFO in your specific tax jurisdiction before attempting to use it.

Specific Identification (Spec ID)

Specific Identification (Spec ID) is the gold standard for crypto tax optimization. It allows you to choose exactly which lot (i.e., which specific buy transaction) you wish to sell at the moment of the transaction realization.

The Power of Choice: Instead of being locked into an arbitrary sequence (like FIFO or LIFO), Spec ID gives you control to achieve specific tax goals:

- Goal: Minimize Tax Today (Loss Realization): If you are selling BTC for cash, you can choose to sell the lot that has the highest cost basis (perhaps a purchase made during a recent market high). This minimizes your gain or maximizes your loss, reducing your immediate tax bill.

- Goal: Maximize Long-Term Holding: If you have several lots, some held for 10 months (short-term) and some held for 14 months (long-term), you can choose to sell only the 14-month lots to take advantage of the lower long-term capital gains rate.

- Goal: Zero Out a Gain (Tax Neutrality): If you realized a $500 short-term gain earlier in the year, you can choose to sell a different lot that currently carries a $500 short-term loss, making the net outcome zero for that tax category.

Requirement for Spec ID: To legally use Spec ID, you must maintain impeccable records demonstrating that you specifically identified the asset lot at the time of the sale. This is often handled through integrated crypto accounting software that allows you to tag or select lots prior to generating the tax report. Without rigorous recordkeeping, tax authorities will default you to FIFO.

Deep Dive: Strategic Tax Loss Harvesting

Tax loss harvesting is a proactive strategy that takes advantage of market dips. Instead of simply waiting for your assets to recover, you intentionally sell assets currently trading at a loss to offset any realized gains you have accrued throughout the year.

This strategy is particularly powerful in volatile markets like crypto, where sharp price movements are common. It allows you to "capture" the loss value for tax purposes without necessarily abandoning your investment position.

Definition and Mechanism

Tax loss harvesting involves three steps:

- Identify Realized Gains: Determine the amount of profits you have already realized this year (e.g., from profitable trades, exchange swaps, or selling stablecoins).

- Identify Unrealized Losses: Find assets in your portfolio whose current market value is lower than their cost basis.

- Execute the Harvest: Sell the assets with the unrealized loss. This converts the unrealized loss into a realized capital loss.

The core optimization step is realizing losses, which are then used to reduce or completely eliminate realized capital gains.

Example Use Case:

- Scenario: You sold ETH in March for a $10,000 short-term gain (highly taxed). Later, in October, your portfolio holds 5 BTC purchased for $50,000 each, now trading at $40,000.

- Harvesting Action: You sell those 5 BTC. You realize a $10,000 loss (5 x $10,000 loss per coin).

- Result: This $10,000 realized loss offsets the $10,000 realized short-term gain, reducing your net taxable short-term capital gain to $0 for the year.

When and How to Harvest Effectively

While tax loss harvesting can be done anytime, its effectiveness is optimized when used against short-term gains, which are taxed at higher ordinary income rates.

- Target High-Tax Gains First: Use harvested losses to cancel out short-term gains first. If you still have excess losses, they can then offset long-term gains.

- The $3,000 Annual Deduction: If your total realized losses exceed your total realized gains, in jurisdictions like the US, you are typically permitted to deduct up to $3,000 of the net loss against your ordinary income (wages, salary). Any remaining loss is carried forward indefinitely to offset future capital gains.

- End-of-Year Timing: While you can harvest anytime, many investors execute large harvesting events in the final weeks of the calendar year. This ensures they have a clear picture of their total gains and losses before the tax filing deadline.

Mitigating Risk: The Substitute Asset Strategy

The primary risk of tax loss harvesting is that you liquidate an asset, and immediately afterward, its price spikes, causing you to miss out on the recovery. To manage this, smart harvesters employ the "substitute asset" strategy.

Instead of simply selling the asset and waiting 31 days (if wash sale rules applied, see next section), you immediately rotate the proceeds into a different asset that tracks the same sector or movement but is not technically identical.

- Action: Sell BTC for a loss.

- Immediate Reinvestment: Immediately use the proceeds to buy an equivalent amount of ETH or a BTC-correlated ETF (if available and regulatory compliant).

This approach maintains your exposure to the crypto market upside while realizing the necessary loss for tax purposes. If BTC recovers, ETH or the correlated asset likely will, too, preserving your overall market position.

Navigating Wash Sale Rules: Compliance and Strategy

Tax loss harvesting must be performed with careful consideration of the Wash Sale Rule. This rule is designed to prevent taxpayers from harvesting losses purely for tax purposes without genuine economic change.

The Traditional Wash Sale Rule

In traditional securities markets (stocks, bonds), the Wash Sale Rule prohibits an investor from claiming a loss if they buy the same or a "substantially identical" security within 30 days before or 30 days after the date of sale (a 61-day window). If a wash sale occurs, the loss is disallowed for tax purposes, and the disallowed loss is added to the cost basis of the newly acquired security.

The Crypto Gray Area (USA)

As of the writing of this guide, cryptocurrencies are generally exempt from the traditional Wash Sale Rule in the United States. Since crypto is typically classified as property rather than stock or security, the IRS rule designed for securities does not automatically apply.

The immense strategic implication of this exemption is that U.S. investors can sell BTC at a loss and buy the exact same amount of BTC back one minute later, realize the loss for tax purposes, and retain their position in the market.

CRITICAL WARNING: This exemption is a significant loophole that major governments, including the US, are actively seeking to close. Legislative proposals aimed at applying wash sale rules to digital assets have been introduced.

- Actionable Advice: Treat the absence of wash sale rules as a temporary advantage. If you execute a loss harvest, be prepared for potential future rule changes that could retroactively impact compliance, though this is unlikely. For extreme certainty, adopt the substitute asset strategy discussed above, which insulates you regardless of future wash sale legislation.

Global Variations and Superficial Losses

While the US stands out in its current exemption, many other jurisdictions have similar rules that effectively limit aggressive loss harvesting:

- Canada: Canada employs the Superficial Loss Rule. This rule is broader than the US wash sale rule and applies to many types of property, including crypto. If you repurchase the same asset or a similar asset within 30 days, the loss will be disallowed. Canadians must therefore employ the substitute asset strategy strictly.

- United Kingdom/Australia: These jurisdictions have their own complex rules regarding losses and holding periods. Always consult with a tax professional familiar with your local jurisdiction’s specific definitions of “security” and “property.”

Minimizing Taxes on Everyday Transactions

Most crypto investors focus optimization efforts on large sales, neglecting the dozens of small, often overlooked taxable events that occur daily, particularly involving stablecoins and decentralized finance (DeFi).

The Stablecoin Trap

Stablecoins (like USDC, USDT, DAI) are essential tools for traders because they allow them to exit volatility without converting back to fiat currency. However, a common misconception is that using stablecoins is tax-neutral.

The Reality: If you held ETH and traded it directly for USDC, that transaction is typically a taxable event (ETH-to-USDC is a crypto-to-crypto trade). If the ETH had gained value since you acquired it, you realize a capital gain, even though you immediately moved into a stable asset.

Strategy for Minimizing Stablecoin Taxes:

- Use Spec ID for Stablecoin Conversions: If you need to convert $10,000 worth of BTC into USDC to sit out a volatile period, use the Specific Identification method. Select the BTC lots that have the highest cost basis (or even a loss) to minimize the gain realized upon conversion.

- Purchase Stablecoins with Fiat: If possible, acquire new stablecoins directly using fresh fiat currency. Since the cost basis of the fiat equals the acquisition price of the stablecoin, the initial transaction incurs zero capital gain. You now have tax-free ammunition for trading.

- Minimize Transaction Volume: If you constantly move assets in and out of stablecoins on an exchange, you generate hundreds of taxable events. Consolidate your trading to fewer, more impactful moves to simplify tracking and reporting.

Managing DeFi and Yield Taxes

Interacting with DeFi protocols (staking, providing liquidity, lending) can generate both capital gains and ordinary income, requiring unique strategies:

- Rewards as Income: Income derived from staking rewards, interest, or mining is typically taxed as ordinary income at the moment it is received (or becomes controllable), based on its fair market value at that time.

- Capital Gains on Rewards: If you receive 1 ETH as a staking reward (valued at $3,000 at receipt), your cost basis for that ETH is $3,000. If you sell it later for $4,000, the $1,000 difference is a capital gain.

Optimization Strategy for Yield: Use your oldest, lowest cost basis gained assets (like rewards) first when harvesting losses or needing to realize minimal gains. Since their cost basis is often $0 (if earned via mining/airdrop, and thus only taxed upon receipt), holding them long-term is especially beneficial.

Gifting and Donations

Gifting crypto to family members or donating to charitable organizations can be highly tax-efficient strategies (depending on local regulations regarding gift/estate tax thresholds).

- Charitable Donation (USA Context): If you donate crypto that you have held for more than one year (long-term capital asset), you generally do not have to pay capital gains tax on the appreciation. Furthermore, you may be able to deduct the full fair market value of the donation from your taxable income, effectively providing a double tax benefit.

- Gifting to an Individual: Gifting crypto is usually not a taxable event for the giver (up to annual and lifetime limits). The recipient inherits the giver's cost basis, meaning when the recipient eventually sells, they will be responsible for the capital gains realized from the original purchase price. This can be a strategic way to transfer appreciated assets to family members who may be in a lower income tax bracket.

Implementing Strategy: Tools and Recordkeeping

The best tax optimization strategies are useless without accurate, detailed, and verifiable records. The transition from simple exchange trading to complex DeFi interactions, multiple wallets, and cross-chain swaps exponentially increases the difficulty of recordkeeping.

Choosing the Right Accounting Software

Modern crypto tax software platforms are no longer just calculators; they are sophisticated compliance and optimization tools. When selecting a platform, prioritize features that enable sophisticated strategic planning:

- Support for Specific Identification (Spec ID): This is paramount. The software must allow you to assign specific lot IDs to sales and track cost basis across thousands of transactions seamlessly. If a platform defaults only to FIFO and does not offer Spec ID functionality, it severely limits your optimization potential.

- Broad Integration: The platform must connect via API or CSV upload to all your centralized exchanges (CEXs), non-custodial wallets (self-custody), and complex DeFi protocols (like lending, staking, and liquidity pools).

- Jurisdictional Support: Ensure the platform can accurately calculate taxes based on your specific country's rules (e.g., handling the Superficial Loss rule for Canada, or complex income categorization for the UK).

- Transaction Tagging and Classification: The tool must allow you to manually review and tag transactions (e.g., differentiating between a "swap" (taxable sale) and a "transfer" (non-taxable movement between your own wallets), or correctly classifying Airdrops, ICOs, and Gifts).

Best Practices for Clean Data

Garbage in, garbage out. The accuracy of your tax reports—and thus the effectiveness of your optimization—depends entirely on the completeness and correctness of your underlying data.

- Track Wallet Transfers Meticulously: Every time you move crypto from a CEX to your hardware wallet, or from Wallet A to Wallet B, this is a non-taxable "transfer." However, if your software cannot clearly link the source and destination, it might accidentally flag the movement as a withdrawal (sale) and a deposit (income), creating phantom taxable events. Manually verify all transfers.

- Tag DeFi Transactions: When providing liquidity or staking, ensure the software tags the transaction correctly. When you withdraw LP tokens or unstake, verify the platform accurately calculates the associated accrued income and capital gain/loss on the underlying assets.

- Keep Records of Cost Basis Inputs: If you acquired crypto through means other than purchasing (e.g., mining, earning salary in crypto, or an airdrop), keep documentation showing the asset's fair market value (FMV) on the date of receipt. This FMV becomes your cost basis, which is essential for calculating future gains when you eventually sell.

Conclusion: Turning Complexity into Capital

Moving from simply calculating your crypto taxes to strategically optimizing them requires a fundamental shift in perspective. It means viewing every transaction—from a major sale to a minor stablecoin swap—as an opportunity to manage your cost basis and minimize your liability.

The most potent tools in this optimization toolkit are the Specific Identification method, which gives you precise control over lot selection, and proactive Tax Loss Harvesting, which utilizes market downturns to offset realized gains.

While the regulatory environment for digital assets remains complex and rapidly evolving, proactive compliance combined with disciplined strategic planning ensures you are building your digital wealth efficiently. By implementing clean recordkeeping practices, leveraging advanced accounting software, and making deliberate decisions about when and how to realize gains and losses, you stop guessing and start building true financial self-sovereignty. Consult with a qualified tax professional to apply these strategies effectively within your specific jurisdiction.