Decentralized finance has fundamentally changed how individuals interact with their digital assets. In the traditional banking world, keeping money in a savings account earns a minimal amount of interest. The bank lends those funds out at a much higher rate and keeps the vast majority of the profit. The depositor, who provided the capital, sees very little return on their investment. DeFi lending flips this model by removing the intermediary institution entirely.

Instead of depositing money into a bank, crypto holders deposit assets into smart contracts. These are automated programs running on a blockchain. Borrowers interact directly with these contracts to take out loans, and they pay interest for this privilege. This interest goes directly back to the lenders who supplied the liquidity. It creates a more efficient market where the providers of capital capture the majority of the yield. This process turns a stagnant crypto portfolio into a productive one.

For anyone holding Bitcoin, Ethereum, or stablecoins, this presents a method to generate passive income. The assets do not need to be sold. They simply need to be moved into a protocol that facilitates these lending and borrowing markets. While the concept sounds complex, the actual process has become streamlined through modern web3 wallets and user-friendly interfaces. The barriers to entry have lowered significantly.

This guide explores the specific mechanics of how to participate in this ecosystem. It covers the necessary tools, the setup process, and the routine management required to maintain a healthy lending position. By understanding the infrastructure of DeFi, users can make informed decisions about where to deploy their capital.

Understanding the Mechanics of DeFi Lending

The core innovation of decentralized lending is the liquidity pool. In a traditional peer-to-peer loan, a lender would need to find a specific borrower who wants the exact amount they have to offer. They would also need to agree on a duration and an interest rate. This matching process is slow and inefficient. DeFi protocols solve this by pooling assets together.

The Liquidity Pool Model

When you lend in DeFi, you do not lend to a specific person. Instead, you deposit your cryptocurrency into a massive pool of funds managed by a smart contract. This pool is open to anyone who wishes to supply liquidity. Because all the funds are aggregated, the pool becomes a deep reservoir of capital. This structure ensures that there is almost always liquidity available for borrowers and lenders alike.

Borrowers draw funds from this pool rather than from an individual. They can borrow any amount up to the limits of the pool's liquidity and their own collateral. This model allows for instant transactions. A lender can deposit funds at 3:00 AM on a Sunday, and a borrower can take a loan seconds later. There is no manual approval process or waiting period. The code governs the entire flow of funds based on pre-set rules.

How Yield is Generated

The interest rate in these protocols is not fixed by a central authority. It is determined by supply and demand dynamics. When a lot of people want to borrow a specific asset but there is not much supply in the pool, the interest rate rises. This high rate encourages more lenders to deposit funds to capture the yield. Conversely, if the pool is full of cash but nobody is borrowing, the rates drop to encourage borrowing.

As a lender, your passive income comes from the interest payments made by these borrowers. The smart contract collects the interest and distributes it pro-rata to everyone who has deposited into the pool. If you provided 1% of the liquidity in the pool, you receive 1% of the interest collected. This distribution happens continuously, often block by block, allowing your balance to grow in real-time.

Essential Prerequisites for Lending

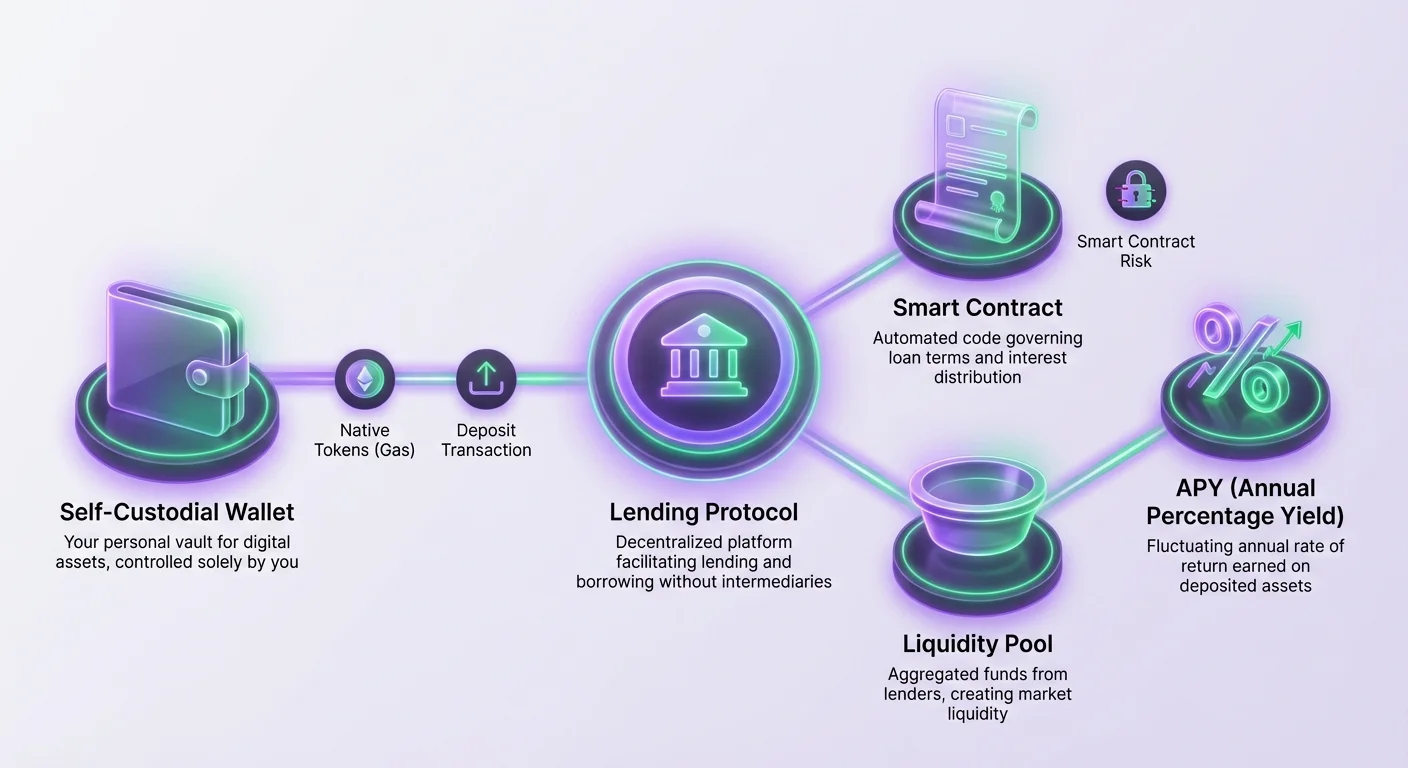

Before interacting with any DeFi protocol, you must have the correct infrastructure in place. The requirements are distinct from traditional finance. You do not need a credit score, a bank account, or proof of identity. The system is permissionless. However, you do need three specific technical components to get started: a digital wallet, cryptocurrency, and a connection to a lending platform.

The digital wallet acts as your interface and your identity. It stores your private keys, which are necessary to approve transactions. For DeFi, you specifically need a self-custodial wallet. This means you are the only person with access to the funds. Custodial wallets, like those found on centralized exchanges, essentially hold the keys on your behalf. While convenient for trading, they often cannot interact directly with decentralized applications (dApps).

You also need the correct type of cryptocurrency. First, you need the asset you intend to lend, such as USDC or ETH. Second, and equally important, you need the blockchain's native currency to pay for transaction fees. These fees, often called "gas," pay the network validators to process your deposit. On Ethereum, this is ETH. On Avalanche, it is AVAX. Without a small balance of the native token, you cannot execute any smart contract interactions.

Setting Up Your Web3 Wallet

The foundation of all DeFi activity is the web3 wallet. This software allows you to communicate with blockchain networks. Modern wallets are often available as mobile apps or browser extensions. The setup process focuses heavily on security, as there is no customer support to reset a password if you lose access.

Installation and Security Measures

When you create a new self-custodial wallet, the software generates a "seed phrase" or "recovery phrase." This is usually a list of 12 to 24 random words. This phrase is the master key to your funds. It is imperative to write this down physically and store it in a secure location. Do not take a screenshot or save it in a text file on an internet-connected device.

If your phone breaks or you delete the app, this seed phrase is the only way to recover your wallet. Anyone who has this phrase can access your funds from anywhere in the world. Once the wallet is installed and backed up, it acts as your personal vault. You do not need to provide an email address or phone number. The wallet addresses are generated mathematically from your seed phrase.

Funding the Wallet

Once your wallet is active, you must fund it. You can purchase cryptocurrency directly within many wallet apps using a credit card, or you can transfer funds from a centralized exchange. Ensure you are sending the assets to the correct network address. Sending Bitcoin to an Ethereum address, for example, can result in a permanent loss of funds.

If you plan to lend on a network like Ethereum, you must hold ETH in the wallet to cover the costs of sending your deposit to the lending pool. If you are using a Layer 2 network or a different blockchain like Polygon, you would need MATIC. A common mistake for beginners is depositing all their funds into the lending protocol and leaving zero ETH in their wallet. This leaves them "stuck" because they cannot pay the gas fee required to withdraw their earnings later.

Choosing the Right Protocol

Not all lending platforms are created equal. Since you are trusting a smart contract with your money, the reliability of that code is paramount. A reputable lending platform typically has a high Total Value Locked (TVL). This metric indicates how much capital other users have entrusted to the system. A high TVL generally suggests that the protocol has been battle-tested over time and is trusted by the wider community.

Users should look for platforms that have undergone rigorous security audits. An audit involves external security experts reviewing the code to find vulnerabilities. While an audit does not guarantee 100% security, it is a baseline requirement for any serious DeFi project. Leading protocols operate on multiple blockchains, giving users choices regarding transaction fees and speed. Aave, for example, is a prominent decentralized application that operates across markets like Ethereum and Avalanche.

The Deposit Process Walkthrough

Once your wallet is ready and you have selected a protocol, the actual lending process involves a few distinct steps. This interaction occurs directly between your wallet and the application's website. It is a permissionless action, meaning no human on the other end reviews your request.

Connecting to the DApp

Navigate to the lending platform's website using the browser inside your wallet app or a desktop browser with an extension. Look for a "Connect" button. This initiates a handshake between the website and your wallet. You may see an option for "WalletConnect," which is an open protocol for connecting mobile wallets to dApps.

If using WalletConnect, a QR code typically appears on the desktop screen. You scan this code with your mobile wallet app. A prompt will appear on your phone asking for permission to connect. Approving this does not spend any money; it simply allows the website to see your public address and your balances so it can display the correct interface.

Approving and Depositing

Before you can deposit a specific token (like USDC), you must first "Approve" the protocol to spend that token. This is a security feature of the blockchain standard. You will see a button labeled "Approve." Clicking this triggers a transaction in your wallet. You must review the gas fee and confirm the action. This grants the smart contract permission to move the specific amount of tokens you designate.

After the approval transaction is confirmed on the blockchain, the "Deposit" or "Supply" button will become active. Enter the amount you wish to lend. Clicking this triggers a second transaction. This is the actual transfer of assets from your wallet to the lending pool. Once this transaction is confirmed, your assets leave your wallet and enter the protocol. In return, you often receive a placeholder token that represents your deposit and the accrued interest.

Monitoring and Managing Your Position

After depositing, your role shifts to monitoring. Most lending protocols provide a dashboard where you can view your deposited balance. You should see your balance increasing over time as interest accrues. This interest is usually compounded, meaning you earn interest on your interest. The rate of return is expressed as APY (Annual Percentage Yield).

| Metric | Definition | Importance |

|---|---|---|

| APY | Annual Percentage Yield | Shows total return including compounding |

| TVL | Total Value Locked | Indicates protocol liquidity and health |

| LTV | Loan to Value | Critical if you use deposits as collateral |

It is important to understand that APY is rarely static in DeFi. It fluctuates based on market conditions. If a sudden wave of liquidity enters the pool, rates might drop. If borrowers demand more capital, rates will rise. Checking your dashboard periodically helps you decide if the current rate is still attractive or if you should move your funds elsewhere.

You do not need to claim interest manually in most modern protocols. The underlying balance of your claim simply grows. For example, if you deposited 100 tokens and earned 1% interest, the protocol now recognizes that you are entitled to 101 tokens. The dashboard reflects this updated value automatically.

Withdrawing Assets and Risks

One of the primary benefits of DeFi lending is flexibility. Unlike a Certificate of Deposit (CD) at a bank, there are typically no lock-up periods. You can withdraw your funds at any moment, provided there is sufficient liquidity in the pool. However, the exit process requires care, especially if you have utilized other features of the protocol.

The Withdrawal Process

To get your money back, navigate to the dashboard where your deposits are listed. There will be a "Withdraw" option. You can choose to withdraw a portion or the entirety of your balance. Just like the deposit, this requires a blockchain transaction. You will need to pay a gas fee to process this request.

If the network is congested, gas fees might be high. It is often wise to wait for a time when the network is less busy to withdraw, maximizing your profit. Once the transaction confirms, the assets—plus the interest earned—are returned to your self-custodial wallet. You can then swap them, hold them, or move them to a different protocol.

Understanding the Risks

While the code is automated, risks exist. The most prominent is "smart contract risk." This is the chance that a bug in the code could be exploited by a hacker to drain the funds. This is why choosing established protocols with high TVL and audits is crucial.

Another risk involves "liquidity utilization." If 100% of the funds in the pool are currently borrowed out, you cannot withdraw until some borrowers repay their loans or new lenders enter. While rare in major protocols, it is theoretically possible.

Additionally, users must be extremely careful if they use their deposited assets as collateral to borrow other assets. If the value of your collateral drops significantly, the protocol may liquidate your deposit to pay back the loan. If you are only lending and not borrowing, this specific liquidation risk does not apply to you, making "lend-only" a safer strategy for beginners.

Conclusion

DeFi lending offers a powerful alternative to traditional savings methods, placing the power of banking directly into the hands of the individual. By leveraging smart contracts and liquidity pools, crypto holders can transform idle assets into productive capital. The process requires a shift in mindset—from trusting a bank manager to trusting open-source code and personal security practices.

Success in this space relies on careful preparation. Setting up a secure self-custodial wallet, keeping your recovery phrase safe, and maintaining a balance of native tokens for gas fees are non-negotiable steps. Selecting reputable protocols like Aave ensures you are operating on a foundation of examined and tested infrastructure.

While the yields can be attractive, they come with responsibilities. You must monitor your positions, understand the fluctuating nature of APY, and remain aware of the technical risks involved. With diligence and the right tools, participating in decentralized finance provides a transparent and accessible way to earn yield on the blockchain.

True financial sovereignty begins when you control both your assets and the yield they generate.