Bitcoin’s ascent to significant valuation levels has created a psychological barrier for many potential investors. When the price of a single whole unit reaches tens of thousands of dollars, it can feel unattainable for the average individual. This perception often leads newcomers to believe they have missed the boat or that the asset is exclusively for the wealthy. However, this view stems from a fundamental misunderstanding of how the digital currency works.

Unlike physical assets or even traditional stocks which often trade in whole units, digital currencies are highly divisible. The system was designed from the inception to handle micro-transactions and fractional ownership. You do not need to purchase a whole unit to participate in the network. In fact, the vast majority of network participants own fractions of a coin rather than whole ones.

This divisibility allows for specific investment strategies that focus on gradual accumulation rather than large, lump-sum purchases. By understanding the denomination of the currency and the mechanics of accumulation, investors can build significant positions over time. This approach shifts the focus from the intimidating price of a whole coin to the accessible goal of accumulating smaller subunits.

The Mechanics of Divisibility

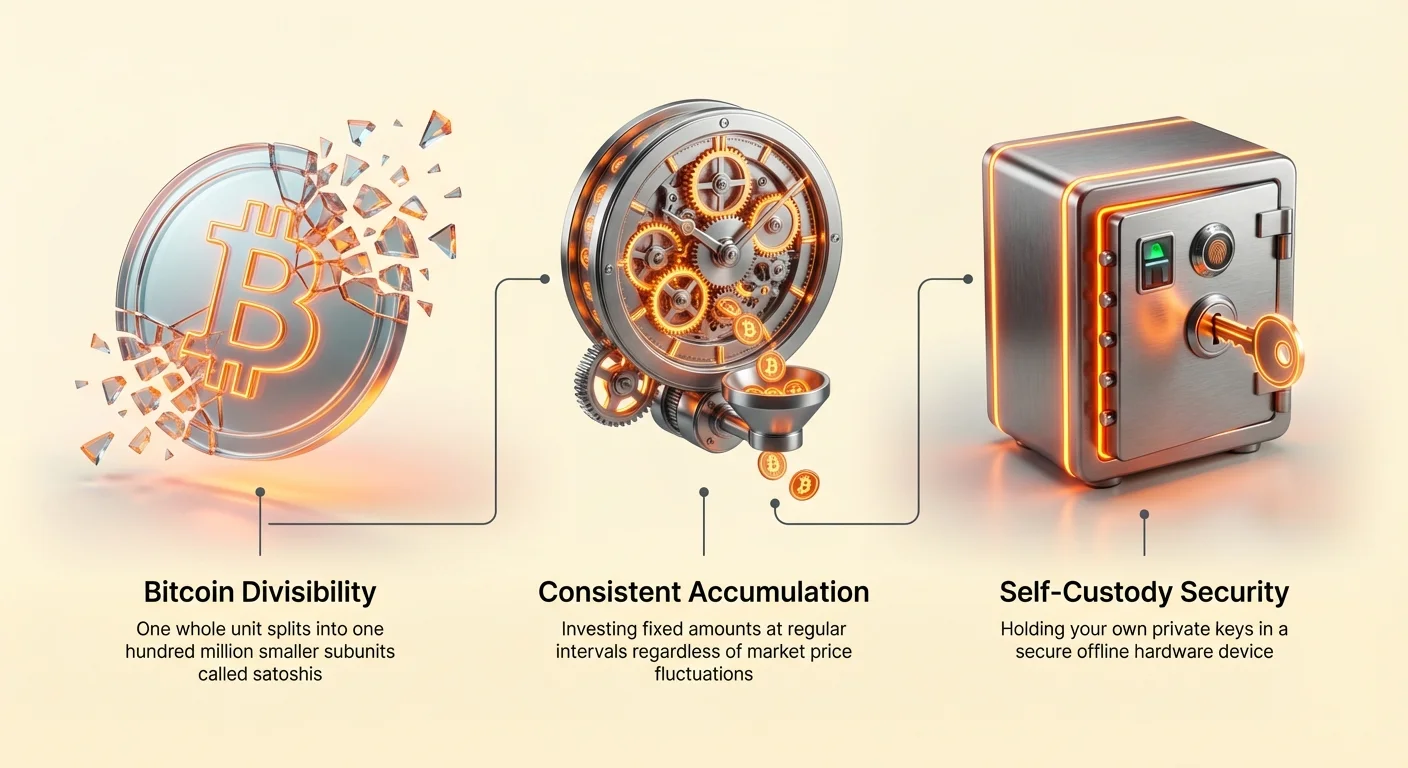

The architecture of Bitcoin allows for extreme precision in value transfer. A single bitcoin is not the base unit of the system; rather, it is a convention used for display. The protocol itself operates on a much smaller unit known as a "satoshi," named after the pseudonymous creator of the network. There are 100 million satoshis in a single bitcoin.

This relationship is similar to dollars and cents, but with much greater granularity. While a dollar is divisible into 100 cents, a bitcoin is divisible into 100,000,000 units. This means that even if the price of a whole bitcoin were to reach one million dollars, a single satoshi would still be worth a mere penny.

| Unit Name | Value in BTC | Value in Satoshis |

|---|---|---|

| Bitcoin | 1.00000000 | 100,000,000 |

| Bit (µBTC) | 0.00000100 | 100 |

| Satoshi | 0.00000001 | 1 |

Understanding this denomination is crucial for adopting the right mental model for accumulation. When you purchase $50 worth of the asset, you are not buying a "fragment" in a derogatory sense; you are purchasing potentially hundreds of thousands of satoshis. This shift in perspective is often referred to as "stacking sats."

Overcoming Psychological Unit Bias

Human psychology plays a significant role in financial decision-making. One specific cognitive quirk relevant to crypto markets is "unit bias." This is the predisposition to prefer whole units over fractional ones. People naturally derive more satisfaction from owning 1,000 units of an asset priced at $1 than owning 0.05 units of an asset priced at $20,000, even if the total value is identical.

This bias often leads inexperienced investors toward high-risk assets solely because they have a low price per coin. They might believe that a coin costing $0.01 has a better chance of doubling than a coin costing $50,000. This is a fallacy. The market capitalization and liquidity of the asset are far more important metrics than the unit price.

By denominating holdings in satoshis rather than whole bitcoins, investors can bypass this psychological hurdle. Instead of seeing a balance of 0.005 BTC, which feels small, an investor can view it as 500,000 satoshis. This framing aligns with the human desire for whole numbers and large quantities, making the accumulation process more satisfying and sustainable.

Implementing Dollar-Cost Averaging

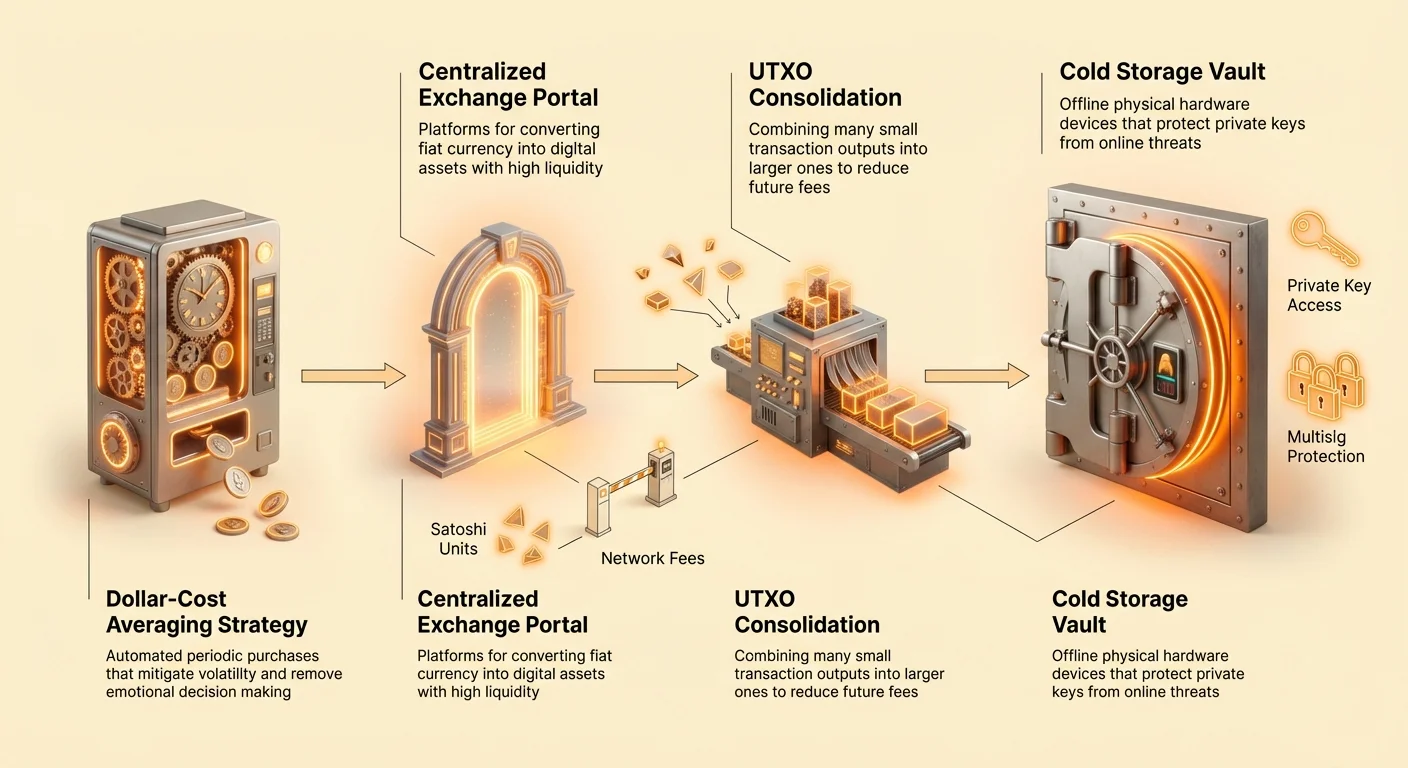

Dollar-Cost Averaging (DCA) is an investment strategy where an individual divides the total amount to be invested across periodic purchases. This is particularly effective for acquiring satoshis. instead of trying to time the market or waiting to save a large lump sum, an investor commits to buying a fixed dollar amount at regular intervals—weekly, bi-weekly, or monthly.

This strategy serves two primary purposes. First, it mitigates the impact of volatility. By buying regularly regardless of price, investors purchase more units when prices are low and fewer units when prices are high. Over time, this averages out the cost basis of the investment.

Second, it instills discipline. The emotional stress of watching price charts is removed. The goal becomes accumulation of units (sats) rather than monitoring the daily fiat value of the portfolio. Whether the market is up or down, the accumulator continues to increase their stack of satoshis. This consistent buying pressure, when adopted by many, creates a robust base of long-term holders.

Strategies for Buying and Accumulation

The pathway to acquiring digital assets has evolved significantly, offering multiple venues for accumulation. Choosing the right platform depends on a balance between convenience, privacy, fees, and control. For those engaging in DCA, minimizing friction and fees is paramount to long-term success.

Centralized Exchanges and Brokerages

Centralized exchanges (CEXs) act as intermediaries, similar to traditional stock brokerages. Users create accounts, verify their identity through Know Your Customer (KYC) regulations, and link banking methods. These platforms generally offer high liquidity, meaning it is easy to buy or sell large amounts without affecting the price.

For a beginner, exchanges offer the most familiar user experience. They typically provide custodial wallets, meaning the exchange holds the keys to the funds on behalf of the user. While convenient for buying, keeping funds on an exchange long-term introduces counterparty risk. If the exchange fails or is hacked, user funds can be lost.

When using an exchange for DCA, it is critical to look at withdrawal fees. Some exchanges charge high flat fees to move funds off the platform. If you are buying small amounts frequently, these withdrawal fees can eat into your accumulated stack. A common strategy is to buy on the exchange regularly but only withdraw to a private wallet once the balance reaches a certain threshold.

Peer-to-Peer and Decentralized Options

Peer-to-Peer (P2P) platforms connect buyers directly with sellers. These marketplaces can offer greater privacy and a wider variety of payment methods, including cash in person or bank transfers. Because trades occur directly between individuals, P2P options can sometimes bypass the strict identity verification requirements of centralized exchanges.

However, P2P trading often comes with a premium over the market price and requires vigilance against scams. Reputation systems are essential in these environments; buyers should look for sellers with a strong history of completed trades and positive feedback.

For accumulators who value privacy, buying via P2P reduces the data trail associated with their holdings. This method is often slower and less convenient than clicking a "buy" button on an app, but it adheres closer to the decentralized ethos of the network. It requires the user to be more hands-on with the security of their transaction.

Fees and Cost Considerations

Every purchase method incurs costs that must be factored into an accumulation strategy. These costs generally fall into three categories: exchange fees, network fees, and spread. Exchange fees are charged by the service provider for facilitating the trade. Spread is the difference between the buying and selling price; some "fee-free" services hide their costs here.

Network fees are paid to miners to process transactions on the blockchain. When you buy on a centralized exchange, the transaction usually happens off-chain within the exchange's internal ledger, avoiding network fees at the moment of purchase. However, when you eventually withdraw your satoshis to your own wallet, a network fee will be incurred.

Smart accumulation involves optimizing these costs. For example, making daily purchases might be inefficient if the platform charges a fixed fee per transaction. Adjusting the frequency to weekly or monthly can reduce the percentage of capital lost to fees. Similarly, monitoring network congestion can help in timing withdrawals to minimize mining fees.

Tehnička strana akumulacije: UTXO

Razumevanje osnovne strukture transakcija je vitalno za svakoga ko akumulira bitcoin tokom dugog perioda. Mreža koristi model poznat kao Neiskorišćeni izlaz transakcije (UTXO). Ovaj koncept se razlikuje od modela baziranih na nalogu koje koriste tradicionalne banke.

Kako UTXO funkcionišu

Kada primate transakciju, ne samo što povećavate broj u bazi podataka. Primajte diskretan „komad“ digitalne valute, slično primanju fizičke novčanice u gotovini. Ako kupite 0,01 BTC deset puta, vaš novčanik ne drži samo 0,1 BTC; drži deset odvojenih „novčanica“ ili UTXO, svaka vredna 0,01 BTC.

Kada kasnije odlučite da potrošite ili premestite svoju 0,1 BTC, vaš novčanik mora prikupiti ovih deset odvojenih ulaza da konstruiše transakciju. U digitalnom dnevniku, veličina transakcije se meri u podacima (bajtovima), a ne u dolarskoj vrednosti. Transakcija koja kombinuje deset ulaza zauzima značajno više prostora podataka nego transakcija koja koristi jedan ulaz.

Trošak prašine

Za investitore u DCA, UTXO model predstavlja specifičan izazov. Česte male povlačenja sa berze u privatni novčanik stvaraju veliki broj malih UTXO. Ovo se često naziva „prašina“ ako su iznosi vrlo mali.

Kada su naknade mreže visoke, trošak potrošnje ovih malih UTXO može postati preteran. Na primer, ako imate UTXO vredan 10 dolara, ali naknada mreže da uključite taj ulaz u transakciju iznosi 5 dolara, efektivno gubite 50% vaše vrednosti samo pokušavajući da ga premestite. U ekstremnom zagušenju, naknada može premašiti vrednost UTXO, čineći ga neprovodivim.

Strategije konsolidacije

Da bi se ublažio nadimanje UTXO, akumulateri treba da pažljivo upravljaju svojim povlačenjima. Umesto povlačenja svake pojedinačne kupovine odmah, investitori mogu pustiti da se fondovi akumuliraju na berzi dok ne dostignu veći iznos, možda 0,01 BTC ili više, pre povlačenja. Ovo stvara jedan veći UTXO u privatnom novčaniku umesto mnogo malih.

Alternativno, korisnici mogu izvršiti transakcije „konsolidacije“ tokom perioda niske aktivnosti mreže. Ovo podrazumeva slanje celog salda sebi na novu adresu unutar sopstvenog novčanika. Ova akcija uzima sve male ulaze i kombinuje ih u jedan novi, veliki izlaz. Radom ovoga kada su naknade niske, pripremate svoj sklad za buduće potrošnje bez brige o visokim troškovima podataka kasnije.

Skladištenje: Osnova vlasništva

Mantra „ne tvoji ključevi, ne tvoji novčići“ je centralna za filozofiju kriptovalute. Akumulacija satoshija je samo polovina bitke; njihovo osiguravanje je druga polovina. Novčanik nije uređaj za skladištenje novčića, već upravljač ključevima. Čuva privatne ključeve koji vam omogućavaju da ovlaštite transakcije na blockchainu.

Softverski novčanici (vrući novčanici)

Softverski novčanici su aplikacije koje rade na mobilnim uređajima ili desktop računarima. Često se nazivaju „vrućim novčanicima“ jer su povezani na internet. Ovi su zgodni za manje iznose i svakodnevno potrošnju. Omogućavaju brzo slanje i primanje, često koristeći QR kodove za deljenje adrese.

Međutim, pošto postoje na opštim računarskim uređajima, ranjivi su na malver i online napade. Za strategiju akumulacije, softverski novčanik je odlična polazna tačka ili privremeno mesto za čekanje. Omogućava lako praćenje salda i brzu verifikaciju primljenih fondova.

Prilikom biranja softverskog novčanika, samokustodija je nepregovorna. Samokustodijalni novčanik osigurava da samo korisnik poseduje privatne ključeve ili fraze za oporavak. Ako pružalac novčanika nestane, korisnik može jednostavno vratiti svoje fondove koristeći frazu za oporavak na drugom softveru.

Hardverski novčanici (hladno skladištenje)

Za dugoročnu akumulaciju, hardverski novčanici su zlatni standard. Ovo su fizički uređaji, često slični USB memorijama, koji čuvaju privatne ključeve offline. Nikada nisu direktno povezani na internet, čak ni kada su priključeni na računar. Kada je transakcija potrebna, nepotpisana transakcija se šalje na uređaj, potpisuje interno privatnim ključem, a zatim se potpisana transakcija vraća računaru da se emituje.

Ova izolacija štiti ključeve od hakera, keyloggera i malvera za snimanje ekrana. Za nekoga ko slaže satoshije godinama, ulaganje u hardverski novčanik je mala premija osiguranja za bezbednost njihove imovine. Deluje kao lični sef koji je imun na vektore digitalne krađe koji pogađaju uređaje povezane na internet.

Deljeni i multisig novčanici

Kako akumulirani sklad raste značajno, novčanici sa jednim potpisom mogu predstavljati jednu tačku kvara. Ako se privatni ključ izgubi ili ukrade, fondovi su nestali. Multisig novčanici rešavaju ovo zahtevajući više ključeva za ovlašćenje transakcije.

Uobičajena konfiguracija je „2-of-3“ postavka. Generišu se tri ključa; jedan može biti držan na hardverskom novčaniku, jedan na telefonu, a jedan na sigurnom fizičkom mestu ili kod pouzdanog člana porodice. Da bi se premestili fondovi, dva od tri ključa moraju potpisati transakciju. Ova struktura pruža redundanciju. Ako se jedan ključ izgubi, fondovi se još uvek mogu oporaviti sa preostala dva. Ako se jedan ključ ukrade, lopov ne može ukrasti fondove bez drugog ključa.

| Karakteristika | Novčanik sa jednim potpisom | Multisig novčanik |

|---|---|---|

| Podešavanje | Jednostavno | Napredno |

| Bezbednost | Umjereno | Visoka |

| Oporavak | Rizik od gubitka ključa | Redundantni ključevi |

Najbolje prakse bezbednosti

Odgovornost da budete svoja banka zahteva strogo poštovanje protokola bezbednosti. Najkritičniji element je backup privatnog ključa, obično predstavljen kao fraza za oporavak od 12 do 24 reči. Ova fraza mora biti zapisana na fizičkom mediju, kao što su papir ili metal, i sigurno čuvana.

Nikada ne čuvajte ovu frazu za oporavak digitalno. Ne pravite fotografiju, ne čuvajte je u cloud belešci i ne šaljite je sebi e-mailom. Digitalne kopije su podložne hakovanju. Ako napadač dobije pristup vašem cloud skladištu ili e-mailu, može istog trenutka isprazniti vaš novčanik.

Pazite na phishing pokušaje. Prevaranti često kreiraju lažne veb-sajtove ili šalju e-mailove predstavljajući se kao timovi podrške novčanika. Traziće vašu frazu za oporavak da „verifikuju“ ili „otključaju“ vaš nalog. Legitimni pružaoci novčanika nikada neće tražiti vašu frazu za oporavak. To je glavni ključ vaših fondova, a otkrivanje njega daje potpunu kontrolu onome ko ga poseduje.

Zaključak

Strategija akumulacije satoshija kroz prosečno ulaganje dolara je moćna metoda za izgradnju bogatstva u prostoru digitalnih imovina. Zaobilazi potrebu za savršenim vremenskim određivanjem tržišta i koristi ekstremnu deljivost valute da učini investiranje dostupnim svima. Fokusiranjem na „stacking sats“ umesto kupovine celih novčića, investitori mogu prevazići psihološke barijere i održavati stabilan napredak bez obzira na akciju tržišnih cena.

Međutim, akumulacija je efikasna samo kada je uparena sa robusnim praksama bezbednosti. Razumevanje tehničkih nijansi izlaza transakcija i naknada osigurava da akumulirano bogatstvo ostane trošivo i efikasno. Premještanje fondova u samokustodijske novčanike, posebno hardverske uređaje ili multisig postavke, štiti investiciju od sistemskih rizika i krađe. Put akumulacije je put discipline, obrazovanja i lične odgovornosti.

Dosledna akumulacija malih iznosa, kombinovana sa sigurnim samokustodijom, gradi dugoročnu finansijsku suverenost i štiti od volatilnosti tržišta.