For years, the promise of Bitcoin (BTC) was to serve as a peer-to-peer electronic cash system. Yet, for the average person standing at a checkout counter, using native Bitcoin remains impractical. Standard BTC transactions are slow, often taking ten minutes or more to confirm, and can incur network fees (gas) that make small purchases expensive. For these reasons, developers continue to focus on tools for reducing transaction costs.

This friction led to the rise of Bitcoin spending cards—tools designed to bridge the gap between the volatile, decentralized world of crypto and the established, instant fiat payment rails (Visa, Mastercard). These cards allow users to spend their BTC anywhere traditional plastic is accepted, instantly converting the digital asset into local currency at the point of sale.

However, not all BTC cards are created equal. The true frontier of efficient Bitcoin spending lies in the adoption of the Lightning Network. This article provides a comprehensive guide to understanding, evaluating, and utilizing the best BTC spending cards, prioritizing those that leverage Lightning technology for instant, low-cost utility, making Bitcoin truly viable for everyday consumer use.

Understanding Bitcoin Spending: The Need for Speed

Before diving into card reviews, it’s essential to understand why a card is necessary in the first place, and what problem technologies like the Lightning Network solve for the end-user.

The Problem with On-Chain BTC Payments

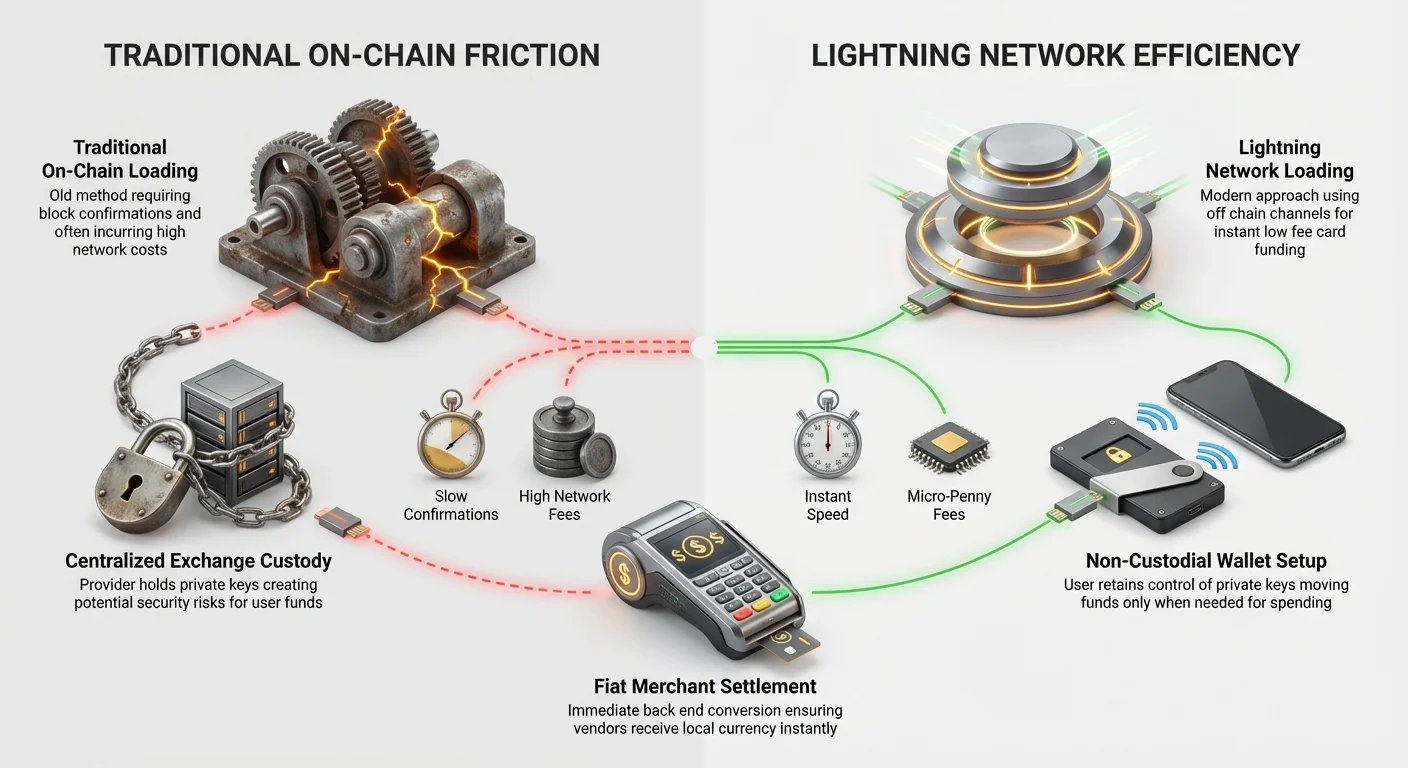

When you send Bitcoin directly on the primary blockchain (known as "on-chain"), every transaction must be bundled into a block and validated by miners across the globe. This process ensures security and immutability but introduces significant delays and costs:

- Confirmation Times: Blocks are found roughly every ten minutes. To be considered secure, a transaction usually needs three to six confirmations, meaning you could wait 30 minutes to an hour for the payment to be finalized. This is unacceptable for buying a coffee or groceries.

- Volatile Fees: During periods of high network congestion, the fees required to incentivize miners to include your transaction quickly can spike dramatically, sometimes exceeding the cost of the purchase itself.

Without instantaneous payment finality, Bitcoin cannot compete with established digital payment systems like credit cards or mobile pay.

What is a Crypto Debit Card, Functionally?

A Bitcoin debit card (or spending card) does not typically send BTC on-chain at the moment you swipe. Instead, it acts as a translator:

- Pre-funding: The user deposits BTC into a wallet associated with the card provider (often a centralized exchange or custodian).

- Instant Conversion: When the card is swiped at a merchant terminal, the card provider instantly sells the necessary amount of BTC (or a linked stablecoin) on their internal exchange.

- Fiat Settlement: The provider immediately converts the crypto into fiat (USD, EUR, etc.) and settles the transaction with the merchant via the Visa or Mastercard network.

This process is instantaneous for the merchant because the card provider takes on the immediate risk and handling of the crypto conversion, guaranteeing the fiat payment instantly. The card is essentially a fiat-denominated spending tool funded by an underlying BTC reserve.

The Game Changer: Lightning Network Integration

The most significant advancement for BTC spending cards is the integration of the Lightning Network (LN). This technology transforms how users load and manage the crypto balance that funds their card, drastically cutting costs and increasing speed compared to traditional on-chain transfers.

Lightning 101: Instant, Low-Cost Payments

The Lightning Network is a "Layer 2" solution built on top of the Bitcoin blockchain. Think of it as opening a private tab at a bar, rather than paying for every drink individually: Layer 2 scaling solutions:

- Payment Channels: Users set up secure, two-way payment channels with other nodes (individuals or services) on the network.

- Off-Chain Transactions: Once a channel is open, users can send unlimited transactions instantly between them without needing to wait for main blockchain confirmation. These transactions are secured cryptographically but occur "off-chain."

- Final Settlement: Only when the users decide to close the channel are the net results of all the thousands of transactions recorded as a single entry on the main Bitcoin blockchain.

The result? Fees drop to fractions of a cent, and transactions are confirmed in milliseconds.

How Lightning Solves the Card Problem

For card users, Lightning integration primarily revolutionizes the loading process:

- On-Chain Loading: If your card provider only accepts on-chain BTC, you must wait 10-60 minutes and pay standard network fees (e.g., $1–$5) every time you move BTC from your personal wallet to your card balance.

- Lightning Loading (The Superior Method): A card provider that supports LN loading allows you to send BTC instantly from any Lightning-enabled wallet (e.g., Wallet of Satoshi, Phoenix) to your card balance. This transfer takes seconds and might cost less than a penny.

This capability fundamentally shifts the economics of spending small amounts of BTC. You can now use your card balance as a true "hot wallet" that is funded just in time without penalizing small transfers.

Identifying True Lightning Cards vs. Marketing Gimmicks

When evaluating a card, check the specific implementation of Lightning. Many companies advertise "crypto cards," but only the best ones allow for instant, low-fee BTC loading.

- True Lightning Integration: The card provider offers a dedicated Lightning invoice or a Lightning Address for funding the card balance. This is the gold standard for BTC power users seeking efficiency.

- Partial or Indirect Integration: Some services claim Lightning support but require you to bridge your BTC through a third-party custodial wallet or a stablecoin (like USDC) before loading the card. This adds steps, often defeats the purpose of pure BTC spending, and reintroduces fees.

- Fiat-Only Load: The worst offenders market themselves as "Bitcoin cards" but require users to load fiat (USD/EUR) onto the card first, and then rely on the user holding BTC in a separate, linked account. This means the card is just a standard debit card, and the BTC conversion happens elsewhere, adding complexity.

Actionable Tip: Always test the loading process with a minimal amount of BTC first. If the platform asks you for an on-chain address or estimates a 10-minute confirmation time, it is not optimized for Lightning loading.

Custody Models: Centralized vs. Non-Custodial Spending

The choice of Bitcoin spending card often comes down to a critical question: how much control do you want over the keys to your BTC? This is defined by the card’s custody model.

Centralized Exchange Cards (The Easiest Path)

The vast majority of currently available BTC spending cards are offered by major centralized crypto exchanges (CEXs). These are the easiest cards to obtain and use for beginners, but they come with a custodial risk.

How They Work

When you use a CEX card, you hold your BTC within an exchange-controlled wallet. This means the exchange holds the private keys—you never truly possess the coins until you withdraw them to a personal wallet. Understanding custody risks.

Pros:

- Simplicity and Rewards: Easy setup, often integrated directly with a robust trading platform. Many CEXs offer tiered cash-back or crypto rewards (e.g., 1% to 8% back on purchases).

- High Limits: Typically allow for higher daily spending and withdrawal limits than smaller providers.

- Insurance (Limited): Some large exchanges carry insurance on their hot wallets, though this rarely covers user funds lost due to exchange mismanagement or collapse.

Cons:

- Custody Risk: If the exchange is hacked, fails, or freezes accounts, your funds may be inaccessible. This violates the core Bitcoin principle of "not your keys, not your coins."

- KYC Requirements: Full Know Your Customer (KYC) compliance is mandatory, requiring government ID and personal data.

- Fees and Spreads: While some advertised fees are low, the exchange controls the BTC-to-fiat conversion rate (the spread), which can be less favorable than market rate.

Non-Custodial Solutions and Load-Based Cards (The Maximalist Path)

Non-custodial solutions aim to mitigate custody risk by requiring the user to hold the private keys in their own self-custody wallet, only moving funds to the card just before spending.

How They Work

True non-custodial BTC spending cards are rare because they must instantly convert an asset held outside their control. Most solutions that lean non-custodial operate on a "load-based" model:

- User Self-Custody: Your main BTC holdings remain secure in your personal hardware or software wallet (e.g., Ledger, Trezor, or a mobile Lightning wallet).

- Load/Top-Up: You use a small, necessary amount of BTC, often via the Lightning Network, to top up the card’s "hot wallet" balance. This small balance is custodial but minimizes risk because only the amount you intend to spend immediately is exposed.

- Spending: The card spends from the small, recently loaded balance.

This model is inherently safer for large BTC holders who want to retain control over the majority of their assets while still having the utility of a spending card. Companies that prioritize Lightning adoption often use this load-based, low-custody approach.

Key Difference: A CEX card wallet might hold $10,000 worth of your BTC. A load-based card wallet only holds the $50 you topped up 30 seconds ago using a Lightning invoice.

Key Evaluation Criteria for BTC Spending Cards

Choosing the right Bitcoin card requires moving beyond glossy marketing and focusing on the underlying financial mechanics. The true cost of using a card is determined by three main factors: conversion, loading, and regional accessibility.

Conversion Fees and Spreads (The Hidden Costs)

When you spend BTC, two fees are incurred in the conversion to fiat:

1. The Explicit Conversion Fee

This is a flat percentage charged by the provider for executing the trade (e.g., 0.5% to 3.0%). This fee is usually clearly listed in the card’s fee schedule. For a BTC maximalist, finding a card with 0% conversion fees should be a priority, although these usually require a monthly subscription or a high tier of staking (holding) the provider’s native token.

2. The Exchange Spread

This is the difference between the true market price of BTC (the midpoint between the bid and ask price) and the price the card issuer gives you for the conversion.

- Example: If BTC is trading at $60,000, but the card provider sells your BTC for $59,500 to fund your purchase, the $500 difference is the spread—a hidden cost that benefits the issuer.

Cards that are highly transparent about their liquidity providers and offer near-spot-price conversions are superior. Non-custodial, Lightning-focused solutions often minimize the spread since their core business is payment processing, not asset trading.

Loading and Withdrawal Fees

The true cost of a BTC card often lies in how you move money onto and off of it.

On-Chain vs. Lightning Load Fees

As established, a card that mandates on-chain BTC deposits will cost you significantly more over time due to network fees. If you load your card weekly, you could spend $20-$50 per month just on network fees. Lightning Network adoption is the primary fee-reducing mechanism for regular users.

ATM Withdrawal Fees

BTC spending cards function as debit cards, allowing cash withdrawals at ATMs. Be aware of the multiple layers of fees here:

- Provider Fee: A fee charged by the card issuer for the withdrawal (e.g., 2%).

- ATM Operator Fee: A fee charged by the bank or company operating the ATM itself.

- Foreign Transaction Fee (if applicable): If you withdraw fiat in a different currency than your card's base currency, a conversion fee applies.

For those planning to use BTC to access cash while traveling, finding a card with high, fee-free monthly ATM limits is crucial.

Regional Availability and Regulatory Compliance (KYC/AML)

The cryptocurrency card landscape is heavily dictated by geography and regulation.

- Jurisdiction: Most major cards are available only in specific regions (e.g., the European Economic Area (EEA), the US, or specific Asian countries). Regulations like the EU’s Markets in Crypto-Assets (MiCA) framework impose strict rules, affecting which cards can operate there.

- KYC/AML: Anti-Money Laundering (AML) and Counter-Terrorist Financing (CTF) rules require almost all card providers to implement mandatory KYC. While some initial "no-KYC" cards existed in the early days, they have largely been phased out due to strict banking partner requirements. If privacy is paramount, non-custodial Lightning wallets used for direct merchant payment (not card spending) are the only truly anonymous option left.

Deep Dive: Specialized Lightning-Focused BTC Cards

The market is rapidly shifting toward specialized cards that prioritize Bitcoin’s Layer 2 capabilities. Here is a look at what makes these cards stand out and how they meet the needs of the BTC maximalist.

The Focus on Utility Over Rewards

Traditional centralized exchange cards compete primarily on rewards (cashback). Lightning-focused cards, conversely, compete on pure utility: speed, minimal fees, and open accessibility.

For a Lightning user, the reward is the minuscule transaction cost. A CEX card offering 2% back on a purchase might sound good, but if you paid a $5 on-chain fee to load the card, it would take $250 in purchases just to break even on the loading fee. A Lightning load costs less than $0.01, making every small transaction profitable from a fee perspective.

Security through Minimal Exposure

Lightning-enabled load cards inherently promote better security practices, even for novice users. By requiring users to only move small amounts for immediate use, it prevents the common mistake of storing large cryptocurrency balances on a centralized exchange platform.

This "load-as-you-go" strategy aligns perfectly with decentralized security models: your capital is protected in your secure self-custody wallet, and only operational cash is exposed to the payment provider.

Case Study: How a Lightning Card Transaction Works

Imagine you are using a Lightning-enabled BTC card to buy a $10 meal:

- Low Balance: Your card balance is currently $0.

- Instant Load: You open your preferred self-custody Lightning wallet (e.g., Muun, BlueWallet) and scan the card provider’s Lightning invoice for $10.05 (including a small buffer).

- Instant Confirmation: The BTC transfer confirms in 1-2 seconds, costing $0.005 in fees.

- Swipe: You swipe the card. The provider instantly converts the $10.00 worth of BTC into $10.00 USD (minus their spread).

- Settlement: The vendor receives $10.00 USD instantly via the traditional payment network.

The total time elapsed between deciding to fund the card and completing the purchase is often less than 10 seconds, fulfilling the requirement to spend BTC instantly.

Practical Strategies for Maximizing BTC Card Utility

Utilizing a Bitcoin spending card optimally requires strategy, particularly in how you handle loading, market volatility, and integration with your broader crypto holdings.

Strategic Loading: Timing the Market

Unlike fiat debit cards, where the balance value is stable, BTC balances fluctuate constantly.

Dollar-Cost Averaging (DCA) vs. Just-in-Time Funding

- DCA Strategy (For Stablecoin Cards): If you use a card backed by stablecoins (like USDC or USDT) which you purchased with BTC, the DCA strategy is simple: periodically sell BTC for stablecoins to maintain a buffer. This minimizes volatility risk for spending.

- Just-in-Time (JIT) Funding (For BTC Cards): Since BTC maximalists prefer holding native BTC, the JIT strategy is superior. Only load the minimum required amount needed for the immediate purchase or the day's expected spending. This minimizes the risk of conversion losses if BTC price suddenly drops between the time you load the card and the time you spend the funds.

Best Practice: Set a weekly budget limit for your card and only execute the Lightning load when the remaining balance falls to zero, or just before a major purchase.

Using BTC Cards for Global Travel

Bitcoin spending cards are exceptionally valuable for international travel, often surpassing the utility of traditional bank cards.

- Eliminating Foreign Exchange Fees: Many traditional banks charge 2%–3% for foreign currency conversion. The best BTC cards often execute the crypto-to-fiat conversion at a competitive rate and charge zero or very low FX fees, potentially saving substantial money on long trips.

- Accessing Local Currency: Using the card to withdraw local cash via an ATM, while still incurring operator fees, is often cleaner than dealing with dedicated currency exchanges or carrying large amounts of cash.

- Security on the Go: If your funds are held primarily in a secure, self-custody wallet, losing the physical BTC card only risks the small amount of funds currently loaded, far less than losing a bank debit card linked to your life savings.

Integrating Wallets: Connecting Lightning Wallets Directly

For seamless utility, the user experience is dramatically improved if the card provider allows direct integration or easy interoperability with popular, non-custodial Lightning wallets.

The modern BTC power user should strive to move all operational BTC into wallets optimized for Layer 2 transactions. This includes: Lightning Network Wallets:

- Phoenix Wallet / Muun Wallet: These wallets simplify channel management, making sending and receiving Lightning payments as easy as sending on-chain.

- Connecting to Card Provider: The user should be able to scan an invoice generated by the card provider directly from their chosen Lightning wallet.

Avoid card providers that require you to use their proprietary custodial mobile wallet for Lightning transactions, as this reintroduces the custody risk you are trying to minimize.

Conclusion: Bitcoin as an Everyday Currency

The journey of Bitcoin from an esoteric investment asset to a functional, everyday currency is dependent on the adoption of Layer 2 solutions like the Lightning Network. While centralized crypto exchanges made the first BTC spending cards viable, the future belongs to integrated solutions that prioritize the efficiency gains of Lightning.

For the beginner and the experienced BTC maximalist alike, the best Bitcoin spending card is the one that minimizes three things: custody risk, conversion spread, and network fees. By focusing on cards that feature seamless, sub-second Lightning Network loading, users can truly unlock the potential of Bitcoin to be spent instantly and affordably, fulfilling its original vision as electronic cash for the modern age.