The cryptocurrency landscape has evolved significantly beyond the initial concept of simple peer-to-peer value transfer. As the market matures, specialized digital assets have emerged to address specific limitations of early blockchain technology. Two of the most critical categories in this evolution are stablecoins and privacy coins. Stablecoins were developed to combat the inherent volatility of assets like Bitcoin, providing a reliable medium of exchange and store of value. Conversely, privacy coins were created to restore the anonymity that is often lost on transparent public ledgers.

These two asset classes represent opposing ends of the regulatory spectrum. Stablecoins, particularly those backed by fiat currencies, are increasingly integrating with traditional financial systems and seeking compliance. Privacy coins, by their very nature, challenge the surveillance capabilities of financial regulators. The future of these assets depends heavily on how they navigate the growing demand for government oversight. This creates a complex environment where innovation must balance against the strict requirements of emerging frameworks.

The tension between preserving the decentralized ethos of crypto and adhering to legal standards is defining the next phase of industry growth. Investors and users must understand the mechanics behind these assets to navigate the shifting terrain. From the reserve audits of centralized stablecoins to the cryptographic proofs of privacy networks, the technical underpinnings will determine which projects survive regulatory purges. This analysis explores the mechanisms, risks, and future trajectories of these specialized altcoins.

The Mechanics of Stability in a Volatile Market

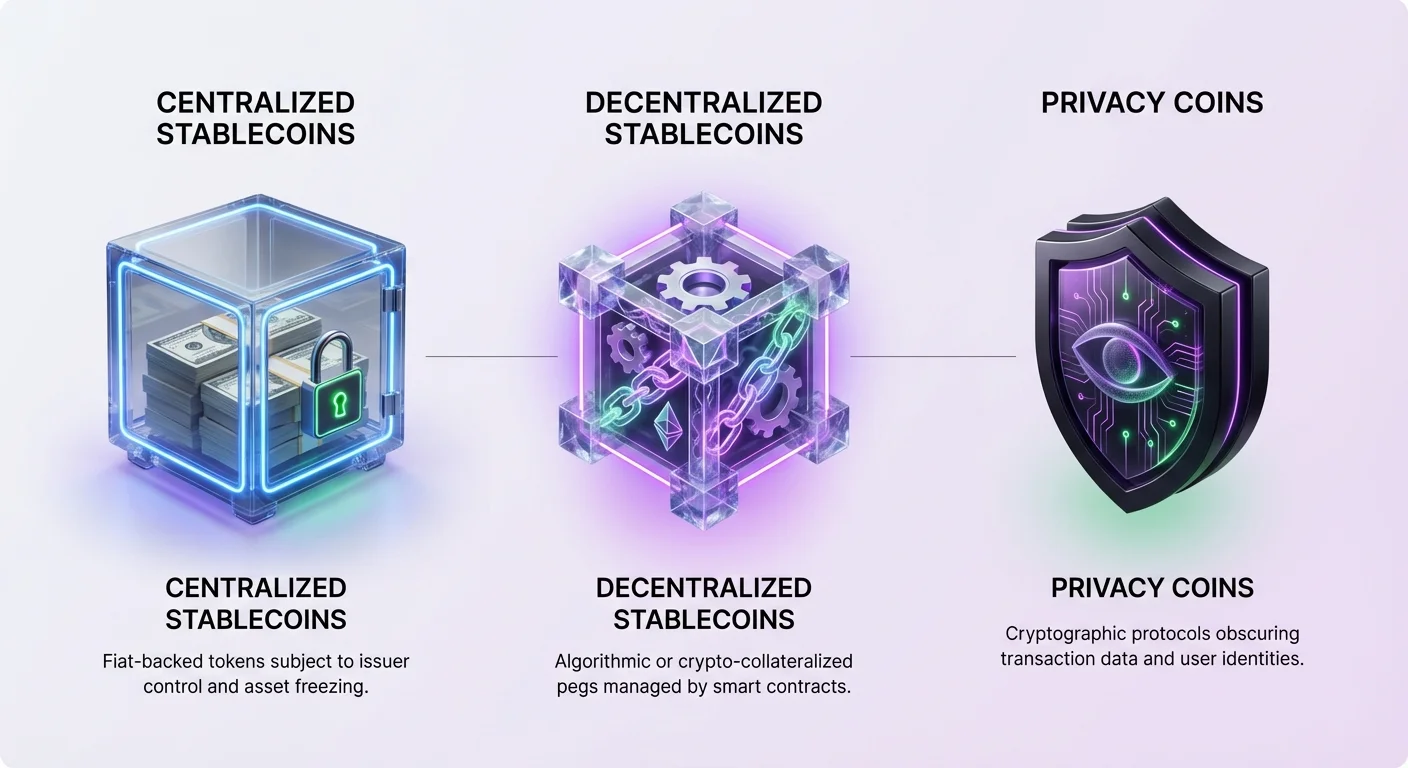

Stablecoins are digital currencies designed to maintain a pegged value, most commonly to the US dollar. They serve as a bridge between the crypto realm and traditional finance. This utility has made them essential for traders who wish to lock in profits without exiting to fiat currency. By holding stablecoins, users can avoid the price swings associated with Bitcoin or Ethereum while remaining within the blockchain ecosystem. This capability has driven massive adoption for international settlements and savings in high-inflation regions.

The most prevalent type of stablecoin is the centralized, fiat-collateralized model. In this system, a central issuer holds reserves of fiat currency or equivalent assets to back every token in circulation. For example, for every unit of a stablecoin issued, there should ideally be a US dollar held in a bank account. This allows users to redeem their tokens for the underlying fiat currency, ensuring the peg remains intact. Tokens like USDT and USDC operate on this model, though their approaches to transparency differ.

Centralized stablecoins rely entirely on trust in the issuing entity. The stability of the asset is only as good as the reserves backing it. Historically, this has led to controversy when issuers fail to provide full transparency regarding their holdings. Despite these concerns, the liquidity and ease of use offered by centralized options have kept them at the forefront of the market. They dominate trading pairs on exchanges and are increasingly used for real-world payments.

However, the reliance on a central authority introduces counterparty risk. If the issuer faces insolvency or regulatory action, the value of the stablecoin could be jeopardized. Additionally, centralized issuers have the power to freeze assets at the request of law enforcement. This censorship capability aligns them closer to traditional banking but alienates users seeking true financial sovereignty.

Decentralized Alternatives and Algorithmic Risks

To counter the risks of centralization, developers created decentralized stablecoins. These assets replace trust in a third-party company with programmatic mechanisms and smart contracts. The goal is to create a dollar-pegged asset that is permissionless and resistant to censorship. The most successful examples use a model known as Collateralized Debt Positions (CDPs). In this system, users lock up crypto assets as collateral to mint new stablecoins.

The CDP model, used by projects like DAI, requires over-collateralization to account for the volatility of the underlying crypto assets. If the value of the collateral drops below a certain threshold, the system automatically liquidates the position to maintain the stablecoin's solvency. This ensures the peg is defended by hard assets rather than promises. While less capital-efficient than fiat-backed models, this approach preserves the decentralized nature of the asset.

A more experimental and risky category is the algorithmic stablecoin. These tokens attempt to maintain their peg through mechanisms that automatically expand or contract the supply based on market demand. They often rely on a relationship with a secondary token to absorb volatility. The most infamous example is TerraUSD (UST), which used a "two-token seigniorage model." Participants were incentivized to burn one token to mint the other, theoretically keeping the price stable through arbitrage.

The failure of UST in May 2022 demonstrated the catastrophic risks of under-collateralized algorithmic models. When confidence in the system eroded, a "run on the bank" occurred, driving the value of both tokens to near zero. This event wiped out billions of dollars in value and highlighted the difficulty of creating stability without substantial backing. It served as a stark lesson that code alone cannot always overcome extreme market panic.

Privacy Coins and the Quest for Anonymity

While stablecoins seek to fix price volatility, privacy coins address the lack of confidentiality on public blockchains. On networks like Bitcoin, every transaction is recorded on a public ledger. Anyone can trace the flow of funds from one address to another, potentially revealing the identity of the user and their financial history. Privacy coins employ advanced cryptography to obscure these details, protecting user data from surveillance.

One of the primary techniques used is the stealth address. This feature generates a unique, one-time address for every transaction. Even if a user publishes a single public address for receiving funds, the blockchain records each incoming payment to a different, unlinkable address. This prevents outside observers from linking multiple payments to a single recipient, effectively severing the connection between a user's identity and their wallet balance.

Ring signatures are another powerful tool used by leading privacy coins like Monero. This technique mixes a user's transaction with several other "decoy" transactions picked from the blockchain. To an outsider, it appears as though a group of people signed the transaction, but it is mathematically impossible to determine which member of the group was the actual sender. This ensures that the origin of the funds remains ambiguous.

Confidential Transactions add a final layer of privacy by hiding the amount being transferred. By combining these technologies, privacy coins ensure that the sender, recipient, and transaction amount are all concealed. This restores the property of fungibility to cryptocurrency. In a transparent system, coins can be "tainted" by their history, but in a private system, all coins are equal and interchangeable because their history is untraceable.

The Compliance Landscape for Stablecoins

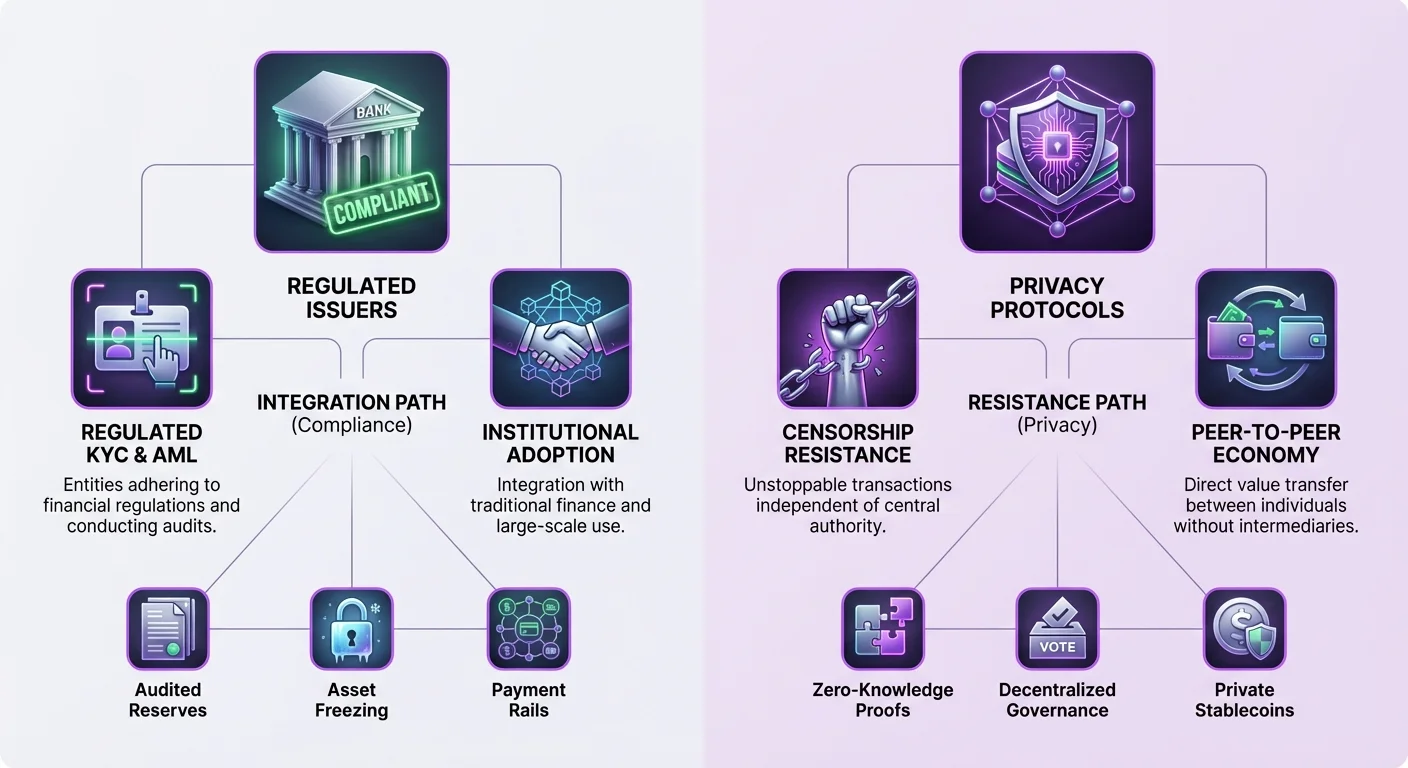

The regulatory future of stablecoins is heavily influenced by their structure. Centralized stablecoins like USDC have positioned themselves as compliant, transparent alternatives. The issuer, Circle, holds reserves in audited cash and short-term government bonds. This strict adherence to US regulations makes USDC attractive to institutions and risk-averse investors who prioritize safety over decentralization.

However, this compliance comes with trade-offs. To operate within US regulatory frameworks, issuers must retain control over the ledger. This includes the ability to blacklist addresses and freeze funds. There are documented instances where law enforcement requested assets be frozen, and compliant issuers fulfilled these requests. For users in jurisdictions with unstable governments or those seeking protection from seizure, this feature is a significant drawback.

Tether (USDT), while also centralized, has historically operated in a grayer regulatory zone. Based in Hong Kong, it has faced long-standing questions regarding the exact composition of its reserves. Despite this, its ubiquity across multiple blockchains and deep liquidity make it the dominant force in the market. Its offshore nature offers a perceived buffer against American regulatory reach, though this also fuels concerns about its long-term safety.

The regulatory pressure on centralized stablecoins is evident in the case of BUSD. Once a top stablecoin issued by Paxos, it faced action from the New York State Department of Financial Services (NYDFS). Paxos was ordered to halt the issuance of new tokens, leading to the gradual phasing out of the asset. This demonstrates that even regulated entities are not immune to sudden shifts in policy or enforcement.

Regulatory Scrutiny of Privacy-Enhancing Technologies

Privacy coins face a different set of regulatory challenges. Governments and financial regulators often view enhanced anonymity with suspicion, citing concerns over money laundering and illicit activities. The ability to transfer wealth without a traceable trail conflicts with global Know Your Customer (KYC) and Anti-Money Laundering (AML) standards. This friction has led to increased scrutiny of privacy-focused projects.

This regulatory pressure often manifests at the exchange level. Many centralized exchanges have delisted privacy coins to remain compliant with local banking regulations. This reduces the liquidity of these assets and makes them harder for the average user to acquire. The "travel rule," which requires exchanges to share customer information for transactions above a certain threshold, is difficult to implement for coins that inherently hide transaction data.

Despite these hurdles, the technology behind privacy coins continues to advance. Projects like Zano utilize hybrid consensus models that combine Proof-of-Work security with Proof-of-Stake efficiency. Zano’s "Zarcanum" protocol introduces hidden-amount Proof-of-Stake, allowing users to stake their coins and secure the network without revealing their wallet balances. This innovation ensures that privacy does not come at the cost of network participation.

Some privacy protocols are exploring "opt-in" compliance features to bridge the gap. For instance, Zano offers auditable wallets, which allow users to selectively reveal transaction data to specific parties, such as auditors or tax authorities. This flexibility could theoretically allow privacy coins to exist within a regulated framework by granting privacy by default while enabling transparency when necessary for legal compliance.

The Convergence: Confidential Assets and Private Stablecoins

A new frontier in the market is the merging of stability and privacy through "confidential assets." These are tokens that operate on privacy-preserving blockchains but represent value from other sources, such as fiat currencies. This hybrid approach attempts to offer the best of both worlds: the stable purchasing power of the US dollar and the censorship resistance of a privacy coin.

Zano’s ecosystem supports the creation of these confidential assets. Tokens issued on this network automatically inherit the privacy features of the underlying blockchain. This means that a stablecoin running on Zano would have hidden amounts, stealth addresses, and ring signatures. Observers would see that a transaction occurred, but they would not know the asset type, the amount, or the participants involved.

The Freedom Dollar (fUSD) is a prime example of this innovation. Launched as a private stablecoin, it is pegged 1:1 to the US dollar but exists as a confidential asset on the Zano blockchain. Unlike centralized stablecoins that rely on bank deposits, fUSD uses an over-collateralized model backed by the native ZANO token. This structure aims to remove the central point of failure and the risk of asset freezing associated with traditional issuers.

By using a decentralized collateral model, projects like Freedom Dollar attempt to bypass the regulatory choke points that centralized stablecoins face. There is no central company to subpoena and no bank account to freeze. The stability is maintained by algorithmic market-making and the value of the collateral reserves. This represents a significant technological leap, offering a tool for financial freedom that is both stable and private.

| Feature | Centralized Stablecoin (USDC) | Privacy Coin (Monero) | Private Stablecoin (fUSD) |

|---|---|---|---|

| Value Basis | Fiat Peg (USD) | Market Value | Fiat Peg (USD) |

| Privacy | Transparent Ledger | Mandatory Privacy | Mandatory Privacy |

| Backing | Fiat Reserves | None (PoW) | Crypto Collateral |

| Control | Issuer Can Freeze | Censorship Resistant | Censorship Resistant |

| Auditability | Centralized Audit | None | On-chain Proofs |

The Role of Governance and Decentralization

The future of these specialized assets is closely tied to their governance models. Decentralized Autonomous Organizations (DAOs) play a crucial role in managing the parameters of decentralized stablecoins and privacy networks. In these systems, token holders vote on protocol upgrades, collateral types, and risk parameters. This shifts control from a corporate boardroom to a distributed community of stakeholders.

For example, the MakerDAO platform, which manages the DAI stablecoin, allows holders of the governance token to vote on stability fees and debt ceilings. This democratic process is designed to ensure the protocol adapts to market conditions without relying on a central authority. However, governance itself can be a vector for regulatory pressure, as seen in discussions about liability for DAO participants.

Zano utilizes a hybrid approach where stakers participate in on-chain governance. Because the staking process is anonymous via Zarcanum, the governance participants are protected from targeted pressure. This anonymity in governance is a vital feature for maintaining true decentralization. If voters can be identified and coerced, the protocol remains vulnerable to external influence.

The evolution of governance tokens also impacts the stability of the ecosystem. In some models, the governance token acts as the backstop for the system. If the stablecoin loses its peg or collateral value drops, the governance token may be minted and sold to recapitalize the system. This aligns the incentives of the community with the health of the protocol, as poor management leads to the devaluation of their own assets.

Future Outlook: Integration vs. Resistance

The path forward for specialized altcoins is bifurcating. On one side, compliant stablecoins are integrating deeper into the global financial infrastructure. We are seeing the rise of "payment stablecoins" like PayPal USD (PYUSD), which are designed to function seamlessly within existing commercial networks. These assets will likely face heavy regulation but will enjoy widespread adoption among merchants and mainstream users.

On the other side, privacy-focused assets and decentralized stablecoins are doubling down on censorship resistance. As governments explore Centralized Bank Digital Currencies (CBDCs), the demand for private alternatives is expected to grow. CBDCs offer governments unprecedented visibility into financial transactions, potentially driving privacy-conscious individuals toward assets like Zano and Monero.

The emergence of privacy-preserving stablecoins like fUSD presents a unique challenge to regulators. They offer the utility of digital cash—stable and private—without the volatility that has historically hindered crypto adoption for payments. If these assets gain significant traction, they could force a re-evaluation of how financial regulations apply to decentralized code.

Ultimately, the market may settle into a two-tiered system. Regulated, transparent stablecoins will serve institutional and high-value commercial needs, acting as the "checking accounts" of the crypto world. Meanwhile, decentralized privacy assets will serve as the "digital cash," utilized by those prioritizing sovereignty, anonymity, and protection from overreach. The interplay between these two sectors will define the liquidity and freedom of the future digital economy.

Conclusion

The regulatory future of stablecoins and privacy coins is being shaped by the fundamental tension between state oversight and individual financial sovereignty. Centralized stablecoins have chosen the path of compliance, offering transparency and integration with traditional banking at the cost of censorship resistance. This makes them safe for institutional adoption but vulnerable to government intervention. Conversely, privacy coins and decentralized stablecoins prioritize the protection of user data and the immutability of the ledger, accepting the risks of regulatory friction and reduced exchange access.

Innovations like confidential assets and private stablecoins are blurring the lines between these categories, creating powerful new tools that offer both stability and anonymity. These hybrid technologies represent the next battleground for financial freedom, challenging the notion that one must choose between a stable currency and a private one. As the technology matures, the ability of these protocols to remain decentralized and resistant to capture will be their defining characteristic in an increasingly regulated world.

True financial freedom requires the ability to transact privately using a currency that retains its purchasing power over time.